I am looking to increase exposure to Intuitive Surgical (ISRG) and its robust growth potential; it was my 15th largest holding when I completed my 2023 Year End FFJ Portfolio Review.

In addition, it is currently the largest holding in a portfolio held by a young investor I am helping on their journey to financial freedom.

I last reviewed ISRG in this October 21, 2023 post and intended to revisit this holding following the release of Q4 and FY2023 results after the January 23 market close.

On January 9, 2024, however, ISRG announced certain unaudited preliminary Q4 and FY2023 financial results. In addition, it presented to the investment community at the 42nd Annual J.P. Morgan Healthcare Conference on January 10, 2024.

Should you be unable to listen/view ISRG’s presentation, this post is primarily limited to the information I gathered from ISRG’s 40 minute J.P. Morgan Healthcare Conference presentation.

Business Overview

ISRG has been developing and supporting robotically assisted minimally invasive care for more than 28 years.

Over 76,000 surgeons have been trained on Da Vinci systems and it boats a 99.9% system uptime.

Even though new rivals are entering the previously monopolistic area of robot-assisted surgery, ISRG remains the leader.

The opportunity to employ robotic surgery is unlimited. Existing applications only account for a very small percentage of all possible soft tissue surgery procedures that could migrate to robotic surgery; robotic surgery’s acceptance in most of the developed world is significantly lower than in the US. System placements outside the US (primarily Europe and Asia), however, are growing steadily and now represent nearly half of total installations.

I reference previous posts in which I touch upon the nature of ISRG’s business. I encourage you to review ‘Item 1 – Business’ in the FY2022 Form 10-K for a good overview of the company.

The Products and Services section of the company’s website provides information about ISRG’s Da Vinci and Ion products. In addition, the Intuitive Hub section of the company’s website describes how ISRG provides healthcare professionals (surgeons, operating room staff, etc.) with automated surgical video for easy recording, review, sharing, and virtual collaboration during Da Vinci surgery.

J.P. Morgan Healthcare Conference Presentation

The following are images from the J.P. Morgan Healthcare Conference presentation.

Source: ISRG – JPM Healthcare Conference January 10 2024

In 2023, ISRG’s objectives were to:

- increase utilization in focus procedures by country through training, commercial activities, and market access efforts;

- expand indications and launch new platforms;

- continue to improve the quality and continuity of supply (ISRG experienced pandemic stresses); and

- increase productivity in functions that benefit from industrial scale.

Challenges during the year consisted of:

- environmental uncertainty in China;

- pressure on gross margin attributed to scrap costs and new product mix;

- GLP-1 impact on bariatric surgery growth. A class of type 2 diabetes drugs, commonly called glucagon-like peptide 1 (GLP-1) agonists, may lead to weight loss. This weight loss is not permanent but some patients have opted to defer bariatric surgery in favor of addressing their health issues through the use of these diabetes drugs; and

- Ion catheter supply constraints. Ion is ISRG’s innovative robotic-assisted platform that aims to enable minimally invasive biopsies that could become a key part of early diagnosis. This system allows surgeons to drive to very small nodules in the periphery of the lung with precision and with safety.

Areas of strength in 2023 were:

- An increase in general surgery procedures in the US;

- Strong performance in Europe and Japan;

- Geographic expansion of ISRG’s Ion and Da Vinci SP; and

- Growth in system placement outside the US.

We see that worldwide procedures have grown significantly over the last several years. Stagnation in procedure growth in 2020 is attributed to COVID.

While the number of installations in the US continue to grow, growth is also evident in Europe and Asia.

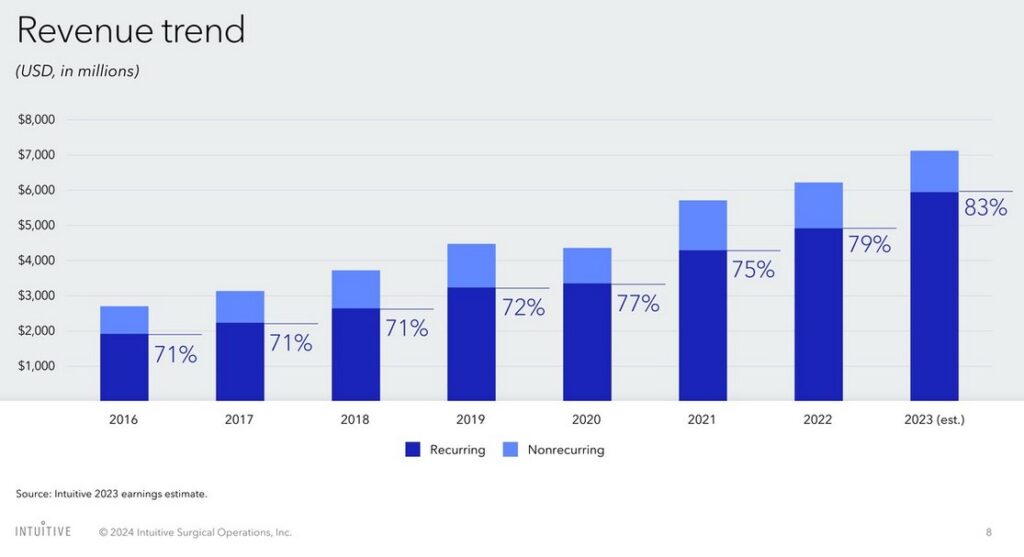

ISRG has grown its recurring revenue from ~71% in 2016 to ~83% in 2023.

Growth in system placements and installations are meaningless if the systems are not being used. We see impressive procedure growth since 2012 with the exception of 2020 when non-life threatening surgeries were postponed due to COVID.

With the products ISRG currently has on the market, in the geographies in which it operates and for which it has received clearances, ISRG has determined there are ~7 million patients annually for which ISRG’s products would be a good solution; this excludes ISRG’s Ion solutions. In 2023, however, only 2.2 million procedures were performed using ISRG’s Da Vinci systems. This suggests there is ample room for growth.

ISRG has determined that lung cancer detection is a significant unmet need with estimated annual incidence of 200,000+ in the US, 300,000+ in Europe, and over 1 million in China. ISRG’s Ion endoluminal system is a robotic-assisted platform for minimally invasive biopsies in the lung. It has received clearance in the US, Europe, and Korea, and it has been submitted for approval in China.

The Ion platform is relatively new, and therefore, does not have the same level of market penetration as Da Vinci. Nevertheless, we see steady growth in the installed base and number of procedures.

More rapid growth in ISRG’s single port Da Vinci platform is expected upon receipt of further regulatory approvals.

ISRG has identified the top 4 issues confronting hospitals:

- workforce challenges

- financial and cost challenges

- behavioral health and addiction

- patient safety and quality

It is, therefore, focused on:

- Improving patient care through better outcomes;

- Helping medical professionals acquire new skills and reaching proficiency sooner; and

- Working with Integrated Delivery Networks (IDNs) and hospitals to make better use of their resources and to generate a higher return on investment.

NOTE: An IDN is a group of healthcare providers, such as hospitals, clinics, and physicians, that work together to provide coordinated patient care (largest IDNs by region in the US).

The process ISRG follows requires its customers to adopt its platforms. This often means the deployment of 1 system in an IDN or hospital and an ISRG representative working very closely with surgeons and operating room personnel.

Once adoption is achieved, phase 2 involves a gradual expansion in the use of ISRG platforms.

The third phase is when an IDN or hospital standardizes its platforms. Once this happens, it is extremely difficult for a competitor to displace ISRG.

Financials

Q4 and FY2023 Preliminary Results

As noted earlier, ISRG announced certain unaudited preliminary Q4 and FY2023 financial results on January 9.

I intend to briefly analyze the results and FY2024 outlook following the January 23 release.

Credit Ratings

No rating agency rates ISRG because it has no debt.

Dividend and Dividend Yield

ISRG does not distribute a dividend.

Valuation

FY2011 – FY2022 PE ratios are 40.02, 30.69, 22.97, 46.20, 37.72, 34.17, 47.07, 72.02, 53.69, 93.18, 77.44, and 70.38.

Refer to my October 19, 2022 post in which I provided ISRG’s valuation at the time I wrote previous posts. The following valuation levels at the time of my more recent ISRG posts are provided below for ease of comparison.

When I wrote my April 19, 2023 post, shares were trading at ~$298.60 and the forward-adjusted diluted PE levels were:

- FY2023 – 23 brokers – ~55 based on a mean of $5.42 and low/high of $5.03 – $5.60.

- FY2024 – 23 brokers – ~47 based on a mean of $6.37 and low/high of $5.93 – $6.88.

- FY2025 – 16 brokers – ~40 based on a mean of $7.43 and low/high of $6.87 – $8.29.

When I wrote my July 22 post, ISRG’s share price had closed at $335.83 on July 21. ISRG had generated $2.18 and $2.65 in diluted EPS and adjusted diluted EPS in the first half of FY2023 and I envisioned ~$4.50 and ~$5.45 in diluted EPS and adjusted diluted EPS. Using my FY2023 earnings estimates, the forward diluted PE and forward adjusted diluted PE were ~74.6 and ~61.6.

The forward-adjusted diluted PE levels using broker estimates were:

- FY2023 – 26 brokers – ~60.7 based on a mean of $5.53 and low/high of $4.70 – $5.76.

- FY2024 – 27 brokers – ~52 based on a mean of $6.46 and low/high of $5.56 – $7.08.

- FY2025 – 19 brokers – ~45 based on a mean of $7.47 and low/high of $6.56 – $8.60.

When I last reviewed ISRG, the share price had closed at ~$267 on October 20. I envisioned FY2023 diluted EPS and adjusted diluted EPS of ~$4.50 and ~$5.45. Using my FY2023 earnings estimates, the forward diluted PE and forward adjusted diluted PE were ~59.3 and ~49.

The forward-adjusted diluted PE levels using broker estimates were:

- FY2023 – 26 brokers – ~47.8 based on a mean of $5.59 and low/high of $5.50 – $5.82.

- FY2024 – 26 brokers – ~41.4 based on a mean of $6.45 and low/high of $6.15 – $6.76.

- FY2025 – 20 brokers – ~35.7 based on a mean of $7.48 and low/high of $7.07 – $8.03.

ISRG’s share price is currently ~$359 and the forward-adjusted diluted PE levels using current broker estimates are:

- FY2023 – 26 brokers – ~64 based on a mean of $5.60 and low/high of $5.51 – $5.68.

- FY2024 – 26 brokers – ~55.8 based on a mean of $6.43 and low/high of $6.01 – $6.65.

- FY2025 – 22 brokers – ~48 based on a mean of $7.47 and low/high of $7.07 – $8.03.

If we use the same ~$359 share price and inflate the estimated forward-adjusted diluted EPS, we get:

- FY2023 – ~53 based on $6.80.

- FY2024 – ~46 based on $7.80.

- FY2025 – ~41 based on $8.80.

Final Thoughts

There is much to like about ISRG:

- strong growth potential;

- impeccable balance sheet;

- highly profitable and a strong Free Cash Flow generator; and

- dominant position within the robotics assisted surgery space.

Although ISRG is a wonderful company, I question how an attractive total investment return can be achieved given the current valuation.

Despite arbitrarily inflating ISRG’s forward-adjusted diluted earnings for FY2023 – FY2025 (see above), the forward adjusted diluted PE levels are still high.

ISRG’s share price can be volatile so it is not beyond the realm of possibility that we could witness an attractive share price pullback in 2024. If this happens, I hope I have more sense than I did in October 2023 when I elected not to add to my exposure.

I currently hold 450 shares in a ‘Core’ account in the FFJ Portfolio. Since I deem shares to be currently overvalued, I do not intend to add to my exposure at this stage.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ISRG.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.