Life teaches us what is not taught in school. I learned very quickly that inflation erodes the value of money and that your investment strategy should account for inflation’s impact!

I vividly recollect some things and then there are other things about which I have no recollection. For example, a former co-worker retired a few months ago and reached out to me. We reminisced about some of the stuff we had done. When he mentioned some of the events and conferences in which we had participated in the early 2000s, I quite honestly did not remember them at all; I could still not recollect them even after he showed me pictures in which I appeared! Ask me about my income, expenses, and lifestyle from many, many years ago and I have a much better recollection.

Given my ability to recollect my financial situation dating back a few decades, I now share life experiences that helped me factor inflation’s impact into my investment strategy.

Although I share how inflation has impacted me over the years, please do not just take my word that inflation can impact your lifestyle. Please read Warren Buffett’s Comments on Inflation which has been compiled by The Canadian Securities Institute. It is a lengthy document but well worth reading.

Inflation’s Impact on Me Over the Years

1970s

I had a morning paper route in the mid-1970s while in high school. This enabled me to generate income to feed my passion for buying records and attending rock concerts.

To put things in perspective, the first concert I attended was Bachman Turner Overdrive in 1975; the opening act was a group from Vancouver (can’t remember the name) and they were followed by Bob Seger and the Silver Bullet Band. The ticket price? ~$5.

Over the years I attended a ton of concerts! I remember some but other concerts are a bit of a blur!!!! Peter Frampton’s concert, for example, was the closing night of the Montreal Olympics in 1976!

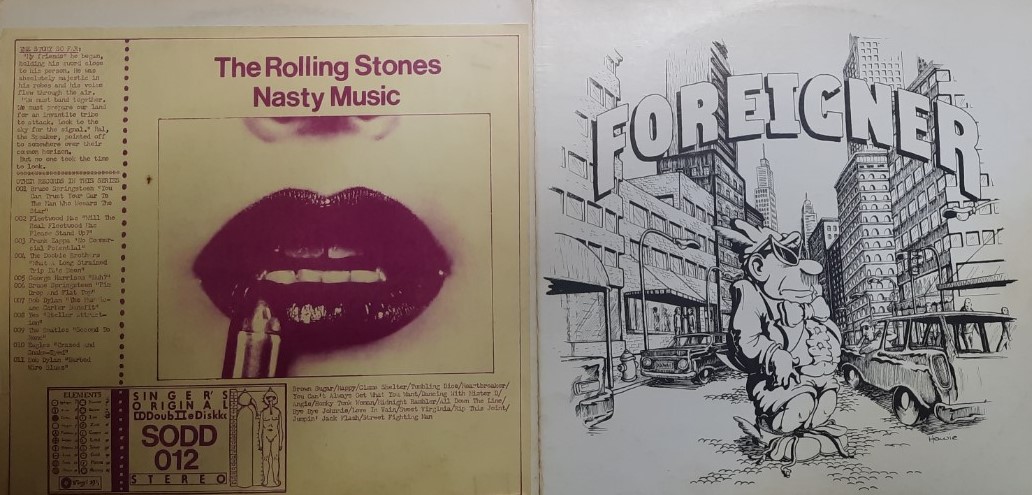

I do not specifically remember the prices of record albums but I am certain they were under $4. Bootlegs were more expensive and were hard to find because these records had not been made legally. Here are images of the bootlegs I still have stored in milk crates; I have not played any albums in decades.

Bootlegs were great because you could crank up the music and feel like you were actually at the concert. You just had to put up with unedited music and rudimentary album covers that did not always reflect all recorded tunes. In other instances, tunes are incorrectly named. In the first image above, ‘Write Me’, off Aerosmith’s first studio album, is reflected as Fly Away (Blind Man). A couple of songs are also omitted from the album cover. The Rolling Stones ‘Nasty Music’ bootleg also incorrectly reflects the names of a couple of songs.

The $7.50 price tag is still on ‘The Cars’ bootleg I bought in 1978. That is equivalent to $29.43 in 2021. The other albums are in the same price range except for the Stones bootleg because it is a double album.

These are the days where milk crates were ideal for storing albums. My girlfriend in Calgary was employed with Warner Elektra Atlantic (WEA). She obtained all her records for free and had roughly 25 – 30 milk crates full of albums.

My parents were not my financiers. In fact, they would have been even more adamant about this had they been fully aware of the extent of all my activities. I needed a job that would not interfere with my after-school and weekend activities. The best gig I could find was delivering newspapers 6 days/week.

I started with a paper route of roughly 40 homes. Over a 3 year period, the carriers on all routes adjacent to mine quit and I picked up all these routes. By the time I finished high school I was delivering the morning paper to ~135 homes.

In those days, the carriers had to collect money weekly from customers. I enjoyed this aspect of delivering newspapers because I would meet my customers and they would get to know me.

I was never organized when it came to handling all the cash I received. Bills were never neatly folded. I would just stuff money in my pockets. When I needed to provide change I would feel the coins to determine what I was about to pull out from my pockets. Quite often, I would be standing inside a homeowner’s entrance and money would fall on the floor. I distinctly remember several customers remarking about the amount of money I was carrying. When I included my tips, I typically netted ~$50/week. That amount in 1976 is equivalent to ~$228 in 2021.

Christmas time is when I hit the jackpot! I typically netted over $1000 in tips. That amount in 1976 is ~$4554 in 2021. I had to make the occasional trip home to empty my pockets because my pockets could not hold all the money I collected.

1980s

I graduated with an undergrad degree in Economics in 1980 and landed a job with one of Canada’s major chartered banks. I had to relocate to Calgary which is a ~4-hour flight from where my parent’s lived.

My starting salary was $14,000, my monthly rent was $375, my weekly grocery bill was $25 – $35, and a season’s pass to ski at Norquay, Sunshine, and Lake Louise was ~$400. That ski pass was a great deal considering I would start skiing in late November/early December and I would stop skiing in mid-June; I was skiing 40+ days during the ski season.

Fast forward to 1984 when I left work to return to university. My income had increased to ~$25,000, my monthly rent had dropped to ~$200 because I now had roommates, and my weekly grocery bill was $45 – $60.

I had even purchased a car for ~$5000 in 1981 and did not require financing. That is the equivalent of $14,652 in 2021.

I encourage you to use the Bank of Canada Inflation Calculator to confirm these figures.

The other thing you need to consider is that in the early 1980s, the inflation level in Canada was through the roof. The economy in Western Canada was booming and anybody employed in the oil and gas sector was making a ton of money. The problem is that the economy in Western Canada crashed in 1981. Unemployment skyrocketed and real estate values plummeted.

Before the economy crashed in 1981, you could invest funds in a Term Deposit at a major Canadian financial institution for which you would receive ~17.75% interest for 4 years with interest paid annually. If you wanted to place funds on deposit for 5 years, however, I distinctly remember the interest rate dropped to 8% – 9%.

While your tax liability on this interest income would be hefty depending on your marginal tax bracket, you certainly were in a far better predicament than consumers who had borrowed money (eg. car loans, boat loans, etc.) at rates over 25%. It is all a matter of perspective!

I returned to university in September 1984 to complete a Master of Business Administration degree. After completing my graduate degree in December 1986, I chose not to return to Western Canada and re-entered the workforce in Ontario. My starting salary was $34,000. Using the Bank of Canada Inflation Calculator we see that $34,000 in 1987 is equivalent to $70,172 in 2021.

I had to forego income for a little over 2.5 years (I went on a 3-month ski trip in Europe before returning to the workforce) but had saved enough money from my 4 years of work in Calgary that I did not need student loan financing. I also self-financed my ski trip.

People debate whether the cost of a college/university education is worth it. I think every situation is different. In some instances, the additional education has proven to be worthwhile and an utter waste of money in others.

I have read numerous stories about people who have graduated from college or university with hundreds of thousands of dollars of debt. Some have found employment but struggle to repay their student debt. Many are resigned to having student debt for the rest of their life. This will ultimately negatively affect family planning, homeownership, and other major life decisions. Depending on your circumstances and the laws of the jurisdiction in which you reside it is entirely possible your student loans may not be discharged if you file for personal bankruptcy.

1990s

In 1990, my wife’s/my income had increased. We purchased our home for $200,000 which is the equivalent of $359,845 in 2021. We put 25% equity into the purchase of our home so we would not have to resort to CMHC financing. Although interest rates were much lower than in the early 1980s, our mortgage rate was still a lofty 14.25% for a 5-year term.

We planned to retire much sooner than most Canadians. Part of our long-term financial plan included being mortgage-free within 10 years and we accomplished this in 1998.

Once our mortgage was retired, we continued to maximize our contributions to tax-advantaged accounts and started investing through taxable accounts.

I had absolutely no interest in investing in debt instruments and opted to invest solely in equities. I figured that as an equity investor I could participate in the appreciation in the value of a company as opposed to being locked in at a particular rate. My game plan was to create an investment portfolio that would generate a stream of dividend income whose growth would outpace the rate of inflation. The intent from the very outset was to have after-tax dividend income that would sustain us until our time was up after which time, our heir would benefit.

2000s – 2020s

Over the years we acquired rental properties in addition to investing in equities. While investing in real estate can be extremely lucrative, we would have been much further ahead if we just stuck with investing in high-quality companies. We were fortunate to have good tenants. Nevertheless, our rental properties did require more work than the time I spend managing our equity portfolio. Secondly, the appreciation in the value of most of our equity investments has been far greater than the appreciation in the value of our rental properties. Thirdly, we incurred a significant capital gain each time we sold a rental property on which we incurred a tax liability. We did not need that much net after-tax capital gain every year we sold a property!

In the case of equity investing, our dividend income is more than ample for our needs. I do not need to sell equities so I can defer the tax liability until we sell; this could be several years into the future.

Although many people travel while they own rental properties, this was not part of our plan. Before COVID-19, we planned to frequently travel and decided to simplify our lives by selling rental properties over a period of years. We sold our last rental property in 2020.

The only remaining piece of real estate we own is our principal residence. I quite honestly do not know the value of our home. Just recently, however, the home across the street from us sold for ~$150,000 over the ~$1,000,000 asking price. If I plug a conservative $900,000 after real estate commission value and 2021 into the Bank of Canada Inflation Calculator to determine the equivalent value in 1990, I get $500,216. I mentioned earlier that we paid ~$200,00 in 1990. Clearly, the appreciation in the value of our home has far exceeded the rate of inflation. An added benefit is that the sale of a principal residence in Canada does not trigger any capital gains tax.

In some countries, mortgage interest is tax-deductible. Such is not the case in Canada. This is why the sale of a principal residence in Canada triggers no taxable capital gain.

Despite the significant appreciation in the value of our home, we have never really viewed our home as an asset even though the accounting definition indicates it is an asset. We do not view it as an asset because it does not generate income. In fact, our home is an expense in that we have to pay property tax, maintenance, repairs, and utilities. How we treat our home from an asset/liability perspective is a matter of personal choice. We just choose to be super conservative.

Invest to Account for Inflation’s Impact

My examples demonstrate the impact of inflation but for a more current and relevant example….has anybody noticed a recent surge in the price of groceries!

Look at the image below about the projected price of a cup of coffee using a couple of different rates of inflation. I used to drink a couple of extra-large double cream coffees from McDonald’s every day. I stopped that months ago when I bought a Keurig coffee machine.

Source: Scotiabank

In my opinion, investing in extremely safe investments (eg. Term deposits, GICs, T-Bills, money market instruments, bonds) adds an element of risk many people fail to consider. The risk of losing your principal with these types of investments is low but your purchasing power deteriorates because the rate of return from these investments is less than the rate of inflation.

Final Thoughts

The primary takeaway from this article is that your investment strategy should account for inflation’s impact. Neglect the impact of inflation as part of your investment strategy and you could end up in a predicament of having more month than money. The earlier in life you realize this, the more likely you have a chance to attain financial freedom.

I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. You should not make any investment decision without conducting your research and due diligence.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with the company mentioned in this article.