Summary

Summary

- This Nike, Inc. stock analysis is based on Q3 2017 financial results released March 21, 2017.

- Nike reported strong Q3 2017 results although some investors have expressed concern about the deterioration in gross profit margin.

- Changing consumer shopping habits is posing a huge challenge but this problem is not unique to NKE. NKE has far greater resources than its competitors to deploy toward addressing these challenges.

- NKE’s Balance Sheet is like a fortress. It has sufficient Cash and Equivalents and Short -Term Investments to completely wipe out its Short-Term Liabilities.

- NKE is currently valued fairly and does not present a bargain.

Addressing the Challenges – Triple Double

On Nike’s (NYSE: NKE) March 21, 2017 conference call, management indicated consumers are using digital technology as the foundation of their shopping experience. This is having a pronounced impact on consumer patterns, especially in North America, as the economics of brick-and-mortar retail is dramatically different from just a few years ago.

While NKE recognizes this is creating significant challenges, it views them as a tremendous opportunity. Brands that will dominate going forward will be those which capitalize on the proper use of technology and which lead with service.

In this regard, NKE is driving fundamental change in 3 core areas of its business through its “Triple Double” initiative:

- INNOVATION – inspire consumers;

- SPEED – a highly effective and efficient supply chain;

- DIRECT – in the marketplace where NKE connects personally with consumers.

While historically successful in all 3 core areas, NKE has committed to doubling its impact in each area.

- PRODUCT – double cadence and scale of innovation through performance and sports style;

- SUPPLY – double speed from product insight to delivery to the consumer;

- MARKETPLACE – double direct connections with consumers through digital, membership, and personalization.

Further details on the Triple Double initiative can be found in the Chairman, CEO, and President’s comments in the Q3 2017 conference call transcript.

Q3 2017 and YTD Financial Results

The following is a very high level recap of NKE’s Q3 and YTD 2017 results.

- Revenue: up 5% to $8.4B for Q3 or 7% growth on a currency-neutral basis and up 6% to $25.673B for 9 months;

- Gross Profit Margin: 44.5% for Q3 vs. 45.9% for same period 2016 and YTD of 44.8% vs. 46.3% for 9 months 2016;

- Net Income: $1.141B Q3 2017 vs. $0.95B in Q3 2016 and YTD of $3.233B vs. $2.914B for 2016;

- Diluted EPS: up 24% ($0.68 vs. $0.55) for Q3 and up 14% for the first 9 months of the current FY ($1.91 vs. $1.67);

- Weighted Avg # of Diluted C/S Outstanding – Q3 2017 and 2016: 1686.3 vs. 1737.3 (millions)

Despite NKE’s impressive results, many investors have opted to focus on the following negative data and have suggested that NKE is faltering.

- Inventory: 7% increase to $4.9B compared to the prior year. Management has indicated this was driven by a higher average cost due primarily to product mix and to support growth of its Direct-to-Consumer (DTC) businesses. Wholesale inventory units were actually down 3%.

- Gross Profit Margin: The contraction was a result of higher average selling prices being more than offset by higher product costs, unfavorable changes in foreign exchange rates, and the impact of higher off-price sales.

- Effective Tax Rate: Some investors have remarked that NKE’s results were beneficially impacted by a 13.8% effective tax rate compared to 16.3% for the same period in the previous fiscal year. This reduction was primarily due to a reduction in tax reserves and an increase in the mix of earnings from operations outside of the U.S., which are generally subject to a lower tax rate.

Why I am not Concerned

NKE is a behemoth. It is virtually impossible to make immediate dramatic changes to a business of this size. Management readily acknowledges there are headwinds but they are taking appropriate measures to adapt to changes in the marketplace.

NKE continues to be extremely profitable and in FY 2016 it spun off almost $2B in FCF. I envision it will spin off $1B – $2B in FCF in FY2017.

What a pristine Balance Sheet! It is a welcome change to see a Balance Sheet that has negligible values associated with “fluff” line items (ie. Goodwill and Identifiable Intangible Assets).

As at the end of Q3 2017, NKE had enough Cash and Equivalents and Short -Term Investments to completely wipe out its Short-Term Liabilities.

The challenge NKE is facing relative to consumer purchasing habits is not unique to them. Its competitors face the same predicament. At least NKE has far greater resources at its disposal to address these challenges relative to most, if not all, its competitors.

NKE appears to be wisely repurchasing shares at reasonable valuations. An increase in NKE’s stock price will not help. Existing shareholders should wish for continued pressure on NKE’s share value.

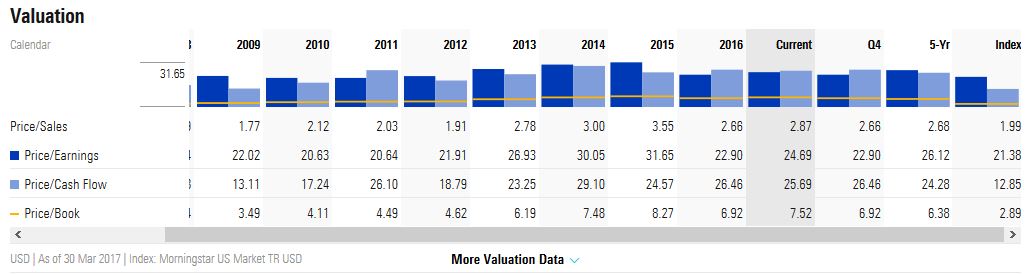

Valuation

NKE closed at $55.73 on March 31, 2017 and is trading at a PE just shy of 23.30. This level is not totally out of whack with historical levels.

NKE – Morningstar March 31 2017

Multiple analysts are projecting FY2017 EPS of ~2.39. Using the PE reflected above, I get a fair value of ~$55.7. Anyone buying NKE at this level is certainly not getting a bargain but at the same time is not grossly overpaying.

Source: TD WebBroker – NKE EPS estimates

Source: ValuEngine – NKE EPS estimates

NKE’s is not for dividend yield hungry investors (although I will gladly accept receipt of our NKE dividend on April 3, 2017)! Its current quarterly dividend is $0.18, which, based on a closing price of $55.73, represents a yield of 1.3%. Despite this low dividend yield, I am a firm believer Low or No Dividend Yield Companies Belong in Your Portfolio.

Nike, Inc. Stock Analysis – Final Thoughts

It is always disconcerting to see deterioration in profit margins but one must remember that business results do not improve in perpetuity. NKE and its competitors are facing a radical shift in the way many end consumers purchase products and services. At least NKE recognizes the challenges and is taking appropriate steps.

I acquired NKE shares for the FFJ Portfolio because its balance sheet is like a fortress, it is immensely profitable, and it generates a ton of FCF. I see no reason for concern at this stage.

While NKE is certainly not valued as attractively as when I purchased shares, I don’t think an investor with a long-term investment horizon could go wrong acquiring shares at current levels. Having said this, I am cautiously optimistic there will be a major pullback given that we have not experienced a correction of any significance in several years. Should one occur, I would very likely add to our existing NKE holdings.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I am long NKE.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.