Contents

I have expressed my concern in several posts in what appears an element of irrational exuberance. This has made it difficult for me to identify attractively valued companies in which I wish to deploy surplus funds.

On occasion, however, a company that appeals to me reaches an attractive or reasonable valuation.

Enter Visa (V).

I last reviewed V in my January 26, 2024 post. I concluded that I was not adding to my exposure because I wanted to acquire shares in undervalued high-quality companies. At the time, the most currently available financial information was for Q1 2024.

Fast forward and we now have V's Q3 and YTD2024 financial results and revised FY2024 outlook. This was released following the July 23, 2024 market close.

I have been a V shareholder almost from the day it went public on March 18, 2008 and have added to my exposure over the years. V has been my largest holding for years and was, once again, my largest holding when I completed my 2024 Mid Year FFJ Portfolio Review.

Historically, I have only disclosed 225 V shares held in a 'Core' account in the FFJ Portfolio; most of my V shares are in a retirement account for which I do not disclose details. On July 24, however, I acquired an additional 300 shares @ ~$255/share in one of the 'Side' accounts within the FFJ Portfolio.

In this post I touch upon why I have added to my exposure.

Financial Results

A comprehensive overview of V is found within its FY2023 Form 10-K.

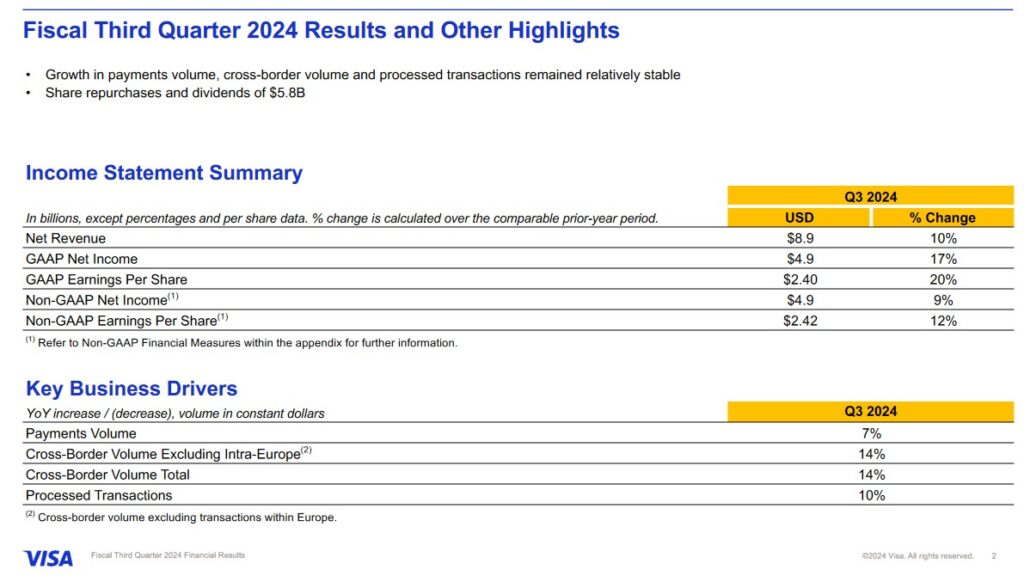

Q3 and YTD2024 Results

V's Q3 and YTD2024 related material is accessible here.

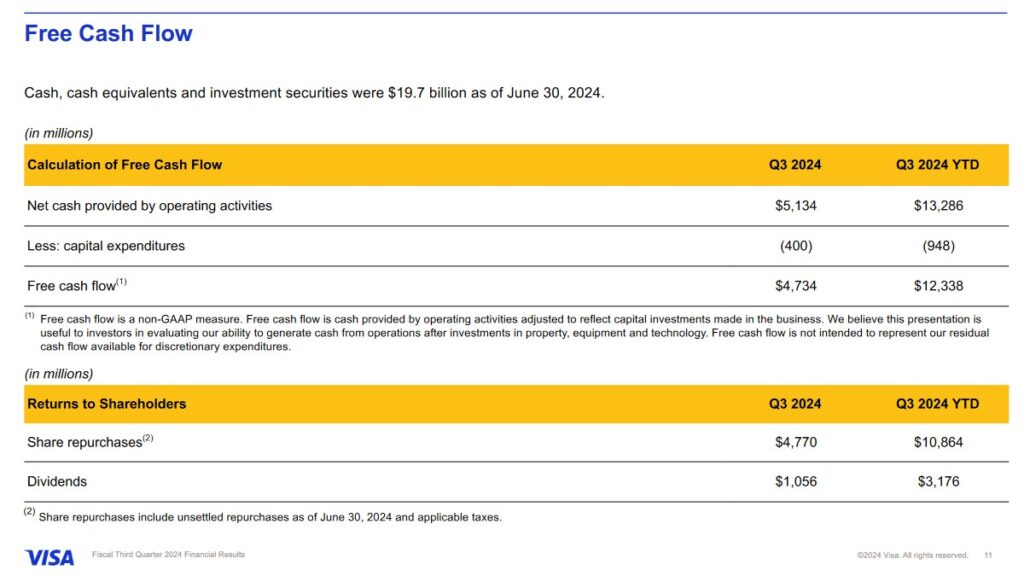

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

In the FY2014 - FY2023 time frame, V's:

- OCF was (in B$) 7.21, 6.58, 5.57, 9.21, 12.71, 12.78, 10.44, 15.23, 18.85, and 20.76.

- CAPEX was (in B$) 0.55, 0.41, 0.52, 0.71, 0.72, 0.76, 0.74, 0.71, 0.97, and 1.06.

- FCF was (in B$) 7.90, 9.72, 8.58, 13.08, 14.65, 18.33, 18.10, 21.22, 25.54, and 29.72.

In the first 3 quarters of FY2024, V has reported ~$13.286B of OCF, ~$0.948B of CAPEX thus giving us ~$12.338B of FCF.

Return On Invested Capital (ROIC)

V's ROIC (%) in FY2014 - FY2023 is 19.97, 22.05, 14.07, 15.05, 23.44, 26.52, 21.65, 22.96, 27.13, and 30.97.

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company's cost of capital will be lower than this level. V's ROIC consistently exceeds this level.

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

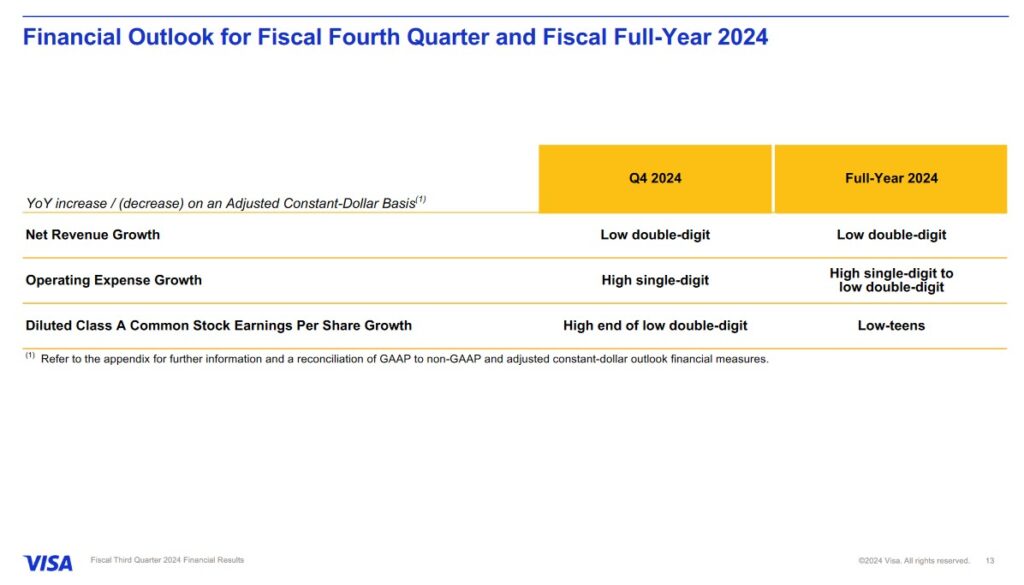

FY2024 Outlook

The following is V's current Q4 and FY2024 outlook.

- V expects payments volume and processed transactions to grow at a similar rate to Q3.

- Total cross-border volume growth is expected to be slightly below Q3.

- Expectations are for adjusted net revenue growth in the low double digits. This equates to a slight improvement from the 10% adjusted revenue growth rate in Q3.

- Adjusted operating expenses are expected to grow in the high single digits in Q4.

- Non-operating income is expected to be ~$40 - ~$50 million.

- The tax rate is expected to be 19% - 19.5% in Q4.

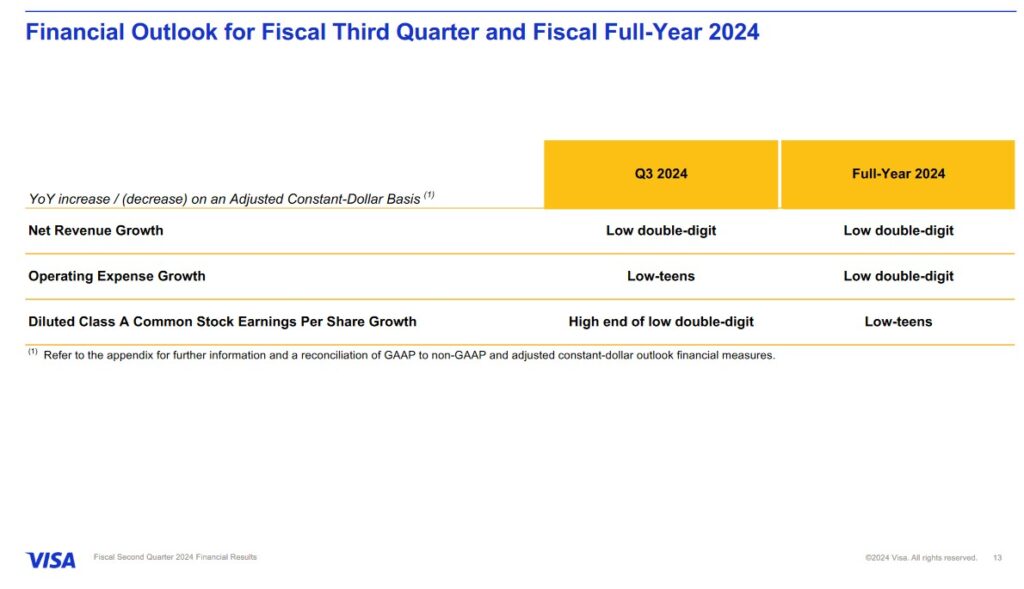

This was V's Q3 and FY2024 outlook when it released its Q2 results.

Credit Ratings

I pay particularly close attention to the risk aspect of my investments. This includes an assessment of the maturity schedule of a company’s credit facilities and credit ratings.

V's borrowings are at very attractive interest rates. Looking at V's track record and the debt maturity schedule, I see no reason why V should have any difficulty in meeting its obligations.

V's current unsecured domestic long-term debt credit ratings and outlook are:

- Moody's: Aa3 (stable)

- S&P Global: AA- (stable)

These ratings are the lowest tier of the high-grade investment-grade category and define V as having a VERY STRONG capacity to meet its financial commitments. The ratings differ from the highest-rated obligors only to a small degree.

Dividend and Dividend Yield

V's dividend history is accessible here.

V's starting share price, accounting for a 4 to 1 stock split effective March 18, 2015, is ~$14. The current share price is ~$254. That is a ~$240 variance.

The cumulative amount of dividends distributed since the first dividend distribution in August 2008 is just over $12.

Enough said.

The weighted average number of outstanding Class A shares in FY2013 - FY2023 (in millions of shares) is 2,624, 2,523, 2,457, 2,414, 2,395, 2,329, 2,272, 2,223, 2,188, 2,136, and 2,085. The weighted average in Q3 was 2,029.

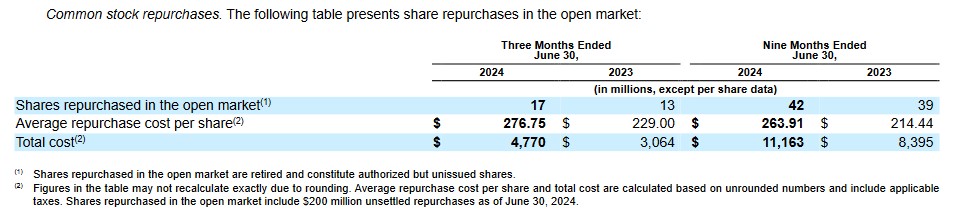

'Note 9 - Stockholders’ Equity' that commences on page 20 of 46 in V's Q3 Form 10-K provides comprehensive information regarding the various classes of V's common shares. For ease of reference, however, I provide the following as it relates to V's Q3 and YTD share repurchase activity.

Valuation

Valuation

At the time of my October 25, 2023 post, V Shares were trading at ~$235. V's forward adjusted diluted PE levels based on broker estimates were:

- FY2024 – 34 brokers – 24 using the mean of $9.86 and low/high of $9.16 – $10.18.

- FY2025 – 26 brokers – 21 using the mean of $11.18 and low/high of $10.65 – $11.60.

When I wrote my January 26, 2024 post, shares were trading at ~$267. I stated that I expected no meaningful changes following analyst updates over the upcoming days and reflected the following valuations based on the current brokers' forward earnings estimates:

- FY2024 – 35 brokers – ~27 using the mean of $9.89 and low/high of $9.36 – $10.06.

- FY2025 – 35 brokers – ~24 using the mean of $11.15 and low/high of $9.72 – $11.59.

- FY2026 – 15 brokers – ~21 using the mean of $12.78 and low/high of $11.81 – $13.47.

Using my ~$255 purchase price and the current forward adjusted diluted earnings brokers' estimates , V's valuation is:

- FY2024 – 36 brokers – ~25.7 using the mean of $9.92 and low/high of $9.75 – $10.02.

- FY2025 – 36 brokers – ~23 using the mean of $11.10 and low/high of $10.73 – $11.32.

- FY2026 – 15 brokers – ~20.3 using the mean of $12.59 and low/high of $12.24 – $12.85.

V has generated $12.338B of FCF in the first 3 quarters of FY2024. I do not anticipate it will achieve $29.72B of FCF as it did in FY2023, however, ~$16.5B is not out of the realm of possibility.

If it continues to repurchase shares over the remainder of FY2024, the weighted average diluted outstanding shares in FY2024 could be ~2,025 million. This gives us ~$8.15 of FCF/share. Using my ~$255 purchase price, the forward P/FCF is ~31.3. V's P/FCF in FY2014 - FY2023 is 19.56, 18.81, 20.70, 19.81, 19.99, 22.37, 25.81, 21.62, 16.74, and 17.64.

Final Thoughts

I have increased my Visa exposure because I consider shares to be slightly undervalued.

- V and MA to limit fees they charge merchants that accept their credit and debit cards;

- the average swipe fee to fall at least 0.04 percentage point for three years, and stay at least 0.07 percentage point below the current average for five years; and

- V and MA to cap rates for five years and remove anti-steering provisions that prevent merchants from steering customers to cheaper cards. Merchants would have also received more discretion to offer discounts or impose surcharges.

The presiding judge denied the request by a group of merchants, primarily small businesses, for preliminary approval. Many merchants and trade groups including the National Retail Federation opposed the accord, saying card fees would remain too high, while V and MA would retain too much control over card transactions.

This recent decision does not affect an earlier $5.6 billion class action swipe fee settlement between V and MA and ~12 million merchants that a federal appeals court in Manhattan upheld in March 2023.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to [email protected].

Disclosure: I am long V and MA.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.