I last reviewed Zoom Video Communications (ZM) in this November 21, 2023 post at which time the most current results were for Q3 and YTD2024.

On February 26, while in transit to British Columbia for a ski trip, ZM released its Q4 and FY2024 results.

Now that I have had the time to analyze ZM’s FY2024 results and FY2025 guidance, I revisit this existing holding.

Business Overview

I recommend you review Part 1, Item 1 in ZM’s FY2024 Form 10-K which provides a comprehensive overview of the business, competition, and risks. This is accessible through the SEC Filings section of the company’s website.

Financials

Q4 and FY2024 Results

Refer to material related to ZM’s Q4 Earnings which is accessible here.

In FY2024, ZM reported 9% growth in enterprise revenue and a 24% increase in Free Cash Flow (FCF).

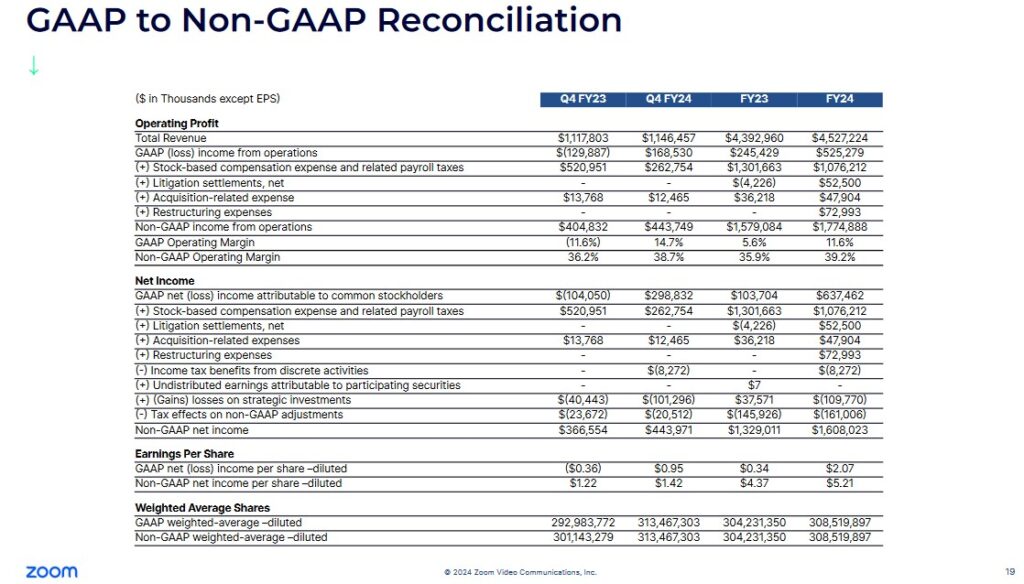

The non-GAAP operating margin of 39.2% was up 326 bps from 35.9% in FY2023.

In Q4, ZM saw traction in its emerging products, including a nearly 3x increase in Zoom contact center licenses. This increase was achieved by adding a significant number of new customers and an expansion in average deal size.

Zoom phone customers with 10,000 or more seats grew 27% YoY to 95.

Zoom AI companion has also grown significantly in just 5 months with over 510,000 accounts enabled and 7.2 million meeting summaries created as of FYE2024.

ZM continues to see improvement in online average monthly churn; it decreased to 3% from 3.4% in Q4 FY2023. This is consistent with the previous quarter and is the lowest churn the company has ever reported.

At FYE2024, ZM had ~$6.962B of cash and cash equivalents and marketable securities on hand; the marketable securities generally consist of high-grade commercial paper, corporate bonds, agency bonds, corporate and other debt securities, U.S. government agency securities, and treasury bills.

Total liabilities, on the other hand, amounted to $1.91B of which $1.252B was deferred revenue (cash received from customers before services have been provided).

ZM’s Remaining Performance Obligations (RPO) are billed and unbilled contracts. The terms of ZM’s subscription agreements are monthly, annual, and multiyear and it may bill for the full term in advance or on an annual, quarterly, or monthly basis, depending on the billing terms with customers.

As of January 31, 2024, the aggregate amount of the transaction price allocated to the RPO was $3,574.8 million. This consists of both billed consideration in the amount of $1,270.4 million and unbilled consideration in the amount of $2,304.4 million that ZM expects to recognize as revenue; ZM expects to recognize 58% of the remaining RPO as revenue over the next 12 months and the remainder thereafter.

NOTE: ZM’s renewal seasonality peaks in Q1 and declines throughout the remainder of the fiscal year.

Source: ZM – Earnings Presentation – February 26 2024

Operating Cash Flow (OCF) and Free Cash Flow (FCF)

In FY2017 – FY2024, ZM generated OCF of (in millions of $) 9.36, 19.43, 51.33, 151.89, 1,471.18, 1,605.27, 1,290.26, and 1,598.8.

In FY2017 – FY2024, ZM generated FCF of (in millions of $) $4.54, $9.69, $20.88, $113.67, $1,385.36, $1,459.66, $1,186.4, and $1,471.9.

Source: ZM – Earnings Presentation – February 26 2024

Source: ZM – Earnings Presentation – February 26 2024

FY2025 Outlook

ZM’s Q1 and FY2025 outlook does not account for any share repurchases the company intends to opportunistically make.

In FY2025, ZM expects a ~79% gross margin. Over the year, the plan is to improve gross margin towards the company’s long-term target of 80%. This is expected to be achieved through the optimization of the company’s data center strategy and growth of higher margin products like Zoom contact center.

Expectations are for FY2025 revenue to be ~$4.6B which represents ~1.6% YoY growth.

Q2 is expected to be the low point from a YoY growth perspective.

Non-GAAP operating income of $1.72B – $1.73B represents a non-GAAP operating margin of ~37.5%.

Credit Ratings

ZM has no debt, and therefore, no rating agency covers it.

Dividends and Share Repurchases

Dividend and Dividend Yield

ZM does not distribute a dividend.

Share Repurchases

ZM’s weighted average shares outstanding in FY2017 – FY2024 are (in millions of shares) 269, 269, 269, 254, 298, 306, 304, and 308.5.

In November 2018, ZM implemented a dual-class common stock structure. A Class A common stock entitles the shareholder to one vote per share. The Class B common stock entitles the shareholder to 10 votes per share. The Class A and Class B common stock have the same dividend and liquidation rights.

Details of ZM’s Stockholders’ Equity and Equity Incentive Plans are in Note 10 (commences on page 92 of 124) in the FY2024 Form 10-K.

In February 2022, ZM’s Board authorized a stock repurchase program of up to $1B of Class A common stock. During the year ended January 31, 2023, ZM purchased and subsequently retired 11,170,907 shares of its Class A common stock for an aggregate amount of $1B.

It repurchased no shares in FY2024.

ZM’s Board has authorized a stock repurchase program of up to $1.5B of the outstanding Class A common stock in FY2025. On the Q4 earnings call, management stated it would start executing repurchases in Q1. Furthermore, the share count and EPS metrics in its Q1 and FY2025 outlook do not account for the impacts from the shareholder repurchase program.

Valuation

In FY2020 – FY2024, ZM generated $0.09, $2.25, $4.50, $0.34, and $2.07 in diluted EPS and $0.35, $3.34, $5.07, $4.37, and $5.21 in adjusted diluted EPS; the following provides a GAAP to Non-GAAP Reconciliation.

My calculations of ZM’s valuation at the time of prior posts is found in my November 21, 2023 post.

ZM’s adjusted diluted EPS guidance for FY2025 is $4.85 – $4.88. Using my $61.695 purchase price on April 10, the forward adjusted diluted PE is ~12.7.

Using my purchase price and the current adjusted diluted EPS broker estimates, ZM’s forward adjusted diluted PE levels are:

- FY2025 – 29 brokers – ~12.5 using a mean of $4.92 and low/high of $4.83 – $5.46.

- FY2026 – 29 brokers – ~12.4 using a mean of $4.98 and low/high of $4.58 – $5.50.

- FY2027 – 9 brokers – ~12.1 using a mean of $5.09 and low/high of $4.38 – $5.69.

These adjusted diluted earnings estimates do not account for any share repurchases which are to occur in FY2025.

If ZM repurchases $1.5B at ~$65/share in equal quarterly tranches, we can expect a total repurchase of ~23.077 million shares.

The FY2025 weighted average shares outstanding forecast is 321 million shares. If we subtract ~23.077 million shares, we get slightly below 300 million shares. ZM, however, issues shares as part of its employee compensation structure. We can, therefore, expect the weighted average number of outstanding shares in FY2025 to likely be closer to 300 million.

Taking into consideration $1.5B of share repurchases in FY2025, ZM could generate $4.96 – $5.00 of non-GAAP EPS. Using the $4.98 mid-point and my $61.695 purchase price, the forward adjusted diluted PE is ~12.4.

ZM’s FY2025 FCF outlook is $1.44B – $1.48B. Using a $1.46B mid point and 300 million weighted average shares outstanding, the projected FCF/share is ~$4.89. $61.695 divided by $4.89 gives us a P/FCF valuation of ~12.6.

Rough estimates suggest that ZM’s valuation based on forward adjusted diluted earnings and FCF is in the very low teens.

Final Thoughts

I continue to seek out decent companies that appear to have fallen out of favor with investors. ZM appears to be such a company.

Between mid June 2020 and late 2021, ZM was grossly overvalued. Now, however, the pendulum has swung in the opposite direction. Given that I consider ZM to be undervalued, I acquired an additional 200 shares @ ~$61.70 in one of the ‘Core’ accounts within the FFJ Portfolio on April 10; this account now holds 800 ZM shares.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ZM.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.