The Canadian Federal government in its infinite wisdom has introduced its 2024 Budget. The Budget calls for an increase of the inclusion rate on capital gains realized annually above $250,000 by individuals and on all capital gains realized by corporations and trusts from one-half to two-thirds. The amendments to the Income Tax Act are to be effective June 25, 2024.

This has prompted many Canadians to revisit existing estate and tax planning arrangements.

These upcoming changes have prompted me to take a closer look at our existing equity holdings. Sure enough, there are some companies I should have exited a long time ago but these positions were relatively insignificant in value that I just procrastinated.

So far, I have punted:

- SmartCentres Real Estate Investment Trust

- Enbridge

- BCE

I have now decided to eliminate my Emera (EMA) exposure. The risk-reward of an EMA investment is unacceptable for my investor profile.

Business Overview

I draw your attention to Emera’s website where you can learn about the company. Its quarterly and annual reports are accessible here.

Financials

Q1 2024 Results

EMA is scheduled to release its Q1 2024 results on May 13. I am not sticking around to see what they look like.

Operating Cash Flow (OCF) and Free Cash Flow (FCF)

Depreciation often serves as an indicator of how much needs to be invested to maintain assets in good operating condition.

In FY2014 – FY2023, EMA generated OCF of approximately (in billions of $) 0.763, 0.674, 1.053, 1.193, 1.690, 1.525, 1.637, 1.185, 0.913, and 2.241.

In FY2014 – FY2023, EMA generated FCF of approximately (in billions of $) 0.312, 0.247, (0.027), (0.336), (0.472), (0.970), (0.986), (1.174), (1.683), and (0.696).

The annual depreciation and amortization in FY2014 – FY2023 (in billions of $) was 0.342, 0.352, 0.593, 0.851, 0.928, 0.911, 0.899, 0.915, 0.959, and 1.060.

Annual CAPEX was 0.450, 0.427, 1.080, 1.529, 2.162, 2.495, 2.623, 2.359, 2.596, 2.937 during the same period.

Return On Invested Capital (ROIC)

In FY20214 – FY2023, EMA’s ROIC (%) was 8.52, 7.67, 4.08, 3.61, 6.01, 5.69, 6.15, 3.94, 5.72, and 5.93.

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company’s cost of capital will be lower than this level. EMA’s ROIC has never come close to 15%!

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

Risk Assessment

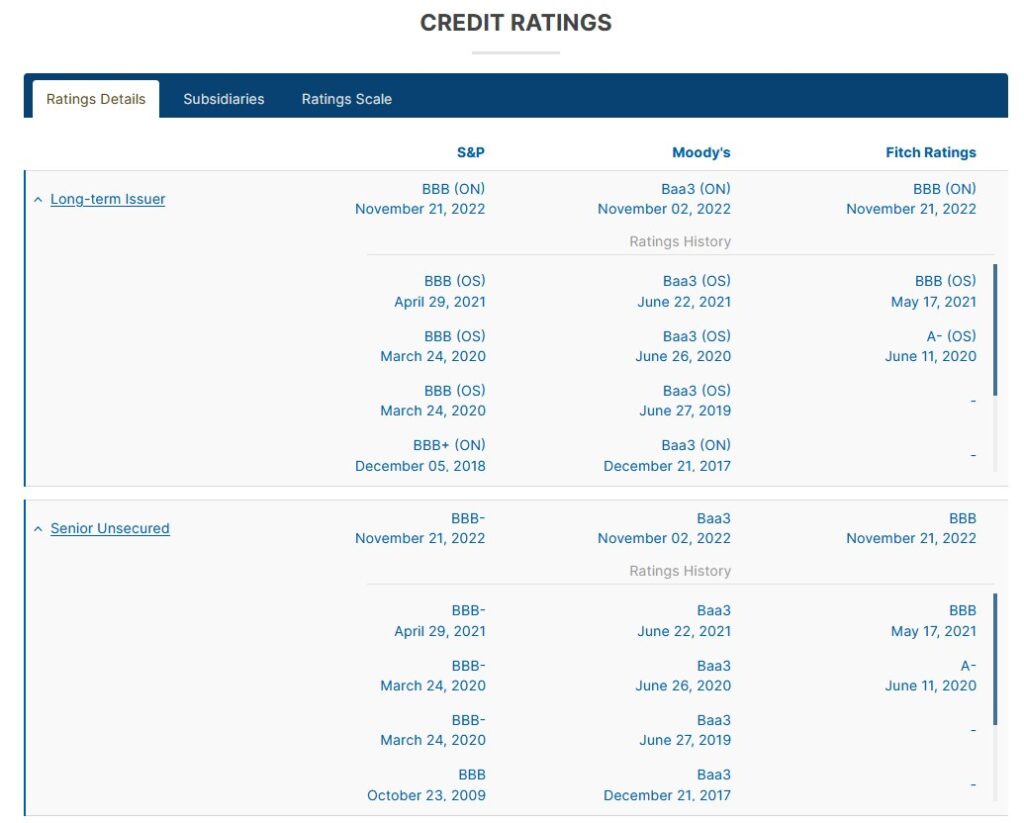

The following reflects EMA’s current and historical credit ratings and is accessible here; a rating scale is also available on the same web page.

Keep in mind that as an equity investor, your risk is greater than that of debt and preferred investors. EMA’s common share owners are essentially exposed to ‘non-investment grade’ risk.

EMA’s risk is totally unacceptable for my investor profile.

Dividends and Share Repurchases

Dividend and Dividend Yield

EMA’s dividend history is accessible here.

EMA is much like BCE; refer to my BCE Is A Dog With Fleas post. Both companies generate negative FCF, and therefore, both companies must look to other sources of funding to service their quarterly dividend distributions.

As I compose this post, shares trade at ~$48.50. The current quarterly dividend is $0.7175 which represents a ~6% dividend yield. A dividend yield at this level is a ‘red flag’ for me.

In my opinion, EMA’s current dividend is not sustainable. A tempting dividend yield is no reason to invest in this company.

Share Repurchases

The weighted average diluted shares outstanding in FY2014 – FY2023 (in millions of shares) is 147, 146, 172, 214, 234, 240, 248, 258, 266, and 274.

EMA, as evidenced by the steady increase in the weighted average diluted shares outstanding, has been and currently is in no position to repurchase shares.

Valuation

EMA’s FY2014 – FY2023 diluted PE levels are 20.02, 17.64, 19.91, 17.66, 44.60, 18.91, 15.50, 34.93, 17.31, and 11.59.

EMA’s current forward-adjusted diluted PE levels using current broker estimates and the $48.50 share price are:

- FY2024 – 11 brokers – ~15.8 using the mean of $3.07 and low/high of $2.89 – $3.30.

- FY2025 – 11 brokers – ~14.5 using the mean of $3.34 and low/high of $3.18 – $3.49.

- FY2026 – 5 brokers – ~13.9 using the mean of $3.48 and low/high of $3.29 – $3.55.

I don’t care how attractive EMA may appear on a forward adjusted diluted earnings basis. With a history of negative FCF, this company has too many strikes against it to even bother investing $1 in the company.

Final Thoughts

There is a ‘silver lining’ to the Canadian Federal government’s amendments to the Income Tax Act. It has forced me to look closely at existing holdings to which I very rarely pay attention.

Even if EMA is able to reverse a history of negative FCF, it will take a long time for it to recoup ~$6.344B of negative FCF it reported in FY2016 – FY2023.

On May 10, I punted 657 shares to the curb @ $48.4891.

After exiting EMA and the 3 companies mentioned at the outset of this post, I have exposure to just a handful of Canadian companies. They are (in no particular order):

- Alimentation Couche-Tard

- The Bank of Nova Scotia

- The Canadian Imperial Bank of Commerce

- The Bank of Montreal

- The Toronto-Dominion Bank

- The Royal Bank of Canada

- Brookfield Corporation

- Brookfield Asset Management

- Brrokfield Infrastructure

- Brookfield Renewable

- Intact Financial

- Canadian National Railway

- Canadian Pacific Kansas City

Within the next few weeks, I intend to further cull my Canadian exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I have no exposure to EMA.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.