Investors typically invest in BCE Inc. (BCE) for dividend income and safety. The probability of significant capital gains, however, is low. This is even more so given BCE’s current valuation.

I last reviewed BCE in this guest post at Dividend Power at which time its Q2 and YTD2021 results were the most current.

On February 3, 2022, BCE released Q4 and FY2021 results and FY2022 Outlook. This post is based on this recently released information.

NOTE: All dollar values reflected herein are in CDN $.

Before I delve into my BCE analysis, I caution that my investment recommendations are tailored to my family’s needs.

I focus on generating attractive long-term total investment returns while taking into consideration ‘credit’ risk. Your investment objectives and goal, risk tolerance, tax bracket, and other factors might differ entirely from mine.

I mention this because of correspondence I had with a reader in November 2021 at which time BCE was trading at CDN ~$65. This reader wanted my opinion about BCE given his significant BCE exposure; he had read a ‘Sell’ recommendation on another blog.

I cautioned that this ‘Sell’ recommendation is made without knowing anything about him.

Although I do not advocate investing based on dividend income/yield, perhaps this investor depends on a safe and reliable stream of dividend income. Capital gains potential may be of far lesser importance.

In addition, investment decisions need to consider the type of investment account in which shares are held. Suppose this investor’s BCE shares are held in a taxable account and the average cost base is well below the current market price. The sale of these shares would trigger a capital gain at the most inopportune time.

Any investment decision MUST be appropriate given your circumstances!

Business Overview

Please refer to my guest post at Dividend Power for which a link is provided above.

The Overview section of BCE’s website and the FY2020 Annual Report together with other information accessible here provide investors with a great overview of the company.

Financials

Q4 and FY2021 Results

Please refer to BCE’s Q4 Press Release and Earnings Presentation.

BCE has steadily improved results each quarter since Q2 2020 and is now essentially at 2019 levels having reached approximately 99% of pre-COVID consolidated revenue and adjusted EBITDA in 2021.

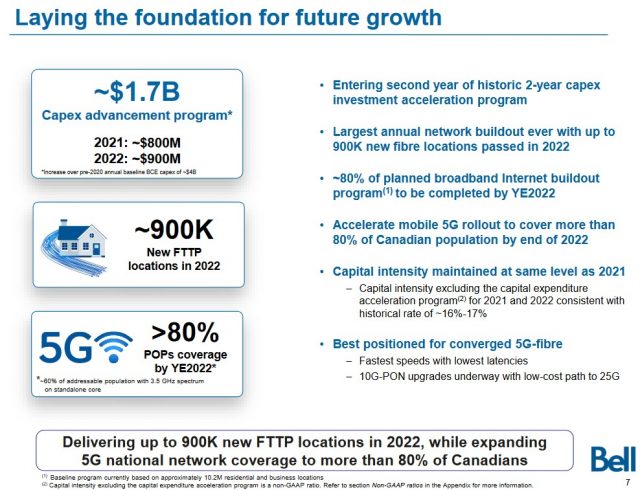

In 2021, it surpassed its network expansion targets by delivering ~1.1 million new locations equipped with either direct fibre or wireless home internet connections. It also expanded mobile 5G coverage to more than 70% of Canadians and completed its Wireless Home Internet buildout program for hundreds of rural communities one year earlier than originally planned.

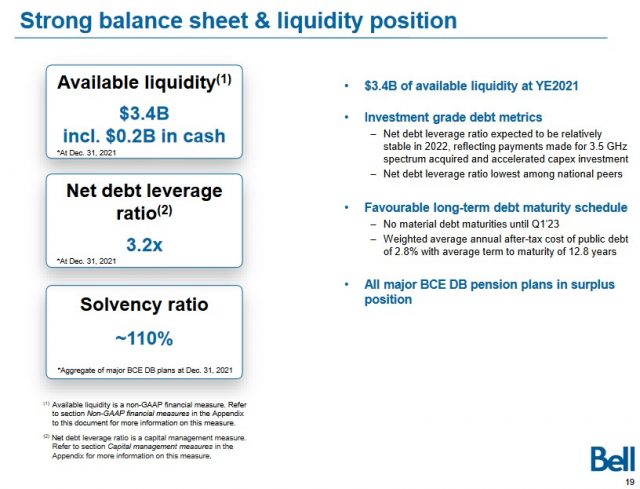

Defined Benefit (DB) Pension Plans

The solvency ratio across the major DB pension plans was above 105% at the end of 2021; the Bell Canada DB is the largest of all within the BCE group of companies and its solvency ratio was 111%. With surplus positions of over 105%, contribution holidays can now be taken on the annual cash funding which totals ~$0.2B in aggregate across all BCE plans.

BCE, however, can only take advantage of a partial reduction in 2022 because its final actuarial evaluations were filed at the end of June 2021. As a result, BCE’s pension cash funding for 2022 is projected to be ~$0.075B lower than ~$0.275B in all of 2021.

Management expects that BCE will be able to take advantage of full cash funding closer to ~$0.2B in 2023. Expectations are for this level to continue for the foreseeable future as projections call for each defined benefit pension plan’s solvency ratio to remain above the mandatory 105% threshold.

Given these foreseeable future projections, management expects a ~$1B free cash flow (FCF) opportunity over the next five years. This was not incorporated in the long-range plans formulated a few years ago.

Capital Expenditures (CapEx)

BCE is a highly capital-intensive business. In FY2016 – FY2021, CAPEX was $3.771B, $4.034B, $3.971B, $3.988B, $4.202B and $4.837B.

FY2022’s capital investment will be ~$5B as BCE continues with its ambitious annual fibre buildout and the launch of a stand-alone 5G core that will enable faster data speeds than what is currently available. With even more fibre and 5G growth upside on the horizon and a cost structure that reflects these advantages, management expects to realize operational benefits sooner which will support free cash flow growth.

The ~$5B of FY2022 CapEx includes ~$0.9B in accelerated investment on top of the ~$4B in baseline CapEx typically spent each year over the last decade. This compares to a total CapEx of $4.837B in 2021 which included ~$0.8B of incremental spending under the first year of the 2 year capital advancement program.

Free Cash Flow (FCF)

BCE’s FY2019 – FY2021 FCF is $3.738B, $3.348B, and $2.995B.

FY2020 FCF decreased by $0.39B in 2020, compared to 2019, mainly due to higher capital expenditures and lower cash flows from operating activities, excluding cash from discontinued operations and acquisition and other costs paid.

FY2021 FCF decreased by $0.353B, compared to 2020, mainly as a result of higher capital expenditures.

Debt

A public debt schedule is accessible here. This schedule includes BCE and Bell Canada debt and pref shares.

BCE’s long-term debt maturity schedule has an average term of fewer than 13 years and an after-tax cost of debt of just 2.8%; there are no material debt refinancing requirements until March 2023.

However, BCE will access debt markets if market conditions are favourable in 2022 to:

- strengthen its liquidity position;

- extend durations ahead of the maturities; and

- finance various spectrum auctions that occur over the next few years.

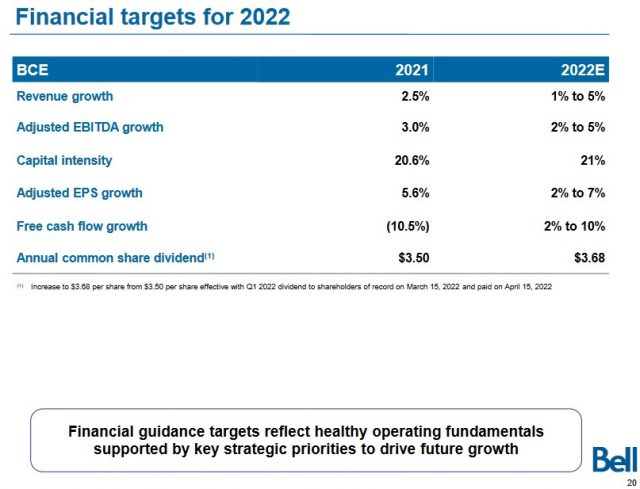

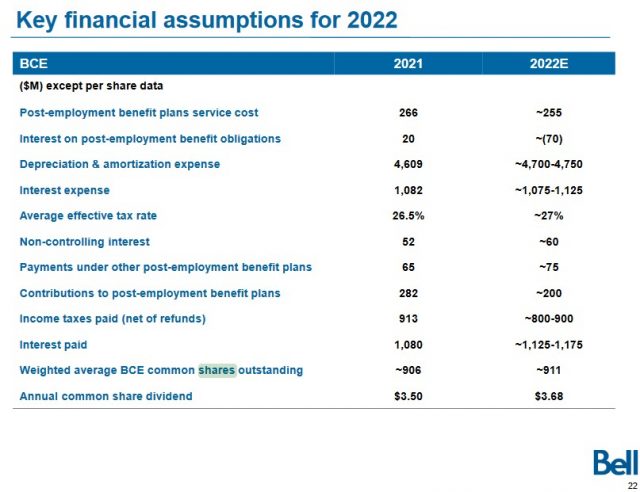

FY2022 Outlook

BCE’s Q4 and FY2021 Earnings Presentation contains a multi-page FY2022 Financial Outlook section.

On the FY2021 earnings call, management indicates 2021 was a reset year. The FY2022 financial targets are based on BCE transitioning toward a return to pre-pandemic levels of financial performance and operating momentum.

The following is a recap of BCE’s FY2022 targets and the assumptions upon which they are based.

These ranges are based on BCE’s current outlook for 2022 taking into account the impact of COVID-19 on the 2021 consolidated financial results.

For FY2022, expectations are for growth in adjusted EBITDA, a reduction in contributions to post-employment benefit plans and payments under other post-employment benefit plans, and lower cash income taxes thus leading to higher FCF.

Credit Ratings

I consider the ratings assigned to the senior unsecured long-term debt in my analysis if a company’s debt is rated by major rating agencies. As a shareholder, I know that my credit risk is far greater than that of any debtholders. I, therefore, typically pass on investing in a company if non-investment grade credit ratings are assigned to a company’s senior unsecured long-term debt.

BCE’s current credit ratings are accessible here.

All 3 ratings are the top tier of the lower medium grade investment-grade category.

These ratings define BCE as having an adequate capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity to meet its financial commitments.

BCE’s ratings are acceptable for my purposes.

Dividend and Dividend Yield

BCE offers investors:

- a reliable stream of dividend income;

- a relatively consistent track record of dividend increases after The Financial Crisis; and

- an attractive dividend yield.

On the Q4 and FY2021 earnings call, management often stresses the company’s dividend growth plans.

As I compose this post, the dividend history on BCE’s website does not reflect the 5.1%, or $0.18/share, increase in the BCE annual common share dividend to $3.68 that was declared on February 3, 2022. The first $0.92/share dividend (increased from $0.875/share) is payable on April 15, 2022 to shareholders of record at the close of business on March 15, 2022.

This increase marks the 14th consecutive year of a 5% or higher dividend increase.

With BCE currently trading at ~$68, the forward dividend yield is ~5.4%.

The dividend payout ratio in FY2022 will remain above BCE’s historical 65% – 75% target range due to the 2nd year of a 2–year capital expenditure acceleration plan. The dividend is supported by 2022 FCF growth and substantial available liquidity.

NOTE: BCE defines the dividend payout ratio as dividends paid on common shares divided by free cash flow. It considers this ratio to be an important financial strength and performance indicator because it shows the sustainability of the dividend payments.

BCE’s weighted average diluted shares outstanding in FY2012 – FY2021 (in millions) is 775, 776, 795, 848, 870, 895, 899, 901, 904, and 911.

A reduction in the issued and outstanding shares is not a key priority in the use of Free Cash Flow; the FY2022 key financial assumptions reflect no change from the current ~911 million weighted average diluted shares outstanding.

Valuation

BCE’s diluted PE in FY2011 – FY2020 is 15.28, 12.58, 15.38, 17.94, 17.64, 18.36, 18.69, 17.68, 18.18, and 21.60.

In my guest post at Dividend Power, I indicate that when BCE released Q4 2020 results on February 4, 2021, it reported FY2020 adjusted diluted EPS of $3.02 and forecast FY2021 adjusted diluted EPS of $3.05 – $3.20.

At the end of Q2 2021, BCE had generated $1.61 in YTD adjusted diluted EPS. I, therefore, did not think it was unreasonable that FY2021 adjusted diluted EPS would fall within guidance.

Using the ~$63.70 share price at the time and the ~$3.13 midpoint of guidance, the forward-adjusted diluted PE was ~20.4.

In addition, adjusted diluted EPS guidance from 17 brokers was:

- FY2021 – a mean of $3.20 and a low/high range of $3.11 – $3.30. Using the current share price and the mean estimate, the forward adjusted diluted PE was ~20.

- FY2022 – a mean of $3.38 and a low/high range of $3.09 – $3.53. Using the current share price and the mean estimate, the forward adjusted diluted PE was ~18.85.

BCE’s Q4 and FY2021 results reflect $2.99 in diluted EPS and $3.19 in adjusted diluted EPS. With shares currently trading at ~$68, the diluted PE is ~22.7 and the adjusted diluted PE is ~21.3.

Management’s FY2022 Adjusted EPS growth target is 2% – 7% thus giving us a range of ~$3.25 – ~$3.41. Using the ~$68 share price, the forward adjusted PE range is ~20 – ~21.

Broker guidance from the two online trading platforms I use and the ~$68 share price gives us the following:

- FY2022 – 16 brokers – mean of $3.38 and low/high of $3.23 – $3.68. Using the mean estimate, the forward adjusted diluted PE is ~20.

- FY2023 – 12 brokers – mean of $3.59 and low/high of $3.34 – $3.93. Using the mean estimate, the forward adjusted diluted PE is ~19.

- FY2024 – 2 brokers – mean of $3.80 and low/high of $3.69 – $3.90. Using the mean estimate, the forward adjusted diluted PE is ~18.

I am disregarding FY2024 estimates because only 2 brokers provide estimates.

BCE’s current valuation is too high for me. There is certainly a possibility BCE’s share price could tick up slightly in the short term. However, investors should not rule out that BCE’s share price comes under pressure in a rising interest rate environment.

Final Thoughts

BCE was my 21st largest holding when I completed my Investment Holdings Review in early January 2022; it was my 23rd largest holding in mid-April 2021 and my 20th largest holding in mid-August 2020.

I have not been aggressively increasing my exposure to BCE in the last few years because its annual growth rate is low and its valuation has been high.

Both the dividend and dividend yield are attractive. I, however, look at an investment’s total potential return which also accounts for potential capital gains. I do not envision significant capital gains potential from BCE.

Any increase in my BCE exposure will be limited to the automatic reinvestment of dividends.

I wish you much success on your journey to financial freedom!

Note: Thanks for reading this article. Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BCE.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.