I last reviewed Genuine Parts Company (GPC) at which time I recommended that its status as a Dividend King not influence investment decisions. Fixating on dividend metrics is a fundamentally flawed way of investing. The focus should be on a company’s total potential shareholder return.

On July 24, 2017, I initiated a 300 share GPC position @ $82.219/share. I subsequently added a few shares over the years and also reinvested the quarterly dividend bringing my exposure to 488 shares. I have deliberated on exiting this position for quite some time as it was never my intention to make it a significant holding.

As evidence of how little interest I have in this company, my last review was in this April 19, 2024 post. It has never been a top 30 holding and in my ongoing effort to reduce the number of companies I need to follow, I was looking for an opportune time to exit my GPC exposure.

The surge in GPC’s share price following the July 22, 2025 Q2 2025 earnings release now provides me with an exit opportunity; I have sold all 488 shares @ $130.5694. I remain hopeful for a market correction and the sale proceeds now sit as cash in a ‘Core’ account in the FFJ Portfolio.

I no longer have any interest in this company, and therefore, dispense with any review of its recent results. If you are interested in learning about GPC, I encourage you to review the company’s website and Part 1 Item 1 in GPC’s FY2024 Form 10-K.

Financials

Q2 and YTD2025 Results

GPC’s Q2 and YTD2025 results are accessible here. Suffice it to say that GPC is experience challenges!

Capital Allocation

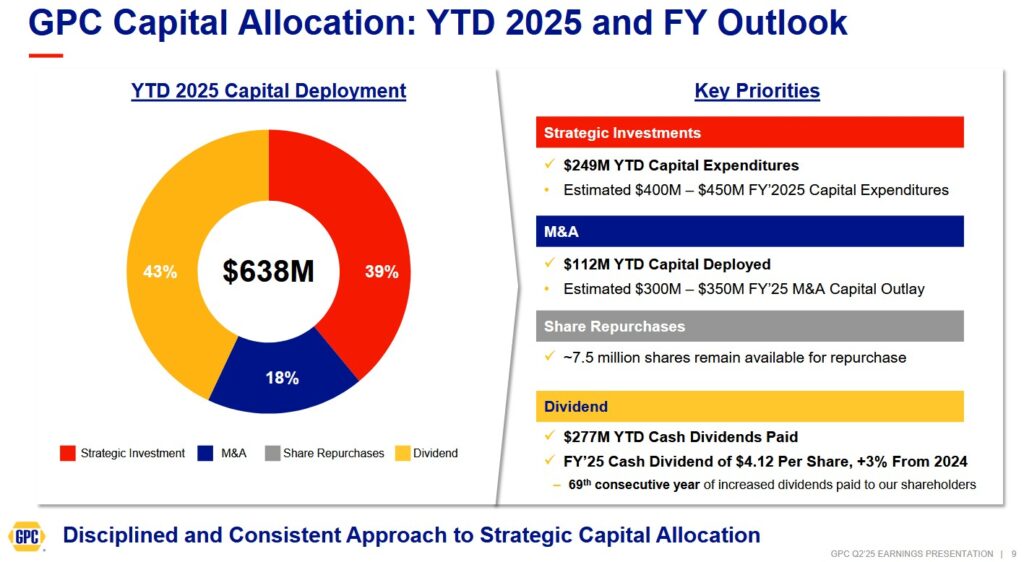

This is GPC’s YTD2025 capital allocation and FY2025 outlook.

FY2025 Outlook

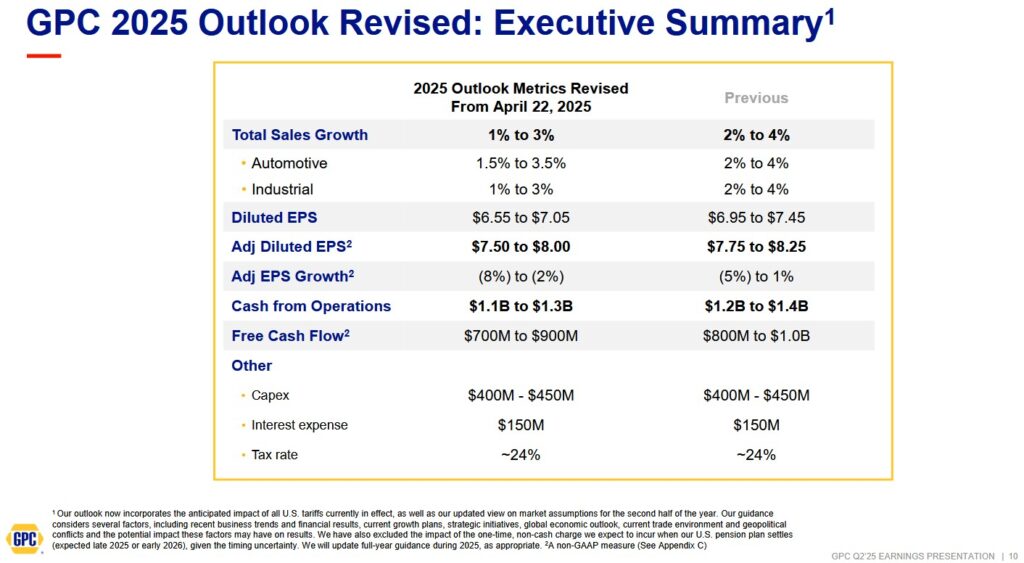

The following reflects GPC’s updated FY2025 outlook.

FY2025 Financial Targets

By way of comparison, I provide GPC’s FY2025 financial targets that were provided in GPC’s March 23, 2023 Investor Day presentation. The probability of GPC achieving these targets is remote…at best!

Source: GPC Investor Day Presentation – March 23, 2023

Credit Ratings

GPC’s unsecured long-term debt ratings are:

- Moody’s: Baa1 (stable outlook) affirmed on November 30, 2023.

- S&P Global: BBB (negative outlook) last reviewed on June 12, 2025.

Moody’s rating is the top tier of the lower medium grade. S&P Global’s rating is the middle tier of the lower medium grade. Both ratings are investment grade and are defined as an obligor having ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

Dividends and Share Repurchases

Dividend and Dividend Yield

GPC’s dividend history is accessible here.

Some investors make the fundamentally flawed mistake of thinking that attractive dividend metrics should influence the investment decision making process. That’s okay. We all make mistakes. Let’s just hope we all come to the realization that the focus should be on total investment return.

Share Repurchases

GPC’s approximate weighted average shares outstanding in FY2010 and FY2024 were (in millions of shares) ~158.461 and ~139.67. In Q2 2025, this had been reduced to 139.244. No shares have been repurchased in the first half of FY2025 given GPC’s cash flow situation.

Valuation

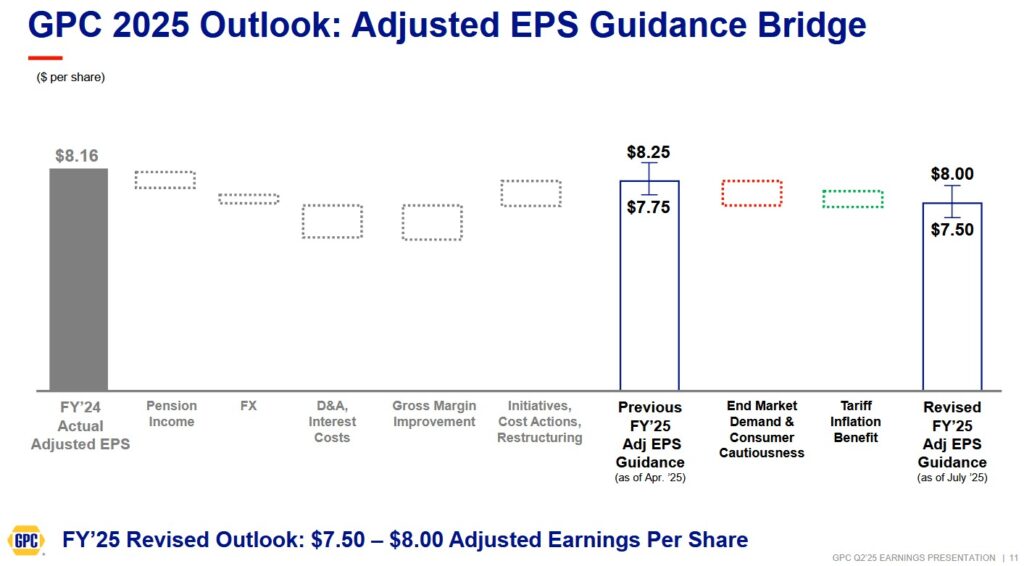

GPC’s FY2025 adjusted diluted EPS range is $7.50 – $8.00. With shares having closed at ~$133.31 on July 22, 2025, the forward adjusted diluted P/E is ~16.67 – ~17.8.

Its valuation using current broker estimates is:

- FY2025 – 11 brokers – ~17.38 based on a mean of $7.67 and low/high of $7.38 – $7.86.

- FY2026 – 11 brokers – ~15.7 based on a mean of $8.49 and low/high of $8.18 – $8.74.

- FY2027 – 7 brokers – ~ 14.5 based on a mean of $9.19 and low/high of $8.91 – $9.41.

The estimates will undoubtedly be revised over the coming days since Q2 2205 results have just been released. I envision these estimates will be revised lower.

GPC has lowered its FY2025 FCF outlook to $0.7B – $0.9B and it is unlikely it will repurchase shares in the second half of FY2025. If we use 139.3 million as the weighted average diluted shares outstanding for all of 2025, GPC will likely generate ~$5.03 – ~$6.46 of FCF/share. Using the current ~$133.31 share price, the forward P/FCF is ~20.6 – ~26.5.

GPC’s YTD2024 and YTD2025 share-based compensation (SBC) is ~$26.57 million and ~$24.18 million. If the SBC in the second half of FY2025 is similar to the first half, the full year’s SBC should be ~$48.36 million. Deducting this amount from GPC’s FY2025 FCF outlook should not result in a meaningful variance between FCF calculated using the conventional and modified methods; the modified method deducts SBC from Operating Cash Flow (OCF).

The following reflects my valuation estimates at the time of prior GPC posts.

When I wrote my October 20, 2023 post, GPC shares were trading at ~$133. Using this share price and the forward-adjusted diluted earnings estimates from the brokers that cover GPC, the forward-adjusted diluted PE levels were:

- FY2023 – 15 brokers – ~14.4 based on a mean of $9.23 and low/high of $9.16 – $9.32.

- FY2024 – 15 brokers – ~13.3 based on a mean of $9.97 and low/high of $9.49 – $10.25.

- FY2025 – 9 brokers – ~12.05 based on a mean of $11.04 and low/high of $10.65 – $11.59.

I have been a GPC shareholder since July 24, 2017. Other than roughly mid/late March 2020 when the North American economy shut down because of COVID, I do not recall GPC having ever been valued so attractively. I had hoped GPC would be aggressively repurchasing shares but that did not happen!

Following the release of Q1 2024 earnings and amended FY2024 outlook on April 18, GPC’s share price surged to ~$160 from the prior day’s $144 closing share price. Using the company’s revised FY2024 adjusted diluted EPS outlook of $9.80 – $9.95, the forward adjusted diluted PE range is ~16.1 – ~16.3.

Its valuation using current broker estimates, which will undoubtedly be revised over the coming days, is:

- FY2024 – 13 brokers – ~16.3 based on a mean of $9.84 and low/high of $9.76 – $9.98.

- FY2025 – 13 brokers – ~15 based on a mean of $10.66 and low/high of $9.84 – $11.02.

- FY2026 – 6 brokers – ~ 14.1 based on a mean of $11.37 and low/high of $10.39 – $11.72.

If GPC repurchases shares at a similar rate over the next 3 quarters, I envision the weighted average outstanding shares in FY2024 will be ~139.5 million. Using the $0.9B mid-point of GPC’s FY2024 FCF outlook, GPC should generate ~$6.45 of FCF per share. Using the current ~$160 share price, we get a P/FCF share value of ~24.8.

Final Thoughts

In prior posts I disclose that I have made my fair share of errors of omission and, to a far lesser extent, errors of commission. I chalk up GPC as being one of my errors of commission. I should have never invested in the company to begin with. Years ago, however, I could be seduced by attractive dividend metrics. My next error of commission was retaining this holding for ~8 years!

Fortunately, my GPC exposure has never been material. Nevertheless, I could have invested this money in a far superior company.

There is no point in fretting over this investment blunder. Time to move on.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I have no GPC exposure following my July 22, 2025 exit.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.