Previous Exxon Mobil (XOM) posts are accessible in the FFJ Archives.

In my previous XOM stock analysis, I concluded shares were attractively valued and acquired another 200 shares in a ‘Core’ account in the FFJ Portfolio.

At the time of that post, XOM’s share price was ~$57. The share price is now ~$64.50 and with the October 29th release of Q3 and YTD2021 results, I revisit XOM to determine whether to acquire additional shares.

Exxon Mobil – Stock Analysis – Financials

Q3 and YTD2021 Results

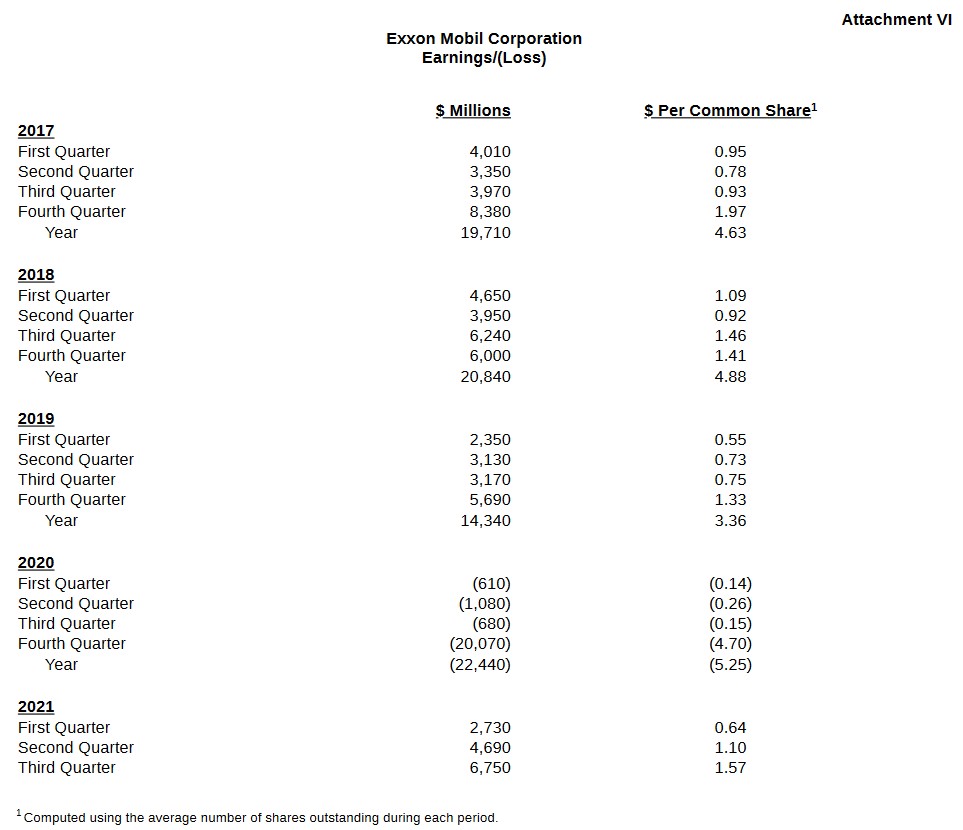

On October 29, 2021, XOM reported Q3 and YTD results (Form 8-K and Earnings Presentation). While these results were very strong (Q3 earnings of $6.8B and YTD earnings of $14.17B), we see XOM’s quarterly results have experienced very wild swings.

Management has diligently been working to improve the company’s cost structure. In FY2020, the cost structure improved by $3B versus 2019. Progress continues and structural costs are now $4.5B lower than in 2019 on an annual basis. Management expects further improvements.

Debt was reduced ~$4B in Q3 and plans are to further reduce debt to within the 20% – 25% debt-to-capital target.

Free Cash Flow (FCF)

Strong earnings and prudent capital expenditure management resulted in Q3 2021 FCF of $2.1B. Stronger cash flow from operations and FCF has enabled XOM to strengthen the balance sheet.

Source: XOM Q3 2021 Earnings Presentation – October 29, 2021

Outlook

XOM’s priority remains to significantly grow the value of the base business. By continuing to leverage competitive advantages in technology, scale, integration, functional excellence, and people, it intends to continue to improve operating performance, reduce costs, and develop a portfolio of industry-advantaged high-return investments.

In 2018, XOM began to develop opportunities in carbon capture and low emission. It also established objectives to significantly reduce emissions intensity by 2025. XOM now expects to meet these objectives in 2021 and work is in progress to significantly raise the bar and reset the 2025 objectives. Cumulative capital investment during the 2022 – 2027 timeframe in emission reduction projects is expected to be ~$15B.

Improvements in the cost structure are also ahead of schedule and XOM expects to deliver more than $6B in structural savings by 2023.

Source: XOM Q3 2021 Earnings Presentation – October 29, 2021

Annual capital spending projections are $20B – $25B. This is a significant reduction versus pre-pandemic plans.

At a presentation for analysts in New York in early 2019, XOM’s CEO indicated the company planned capital spending of $30B in FY2019 and $33B – $35B in FY2020. These were increases from ~$26B in FY2018. The projected increases in capital spending were because the acquisition of assets in the Permian Basin and oil discoveries in Guyana created investment opportunities that were more attractive than at any other time following the 1999 merger of Exxon and Mobil.

How times changed after that early 2019 presentation!

Exxon Mobil – Stock Analysis – Credit Ratings

The following senior unsecured domestic currency debt ratings remain unchanged from my previous post.

- Moody’s: Aa2 with a stable outlook (this is the middle tier of the high-grade investment-grade category).

- S&P Global: AA- with a negative outlook (this is the bottom tier of the high-grade investment-grade category).

The rating assigned by S&P Global is one notch lower than that assigned by Moody’s. Both ratings, however, define XOM as having a VERY STRONG capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

XOM’s current ratings are satisfactory for my purposes.

Exxon Mobil – Stock Analysis –

Dividend and Dividend Yield

Looking at XOM’s dividend history, we see XOM distributed an $0.87/share quarterly dividend for 10 consecutive quarters.

When I wrote my previous post I expected the quarterly dividend to remain unchanged until Q1 2022 to allow XOM to deploy as much FCF as possible toward debt reduction. XOM, however, has elected to increase its quarterly dividend to $0.88/share. This dividend is payable on December 10 to shareholders of record on November 12.

With shares trading at ~$64.50, the new dividend yield is ~5.5%. This is slightly lower than at the time of my prior post at which time the $3.48 annual dividend and the ~$57 share price yielded ~6.1%.

XOM’s diluted weighted average shares outstanding in FY2011 – FY2020 (in millions) is 4,876, 4,628, 4,419, 4,282, 4,196, 4,177, 4,256, 4,270, 4,270, and 4,271. This share count has increased to 4,275 as XOM has repurchased no shares YTD2021.

On October 27, XOM announced an expansion in shareholder distributions by up to $10B over 12 – 24 months through a repurchase program beginning FY2022.

Exxon Mobil – Stock Analysis – Valuation

XOM has generated YTD diluted EPS of $3.31 consisting of $0.64, $1.10, and $1.57 in Q1, Q2, and Q3 respectively. If we conservatively estimate XOM will generate $1.55 in Q4 then FY2021 diluted EPS should be ~$4.86. With shares trading at ~$64.50, the forward diluted PE is ~13.3.

By way of comparison, XOM’s FY2011 – FY2020 PE levels are 10.21, 8.92, 13.21, 11.63, 16.45, 42.18, 27.24, 12.53, 20.28, and 52.85.

When I wrote my July 23 post, shares were trading at ~$57 and this was the adjusted diluted EPS guidance from 26 brokers:

- FY2021: mean of $3.95 and a low/high range of $3.09 – $5.12. The forward adjusted diluted PE using the mean estimate is ~14.43 and ~12.67 if I use $4.50.

- FY2022: mean of $4.73 and a low/high range of $3.75 – $6.03. The forward adjusted diluted PE using the mean estimate is ~12.05 and ~10.36 if I use $5.50.

The following earnings estimates are reflected in the 2 online trading platforms I use. There is a huge disparity in estimates and this is likely because some brokers are likely still revising their estimates; I expect the disparity will narrow over the coming days. For now, however, these are XOM’s forward adjusted diluted PE valuations using the ~$64.50 share price:

- FY2021: mean of $4.72 and a low/high range of $3.09 – $5.41 from 28 brokers. The forward adjusted diluted PE using the mean estimate is ~13.7 and ~12 if I use $5.41.

- FY2022: mean of $5.61 and a low/high range of $4.18 – $7.40 from 29 brokers. The forward adjusted diluted PE using the mean estimate is ~11.5 and ~8.7 if I use $7.40.

With such a disparity in earnings estimates, I think some brokers have yet to update their earnings estimates. I envision the low end of earnings estimates will be increased which would lower the forward adjusted diluted PE levels thereby making shares more attractively valued than they currently appear.

Exxon Mobil – Stock Analysis – Final Thoughts

I deem Chevron (CVX) to be a superior investment to XOM. This is borne out by the difference in the number of shares I own in each company:

- 1954 CVX shares

- 980 XOM shares and more XOM shares in a retirement account for which I do not disclose details.

Volatility is something investors need to accept when investing in an oil and gas company. While XOM is being managed to reduce the wild swings in quarterly results, the nature of the business is such that there will always be peaks and troughs.

I do not intend to acquire additional XOM shares. However, if you intend to invest in XOM, you may want to patiently wait for when industry conditions once again become unfavourable at which time XOM’s share price will likely take a hit.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long XOM and CVX.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.