S&P Global’s (SPGI) current valuation and long-term outlook are such that I recommend you invest in S&P Global (SPGI) to create long-term wealth.

In my October 27, 2021 post, I conclude that SPGI is very likely to be a far more valuable company once it merges with IHS Markit (INFO). At the time, however, the valuation was too high to acquire additional shares. SPGI was trading at ~$465 and FY2021 GAAP guidance was $12.50 – $12.65 thus giving us a forward valuation of ~36.8 – ~37.2.

I conclude that post stating that I would want to see management’s FY2022 guidance after the merger completion before acquiring additional shares.

Despite the merger not having closed (expectations are for a closing before March 31, 2022), I have purchased 100 shares ~$397/share following the release of Q4 and FY2021 results on February 8, 2022. These shares have been added to my existing position within a ‘Core’ account in the FFJ Portfolio.

SPGI was my 18th largest holding when I completed my Investment Holdings Review in early January 2022; it was my 21st largest holding in mid-April 2021 and my 24th largest holding in mid-August 2020.

At the time of my January review, I held a total of 300 shares and the share price was ~$447. I now hold 400 shares and the share price is ~$399. The decline in SPGI’s share price is of little concern to me since I am more interested in a company’s valuation.

Financials

Q4 and FY2021 Results

SPGI’s Q4 and FY2021 results are found in the Form 8-K and Earnings Presentation.

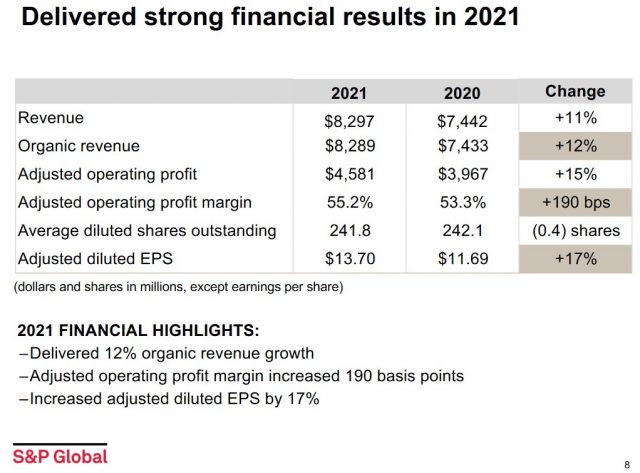

In addition to delivering strong financial results, SPGI made significant progress on its key initiatives.

The most important initiative has been preparing for the merger. SPGI is well prepared to rapidly begin operating as one company and to begin to realize cost and revenue synergies upon closing.

FY2021 adjusted diluted EPS of $13.70 exceeded the original FY2021 guidance of $12.25 – $12.45.

Its 55.2% adjusted operating profit margin exceeded the original guidance of 53.8% – 54.3%. Much of this was due to the unexpected outperformance in SPGI’s ‘ratings’ business segment following a very strong 2020.

SPGI’s revenue over the past 4 years has posted a compound annual growth rate of ~8%.

The annual adjusted operating profit margin expansion over the same timeframe has averaged 217 bps; this has resulted in a near doubling of adjusted diluted EPS over 4 years.

On the Q3 2020 earnings call, management introduced a new $0.12B productivity program to be completed over a 2 – 3 year period. This program is largely complete after only 18 months.

There remain a few small procurement projects that await the close of the merger to take advantage of the increased scale of the combined company. All productivity efforts, however, will now focus on achieving the merger synergies.

SPGI has low leverage and ample liquidity with ~$6.5B of cash and cash equivalents and ~$4.1B of debt.

Adjusted gross debt to adjusted EBITDA has improved since FYE2020 to 1.8x.

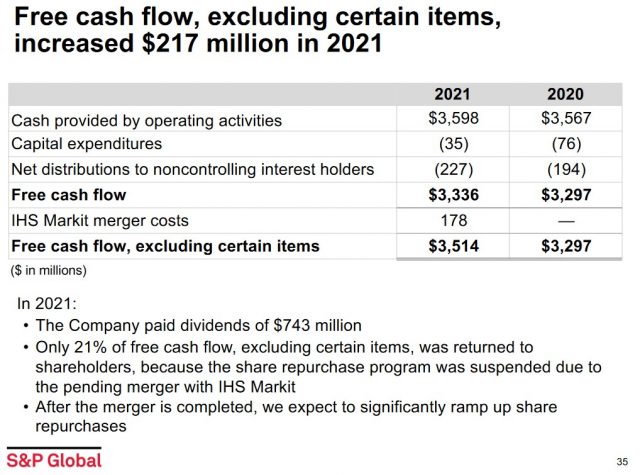

Free cash flow, excluding certain items, was $3.5B in FY2021. This is a ~$0.217B increase, or 7%, over FY2020.

FY2022 Outlook

Management will host an investor call to provide an update on the merged company strategy, business segment details, synergies, investment programs, share repurchase plans, and guidance after the merger is completed.

Credit Ratings

Moody’s continues to rate SPGI’s senior domestic unsecured debt at the A3 level. This rating is stable and is the lowest tier of the upper-medium grade investment-grade category.

The rating defines SPGI as having a VERY STRONG capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

SPGI is the world’s largest global rating agency. I do not think it is prepared to jeopardize its investment-grade credit rating.

I deem my risk exposure to be well within my tolerance for risk.

Dividend and Dividend Yield

The dividend history found on SPGI’s website dates back to 1995. It, however, has distributed a dividend for almost 50 years.

A decision was made not to increase the $0.77 quarterly dividend until the merger closes; the Board is to revisit the dividend policy for the combined company following the closing.

The next $0.77/share quarterly dividend is payable on March 10, 2022 to shareholders of record on February 10, 2022.

The dividend yield was 0.066% based on the ~$465 share price when I reviewed SPGI in October 2021. The dividend yield is now ~0.078% based on my recent ~$397 purchase price.

Capital gains will very likely continue to be the primary manner in which investors will benefit from an investment in SPGI. Given this, it is exceedingly important to acquire shares at an attractive valuation.

SPGI’s weighted average number of shares outstanding over the FY2011 – FY2021 timeframe (in millions of shares) is 304, 285, 280, 272, 275, 265, 259, 253, 247, 242, and 241.

The repurchase of treasury shares in FY2018 – FY2020 amounted to $1.66B, $1.24B, and $1.164B. Share repurchases were suspended upon the announcement of the merger. Share repurchases, however, remain a component of SPGI’s total capital return program and management expects to significantly ramp up share repurchases after the merger is completed.

Valuation

At the time of my October 27, 2021 post, shares were trading at ~$465 and FY2021 GAAP guidance was $12.50 – $12.65 resulting in a forward valuation of ~36.8 – ~37.2.

FY2021 adjusted diluted EPS guidance was $13.50 – $13.65 thus giving us a forward adjusted diluted PE range of ~34.1 – ~34.4.

The forward adjusted diluted PE levels using the ~$465 share price and earnings estimates from the brokers which cover SPGI were:

- FY2021 – 18 brokers – mean of $13.36 and low/high of $13.05 – $13.84. Using the mean estimate and the current share price, the forward adjusted diluted PE was ~34.8.

- FY2022 – 18 brokers – mean of $14.49 and low/high of $13.72 – $15.30. Using the mean estimate and the current share price, the forward adjusted diluted PE was ~32.

- FY2023 – 16 brokers – mean of $15.97 and low/high of $14.95 – $17.18. Using the mean estimate and the current share price, the forward adjusted diluted PE was ~29.

Fast forward to my February 8, 2022 ~$397 purchase price and $12.51 in FY2021 diluted EPS; the diluted PE is now ~31.7. FY2021 adjusted earnings were $13.70 thus resulting in an adjusted diluted PE of ~29.

Management is not providing guidance. However, the current broker adjusted diluted EPS estimates, are:

- FY2022 – 15 brokers – mean of $14.69 and low/high of $14.05 – $15.30. Using the mean estimate and the ~$397 share price, the forward adjusted diluted PE is ~27.

- FY2023 – 13 brokers – mean of $16.20 and low/high of $15.41 – $17.36. Using the mean estimate and the ~$397 share price, the forward adjusted diluted PE is ~24.5.

I think the current broker estimates will be revised higher once the merger is complete.

Final Thoughts

SPGI has demonstrated its ability to create long-term wealth. Over the past 10 years, the average annual total return without the reinvestment of dividends is ~25%. In contrast, the S&P 500’s return over the same timeframe is ~14%.

I think investors should reasonably expect double-digit annual returns to persist following the merger.

Applying the rule of 72, an investment in SPGI should double in value in 4 years if SPGI’s average annual total return only comes in at 18%.

It was not my intent to add to my SPGI position until I could review the numbers for the combined entity. The current valuation, however, is too reasonable to pass up.

SPGI’s share price may experience an even further pullback from its ~$484 52-week-high. Given that I invest in SPGI to create long-term wealth, however, any further pullback is of little concern to me. I would simply acquire additional shares if the valuation were to improve from the current level.

I wish you much success on your journey to financial freedom!

Note: Thanks for reading this article. Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long SPGI.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.