![]()

Summary

- MCO is one of 10 statistical rating organizations recognized by the US Securities and Exchange Commission. It is the 2nd largest publicly traded member of this small group behind S&P Global Inc..

- The company’s reputation took a hit when it completely failed to warn investors of the risks which led to the Financial Crisis.

- Secular trends such as global GDP growth and the disintermediation of credit markets in developed and emerging economies are expected to provide MCO with long-term growth opportunities.

- MCO will most likely not appeal to dividend yield hungry investors given that its dividend yield is typically sub 1.50%. The compound annual dividend growth rate over the last several years, however, is in the mid to high teens.

Introduction

This article is the first of two articles on the largest publicly traded credit rating agencies in North America.

As part of this ongoing process to scout for attractive long-term investment opportunities, it dawned on me that whenever I analyze a company I check the credit ratings assigned by the ratings agencies. Given the important role ratings agencies play I am undertaking this review to determine whether Moody’s Corporation (NYSE: MCO) would be a suitable addition to our investment holdings.

In reviewing the US Securities and Exchange Commission (‘Commission’) EDGAR database, I note that Berkshire Hathaway (NYSE: BRK.b) has held a position in MCO as far back as 2000 which is when Dun & Bradstreet split into 2 companies and took Moody’s public; BRK.b’s exposure to MCO has increased over the years.

Since Messrs. Buffett and Munger are sufficiently comfortable that MCO represents a great long-term investment despite the debacle it experienced as a result of its failure to forewarn investors of the risks which led to the Financial Crisis, I am comfortable in taking a position in MCO. The matter at hand is to determine a reasonable entry level.

Industry Overview

Most investors are familiar with MCO and perhaps a few of the other 10 statistical rating organizations (“NRSROs”) the Commission recognizes; NRSROs are organizations that provide an assessment of the creditworthiness of a company or a financial instrument.

S&P Global Inc. (NYSE: SPGI) with a ~$48B market cap and MCO with a ~$31.9B market cap are by far the two largest ratings agencies of the 10 NRSROs.

The NRSROs were recognized by the Commission through a no-action letter process until 2006 at which time Congress passed the Credit Rating Agency Reform Act (the “Reform Act”). This act added Section 15E to the Securities Exchange Act of 1934 (the “Exchange Act”) and provided the Commission with the authority to establish a registration and oversight program for credit rating agencies registered as NRSROs.

The failure of the ratings agencies to properly rate multiple financial institutions and financial instruments prior to the Financial Crisis resulted in Congress passing the Dodd-Frank Wall Street Reform and Consumer Protection Act in 2010. This Act enhanced the Commission’s oversight of the regulation of NRSROs. Through a series of rulemakings, the Commission has implemented a number of Exchange Act provisions related to NRSROs.

The credit rating agencies are essentially an oligopoly in which issuers, who want investors to acquire their debt, pay these agencies’ wages. The irony of the credit ratings process was not lost on The Financial Crisis Inquiry Commission. In its January 2011 report, the Commission noted that in order to secure favorable credit ratings from the NRSROs so as to be able to sell structured products to investors, the investment banks were paying significant fees to the rating agencies to obtain the desired ratings. In the run up to the Financial Crisis, investment banks were actually shopping around to see which agency would provide the best rating for investment vehicles.

As we have come to learn, the NRSROs were asleep at the switch prior to the Financial Crisis and many investors who relied heavily on the ratings assigned to borrowers and financial instruments suffered very heavy losses.

I distinctly remember Enron products were rated investment-grade just a few days before it failed. Even Fannie Mae and Freddie Mac had highly rated financial instruments up until mid-2008! Some of you may also recollect that AIG (the insurance behemoth at the time) had entered into credit default swaps to insure $441B of AAA-rated securities on the London market. Very shortly after this transpired, AIG had to be bailed out!

MCO was probably the worst offender amongst the ratings agencies just prior to the Financial Crisis in that it rated nearly 45,000 securities as AAA. Of all the securities which received the coveted AAA rating in 2006, 83% were ultimately downgraded.

In my opinion, a combination of pressure from financial firms that paid the ratings agencies for the ratings, the absence of meaningful public oversight, the lack of proper resources, and the relentless drive for market share all contributed to investors losing a staggering amount of money.

Business Overview

In early 2017, MCO agreed to pay ~$0.8638B to resolve a multi-year investigation into credit ratings which had been assigned to subprime mortgage securities. It paid ~$0.4375B to the justice department and $0.4263B to 21 states, the District of Columbia, and Washington, DC. This settlement was similar to that negotiated by SPGI which paid $1.375B in penalties in 2015.

In addition to this financial penalty, MCO agreed to measures designed to ensure the integrity of future credit ratings going forward, including keeping analytic employees out of commercial-related discussions.

MCO operates the following two lines of business.

Moody’s Investor Services provides credit ratings, research, and risk analysis. It rates and analyzes debt covering ~120 sovereign nations, 11,000 corporate issuers, 18,000 public finance issuers, and 64,000 structured finance obligations.

Moody’s Analytics provides leading-edge software, advisory services, and research, including the proprietary analysis of Moody’s Investors Service.

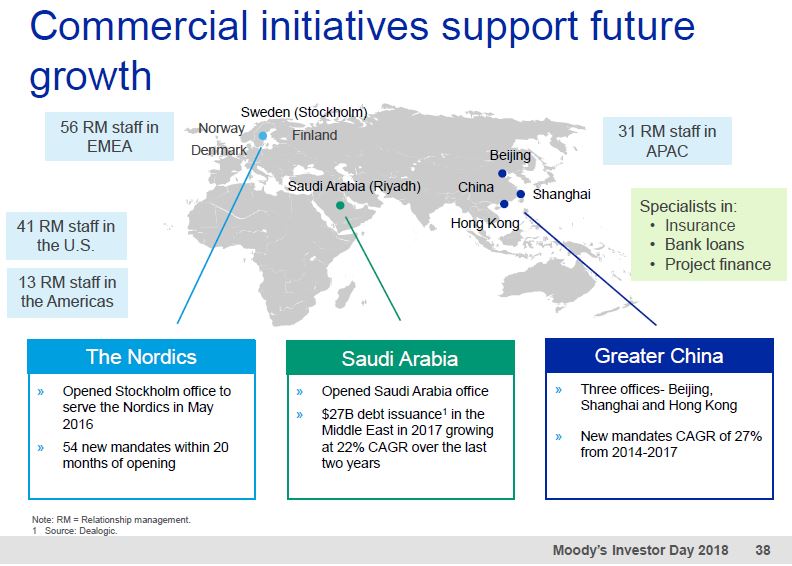

On February 28, 2018 at MCO’s Investor Day, MCO’s President and CEO highlighted the following key factors that are shaping the company’s vision and strategy.

Source: MCO Investor Day Presentation – February 28, 2018

Secular trends such as global GDP growth and the disintermediation of credit markets in developed and emerging economies are expected to provide MCO with long-term growth opportunities.

Source: MCO Investor Day Presentation – February 28, 2018

MCO’s top line has grown steadily from $1.755B in FY2008 to ~$4.2B in FY2017. Gross margin has been relatively stable during this period (70% – 72% range).

During the presentation, management stressed that MCO will continue to pursue bolt-on acquisitions. In FY2017, for example, MCO completed the $3.27B acquisition of Bureau van Dijk, a global provider of business intelligence and company information based in Amsterdam. Bureau van Dijk aggregates, standardizes and distributes one of the world’s most extensive private company datasets, with coverage exceeding 220 million companies and partnerships with more than 160 independent information providers.

The Bureau van Dijk acquisition certainly bumped up MCO’s total debt ($5.5405B as at FYE2017 versus $3.363B as at FYE2016). Management, however, fully expects the combined entity to generate immediate synergies of ~$0.045B immediately with this number reaching ~$0.08B by 2021. The acquisition is also expected to increase revenue and EPS growth rates to the high single digits.

In addition to growth via acquisition, other operating margin expansion opportunities exist. Shareholders can also expect EPS growth from continued share buybacks.

While growth opportunities exist, MCO also faces numerous risks. Should economic growth slow and/or should interest rates rise, there is the possibility the demand for corporate debt and ratings may slow from that evidenced in 2017 as many issuers took advantage of attractive rates and tight spreads in 2017.

Impact of the Tax Cuts and Jobs Act (TCJ) on MCO

MCO’s 2017 43.6% effective tax rate included a net charge in Q4 related to the impacts of tax reform in the U.S. and Europe. The effective tax rate was down from 50.6% in 2016, which included the non-deductible portion of the ~$0.8638B Settlement Charge. Excluding the net charge in 2017, the effective tax rate was 29.9%. Excluding the Settlement Charge in 2016, the effective tax rate was 31.3%.

The effective tax rate is expected to be 22% to 23% in 2018.

Q4 and FY2017 Financial Results and FY 2018 Outlook

MCO’s February 9, 2018 Earnings Release can be found here.

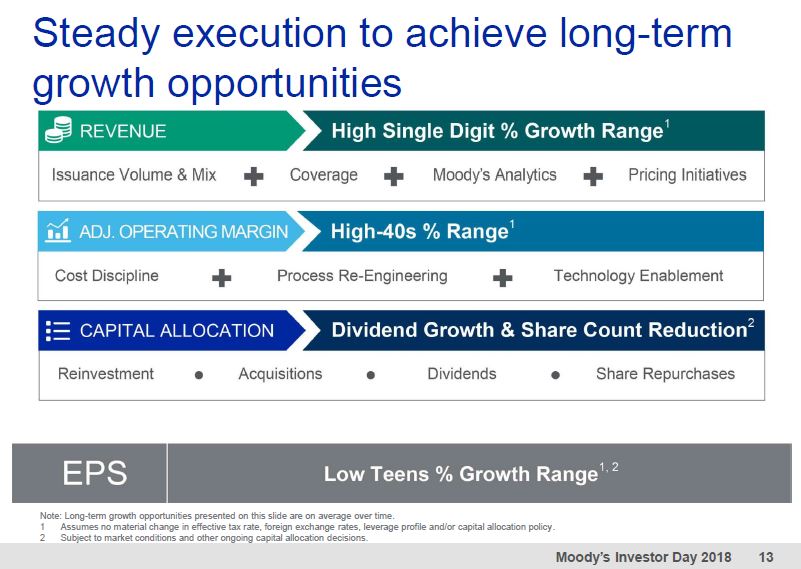

Source: MCO Investor Day Presentation – February 28, 2018

Source: MCO Investor Day Presentation – February 28, 2018

Credit Ratings

On December 31, 2017, MCO had $5.5B of outstanding debt and $0.870B of additional borrowing capacity under its revolving credit facility.

The majority of MCO’s credit ratings assigned by SPGI and Fitch are BBB+; this is a lower medium grade credit rating.

Free Cash Flow (FCF)

Cash flow from operations in 2017 was $0.7475B versus $1.3B in 2016. FCF amounted to $0.6569B versus $1.1B in 2016. These declines are due to the $0.864B Settlement Charge payment in 2017.

FCF in 2014, 2015, and 2016 amounted to $0.944B, $1.1B, and $1.1B respectively.

The FCF forecast for FY2018 is $1.6B. With ~194.2 million diluted weighted average number of shares outstanding in FY2017 I get FCF per share of $8.24. MCO closed at ~$166.94 on March 2, thus resulting in MCO trading at ~20.26 times forward FCF per share which I view as reasonable.

Valuation

FY2017 diluted EPS amounted to $5.15 versus $1.34 reported in FY2016. Adjusted diluted EPS of $6.07 was up 23% from $4.94 in 2016.

Management has forecast FY2018 diluted EPS of $7.20 – $7.40 with adjusted diluted EPS expected to be $7.65 – $7.85. These two ranges include a ~$0.65 benefit resulting from U.S. tax reform and a ~$0.20 benefit related to the tax accounting for equity compensation; the majority of the latter benefit is expected to be recognized in Q1 2018.

On the basis of MCO’s March 2 closing stock price of $166.94, I get a forward PE range of ~22.6 – ~23.2 using the projected FY2018 diluted EPS range of $7.20 – $7.40. A forward PE of ~20 or below is what I would be prepared to pay for MCO. On this basis I am looking for a price ~$148 (20 x $7.4).

Dividend, Dividend Yield, and Dividend Payout Ratio

MCO’s dividend history can be found here; MCO returned ~$0.2904B to shareholders via dividend payments during 2017.

As previously noted, MCO closed at $166.94 on March 2nd . With the recent $0.06/quarter dividend increase ($0.38 increased to $0.44 effective with the March 12th dividend payment) the $1.76 annual dividend provides investors with a forward dividend yield of ~1%.

Investors focused on equities with attractive dividend yields will likely rule out MCO as a potential investment given that its dividend yield is typically sub 1.5%.

MCO’s annual dividend growth subsequent to 2001 has been inconsistent as evidenced by the following two charts. The compound annual growth rate over the two timeframes analyzed, however, has been respectable.

The $1.52 dividend in FY2017 amounted to 29.5% of the diluted EPS of $5.15 or 25% of the adjusted diluted EPS of $6.07. The projected $1.76 annual dividend for FY2018 represents a payout ratio in the range of 23.8% – 24.4% of MCO’s projected diluted EPS or 22.4% – 23% of projected adjusted diluted EPS. Regardless of the projected EPS figure used to determine the forward dividend payout ratio, MCO’s earnings should easily cover the dividend.

Share Repurchases

The diluted weighted average number of shares outstanding in FY2017 was 194.2 million versus 195.4 million in FY2016. This compares very favorably with the 291.9 million diluted weighted average number of shares outstanding in FY2006.

In FY2017, MCO repurchased 1.6 million shares at a total cost of $199.7 million, or an average cost of $121.21/share.

As of December 31, 2017, Moody’s had $0.5B of share repurchase authority remaining.

Final Thoughts

I like that MCO provides critical services to the investment community. Secondly, the fact MCO and SPGI are the leaders in their industry greatly appeals to me.

Yield hungry investors will likely have no interest in MCO. Furthermore, some investors will automatically rule out MCO as a potential investment since it has not consistently raised its dividend every year since becoming a publicly traded company in 2000. Neither of these two factors are deal breakers from my perspective. I seek companies with competitive advantages and look for overall potential returns (dividends and capital gains) as opposed to just growth in dividend income; despite the YoY volatility in MCO’s dividend, MCO has an attractive long-term compound annual dividend growth rate.

An added bonus is that management is prepared to repurchase outstanding shares when the stock price is attractive; the weighted average number of diluted shares outstanding has been reduced by almost 98 million since FY2006.

While there are risks associated with an investment in MCO, I take some comfort in that additional oversight authority was granted to the US Securities and Exchange Commission in recent years. I am also confident MCO’s management is well aware of the potentially irreparable damage to MCO’s reputation if another debacle were to occur; I am confident that systems, procedures, and processes are now in place to avoid another major blunder.

I fully intend to initiate a position in MCO but will patiently wait for a ~$148 or lower entry price. This would be a pullback of ~10% which I am cautiously optimistic will occur in 2018.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I do not currently hold a position in any company referenced herein and do not intend to initiate a position within the next 72 hours.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.