Summary

Summary

- This The Bank of Nova Scotia Stock Analysis is the fifth of a 6 part series covering the Big 6 Canadian Banks.

- BNS reported Q2 2017 results May 30th and its Liquidity Ratios continue to be strong thus providing investors with assurances that an investment in the bank is relatively safe.

- BNS is Canada’s most international bank and its geographical diversification provides it with a superior ability than some of its peers to weather a financial storm.

- Pockets of the Canadian real estate market are wildly overheated but BNS is an extremely prudent lender and it actually started dialing back its new mortgage business in 2016.

- BNS is an attractive long-term investment with a solid dividend payment history.

- I suspect we will experience a major market correction within the next 12 months and urge caution.

All figures are expressed in Canadian dollars unless otherwise noted.

Introduction

The Bank of Nova Scotia (NYSE: BNS), Canada’s 3rd largest bank by market cap, reported Q2 2017 results on May 30th. A link to the Earnings release can be found below in the Q2 2017 Financial Results section of this post.

Fast facts about BNS can be found here.

BNS Q2 2017 Financial Performance Overview

While I touch upon various topics that impact the Canadian Banking Sector and the top 6 Schedule I Canadian Banks, I strongly encourage you to listen to the BNS segment of the March 29 and 30, 2017 National Bank Financial Markets – 15th Annual Financial Services Conference where Sean McGuckin (Group Head and CFO) discusses a wide range of topics. There is far too much information covered in this ~30 minute segment for me to give the content justice in this post.

The Canadian Banking Sector

Details on the Canadian Banking Sector can be found here.

Technological Innovation

Details about the Technological Innovation the Canadian banks are undertaking can be found here.

BNS Overview

Canada is celebrating its 150th anniversary in 2017 but BNS was founded in Halifax, Nova Scotia in 1832 (185 years ago). BNS’s historical timeline can be found here. BNS has certainly come a long way since its very early days when, in 1869, deposits hit the $1 million mark for the first time in the bank’s history!

Scotia Mocatta, one of the world’s top bullion dealers in precious and base metals trading, financing, hedging and physical metals distribution was founded in 1671!

BNS’s international presence started in 1889 when it established an agency in Jamaica to provide a place for merchants engaged in the business of trading salt fish, lumber, and potatoes for Jamaican rum and molasses to barter trade on a monetary basis. In so doing this, BNS became the first Canadian Bank to open in the West Indies, and the first Canadian Bank with a foreign operation outside of the United States or the United Kingdom.

Over the years, BNS has continued to expand its international operations. While its Canadian counterparts have decided to focus on penetrating the US market, BNS has made a strategic decision not to enter the US market but rather to focus on expanding in Latin America, the Caribbean and Central America. The reasons for this are:

- The US market is highly saturated.

- There are much larger US competitors which are deeply entrenched and which are much less risk averse than BNS. This would make it extremely difficult for BNS to achieve a market share which would place it in the top 5.

- Margins on loans and deposits in the US are razor thin in comparison to what can be achieved in the markets where BNS has decided to focus.

- The demographic trends in Mexico, Peru, Chile, and Colombia are such that you have a growing young population and where wealth levels are improving.

Acquisitions and Divestitures

If you are looking for an interesting read on how/why BNS made so many acquisitions under former CEO Rick Waugh, read here. Several acquisitions during his tenure have worked out phenomenally well….even acquisitions that were doomed from the start such as the CI Financial acquisition.

Tangerine

One of BNS’s most recent notable acquisitions in Canada was the acquisition of ING’s Canadian banking operations in 2012; this entity was subsequently renamed Tangerine.

While Tangerine is part of the BNS Canada family of companies, the bank has made the deliberate decision to let it operate as an independent brand. In my opinion, this has been a shrewd decision. Typically, an acquirer will want the entity it has acquired to adapt and conform. In some cases the superior services and service levels get lost when the acquired company is forced to conform.

When this happens, some of the reasons the acquired company’s clients choose to deal with the acquired company suddenly disappear; this can be the impetus for these clients to seek other service providers. In the case of Tangerine, BNS’s senior management has had the sense not to change something that is working well.

CI Financial Corp.

At the height of the Financial Crisis, Sun Life Financial unloaded its ownership interest in CI Financial Corp. to BNS. Absolutely no synergies were derived by reason of this acquisition as members of senior management at both companies had an acrimonious relationship. See here and here and here to see just how bad things were.

In Q3 2014, BNS sold a majority of its holding in CI Financial Corp. resulting in a $0.643B pre-tax gain ($0.555B after tax), or $0.45/share. This included an unrealized gain of $0.174B pre-tax, or

$0.152B after tax, on the reclassification of the BNS’s remaining investment to available-for-sale securities. Not a bad return for a relationship that was doomed from the start!

DundeeWealth

DundeeWealth needed a savior at the height of the Financial Crisis. In September 2007, BNS stepped up to the plate and acquired and 18% stake in the firm.

In early February 2011, BNS acquired the remainder of DundeeWealth it did not own.

In 2013, DundeeWealth was renamed HollisWealth.

In late 2016, BNS and Industrial Alliance entered into an agreement wherein Industrial Alliance would acquire HollisWealth from BNS with the transaction expected to close in Q3 2017.

Banco Colpatria

Colombia is one of the countries in which BNS wants to have a strategic presence. In this regard, BNS acquired a 51% stake Banco Colpatria in 2011. More information can be found here. At the time of this acquisition, Brian Porter (BNS’s current CEO) was BNS’s Group Head of International Banking.

Other Strategic Acquisitions or Alliances

A few of BNS’s other strategic acquisitions or alliances include BNS’s and Cencosud’s strategic alliance in Chile, BNS’s strategic partnership with Canadian Tire, BNS’s lengthy relationship with Cineplex, BNS’s heavy presence in pro hockey, BNS’s strategic partnership with CARA, BNS’s acquisition of Citibank’s credit card portfolios in Panama and Costa Rica, and its acquisition of Citibank’s credit card operations in Peru.

In November 2013, BNS’s current CEO (Brian Porter) took over at the helm. Noticeable changes came about almost immediately. First and foremost, senior executives who were extremely loyal to the former CEO were suddenly no longer with the bank (including senior executives who had been gunning for the CEO position).

Then, the long overdue shrinking of the pyramid began; BNS was notorious for not making wholesale personnel changes like its Canadian and US counterparts (there were pros and cons to this). With the departure of a number of senior executives, roles were combined and where there may have been X positions at a certain job level, that job level suddenly had a fraction of the number of positions. This consolidation has been trickling down the pyramid subsequent to Brian Porter stepping into the role of CEO.

Having been Group Head of International Banking at one time, Brian Porter most likely realized that BNS no longer had any logical reason to be in some of the markets in which it had a presence or in which it was looking to establish a presence. While the acquisitions / proposed acquisitions may have made some sense at the time they were made, things just did not materialize as planned. Here are some examples:

BNS buys stake of Chinese bank in 2011

Scotiabank backs away from Chinese bank stake

Scotiabank plans Taiwan exit as Asia revamp continues

In December 2015, BNS indicated it was mulling the partial or full sale of its 49% interest in Thanachart Bank in Thailand. As part of its focus on expansion in Latin America, these plans were shelved in 2017 when BNS decided it was still committed to its long-term investment in Thanachart Bank.

Most recently, BNS has reached an agreement to sell its Malaysian operations to Cathay Financial.

In addition to the strategic realignment of operations over the years, BNS exited other markets through the closure of its rep offices in Russia and Turkey.

Essentially, BNS is now much more focused. It will continue to grow its business in Canada and rather than “throwing mud at the wall to see what sticks” it is strategically expanding its presence in specific countries within Central and South America.

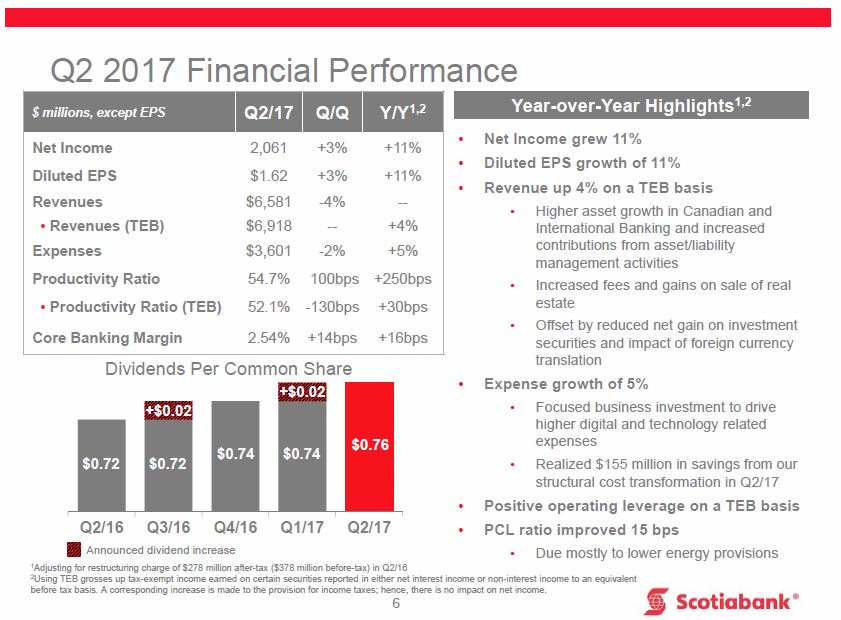

Q2 2017 Financial Results

Readers are encouraged to review BNS’s May 30, 2017 Earnings Release, Earnings Presentation, and to listen to the conference call.

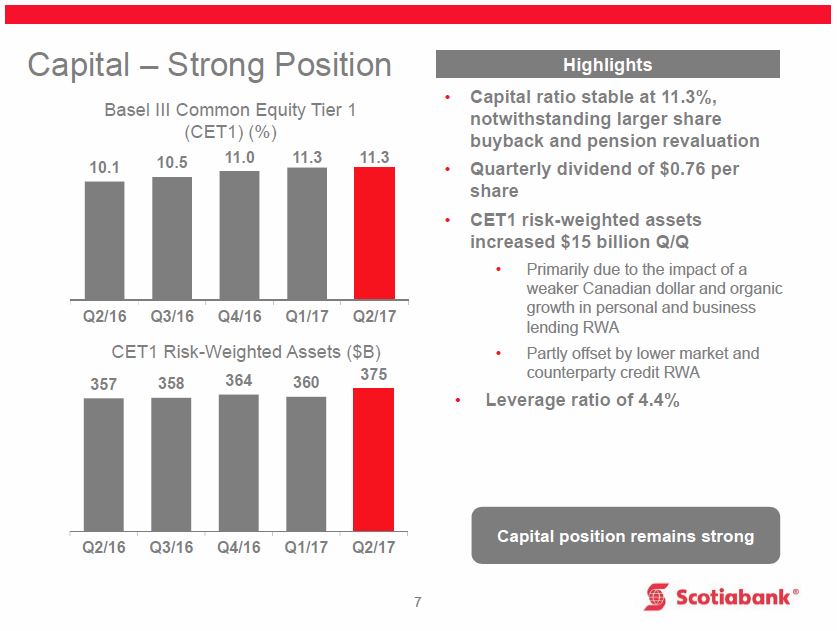

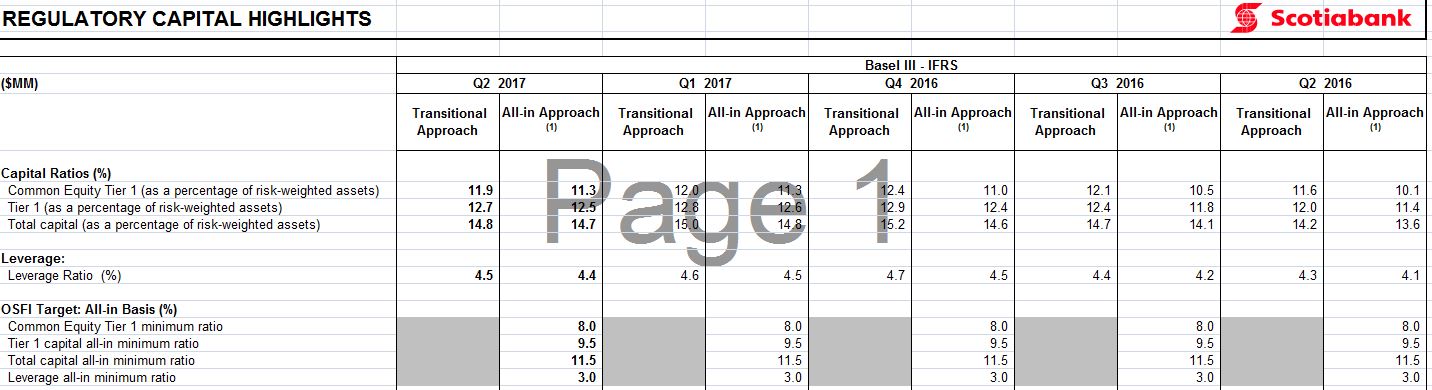

Capital Measure Ratios

In addition to touching upon the Capital Measure Ratios for BNS, you can find more information here.

BNS – Q2 2017 Strong Capital Position

BNS – Capital Ratios

If numbers are your thing, you can find a host of numbers in multiple worksheets within the Excel files right here!

Recent Events in the Canadian Banking Sector

A brief overview about a few major Recent Events in the Canadian Banking Sector can be found here.

As to whether the Home Capital problems in Canada will spillover to the Big 6 banks, here is a recent article which supports my opinion that the Big 6 will be just fine.

Inflated Real Estate Values

Given the impact the US real estate bubble had on the US Banking sector, it is only fair that people should be wondering what would happen to the Canadian financial institutions if the grossly inflated real estate values in various major centres in Canada were to experience a correction.

Multiple articles have been published about the state of certain pockets of the Canadian real estate market and how consumers are stretched financially. Recently, more articles have appeared about the sudden cooling of the real estate market.

Change in Sales of Freehold Houses 2016 vs 2017

In addition to my opinion on this topic which can be found here, I have very recently attended Open Houses (a community on the outskirts of Toronto) so I could speak with various real estate agents and brokers. All have indicated they have noticed a marked change in the last couple of months. Buyers appear to be less aggressive and in all cases, Open Houses are getting much less foot traffic. They have also commented that there is concern that some buyers may be willing to risk the loss of their deposit and will just walk away from their offers.

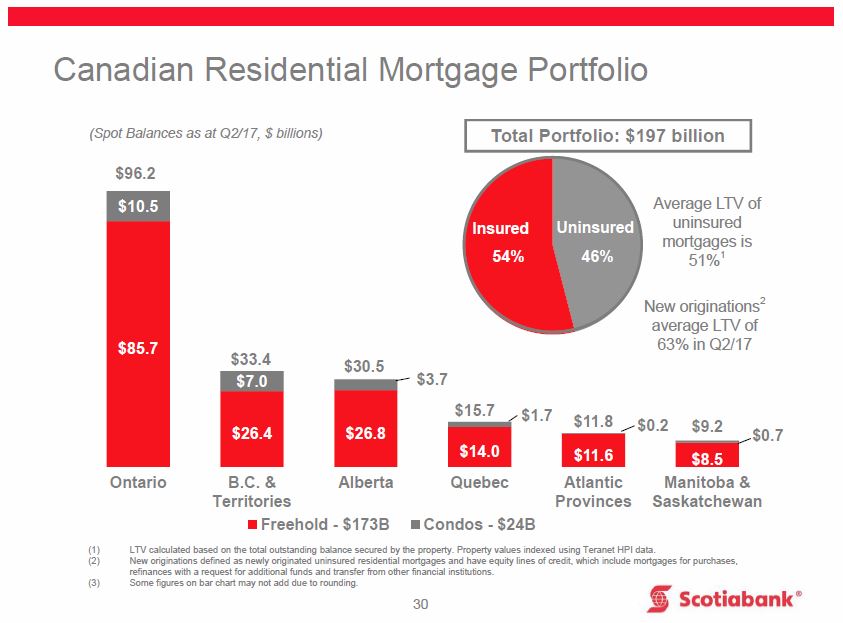

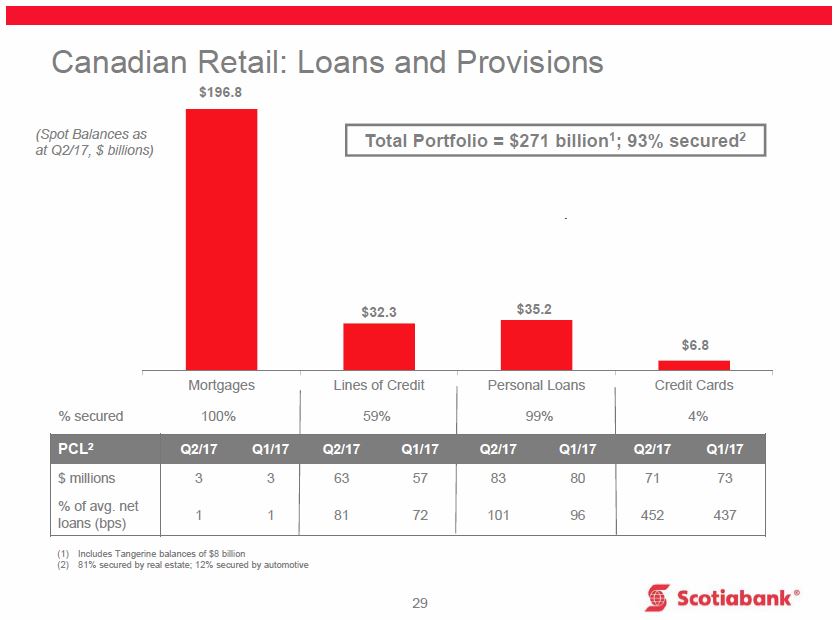

BNS’s Canadian Business

With all the concerns about the average Canadian consumer being stretched financially and the inflated real estate values in specific geographic pockets within Canada, the major Canadian financial institutions have provided more information regarding the composition of their respective real estate related loan portfolio.

The following data was included in BNS’s Q2 2017 Earnings report.

BNS – Q2 2017 CDN Residential Mortgage Portfolio

BNS – Q2 2017 CDN Retail Loans and Provisions

Overall, BNS’s Provision for Credit Losses and Loans 90+ days past due appear to be well controlled. Naturally, if we enter an economic downturn we can certainly expect to see an increase from current levels. At the moment, however, there is no cause for alarm but caution is definitely warranted.

Sean McGuckin, BNS’s Group Head and CFO, indicated during his segment of the National Bank Financial Markets – 15th Annual Financial Services Conference on March 30, 2017 that BNS continues to focus on credit quality and great strides are being made from a productivity standpoint. Relative to its peers, BNS is expected to achieve higher costs savings from its restructuring efforts than its peers. Improvements in results from all the restructuring currently underway is not going to come about solely from personnel changes but rather from process efficiencies and technological enhancements.

BNS has historically been a laggard on the credit card front. Some of the strategic acquisitions or alliances developed over recent years are starting to result in improvements in the credit card business. While growth rates will probably not be nearly as high going forward relative to last couple of years, BNS still has lots of room to grow its credit card market share.

Last year, BNS started to see that margins were shrinking on the residential mortgage side of the business and a conscious decision was made to back off in this area. Volume growth on the mortgage side is expected to be in the 3 – 5% range but much depends on the outcome of the changes various provincial governments are implementing to cool the real estate market.

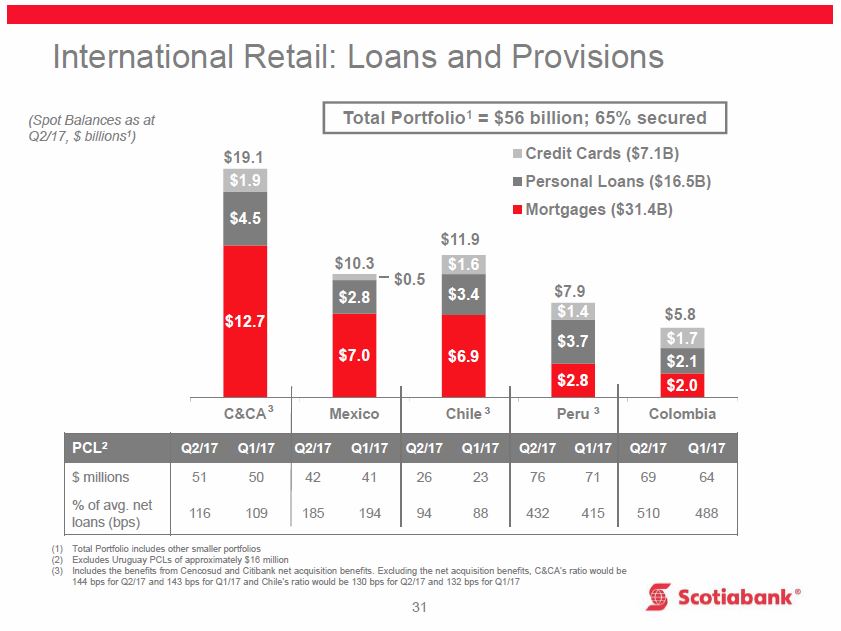

BNS’s International Business

Sean McGuckin discussed huge efficiency improvements that have been made in Mexico. The biggest opportunities in Mexico are expected to come from the optimization of the branch footprint, implementing a new core banking system, about a 50% reduction in the number of systems, and much easier end-to-end processing.

Because BNS has grown through acquisition, this has resulted in the bank having multiple systems and data centres which is grossly inefficient. The intent is to reduce the number of data centres in Latin America from 14 to 2. In addition, a call centre implemented in Mexico has been a great success and BNS envision this call centre being able to service other Latin American countries.

The topic of BNS’s strong capital position (ie. excess capital) arose in the presentation. McGuckin indicated this provides the bank with considerable flexibility. While further acquisitions in key markets are possible, he indicated this is not essential to grow as the bank has wonderful organic growth opportunities.

BNS – Q2 2017 International Retail Loans and Provisions

While some investors may wonder what will be the impact on Mexico’s manufacturing industry if the US follows through with changes it wishes to implement re: trade agreements, BNS does not envision that Mexico will suffer greatly. The weaker peso has made Mexican products that much more competitive and Mexico has 40 trade agreements with other countries. In fact, Mexican exporters are conducting an increasingly greater percentage of business with countries to the south; trade is not exclusively with countries to the North of Mexico.

Risk Management

There are a host of risks the Canadian financial institutions face. Global uncertainty, Brexit, Oil & Gas, Cyber risk, anti-money laundering, renegotiation of NAFTA, and the increasing complexity of regulation are just a few of these other risks.

Readers are encouraged to review the 34 page “Quarterly Slides” presentation found here as there are multiple pages that provide details addressing the quality of CM’s loan portfolio. There are also multiple pages in BNS’s 2016 Annual Report addressing CM’s Risk Management. Page 10 of the Annual Report lists the locations of the disclosures within the report.

Dividend

Unlike many foreign banks which were forced to dramatically reduce or suspend their dividend during the Financial Crisis, BNS and its Canadian counterparts froze their quarterly dividend. In mid-2011, BNS reinstated dividend increases.

BNS’s dividend distribution and stock split history can be found here.

On May 30, 2017, BNS announced that its Board of Directors declared a quarterly dividend increase of $0.02/share from $0.74 to $0.76. The next dividend is payable July 27, 2017 to shareholders of record at the close of business on July 4, 2017.

BNS is a reliable dividend machine. The likelihood of a dividend cut, or elimination, is remote so investors seeking a safe dividend and a respectable dividend yield (~4% as I compose this) would be well served acquiring BNS shares at current levels.

Valuation

On May 30, 2017, BNS announced that the Toronto Stock Exchange and the Office of the Superintendent of Financial Institutions have approved its normal course issuer bid to purchase up to 24 million of its Common Shares (you will need to click on News Releases when you get to this page). This represents approximately 2% of the 1,201,878,897 Common Shares issued and outstanding as of May 25, 2017.

The current mean FY2017 adjusted EPS estimates from various brokers for fiscal 2017 is $6.43.

BNS EPS estimates

BNS – Historical High Low PE Ratios

As I compose this post, BNS is trading at ~$76.60 on the TSX thus giving us a forward PE of ~11.9. When I look at the high/low PE ratio levels for the past several years I view the current level as acceptable and would consider adding to our existing position. In fact, we DRIP all our BNS dividends and hold BNS shares in RRSPs, TFSAs, and non-registered accounts.

The Bank of Nova Scotia Stock Analysis – Final Thoughts

Diversification really goes a long way. It is interesting to note that not one country within BNS’s international footprint represents more than 5 – 6% of the bank’s overall earnings.

While multiple acquisitions over the years have resulted in BNS essentially being a bank with multiple banks under the same banner, a concerted effort is now being made to streamline operations and to become more efficient. If you couple BNS’s projected growth with its proposed productivity enhancements, I think you will see continued improvements in the bank’s stock price over the long-term.

Having worked at BNS for the last 12 years of my banking career, I witnessed firsthand the major improvements that have transpired in recent years. While the bank was well shepherded by Mr. Waugh (former CEO), I am truly impressed with Mr. Porter (current CEO). He is driven, extremely focused, and knows where he wants the bank to be by the time his tenure as CEO comes to an end in roughly 7 years.

I view BNS as an attractive long-term investment but have one major concern. I suspect a major market pullback (also see here and here and here) will come about within the next 12 months. I, therefore, urge caution and suggest your purchases be made in small tranches. In the event a major market correction materializes, you should seriously consider backing up the truck to load up on BNS shares.

Note: I appreciate the time you took to read this article and hope you got something out of it. As always, please leave any feedback and questions you may have in the “Contact Me Here” section to the right.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: At the time of writing this post I am long BNS, CM, RY, BMO, and TD.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.