In a recent post on a popular investment website, readers are presented with 5 low P/E stocks that investors must not overlook. Within minutes, however, it is readily apparent these are 5 low P/E stocks investors should overlook.

The 5 companies ranked from highest to lowest risk, are as follows.

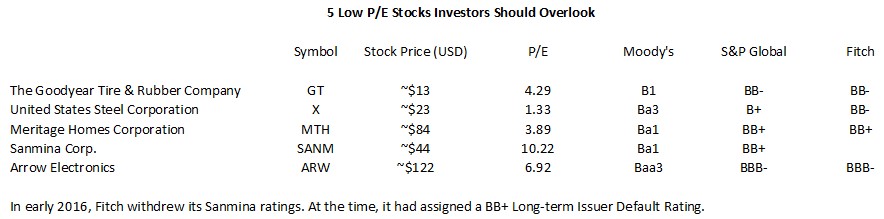

Although the major rating agencies rate these 5, they do not rate all companies. In such cases, we can quickly determine a company’s risk level.

R-I-S-K

Every investment carries a certain degree of risk. Furthermore, we each have our respective risk tolerance. Oftentimes, however, we truly learn how much risk we are prepared to assume only once things go wrong.

Looking at the 5 low P/E stocks investors should overlook, we see that GT is the weakest of the 5. Moody’s rating is the top tier of the highly speculative category. The rating assigned by S&P Global and Fitch is the lowest tier of the non-investment grade speculative category. This is one tier above the rating assigned by Moody’s.

The rating assigned to X by Moody’s and Fitch is the lowest tier of the non-investment grade speculative category. This is one tier higher than the rating assigned by S&P Global which is the top tier of the highly speculative category.

The ratings assigned to MTH and SANM by the major rating agencies are the top tier of the non-investment grade speculative category.

Only Arrow Electronics has investment-grade credit ratings. Even so, these ratings are the lowest tier of all the investment grade ratings. In this recent post, I disclose my decision to exit 4 positions because of their elevated risk; 2 of the 4 companies have credit ratings similar to Arrow Electronics.

Final Thoughts

Relying solely on a company’s valuation is not a prudent way in which to select companies as potential investments. The 5 low P/E stocks investors should overlook are good examples of why we need to analyze a company’s financial statements.

Look at the interest rates assigned to GT’s long-term debt (page 92 of 483 in the FY2021 Form 10-K) and X’s long-term debt (page 93 of 583 in the FY2021 Form 10-K). They are very high considering the multi-year low-interest rate environment we have experienced. This is an indication lenders consider both companies to be high risk. As equity investors, we need to acknowledge our risk is greater than that of debt holders.

In addition to excessively high-interest rates, these companies have a history of weak operating margins, a poor bottom line track record, and minimal (and sometimes negative) free cash flow.

In my opinion, it is wise to dial back risk given the current environment. I favour the high-quality companies for which reviews are found in the FFJ Archives.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I have no exposure to any company mentioned in this post.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.