Intercontinental Exchange (ICE) is attractively valued so I have acquired an additional 200 shares @ ~$127 in one of the ‘Side’ accounts within the FFJ Portfolio.

ICE did not fall within my top 30 holdings when I completed my January 2022 Investment Holdings Review. With this recent purchase, I now hold 600 shares but ICE is not yet one of my top 30 holdings.

At the time of my October 28, 2021 analysis, shares were trading at ~$135.50 and the valuation was reasonable. I now revisit ICE after its February 3, 2022 release of Q4 and FY2022 results that exceed expectations.

Business Overview

A business overview has been provided in previous posts.

Please read Part 1 of ICE’s FY2021 10-K in which there is a comprehensive overview of the company’s history, business strategy, competitive landscape, risk factors, and more.

Financials

Q4 and FY2021 Results

Please refer to ICE’s FY2021 Form 10-K, earnings release and earnings presentation.

ICE has diversified its business so that it is less dependent on volatility or transaction activity in any one asset class. In addition, it has increased the portion of recurring revenues from 34% in FY2014 to 49% in FY2021. These recurring revenues include data services, listings and various mortgage technology solutions.

The following images show the extent to which ICE’s performance has improved over the past 9 fiscal years.

Source: ICE – Q4 and FY2021 Earnings Presentation – February 3, 2022

Source: ICE – Q4 and FY2021 Earnings Presentation – February 3, 2022

We see from ICE’s consistent track record of growth that it has a proven ability to reward long-term shareholders.

Source: ICE – Q4 and FY2021 Earnings Presentation – February 3, 2022

Free Cash Flow

ICE is not a capital-intensive business such as railroads and automobile manufacturers. This results in a significant portion of its net cash provided by operating activities being available for debt reduction, acquisitions, share repurchases, and dividend growth.

Source: ICE – Q4 and FY2021 Earnings Presentation – February 3, 2022

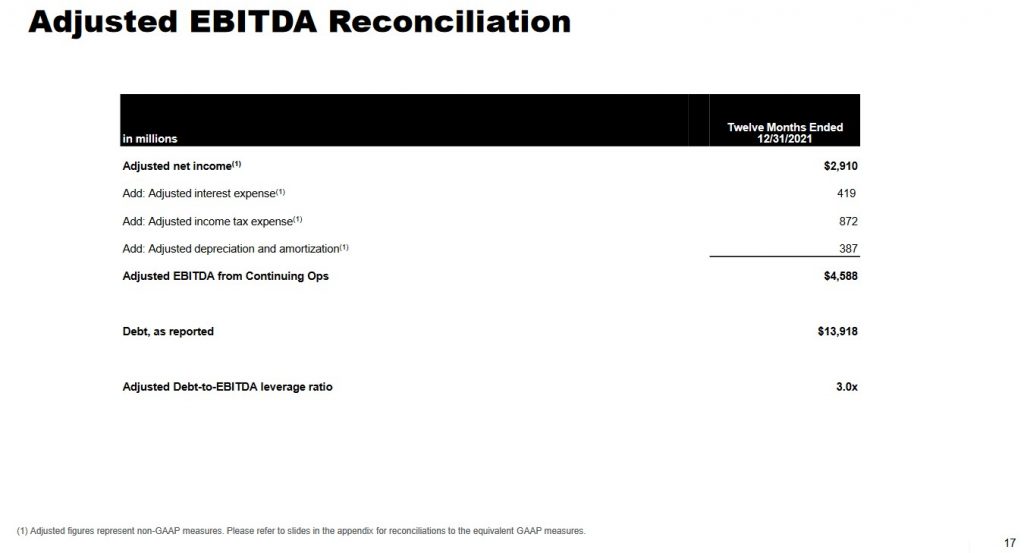

Debt

The following is a schedule of ICE’s Long-Term Debt as of December 31, 2021. In comparison, the total outstanding debt at the end of Q3 was $14.225B of which $1.831B was total short-term debt.

Source: ICE – FY2022 Form 10-K

As of December 31, 2021, ICE had $13.9B in outstanding debt, consisting of $12.9B of fixed-rate senior notes, $1.0B under its USD commercial paper program, and $10 million under credit lines at its ICE India subsidiaries.

The fixed-rate senior notes have a weighted average maturity of 15 years and a weighted average cost of 2.9% per annum.

As of December 31, 2021, the commercial paper notes had original maturities ranging from 3 – 73 days, with a weighted average interest rate of 0.33% per annum, and a weighted average remaining maturity of 26 days.

FY2022 Guidance

ICE’s Fy2022 guidance is reflected below.

Credit Ratings

Moody’s downgraded ICE’s senior unsecured long-term debt credit rating from A2 to A3 following the Ellie Mae acquisition; the revised rating is the lowest tier of the upper-medium investment-grade category.

At the time of my previous review, S&P Global had assigned a BBB+ rating which is one notch lower than Moody’s rating. On November 29, 2021, S&P Global raised the rating to A- citing:

- the dominance of revenues from subsidiaries free of regulatory capital restrictions; and

- good progress in reducing debt, with adjusted debt-to-EBITDA of 3.1x at Sept. 30, 2021 (down from 4.0x the close of the Ellie Mae acquisition in the Fall of 2020) due to solid cash flow generation and the sale of ICE’s stake in Coinbase.

Both ratings are now the bottom tier of the upper-medium grade investment-grade category and the outlook is stable.

Source: ICE – Q4 and FY2021 Earnings Presentation – February 3, 2022

These ratings define ICE as having a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

ICE’s ratings are acceptable for my purposes.

Dividend and Dividend Yield

ICE’s dividend history is accessible on the NASDAQ website; ICE does not maintain its dividend history on its website.

At the time of my prior review, ICE’s quarterly dividend was $0.33. With shares trading at ~$135.50, the dividend yield is just shy of 1%.

On February 3, 2022, ICE announced a ~15% increase in its quarterly dividend to $0.38/share resulting in a ~1.2% dividend yield based on my ~$127 purchase price.

ICE’s weighted average diluted shares outstanding in FY2012 – FY2021 (in millions) is 365, 395, 573, 559, 599, 594, 579, 565, 555, and 565.

Following the $11B acquisition of Ellie Mae from Thoma Bravo in September 2020, share repurchases were suspended until leverage fell below 3.25 times Adjusted Debt-to-EBITDA.

This level was attained in Q4 and ICE reinstated its share repurchases and acquired $0.25B of outstanding shares during the quarter.

The weighted average share count for Q1 2022 is expected to be 562 million – 568 million. This excludes the impact of any potential share repurchases.

Valuation

ICE’s diluted PE in FY2011 – FY2020 is 18.52, 16.46, 29.52, 66.86, 24.11, 23.09, 25.66, 17.00, 25.15, and 31.76. It has generated $4.48 in YTD2021 diluted EPS and I envision FY2021 EPS of ~$5.60. Using this estimated range and the current share price, the forward diluted PE is ~24.

Please reference my August 9, 2021 post in which I provide ICE’s valuation based on adjusted diluted EPS at the time I initiated a position in August 2020 and at the time of subsequent ICE posts.

When I wrote my October 28, 2021 post, ICE was trading at ~$135.50 and broker guidance derived from the two online trading platforms I use was:

- FY2021 – 18 brokers – mean of $5.02 and low/high of $4.87 – $5.16. Using the mean estimate, the forward adjusted diluted PE is ~27.

- FY2022 – 18 brokers – mean of $5.40 and low/high of $5.06 – $5.81. Using the mean estimate, the forward adjusted diluted PE is ~25.

- FY2023 – 16 brokers – mean of $5.95 and low/high of $5.41 – $6.41. Using the mean estimate, the forward adjusted diluted PE is ~22.8.

Using my ~$127 purchase price and broker guidance, I now get:

- FY2022 – 19 brokers – mean of $5.59 and low/high of $5.41 – $5.78. Using the mean estimate, the forward adjusted diluted PE is ~22.7.

- FY2023 – 17 brokers – mean of $6.13 and low/high of $5.85 – $6.33. Using the mean estimate, the forward adjusted diluted PE is ~20.7.

- FY2024 – 4 brokers – mean of $6.76 and low/high of $6.58 – $7.03. Using the mean estimate, the forward adjusted diluted PE is ~18.8.

I am disregarding FY2024 estimates because so few brokers have provided input.

I anticipate these broker estimates will be adjusted higher in the coming days.

Final Thoughts

I deem ICE to be a high-quality company that is likely going to continue to reward shareholders with attractive total investment returns.

Management has reduced adjusted debt-to-EBITDA as forecast and share repurchases have been reinstated. Couple share repurchases with further debt reduction and dividend increases and I think investors can realistically expect total investment returns in the upper teens; ICE’s average annual total return over the past 10 years is ~19%.

Applying the Rule of 72, an investor can expect to double the value of an ICE investment in 6 years if ICE only generates a 12% average annual total return.

I think Intercontinental Exchange is attractively valued based on its prospects. Therefore, I have added to my exposure and would consider adding to my position if its valuation becomes even more attractive.

I wish you much success on your journey to financial freedom!

Note: Thanks for reading this article. Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ICE.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.