Contents

Once upon a time, BCE Inc. (BCE) was the quintessential 'widows and orphans' stock. Investors seeking income could count on BCE to distribute its quarterly dividend like clockwork. Now? BCE is a 'dog with fleas'.

I can't specifically pinpoint when I became a BCE shareholder but I know my parents acquired BCE shares for me in the early 1960s. I have never paid much attention to this holding and at the time of my 2023 Year End FFJ Portfolio Review, it was not a top 30 holding.

This is one where I should have easily noticed its flea infestation some time ago.

Fortunately, recent tax and estate planning matters have prompted me to look at BCE more closely. Following my analysis, I immediately exited my position. Here is what alarmed me.

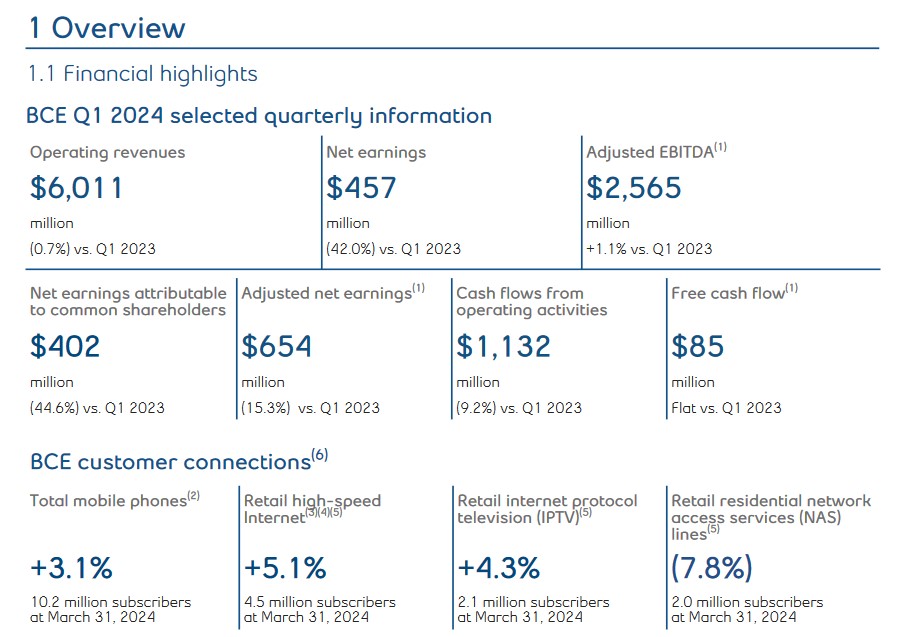

Financial Highlights

BCE's Q1 2024 results are accessible here.

It is a highly capital intensive business. It operates in a highly regulated environment and competition amongst the few large telecommunications companies in Canada is cutthroat.

BCE's annual revenue in FY2014 - 2023 (in billions of CAD $) is 21.04, 21.51, 21.72, 22.76, 23.47, 23.79, 22.88, 23.45, 24.17, and 24.67. In Q1 2024 it generated ~$6B. Looking at Q1 2024's financial highlights, we see that FY2024 Operating Revenues have 'started off on the wrong foot' and BCE will likely reflect no top line growth from the prior couple of fiscal years.

Layoffs

BCE needs to slash expenses! What is the easiest way? Downsize the labor force.

Earlier this year, BCE's CEO blamed the Canadian federal government for being slow to deliver aid to media enterprises, citing the Canadian Radio-television and Telecommunications Commission (CRTC) for its sluggish response to 'a time of crisis.'

This has led to BCE's decision to reduce its workforce by ~9% or ~4800 positions out of a total 44,610 employees. The majority of the lost jobs will be within Bell Canada, with under 10% coming from the Bell Media division.

In addition, BCE announced its plan to sell/close 45 of its 103 regional radio stations with 21 in British Columbia, 12 in Ontario, 7 in Quebec and 5 in Atlantic Canada.

This represents the most substantial reduction in headcount at BCE in ~30 years. It is also the second significant round of layoffs at BCE since the spring of 2023 when it reduced ~6% of Bell Media positions and axed 9 radio stations through closure or divestment.

Free Cash Flow (FCF)

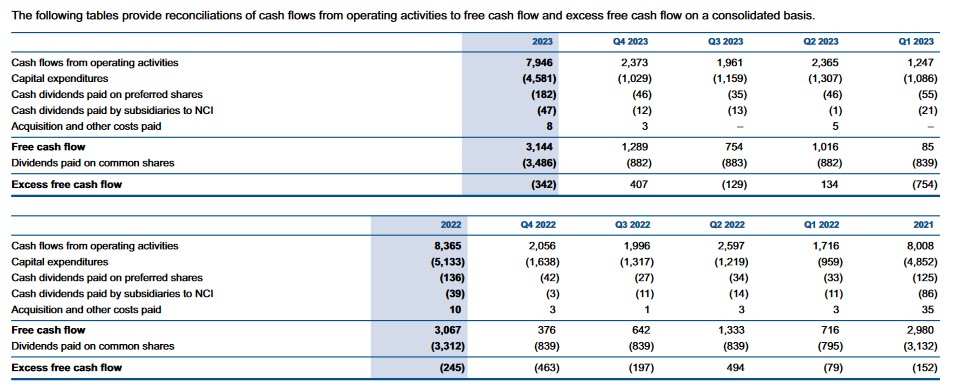

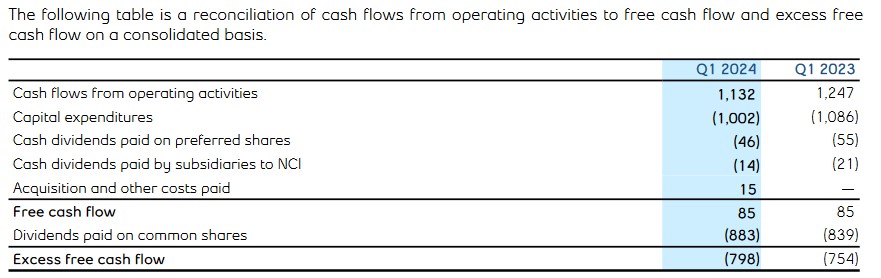

This is a highly capital intensive business and while BCE has been generating substantial FCF, the last time it had surplus FCF after distributing its common share dividends was in FY2020. That surplus was only $0.373B!

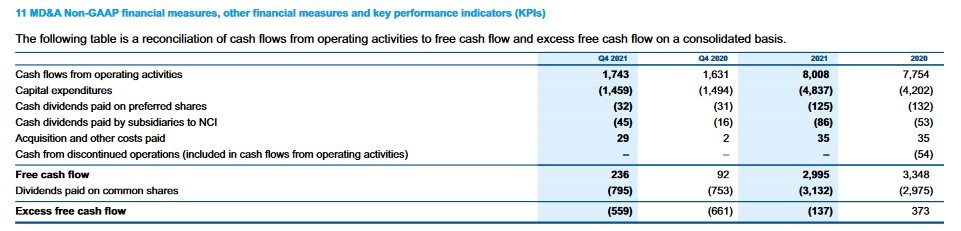

I am not making this stuff up. The following images are extracted from BCE's Form 40-Fs which are accessible here.

If a company can not generate sufficient FCF to service its dividend, it has to resort to other sources of funding (debt?). Brutal! This company already has a boatload of debt.

Financial and Capital Management

BCE's financial and capital management is not very encouraging! BCE's net debt has risen from $33.706B at FYE2022 to $37.816B at the end of Q1 2024.

Risk Assessment

On March 11, 2024 and March 21, 2024, respectively, S&P Global Ratings Canada, a business unit of S&P Global Canada Corp., and Moody’s Canada Inc. revised their outlook on BCE and Bell Canada to negative from stable principally as a result of ongoing debt leverage above their respective thresholds for the current ratings. Both, however, also affirmed all of BCE’s and Bell Canada’s existing ratings. On March 28, 2024, DBRS Limited confirmed BCE's and Bell Canada’s ratings and stable trend.

BCE has a TON of debt and preferred shares which rank in priority relative to common shareholders. If the credit ratings from DBRS and S&P Global for BCE's preferred shares are the lowest investment grade tier, you can bet the common shareholders are exposed to 'junk' risk.

Why take on this type of risk when there are countless companies with far superior credit ratings.

Dividend Yield

Shares closed at CDN$45.91 on May 7, 2024 and the quarterly dividend is $0.9975 quarterly dividend! The ~8.7% annual dividend yield should 'set off alarm bells'.

Deciding to invest in a company based on dividend metrics is extremely foolish.

Abysmal Average Annual Total Return

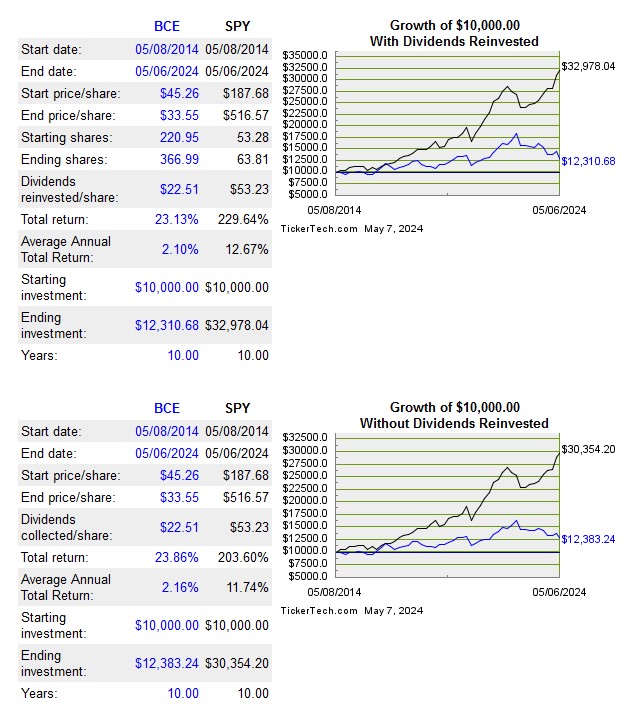

Between May 6, 2014 and May 6, 2024, BCE has generated and average annual total return of ~2.26% when dividend are reinvested.

How does this look when we factor in Canada's historical rate of inflation? The average annual rate of inflation in Canada from 2014 to 2024 is ~2.50% (see Bank of Canada Inflation Calculator).

Return On Invested Capital (ROIC)

In FY20214 - FY2023, BCE's ROIC (%) was 10.25, 10.49, 11.18, 10.46, 9.82, 9.94, 8.0, 7.77, 7.3, and 5.86.

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company's cost of capital will be lower than this level. In the past 7 fiscal years, BCE's ROIC has never come close to 15%!

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

Valuation

Using the current CDN$45.91 share price and the current forward-adjusted diluted EPS broker estimates, BCE's forward adjusted diluted PE levels are:

- FY2024 - 17 brokers - ~15.1 using the mean of $3.04 and low/high of $2.94 - $3.27.

- FY2025 - 16 brokers - ~14.8 using the mean of $3.11 and low/high of $2.97 - $3.31.

- FY2026 - 6 brokers - ~14.4 using the mean of $3.19 and low/high of $2.95 - $3.34.

This is a 'dog with fleas'. Even if you like BCE's valuation based on forward adjusted diluted EPS estimates, look at your risk. As a common shareholder, you are exposed to 'junk' risk. Furthermore, BCE generates insufficient cash from normal business operations to cover the common share dividends.

Final Thoughts

In the universe of companies in which to invest, what would possess a rational investor to invest in BCE?

This is truly a dog with fleas and I kick myself for not having paid any attention to this holding. Fortunately, I have exited positions where I have come out with a slight capital gain or a marginal capital loss.

If you think BCE's valuation is tempting...please reconsider.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to [email protected].

Disclosure: I have no exposure to BCE.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.