![]()

Summary

- UPS reported its Q4 and FY2017 results on February 1, 2018. UPS was trading at a lofty valuation and investors were disappointed to see UPS was once again negatively impacted by the surge in pre-Christmas volume.

- The retracement in UPS’ stock price to the ~$119.50 level and the growth in earnings have now restored UPS to a reasonable valuation.

- In FY2017, UPS significantly lowered its long-term pension risk by making a $5B tax efficient contribution to the pensions.

- UPS plans to invest $12B to expand its logistics network, increase pension funding, and to position the company to further enhance shareowner value.

- I will refrain from acquiring additional UPS shares for the reasons reflected under ‘Final Thoughts’.

Introduction

I wrote about United Parcel Service (NYSE: UPS) on April 4, 2017 at which time I felt UPS was fairly valued at $107.46.

If you look at UPS’ stock chart you can see UPS’s stock price ran up to ~$134 in mid January 2018. On February 1, 2018, however, UPS released its Q4 and FY2017 results. The investment community was not overly impressed with the results and the stock price took a hit dropping to ~$119.50.

In this post I analyze whether the recent pullback is sufficient to warrant the acquisition of additional shares.

Q4 and FY2018 Results

UPS’s most recent results can be accessed here.

The surge in shipping volumes during the peak holiday period continues to plague UPS. Once again, earnings suffered from higher costs despite UPS’ ongoing efforts to reduce bottlenecks and delayed deliveries in the period leading up to Christmas. Management indicated that bottleneck costs of ~$0.125B and investments in new technology and automated capacity expansion cost ~$0.06B.

UPS has benefited from a rapid rise in ecommerce, improvements in US economic activity, and an increase in consumer spending. Holiday online shopping orders overwhelmed UPS’ system when it delivered 762 million packages which were in excess of its forecasts.

Despite ongoing efforts (eg. the addition of increased shipping rates and peak-season surcharges) to ease the strain brought on by major package volume spikes ahead of the holidays, UPS continues to struggle to reduce the extra costs of making stops at individual residential addresses rather than at businesses.

“Revenue is Vanity. Profits are Sanity. Cash Flow is Reality”.

Fortunately, UPS continues to generate strong Free Cash Flow (FCF). In fiscal 2013 – 2017, UPS generated $5.239B, $3.398B, $5.051B, $3.508B, and $3.573B in FCF.

Pension Mark to Market

At the end of FY2017, UPS significantly lowered its long-term pension risk by making a $5B tax efficient contribution to the pensions.

Pension and Postretirement Benefit Obligations as at FYE 2015, 2016, and 2017 amounted to $10.638B, $12.694B, and $7.061B.

UPS is exposed to changes in interest rates which impact the valuation of its pension and postretirement benefit obligations and the related benefit cost recognized in the income statement.

In 2011, UPS adopted the Mark to Market methodology so as to:

- simplify pension accounting;

- align itself with U.S. GAAP fair value accounting concepts;

- reflect current market returns;

- provide greater transparency.

This change had no impact to funding requirements or cash flow nor was there any change in benefits paid to plan participants.

Long-Term Credit Ratings

UPS’ long-term debt credit rating from Moody’s is A1 and A+ from S&P. These ratings are upper medium grade credit ratings. These ratings are 5 notches below the top AAA rating but are still considered good ratings.

Competition from Amazon

Readers are encouraged to read my April 4, 2017 post wherein I discussed the competition UPS can expect from Amazon (NASDAQ: AMZN).

In addition, Amazon has launched a trial to expand a service which will make products available for quick delivery directly from merchants without overwhelming the AMZN warehouses with additional inventory. What AMZN is doing is enticing the sellers who use its online marketplace with lower delivery costs, logistics software, warehouse inspections and recommendations.

While UPS’ senior management had the foresight to identify this huge potential risk from AMZN by launching several initiatives which are in various stages of roll-out to remain at the cutting edge in the logistics business, it remains to be seen to what extent AMZN will negatively impact UPS and its competition.

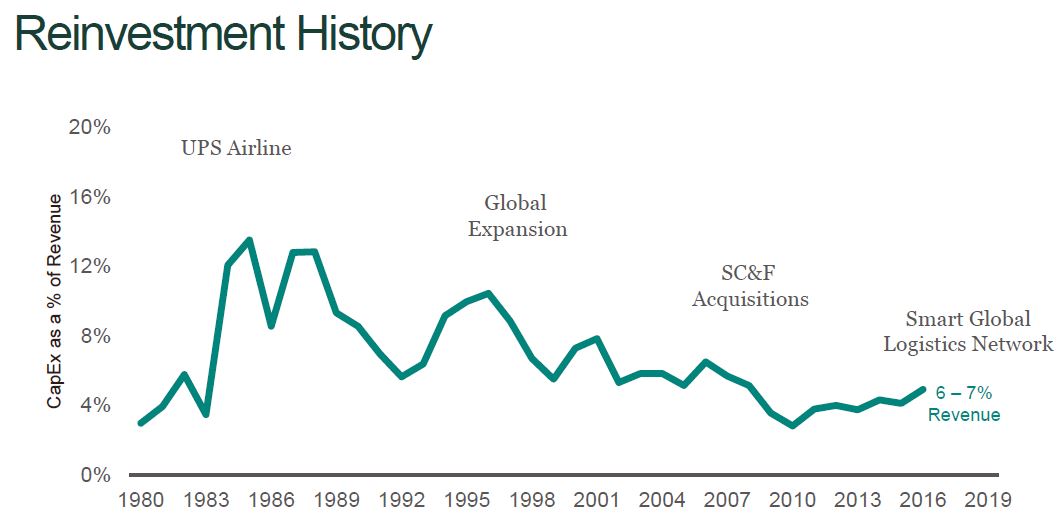

CAPEX Forecast

This is a highly capital intensive business as borne out by the following graph which shows UPS’ historical CAPEX as a percentage of revenue dating back to 1980.

Source: UPS Overview October 31, 2017 presentation

Source: UPS Overview October 31, 2017 presentation

UPS’s CEO indicated the company plans to invest $12B to expand its logistics network, increase pension funding, and to position the company to further enhance shareowner value. This investment program is partially a result of the tax savings created by the Tax and Jobs Act; changes to U.S. tax laws added ~$0.30/share.

The CAPEX will include $6.5B – $7B for the purchase of 14 additional Boeing 747-8 aircraft and 4 new aircraft freighters. There are also plans for 18 new or retrofitted facilities this year including three U.S. ground hubs. These new ground hubs are the first new major hubs in two decades. Further investments over the next 3 years will include the acquisition of new ground vehicles and IT platform improvements.

Valuation

UPS reported 2017 EPS of $5.61 and adjusted 2017 EPS of $6.01. Management also announced Full-Year 2018 adjusted EPS guidance of $7.03 to $7.37.

With UPS currently trading at ~$119.50 we get a PE of ~21.3 and an adjusted PE of ~19.9. On the basis of the 2018 adjusted EPS guidance we get a forward adjusted PE range of ~16.21 – ~17.

This range is reasonably attractive and is below the ~18 forward adjusted PE level evidenced at the time of my April 4, 2017 post.

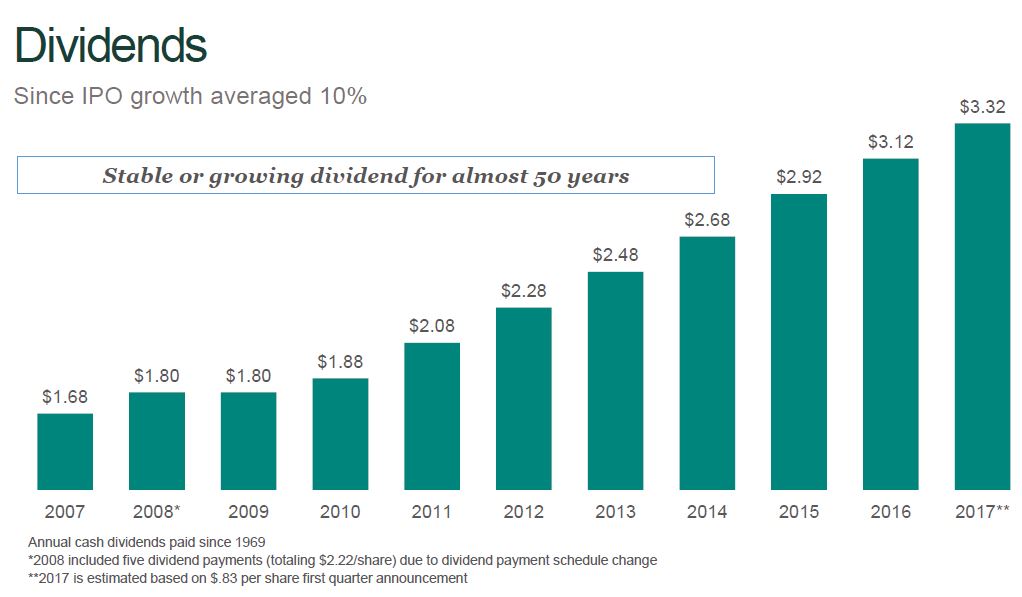

Dividend, Dividend Yield, Dividend Payout Ratio, and Share Repurchases

UPS’ dividend history can be found here; the current annual dividend is $3.32. Source: UPS Overview October 31, 2017 presentation

Source: UPS Overview October 31, 2017 presentation

Based on 2017 EPS of $5.61 and adjusted 2017 EPS of $6.01, the current dividend payout ratio is ~59% of 2017’s EPS and ~55% of 2017’s adjusted EPS.

UPS distributed its 4th quarterly $0.83 dividend on November 29, 2017. On the February 1, 2018 conference call, UPS’ CFO indicated that the number one priority is to reinvest in the business with the dividend also being of significant importance. With Board approval, shareholders can expect to see further dividend increases in the future.

UPS is trading at ~$119.50 and I suspect UPS’ quarterly dividend will be increased $0.05 to $0.88 ($3.52/annually) when I look at dividend increases over the last few years. On this basis investors can expect the dividend yield to increase from ~2.78% to ~2.95%.

As at December 31, 2016 and 2017, UPS’ weighted average shares outstanding amounted to 876 million and 872 million. While UPS repurchased more than 16 million shares for about $1.8B, the net reduction was only 4 million shares.

The extent of UPS’ share purchases over the years is borne out by the fact 1,063 million shares were outstanding as at the FY2007 fiscal year end.

Final Thoughts

While I view UPS as an attractive investment after the recent pullback and the projected growth in earnings, I do not intend to acquire additional shares at the moment. My rationale is that I:

- already own several hundred UPS shares and am of the opinion I have sufficient UPS shares at the moment;

- think the US equity market will likely experience a correction of some magnitude within the year and UPS will not be immune from any major market pullback;

- want to monitor the success of AMZN’s trial program to determine whether UPS and FedEx (NYSE: FDX) might be at risk.

IF UPS’ share price were to experience a dramatic pullback to ~$110 or less for reasons other than a deterioration in its business, however, I would revisit my decision and might acquire additional shares.

Having said this, I think you would be safe to acquire UPS shares at the current ~$119.50 level given that the:

- company continues to generate strong free cash flow;

- current valuation level is reasonable following the recent pullback in the stock price;

- the current and projected dividend yields are is acceptable;

- further dividend increases can be expected over the years;

- management is being proactive in fending off AMZN;

Thanks for reading!

Note: Thanks for reading this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long UPS.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.