I have held shares in this company since January 2007 and view its as a core holding and fully intend to continue to add to my current position.

The company’s stock price, however, has surged subsequent to early July 2018 to the extent where I view the shares as being priced to perfection.

Summary

- This high quality Canadian insurance company has grown successfully through multiple acquisitions and is now one of Canada’s largest P&C insurance companies (~17% market share).

- Growth opportunities in Canada are limited in that the top 5 P&C insurers in Canada have a 48% market share.

- In 2017, it expanded into the US market but strategically decided to enter the US specialty insurance market thus avoiding direct competition with much larger and well entrenched P&C companies.

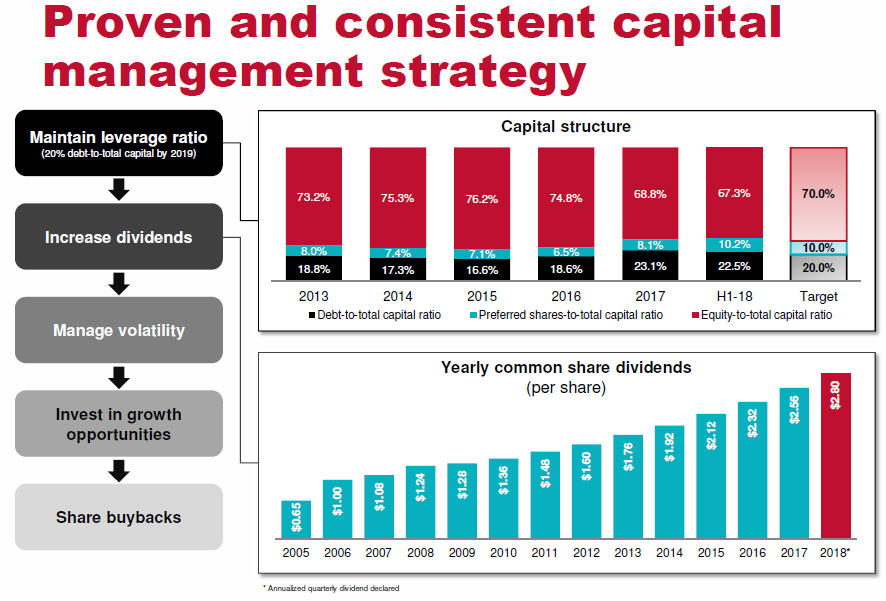

- At the time of the US acquisition management indicated that it expected to restore its capital structure to a 20% the debt-to-total capital ratio within 2 years. Once achieved I fully expect this company to make further acquisitions in the US specialty insurance market.

- While definitely a wonderful company, I am of the opinion that this company’s stock is now priced to perfection.

All figures are expressed in CDN dollars unless otherwise noted.

Introduction

The subject company is Canada’s largest provider of property and casualty (P&C) insurance and it is also a provider of specialty insurance in North America. It serves more than five million personal, business, public sector and institutional clients through its Canadian and US Offices.

This company traces its roots to 1809. In the late 1950s, however, it was acquired by one of the largest insurance companies in the Netherlands.

In 2004, the company went public with a listing on the TSX; the Dutch parent retained 70% ownership.

In 2009, the Dutch parent needed to raise equity to shore up its financial position as a result of some challenges it encountered at the height of the Financial Crisis. The Dutch parent divested itself of its 70% interest and the Canadian entity amended its name.

This company is a proven industry consolidator having made 16 successful P&C acquisitions since 1988; 8 have been made after 2000.

In fiscal 2017 it generated ~$10B in total annual premiums and reported having a ~17% share of Canada’s P&C market.

In 2017, it acquired a pure-play specialty lines insurer in the US. This specialty insurance company focuses on small to midsized businesses and sells specialty products that solve the unique needs of particular customers or industry groups including accident and health, technology, ocean and inland marine, public entities, and entertainment. The distinct products and tailored coverages are provided to a broad customer base across the U.S. (ie. healthcare, tuition reimbursement, surety, management liability, financial services, specialty property, environmental and financial institutions). This acquired company is relatively small; it reported ~$1.1B in Direct Premiums Written in 2017.

A key reason for this company’s expansion into the US specialty insurance market is that the Canadian Property and Casualty (P&C) insurance industry has been undergoing consolidation and there is little room for further expansion. The top 20 P&C insurers in Canada have an 84% market share. In 2009, the top 5 had a 36% market share. In 2017, the top 5 had a 48% market share.

Given this company’s acquisition track record, it would be fair to presume that further acquisitions in the U.S. specialty insurance market is highly probable. This, however, is unlikely to transpire for at least another 2 years as the focus is on fully integrating the recently acquired specialty insurer and in restoring the capital ratios to target levels; at the time of the 2017 acquisition, management specifically stated the plan was to reduce the debt-to-total capital ratio below the 20% target level within 24 months.

In addition, management specifically stated at the time of the 2017 US acquisition that the plan is to:

- expand the company’s future potential by combining the acquired company’s strengths with the acquirer’s data, claims and digital expertise;

- diversify the business and geographic mix.

I have not analyzed this company since May 2017 and given that its stock price has risen roughly 16% within the past month I thought it would be an opportune time to revisit this company.

Full disclosure: In January 2007 I initiated a position in this company and have periodically added to my position; all shares are held in undisclosed accounts. I do, however, hold shares in this company in the Financial Freedom is a Journey portfolio.

Please click here to read the complete version of this article.

Members of the FFJ community can access reports I generate on high quality companies which add long-term shareholder value. In an effort to help you determine whether my offering is of any value to you I am pleased to offer 30 days’ free access to all sections of my site. No commitments. No obligations. That’s 30 days from the time you register at absolutely no cost to you!