I last reviewed Nasdaq (NDAQ) in this April 26, 2024 post at which time the Q1 2024 results were the most current. Now that we have NDAQ’s Q2 and YTD2024 results, I revisit this holding.

I last reviewed Nasdaq (NDAQ) in this April 26, 2024 post at which time the Q1 2024 results were the most current. Now that we have NDAQ’s Q2 and YTD2024 results, I revisit this holding.

Business Overview

The best way to learn about NDAQ is to review its website. Part 1 Items 1 (Business) and 1A (Risk Factors) in the FY2023 Form 10-K is also a great source of information.

Financials

Q2 and YTD2024 Results

NDAQ’s Q2 and YTD2024 results are accessible on the company’s website.

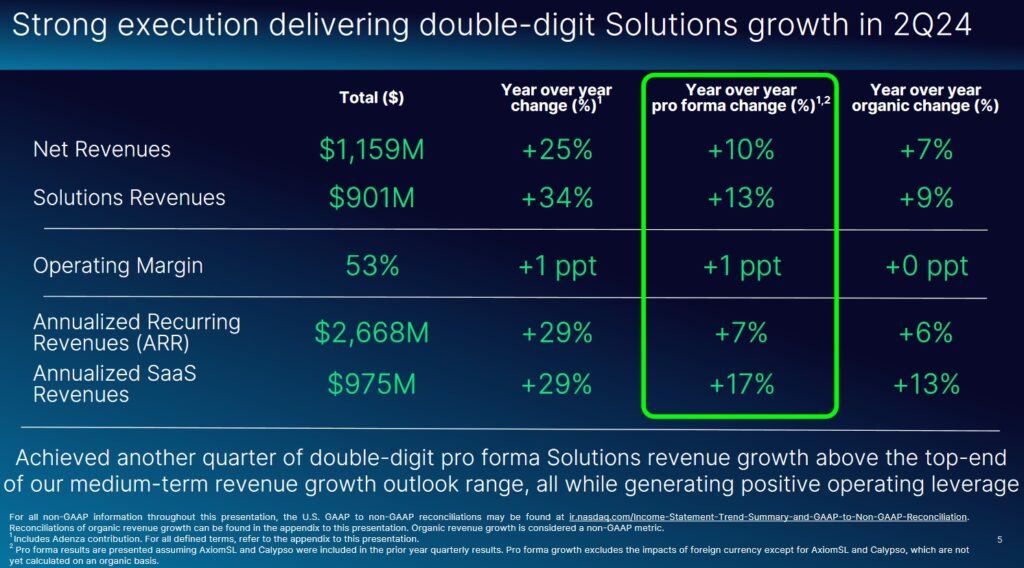

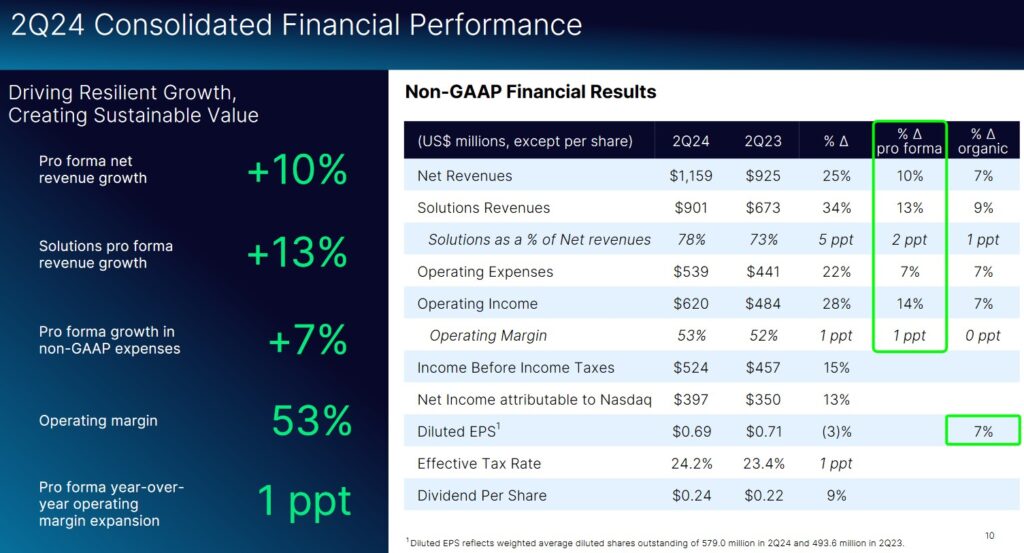

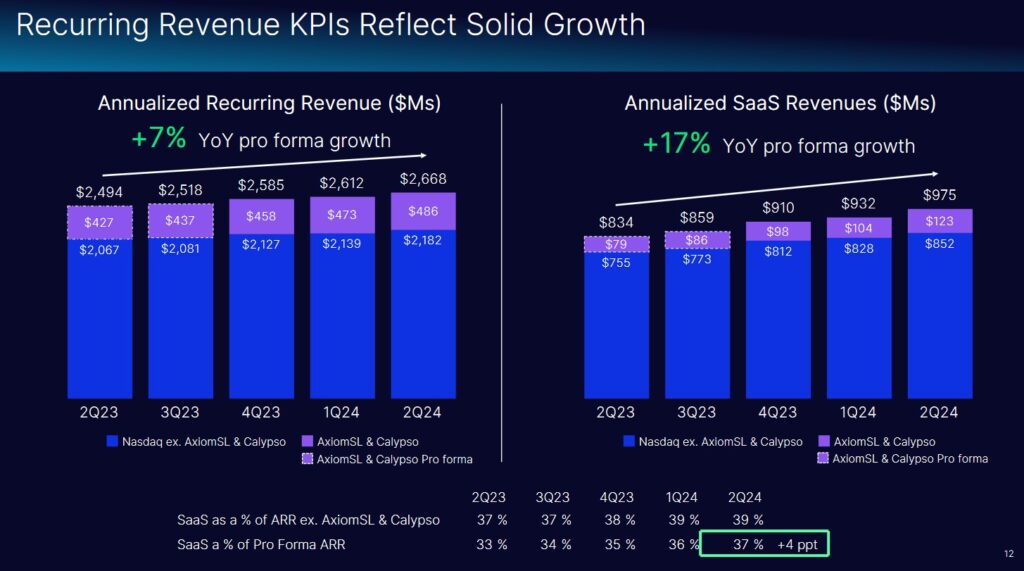

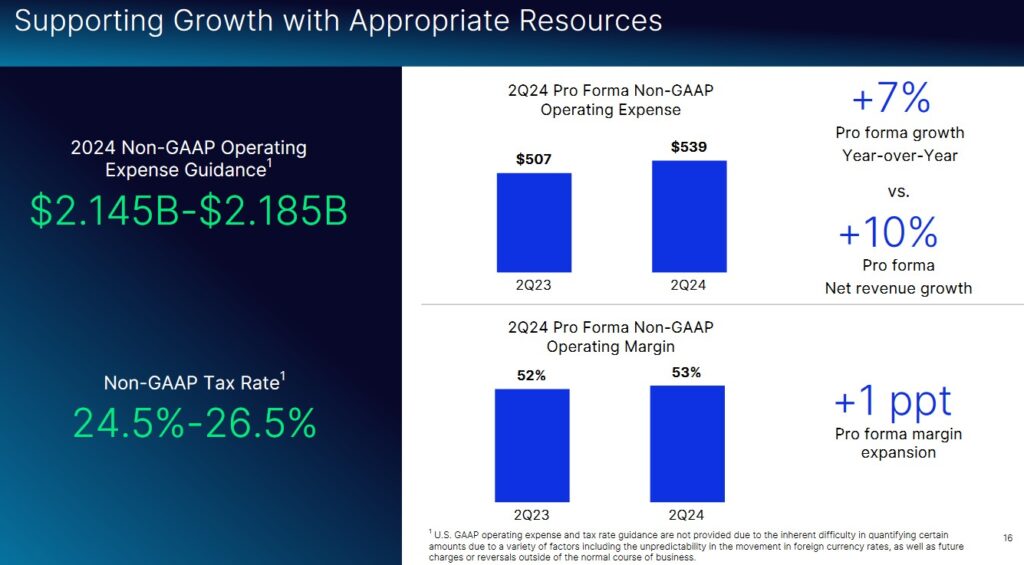

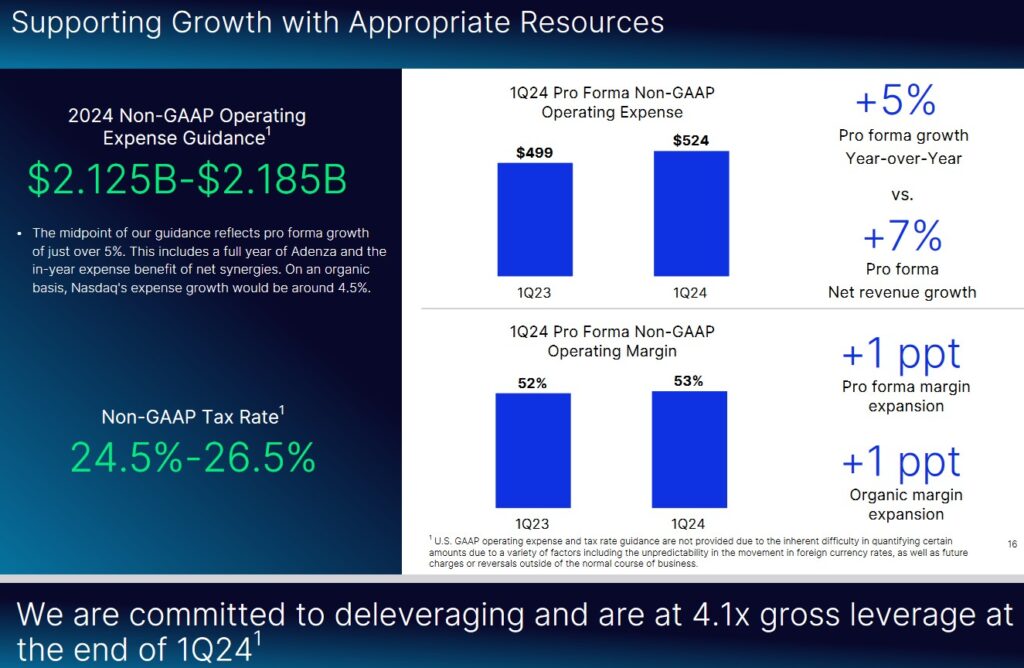

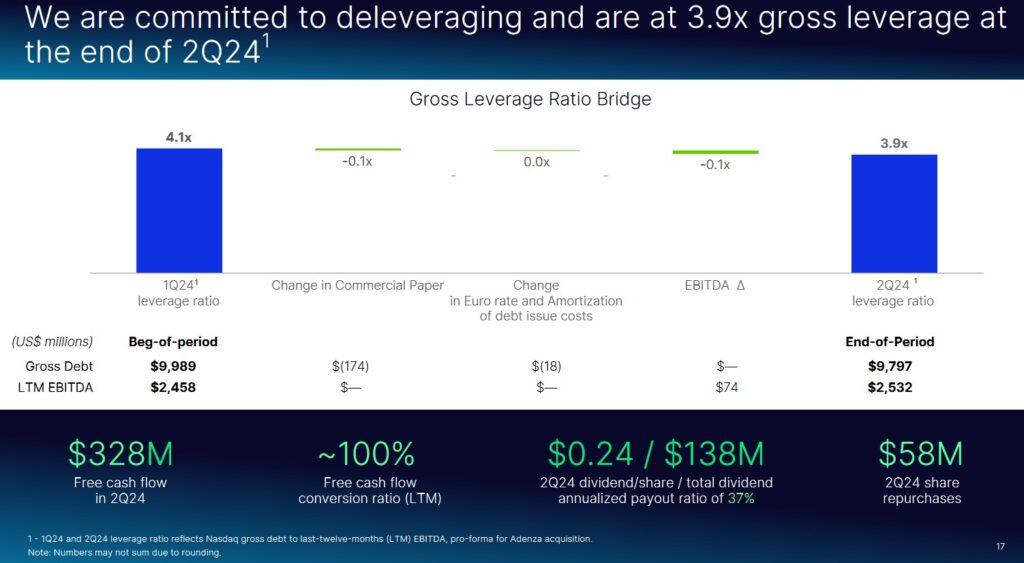

The following images extracted from the Q2 earnings presentation are but a fraction of the information NDAQ provides showing the progress being made on its integrate, innovate and accelerate 2024 strategic priorities. The integration of Adenza which NDAQ acquired from Thoma Bravo in November 2023, for example, is ahead of schedule.

Integration

NDAQ has actioned over 70% of the $80 million of net expense synergies and its leverage ratio reached 3.9x at quarter end. Both are ahead of plan.

Innovation

Approximately 50% of the employee base works with AI tools focused on enhancing productivity. By the end of Q3, 100% of NDAQ’s developers will have access to AI copilot tools.

NDAQ also continues to introduce new AI capabilities within its client-facing solutions.

Accelerate

NDAQ has set a target of exceeding $100 million in cross-sells by the end of 2027 following the Adenza acquisition in November 2023. To date, it has executed 11 fintech cross-sells. Currently ~10% of the opportunities in the sales pipeline are cross-sells with this number expected to grow.

In Q2, NDAQ welcomed 31 operating company IPOs. While the slower IPO environment remains a headwind, there are signs of improvement.

Overall growth in data and listings continue to experience challenges. The modest growth in market data and the slowly improving IPO environment were offset by the impact of prior year delistings.

Growth in the Analytics business continues to benefit from continued demand across the investment community for actionable intelligence and increased efficiency. This growth, however, was partially offset by continued headwinds in Corporate Solutions resulting in more muted growth for workflow and insights.

NDAQ’s recent acquisitions have been made with a focus on improving the percentage of annual recurring revenue (ARR). Progress is being made in this regard with the Financial Technology segment reporting ~13% ARR YoY growth and the signing of 69 new client signings, 96 upsells, and 4 cross-sells.

The Financial Crime Management Technology sub-segment signed over 50 new clients in the SMB space and NDAQ continues to progress in the Upmarket segment that focuses on Tier 1 and Tier 2 banks with a growing pipeline; just after the end of Q2, NDAQ signed a new international Tier 1 bank.

In the Regulatory Technology sub-segment, NDAQ sees sustained demand across existing and new clients as financial institutions face increasingly dynamic regulatory environment, including changes in regulation globally related to asset thresholds.

In Capital Markets Technology sub-segment, NDAQ continues to see strong demand for mission-critical technology with many clients focusing on the modernization of their infrastructure to enhance resilience and performance.

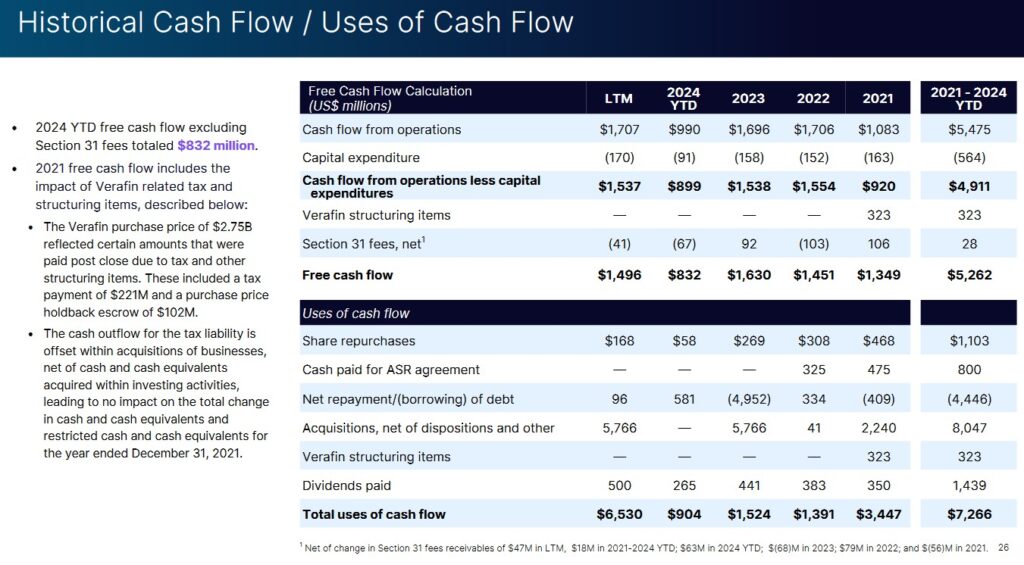

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

NDAQ’s OCF and FCF in FY2021 – YTD2024 are reflected below.

In Q1 and Q2, NDAQ generated ~$0.504B and ~$0.328B of FCF. The FCF generation in Q1 is generally elevated versus the rest of the year; there should be no alarm with the decline from Q1 to Q2.

NDAQ’s FCF conversion ratio is typically slightly higher than 100%. This year should be no different even when we consider specific onetime costs associated with the Adenza acquisition and integration.

NDAQ’s OCF, CAPEX, and FCF over a longer time frame (FY2014 – FY2023) is:

- OCF was (in B$) 0.69, 0.69, 0.72, 0.91, 1.03, 0.96, 1.25, 1.08, 1.71, and 1.70.

- CAPEX was (in B$) 0.14, 0.13, 0.13, 0.14, 0.11, 0.13, 0.19, 0.16, 0.15, and 0.16.

- FCF was (in B$) 0.479, 0.610, 0.638, 0.756, 0.926, 0.822, 1.007, 1.349, 1.451, and 1.630.

The variance in the FCF results NDAQ presents differs from online sources. This is because NDAQ makes a moderate adjustment to account for mandatory net Section 31 fees.

Return On Invested Capital (ROIC)

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

NDAQ’s FY2013 – FY2023 ROIC (%) was 5.82, 6.18, 2.43, 8.58, 5.71, 9.16, 9.39, 9.81, 9.84, and 6.99.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company’s cost of capital will be lower than this level. NDAQ’s ROIC falls short of this level but there are sufficient other metrics that make it at attractive long term investment.

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

FY2024 Guidance

NDAQ’s continues to expect modestly improving IPO activity for the remainder of 2024. The current US IPO pipeline indicates that stronger momentum is likely to start in the first half of 2025.

The ECB’s easing monetary policy is contributing to an improvement in economic prospects in the Nordics. This improvement, however, is not yet translating into a material increase in new public issuances. NDAQ’s European IPO pipeline, however, is growing and expectations are for a better 2025.

There is sustained robust trading activity in the markets and strong demand for mission-critical technology solutions from financial institutions globally. Given this, NDAQ’s markets continue to experience strong volumes; client demand for NDAQ’s fintech solutions provide a healthy backdrop for continued revenue growth across its suite of solutions.

The following is NDAQ’s current and prior FY2024 guidance.

Risk Assessment

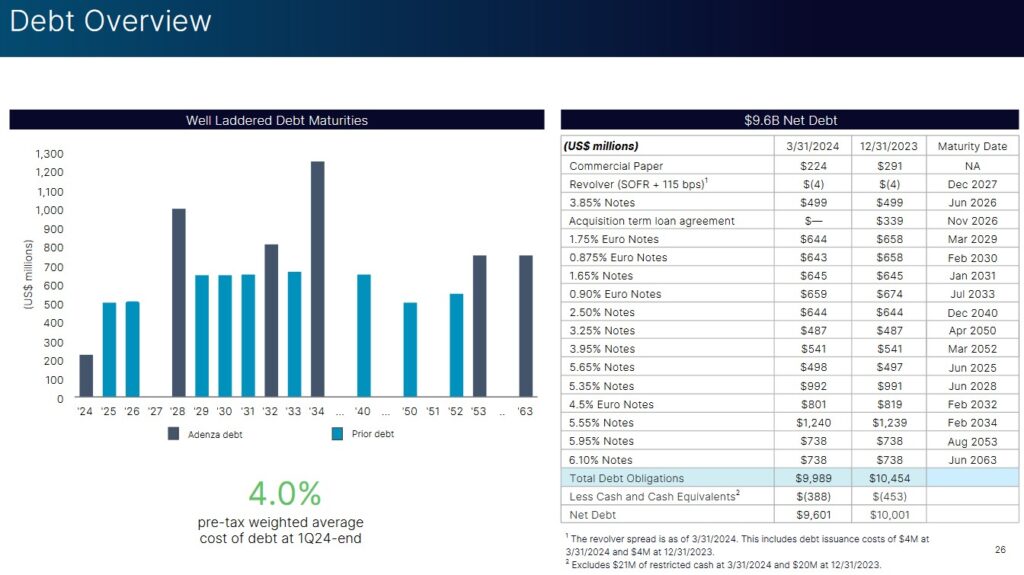

NDAQ provides debt information on its website.

In November 2021, S&P Global raised NDAQ’s domestic unsecured long-term debt credit rating from BBB to BBB+.

In December 2022, Moody’s raised NDAQ’s domestic unsecured long-term debt credit rating from Baa2 to Baa1.

S&P Global lowered NDAQ’s rating to BBB and Moody’s lowered the rating to Baa2 in June 2023 when NDAQ announced it had signed an agreement to acquire Adenza Group.

Both ratings are the middle tier of the lower medium grade investment grade category. The ratings define NDAQ as having adequate capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

Despite the rating downgrades, NDAQ has demonstrated its ability to reduce leverage within a reasonable time frame following major acquisitions.

NDAQ’s capital allocation priority over the next 3 years following the November 2023 acquisition is to reduce Gross Debt / Non-GAAP EBITDA to 4.0x in 18 months and to 3.3x in 36 months.

When I disclosed that a new NDAQ position in this June 13, 2023 post, I stated:

I do not like the degree of leverage NDAQ is taking on nor the downgrade in the credit ratings. However, I agree with management’s strategy of making transformational acquisitions as opposed to small acquisitions that will not materially impact the company’s direction.

Despite the significant increase in debt, NDAQ has demonstrated its ability to reduce leverage. NDAQ is committed to reducing leverage to 4.0x in 18 months and to 3.3x in 36 months at which time I expect rating upgrades from Moody’s and S&P Global.

I was optimistic that NDAQ would be able to achieve its deleveraging objectives. The 4.3x, 4.1x, and 3.9x gross leverage ratio at FYE2023, Q1, and Q2 2024 shows that deleveraging is proceeding according to plan.

The following reflects NDAQ’s net debt position at the end of Q1, Q2 2024 and FYE2023.

Dividends, Share Repurchases, and Stock Splits

Dividend and Dividend Yield

NDAQ’s dividend history is accessible here.

On July 25, NDAQ’s Board declared a regular quarterly dividend of $0.24/share. This is payable on September 27, 2024 to shareholders of record at the close of business on September 13, 2024.

We can expect the next 3 dividend distributions will total $0.72 (3 x $0.24). In April 2025, NDAQ’s will likely declare a $0.26 quarterly dividend. This ~8.33% increase would be consistent with recent dividend increases. If this materializes, the next 4 quarterly dividend payments will total $0.98. Using the $66.96 share price at the July 26 market close, the forward dividend yield is ~1.4%.

NDAQ’s current ~37% annualized payout ratio is within the 35% – 38% payout ratio targeted for the next 3 or 4 years.

Share Repurchases

In September 2023, NDAQ’s Board approved an increase in its share repurchase authorization to a total of $2B. As of FYE2023 and Q2 2024, there was slightly less than $1.9B remaining under the board authorized share repurchase program.

The weighted average number of shares outstanding in FY2013 – FY2023 (in millions of shares rounded) is 514, 519, 514, 506, 509, 503, 501, 501, 505, 498, and 508.4. The weighted average number of shares outstanding in Q2 2024 is ~579. The reason for the increase is because NDAQ issued 85.6 million common shares to Thoma Bravo for the Adenza purchase.

Debt reduction is a priority. NDAQ plans to continue share repurchases, however, to offset employee stock compensation. In Q2, it repurchased ~$60 million of its shares to opportunistically take advantage of the attractiveness of its depressed stock price and to start offsetting shares issued under the company’s 2024 compensation program.

After the leverage reaches target levels, the vast majority of remaining FCF will be applied toward share buybacks. Management does not anticipate making any significant acquisition-related capital allocation decisions that would deter the company from sizable stock buybacks over the coming years.

Stock Splits

NDAQ initiated a 3 for 1 stock split in 2022.

Valuation

In FY2013 – FY2023, NDAQ generated diluted EPS of $0.75, $0.80, $0.83, $0.21, $1.43, $0.91, $1.54, $1.86, $2.35, and $2.26. Its diluted PE levels were 20.52, 17.70, 27.31, 23.63, 49.57, 18.25, 33.89, 24.31, 30.57, and 26.91.

At the time of my April 26, 2024 post, shares were at ~$60.30 and using the forward adjusted diluted EPS broker estimates, NDAQ’s forward adjusted diluted PE levels were:

- FY2024 – 16 brokers – mean of $2.74 and low/high of $2.63 – $3.03. Using the mean estimate, the forward-adjusted diluted PE is ~22.

- FY2025 – 16 brokers – mean of $3.08 and low/high of $2.95 – $3.34. Using the mean estimate, the forward-adjusted diluted PE is ~19.6.

- FY2026 – 9 brokers – mean of $3.47 and low/high of $3.35 – $3.53. Using the mean estimate, the forward-adjusted diluted PE is ~17.4.

The weighted average number of shares outstanding in Q1 2024 was 578.9. I did not foresee a significant change over the remainder of FY2024. Debt reduction is a priority so any share repurchases should just offset issued shares under the company’s compensation programs.

In Q1, NDAQ generated ~$0.504B of FCF and I thought $1.7B of FCF in FY2024 was attainable. Dividing $1.7B by 580 million shares, I arrived at FY2024 FCF/share of ~$2.93. Dividing the $60.30 share price by $2.93, the forward P/FCF was ~20.6.

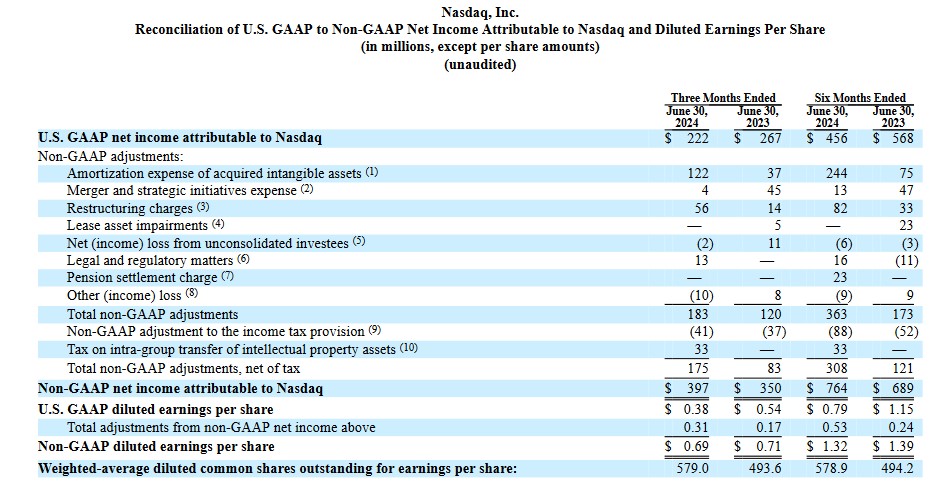

The following reflects NDAQ’s GAAP EPS and non-GAAP EPS for the first half of FY2024.

NDAQ typically generates stronger results in Q1. Given this my FY2024 forecast is:

- GAAP diluted EPS close to ~$1.55; and

- adjusted diluted GAAP EPS close to ~$2.70.

Divide the current $66.96 share price by $1.55 and we get a forward diluted PE of ~43.2. Divide it by ~$2.70 and we get a forward adjusted diluted PE of ~24.8.

Using the currently available forward adjusted diluted EPS broker estimates, NDAQ’s forward adjusted diluted PE levels are:

- FY2024 – 15 brokers – mean of $2.73 and low/high of $2.66 – $2.80. Using the mean estimate, the forward-adjusted diluted PE is ~24.5.

- FY2025 – 15 brokers – mean of $3.09 and low/high of $3.00 – $3.19. Using the mean estimate, the forward-adjusted diluted PE is ~21.7.

- FY2026 – 11 brokers – mean of $3.52 and low/high of $3.38 – $3.71. Using the mean estimate, the forward-adjusted diluted PE is ~19.02.

The weighted average number of shares outstanding in Q2 2024 was 579 and I foresee no material change over the remainder of FY2024.

NDAQ’s FCF conversion ratio is typically slightly higher than 100%.

In the first half of FY2024, NDAQ generated ~$0.832B of FCF. If NDAQ generates ~$2.70/share in FY2024 adjusted diluted EPS and we use a ~102% FCF conversation ratio, the FY2024 adjusted FCF share is ~$2.75. Assuming the weighted average diluted shares outstanding remains constant at ~579 shares, the FY2024 FCF should be ~$1.592B.

We get a forward P/FCF of ~24.8 by dividing the current $66.96 share price by $2.70. This is similar to my ~24.8 forward adjusted diluted PE estimate.

Final Thoughts

In my June 13, 2023 post, I disclosed that I had initiated a 500 share position in a ‘Core’ account within the FFJ Portfolio at ~$51/share on June 12, 2023. I subsequently acquired another 100 shares at ~$50.75 on July 19 and disclosed this purchase in this July 20, 2023 post. With the automatic reinvestment of dividend income, I now hold 608 shares. At no time when I have completed a FFJ Portfolio Review (the 2024 Mid Year FFJ Portfolio Review being the most recent) has NDAQ been a top 30 holding.

When I initiated my NDAQ position, I noted that the success of the Nasdaq 100 index made NDAQ sensitive to the volatile technology sector thus leading to volatile quarterly results. To reduce this volatility, NDAQ undertook a strategic review which led to the beefing up of its anti-financial-crimes business (now known as regulatory technologies).

Sensing that NDAQ’s strategic direction would lead to more stable results (higher annual recurring revenue (ARR)), I envisioned an increase in NDAQ’s earnings multiple once NDAQ achieved its deleveraging objectives.

The benefits from the Adenza acquisition, however, will not happen overnight. NDAQ has higher interest costs resulting from the issuance of additional debt to assist in the financing of the acquisition. Its earnings are also spread over a larger number of shares; Thoma Bravo likely negotiated the receipt of NDAQ shares as partial compensation for the Adenza sale with the expectation that NDAQ’s future value would be much higher.

In the short-term, investors should expect muted results from NDAQ. Once it reduces its Gross Debt / Non-GAAP EBITDA to target levels and the Adenza business is demonstrating steady growth, I expect NDAQ’s financial picture will permit it to aggressively resume share repurchases. This should contribute to stronger future EPS results.

I intend to increase my NDAQ exposure. Its shares, however, are currently not on sale and I will patiently wait for NDAQ’s valuation to improve.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long NDAQ.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.