A year has elapsed since I last reviewed Otis Worldwide Corporation (OTIS). At the time, I envisioned a broad market sell-off would lead to a more attractive valuation. Following that post, OTIS’s share price skyrocketed and its valuation deteriorated.

In early February 2022, I took a quick look at OTIS but still did not like the valuation. Furthermore, OTIS’s Investor Day was scheduled for February 15, 2022. I, therefore, elected to postpone my review.

With the release of Q1 2022 results on April 25 and the expected completion of the acquisition of 49.99% of Zardoya Otis, S.A. in Q2 2022, I now reanalyze OTIS.

Zardoya is an elevator equipment and service business with operations in Spain, Portugal and Morocco. The structure of the transaction is an all-cash voluntary tender offer. The intention is to delist Zardoya Otis from the Madrid, Barcelona, Bilbao and Valencia stock exchanges in May 2022.

Management expects this acquisition to add $0.02 of EPS accretion in FY2022.

In my previous post, I include an Industry and Business Overview. Part 1 of the 2021 Form 10-K, however, provides a more comprehensive overview of the company and a discussion of various risk factors.

2021 Investor Day

Investors are encouraged to review the Investor Day presentation.

We see from this presentation that the industry benefits from strong fundamentals supported by global growth trends, including urbanization. Other benefits include:

- Highly regulated, life–safety business;

- The top 5 participants represent ~70% of the industry;

- Concentrated new equipment market;

- Fragmented service base; and

- ~44% of Sales are from the sale of new equipment with the remaining ~56% being mostly recurring Service revenue.

Financials

Q1 2022 Results

On April 25, 2022, OTIS released Q1 2022 results.

Looking at OTIS’s Q1 2022 Balance Sheet, there is $2.93B in short-term Contract Liabilities. A very small component of noncurrent Contract Liabilities is included within Other long-term liabilities.

These Contract Liabilities are recognized when a customer pays consideration, or OTIS has a right to receive an amount of unconditional consideration, in advance of the satisfaction of performance obligations under a contract; OTIS typically receives progress payments from customers as it performs work over time.

In essence, OTIS has client funds before it performs its services under the terms of a contract. Once services are performed, the appropriate amount is recorded as Revenue and OTIS incurs expenses related to the performance of its services. As a result, OTIS will not be disbursing $2.93B within 1 year.

Only $0.538B is reported as Contract Assets. This line item reflects revenue recognized in advance of customer billing.

In Q1, new equipment orders were up 8.8% with growth in all regions.

In Korea, OTIS was selected to provide more than 70 Gen 2 elevators equipped with ReGen drive technology that can deliver substantial energy savings. These elevators will serve more than 2,200 apartment units and is OTIS’s latest project in the region with GS Engineering & Construction with whom it has collaborated for ~20 years.

In China, OTIS received an order to support the next phase of the Shenzhen Metro project. This extends OTIS’s more than two decades of collaboration with the installation of nearly 1,000 units to date. In this phase, OTIS will provide more than 350 ‘internet of things’ enabled elevators and escalators.

As with many other companies, OTIS faces commodity headwinds and annual labour cost increases. Despite these headwinds, Selling, General, and Administrative costs and R&D expenses are being very well controlled.

Free Cash Flow (FCF)

OTIS continues to generate strong FCF. In FY2020 and FY2021, it generated $1.297B and $1.594B, respectively. In Q1 2022, OTIS generated FCF that continues to outpace net income.

Source: OTIS Form 8-K – April 25, 2022

FY2022 Guidance

OTIS has refined its FY2022 guidance.

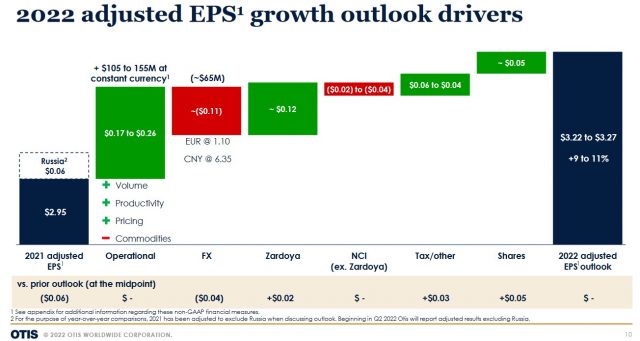

Source: OTIS Q1 2022 Earnings Presentation – April 25, 2022

Source: OTIS Q1 2022 Earnings Presentation – April 25, 2022

Overall, the improvement in the service business is expected to be offset by lower new equipment growth. The outlook for service margin, however, is raised to 70 bps from the previous 50 bps guidance.

The improvements on the service front are expected to be offset by reduced margin expectations in the new equipment segment. This is attributed to increased headwinds on commodities and higher freight costs and lower volume growth.

The backlog in Europe, the Middle East, and Africa (EMEA) is up more than 5%. Customers are requesting the postponement of deliveries, however, due to a broader slowdown in building construction activity; some shipments slated for 2022 are being delayed to 2023. As a result, management expects EMEA sales to be up low to mid-single-digits for 2022.

In China, the Q1 backlog was up 4% from strong orders growth. The current lockdowns, however, are not only impacting shipments but are also disrupting the supply chain. While deliveries are expected to pick up starting in May, management is adjusting its 2022 China outlook given the supply chain challenges.

Given the lower volume expectations in China, Asia is now expected to be down slightly for the year.

The outlook on new equipment organic sales in the Americas remains unchanged and is expected to be up low single-digits in 2022.

Management has growing concerns about the long-term sustainability of its operations in Russia. As a result, OTIS is motivated to find solutions and explore alternatives for its Russian business.

OTIS has removed its Russian operations from its FY2022 outlook and prior year comparisons; this adjustment will largely impact the new equipment business.

Credit Ratings

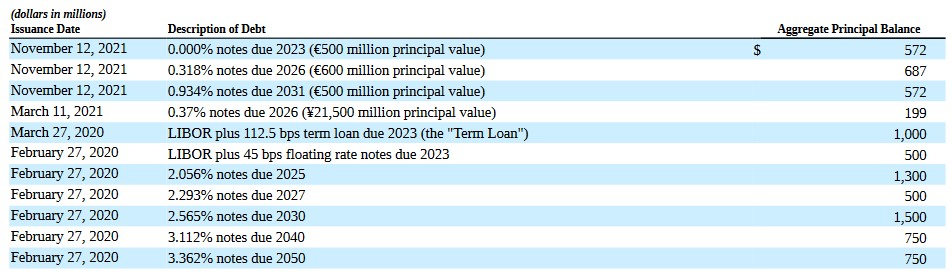

The following table reflects OTIS’s long-term debt issuances in FY2020 and FY2021.

The $6.3B net proceeds from the February and March 2020 debt issuances were used to distribute cash to United Technologies as part of the separation in 2020.

Proceeds from the March 2021 issuance of Japanese Yen notes were used to repay a portion of OTIS’s outstanding Euro-denominated commercial paper.

OTIS is holding the proceeds from the November 2021 issuance of the Euro notes in escrow to fund the acquisition of the remaining 49.99% of Zardoya. This is reflected as Restricted Cash on the December 31, 2021 and March 31, 2022 Consolidated Balance Sheets.

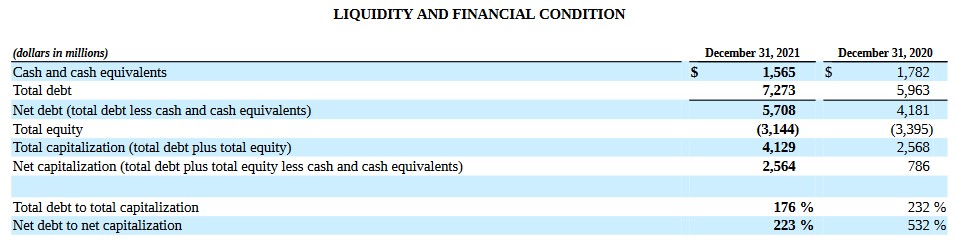

One of OTIS’s priorities has been to improve its debt/capitalization positions. This table reflects the improvement in OTIS’s debt/capitalization on a total and a net basis in FY2020 and FY2021.

Moody’s and S&P Global continue to assign Baa2 and BBB ratings (respectively) to OTIS’s domestic unsecured long-term debt; the outlook from both is stable.

These ratings are the middle tier of the ‘lower medium grade’ category. They define an obligor as having an ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

These ratings are satisfactory for my prudent investor profile.

Dividend and Dividend Yield

A medium-term capital allocation priority includes the disbursement of ~35% – ~40% of GAAP Net Income.

On April 22, 2022, OTIS declared a $0.29/share quarterly dividend payable on June 10, 2022, to shareholders of record at the close of business on May 20, 2022. This is a 20.8% increase from the prior $0.24/share and a 45% increase since OTIS became a public company (see dividend history).

The $1.16 in annual dividend distributions is a ~1.6% dividend yield based on the current ~$74.60 share price.

I envision OTIS will continue to generate strong FCF thereby leading to future dividend increases.

On April 27, 2020, OTIS’s Board authorized a ~$1.0B share repurchase program; in FY2021, 9.7 million shares were repurchased for ~$0.725B. Under this program, shares may be purchased on the open market, in privately negotiated transactions, or under accelerated share repurchase programs or other plans that comply with the Securities Exchange Act.

A new share repurchase program for up to $1.0B was authorized in Q1 2022.

In FY2021, as a result of the increased debt incurred to fund the acquisition of the remaining 49.99% of Zardoya, OTIS temporarily suspended its share repurchases to prioritize deleveraging. OTIS, however, completed its deleveraging and resumed share repurchases in Q1 with $0.2B in share repurchases. The FY2022 outlook calls for a total of $0.5B in share repurchases.

In FY2020 and FY2021, the diluted weighted average number of shares outstanding (in millions) was 434.6 and 431.4. In Q1 2022, this has been reduced to 427.7 (433.7 in Q1 2021).

Valuation

Shares were trading at $76.27 when I last reviewed OTIS and FY2021 adjusted diluted EPS guidance from the brokers which cover OTIS was $2.78 – $2.84. Using that share price, the forward adjusted diluted PE range was ~26.9 – ~27.4 and ~27.14 based on the $2.81 mid-point.

The release of Q1 2022 results includes the refinement of management’s FY2022 adjusted diluted EPS outlook.

OTIS’s share price is currently ~$74.60. Based on management’s revised guidance, the FY2022 forward adjusted diluted PE range is ~22.8 – ~23.2.

The valuation based on this share price and the following forward adjusted diluted EPS guidance (likely to be revised over the coming days) from the brokers which cover OTIS is:

- FY2022 – 14 brokers – mean of $3.27 and low/high of $3.21 – $3.34. Using the mean estimate, the forward adjusted diluted PE is ~22.8.

- FY2023 – 14 brokers – mean of $3.65 and low/high of $3.43 – $3.88. Using the mean estimate, the forward adjusted diluted PE is ~20.4.

- FY2024 – 7 brokers – mean of $4.02 and low/high of $3.81 – $4.40. Using the mean estimate, the forward adjusted diluted PE is ~18.6.

Final Thoughts

In April 2022, an agreement between the National Elevator Bargaining Association and the International Union of Elevator Constructors was ratified. This 5-year collective bargaining agreement covers the majority of OTIS’s U.S. field employees and is effective July 2022 with wage increases taking effect in January 2023. The annual increases are generally in line with historical trends and, as in previous years, OTIS fully expects to offset this additional cost through increased productivity.

Although OTIS’s order backlog is growing, some regions are experiencing conditions leading to requests for shipment postponements. In addition, another major global resurgence of COVID may lead to further lockdowns and project delays.

Despite these headwinds, OTIS has the largest elevator/escalator service portfolio in the world from which it generates substantial recurring revenue. Furthermore, there are an estimated ~2 million OTIS elevators that are currently under service by third parties. OTIS has the opportunity to recapture some of these elevators due to increasing modernization demand, which favours OEMs. In addition, OTIS would be able to increase the penetration of its preventative maintenance software which would improve elevator uptimes.

Management’s guidance reflects the acceleration of both sales and the profit trajectory of the service business resulting from the benefits of investments and sustained focus on driving productivity. Although the new equipment business is challenged because of the current macroeconomic environment, OTIS’s backlog, pricing actions, and over $0.1B of productivity improvements should lead to a sharp recovery once the commodity and the freight headwinds abate.

I currently hold 409 shares in one of the ‘Side’ accounts within the FFJ Portfolio plus shares in a retirement account for which I do not disclose details; I received all these shares as part of the separation from United Technologies in 2020. My dilemma is that I require the liquidity in the accounts in which I hold OTIS shares to satisfy upcoming income tax payments. If OTIS was one of my top 20 holdings, I might consider initiating a position in a third account. It is not, however, even in the top 30 so I will not be acquiring additional shares at this point.

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long OTIS.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.