This MSCI Inc. (MSCI) stock analysis is the 4th in my series of analyses of Financial Data & Stock Exchanges industry participants. Please click here to access previous posts within this series.

I view the Financial Data & Stock Exchanges industry as an attractive industry in which to invest for the long term. I currently have exposure to the following in retirement accounts, for which I do not disclose details, and/or in the FFJ Portfolio:

- S&P Global (SPGI) – guest post at Dividend Power

- Moody’s (MCO)

- CME Group (CME) – guest post at Dividend Power

- Intercontinental Exchange (ICE)

These industry participants will release earnings on the following dates. I intend to review each company shortly following their respective earnings release.

- FactSet Research Systems Inc. (FDS) – released September 28

- Nasdaq, Inc. (NDAQ) – released October 20

- S&P Global Inc. (SPGI) – released October 26

- MSCI Inc. (MSCI) – released October 26

- CME Group Inc. (CME) – released October 27

- Morningstar, Inc. (MORN) – released October 27

- Intercontinental Exchange, Inc. (ICE) – released October 28

- Moody’s Corporation (MCO) – released October 28

- CBOE Global Markets, Inc. (CBOE) – October 29

- TMX Group Limited (X.to) – November 8

Value Line, Inc. (VALU) released its Q1 2022 results for the quarter ending July 31 on September 13, 2021. This is a small-cap company ($0.31B market cap). I do not invest in small-cap companies, and therefore, do not intend to review it.

MSCI – Stock Analysis – Industry Overview

Further commentary about the industry and how industry participants are expanding into adjacent lines of business is found in my recent FactSet Research post. In that post, I mention I would not be surprised to learn that FDS may become an acquisition target; its market cap is currently ~$15.7B.

MSCI’s market cap, however, is currently above $52B yet FY2020 revenue was ~$1.7B and revenue for the first 9 months of FY2021 is ~$1.5B. I think the probability of MSCI being an acquisition target is low. It will likely continue to be the pursuer as opposed to being the pursued.

MSCI – Stock Analysis – Business Overview

On August 9, 2021, MSCI published an Investor Presentation that provides a good company overview. A quarterly update to this presentation is accessible here.

In a brief video, MSCI’s Chief Technology Officer and Head of Engineering shares how technological advancements are impacting the financial industry. On the same page is a high-level overview of MSCI’s new services to transform the investment industry.

Part 1 of MSCI’s FY2020 10-K also contains a wealth of information about the company’s history, business strategy, the competitive landscape, risk factors, and more.

MSCI – Stock Analysis – Financials

Q3 and YTD2021 Results

On October 26, 2021, MSCI released Q3 and YTD2021 results; refer to Form 8-K and the accompanying earnings presentation.

Deferred Revenue

MSCI’s subscription business model allows it to benefit from having client funds in advance of rendering services.

In FY2016 – FY2020, MSCI reported deferred revenue of $0.334B, $0.374B, $0.538B, $0.575B, and $0.676B. In the first 3 quarters of FY2021, MSCI has generated ~$0.643B. An insignificant long-term deferred revenue balance is reflected as a part of ‘Other non-current liabilities’.

Long-Term Debt

Given that two of the major rating agencies have assigned non-investment grade ratings (see below), I think it is prudent that we take a closer look at MSCI’s long-term debt obligations.

The Q3 10-Q is not yet available but we see from the schedule of long-term debt on page 14 of 55 in the Q2 10-Q that the earliest maturity date of MSCI’s senior unsecured notes is August 1, 2026; the fair value of this debt as of FYE2020 is ~$0.522B. The next long-term debt maturity date is May 15, 2027 and the fair value of this debt as of FYE2020 is ~$0.538B.

MSCI is in growth mode (see September 13, 2021 Press Release regarding the Real Capital Analytics acquisition for $0.95B and the January 21, 2020 Press Release regarding $0.19B investment to acquire a 40% stake in The Burgiss Group, LLC) so I do not envision significant prepayments on its long-term debt obligations. If there are any prepayments, it might be the result of MSCI having negotiated better terms on its debt. In fact, on pages 14 and 15 of 55 in the Q2 10-Q (link provided above), this is exactly what occurred.

Furthermore, we see from the August 17, 2021 Press Release that MSCI completed a Private Offering of $0.7B of 3.250% Senior Notes Due 2033 of which the net proceeds from the offering were used to redeem all $0.5B 5.375% senior unsecured notes due 2027. The remainder was allocated toward general corporate purposes (including, without limitation, potential purchases of its common stock, investments and acquisitions) and to pay fees and expenses incurred in connection with the offering of the notes.

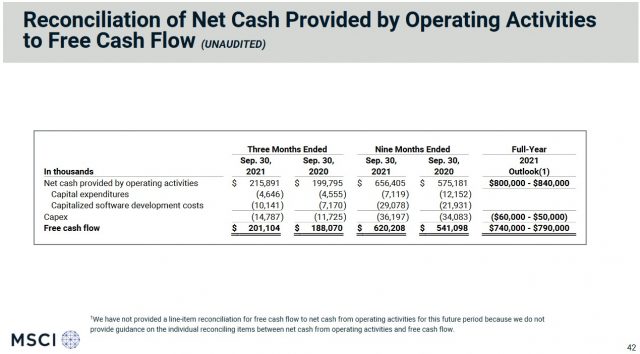

Free Cash Flow (FCF)

MSCI’s management is committed to generating strong FCF from the following comment found on page 11 of 140 in the FY2020 Annual Report:

‘We believe that free cash flow is useful to investors because it relates the operating cash flow of MSCI to the capital that is spent to continue and improve business operations, such as investment in MSCI’s existing products. Further, free cash flow indicates our ability to strengthen MSCI’s balance sheet, repay our debt obligations, pay cash dividends and repurchase shares of our common stock.’

In calculating FCF, I deduct Capital Expenditures and Capitalized Software Development Costs from Net Cash Providing By Operating Activities found on the Consolidated Statement of Cash Flows within the annual 10-Ks.

MSCI generated (in millions) 118, 170, 232, 302, 278, 255, 272, 400, 355, 564, 656, and 760 of FCF in FY2009 – FY2020. YTD2021 FCF is ~$620 and the FY2021 outlook is $0.74B – $0.79B.

I expect MSCI will have no difficulty in its ongoing ability to service its debt, repurchase shares, and increase the dividend.

FY2021 Guidance

MSCI’s FY2021 guidance is as follows.

Source: MSCI – Q3 2021 Earnings Presentation – October 26, 2021

MSCI – Stock Analysis – Credit Ratings

MSCI’s current credit ratings from Moody’s, S&P Global, and Fitch are accessible here.

- Moody’s upgraded MSCI’s domestic senior unsecured debt from Ba2 to Ba1 on April 29, 2021.

- S&P Global last reviewed MSCI on March 16, 2021 and the domestic senior unsecured debt is rated BB+.

- Fitch initiated coverage on April 29, 2021 at BBB-.

The ratings assigned by Moody’s and S&P Global are the top tier of the Non-investment grade speculative category and are non-investment grade ratings. These ratings define MSCI as being LESS VULNERABLE in the near term than other lower-rated obligors. However, it faces major ongoing uncertainties and exposure to adverse business, financial, or economic conditions which could lead to inadequate capacity to meet its financial commitments.

The rating assigned by Fitch is the lowest tier within the Lower medium grade category and is the lowest investment-grade rating. This rating defines MSCI as having an ADEQUATE capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity for MSCI to meet its financial commitments.

I am typically very hesitant to invest in companies whose domestic senior unsecured debt ratings are not investment grade. This is because I know that as an equity investor I am assuming even greater risk than unsecured debt holders.

I think, however, MSCI is on the right track to potentially receive an investment-grade rating from all rating agencies in the not too distant future.

MSCI – Stock Analysis

Dividend and Dividend Yield

MSCI does not maintain are readily accessible dividend history on its website. This information, however, is accessible on NDAQ’s website; at the time this post is being composed, this site does not reflect the recently declared $1.04/share cash dividend payable on November 30, 2021 to shareholders of record as of the close of trading on November 12, 2021.

When Q2 2021 financial results were released on July 26, 2021, MSCI announced that its Board of Directors approved a 33.3% increase to the quarterly dividend to $1.04/share. This dividend was paid on August 31, 2021; the payout ratio target is maintained at a range of 40% to 50% of Adjusted EPS.

With shares having closed at ~$637 on October 27, the $1.04 quarterly dividend yields ~0.65%.

MSCI repurchases shares from time to time at prevailing market prices in open market purchases, privately negotiated transactions, block purchase techniques or otherwise, as determined by management. The purchases are primarily funded from existing cash balances. The share repurchase program may be suspended, modified or discontinued at any time. The share repurchase program has no defined expiration date.

We see that the average shares outstanding in FY2009 – FY2020 a reduction in the share count in recent years (in millions of shares outstanding): 101, 113, 122, 123, 121, 117, 110, 97, 92, 90, 86, and 85.

The weighted average diluted shares outstanding were 83.6 million in Q3 2021 and total shares outstanding as of September 30, 2021 were 82.4 million. A total of $1.6B of outstanding share repurchase authorization remains as of October 22, 2021.

MSCI – Stock Analysis – Valuation

In the first 9 months of FY2021, MSCI has generated $6.38 in diluted EPS versus $1.41, $1.48, $1.83, $2.43, $2.03, $2.70, $3.31, $5.66, $6.59, and $7.12 in FY2011 – FY2020.

Management has not provided FY2021 diluted EPS guidance. I, however, anticipate FY2021 diluted EPS of $8.45 – $8.55. With share trading at ~$637, the forward diluted PE is ~74.5 – ~75.4.

By way of comparison, FY2011 – FY2021 diluted PE levels are 40.65, 20.94, 23.38, 25.78, 37.96, 30.89, 38.00, 32.26, 37.20, and 66.65.

MSCI has generated YTD adjusted diluted EPS of $7.44. I anticipate FY2021 adjusted diluted EPS will end up in the range of $9.85 – $9.95. On this basis, the current forward adjusted diluted PE is ~64- ~64.7.

Although the brokers which cover MSCI will very likely be amending their guidance over the coming days, the two discount brokerage platforms I use reflect the following adjusted diluted EPS guidance.

- FY2021 – 12 brokers – mean of $9.81 and low/high of $9.57 – $10.17. Using the mean estimate, the forward adjusted diluted PE is ~65 and ~63 if I use $10.17.

- FY2022 – 12 brokers – mean of $11.05 and low/high of $10.39 – $11.64. Using the mean estimate, the forward adjusted diluted PE is ~58 and ~55 if I use $11.64.

- FY2023 – 11 brokers – mean of $12.77 and low/high of $12.18 – $13.56. Using the mean estimate, the forward adjusted diluted PE is ~50 and ~47 if I use $13.40.

I view shares to be considerably overvalued.

MSCI – Stock Analysis – Final Thoughts

MSCI is well managed, it generates strong FCF, and current credit conditions have enabled the company to renegotiate some of its long-term debt under more favourable terms. Although the credit ratings are non-investment grade, I envision the ratings will eventually be upgraded to investment grade if MSCI continues to generate strong results.

Although the dividend yield is ~0.65% this does not concern me since I invest from a total potential investment return perspective. Having said this, MSCI’s current valuation is such that there is little margin for error. I do not intend to initiate a position at this time.

Stay safe. Stay focused.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long SPGI, MCO, CME, ICE and CSCO. I do not currently hold a position in MSCI and do not intend to initiate a position within the next 72 hours.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.