In this Danaher Corporation stock analysis, I disclose why I have initiated a small position in one of the ‘Core’ accounts within the FFJ Portfolio; I acquired 50 shares on January 4, 2022 at ~$307/share.

In previous posts, I have stated that the vast majority of my investment errors over the years are errors of omission as opposed to errors of commission. I can think of several instances in which I should have invested in a company. For whatever reason, however, I failed to take action. Danaher Corporation (DHR) is one such error.

Danaher – Stock Analysis – Business Overview

DHR is a global science and technology innovator. It is comprised of more than 20 operating companies with leadership positions in the life sciences, diagnostics, environmental and applied sectors. It is organized under three segments:

- Life Sciences;

- Diagnostics; and

- Environmental & Applied Solutions

It continually acquires and divests companies; more than 50% of DHR’s current total revenue has been acquired in the past 7 years.

The DHR Business Directory provides a link to the website of each company within the group.

A key reason for DHR’s success is the proven effectiveness of the Danaher Business System. This business system is so effective that companies spun-off from DHR have adopted it.

While DHR is continually evolving (The Danaher Story) and has a promising future, one of the deciding factors in my decision to initiate a position is the Rales brothers (Steven Rales and Mitchell Rales).

Steven Rales (Chairman of the Board) and his brother Mitchell Rales (Chairman of the Executive Committee) were instrumental in creating what is now a $200B+ market cap company in a span of 4 decades. Steven Rales is currently ranked 264th on the Forbes list of billionaires with an estimated net worth of $9.5B+. Mitchell Rales is currently ranked 432nd with an estimated net worth of $7B+.

Clearly, these brothers know how to create wealth and my decision to invest in DHR is heavily influenced by their successful track record.

The best way in which to gain an understanding of DHR is to read Part 1 of its 2020 Annual Report / Form 10-K and to review the 2021 Investor and Analyst Day Presentation.

Subsequent to DHR’s 2020 fiscal year-end, it announced its intent to acquire privately-held Aldevron for a cash purchase price of ~$9.6B. This acquisition was completed on August 30, 2021.

In addition, during the 9 months ended October 1, 2021, DHR acquired 9 other businesses for total consideration of ~$1.1B in cash, net of cash acquired. Details of these acquisitions are found in Note 3 in DHR’s Q3 2021 10-Q commencing on page 14 of 59.

Danaher – Stock Analysis – Financials

Q3 2021 and YTD Results

Please refer to DHR’s October 21, 2021 Q3 and YTD2021 Earnings Release and Earnings Presentation which are accessible here.

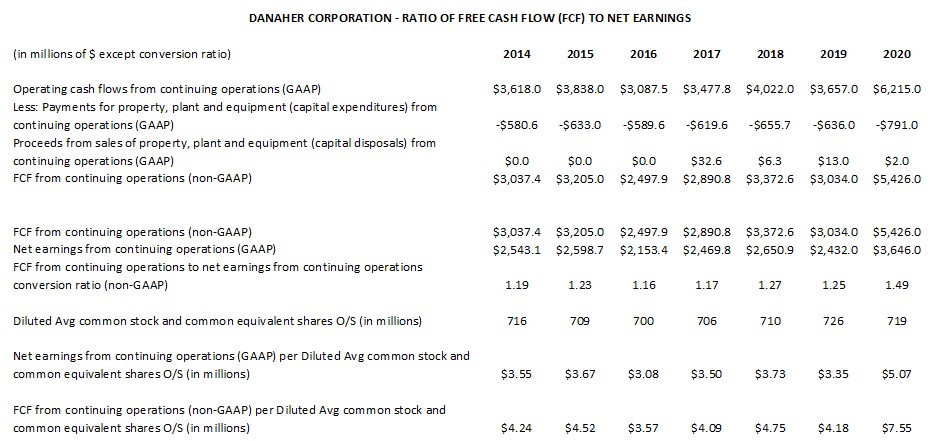

Operating Cash Flow (OCF) and Free Cash Flow (FCF)

Since DHR actively acquires and divests assets, its diluted earnings per share (EPS) is deceiving. ‘Amortization of intangible assets’ and ‘amortization of acquisition-related inventory fair value step-up’ are two large line items that consistently appear in the Consolidated Condensed Statements of Cash Flows.

DHR’s results are such that FCF consistently exceeds Net Income; FY2020 marked the 29th consecutive year in which FCF exceeded Net Income and YTD results suggest DHR has a good chance of achieving 30 consecutive years.

The data reflected below is extracted from DHR’s Annual Reports.

The following are YTD results.

Danaher – Stock Analysis – Credit Ratings

Details of DHR’s outstanding debt are found in Note 7 – Financing on page 19 of 59 in the Q3 10-Q. The maturity dates of DHR’s debt are well distributed and the company’s strong cash flow generating capabilities should enable it to easily meet its obligations.

On March 31, 2020, DHR announced the completion of its ~$21.4B acquisition of the Biopharma business from General Electric Company’s Life Sciences division; the net purchase price was ~$20B given the tax benefits from the transaction structure. Following the completion of this acquisition, DHR’s domestic long-term unsecured debt ratings were downgraded 2 notches on April 1, 2020.

The current ratings and outlook are:

- Moody’s: Baa1 with a stable outlook;

- S&P Global: BBB+ with a positive outlook.

Both ratings are the top tier of the lower-medium-grade investment-grade tier. These ratings define DHR as having the ADEQUATE capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity to meet its financial commitments.

These ratings satisfy my conservative investment profile.

Danaher – Stock Analysis

Dividend and Dividend Yield

DHR generates superior long-term investment returns by retaining funds in the business. While DHR distributes a quarterly dividend, an investment in this company is made predominantly on the basis of potential long-term capital appreciation; the current $0.21/share quarterly dividend is a yield of less than 0.3% based on the current ~$305 share price.

Although DHR periodically repurchases shares, the diluted average common stock and common equivalent shares outstanding (in millions) in FY2012 – FY2020 is 713, 711, 716, 709, 700, 706, 710, 726, and 719. For the 9 months ended October 1, 2021, this had risen to 736.4; shares were issued to aid in the acquisition of Aldevron.

As noted earlier, DHR actively acquires and divests entities. The fluctuation in the outstanding number of shares is heavily dependent on this level of activity.

Danaher – Stock Analysis – Valuation

Based on the current ~$305 share price and adjusted diluted EPS estimates from the brokers which follow DHR, we see:

- FY2021 – 20 brokers – mean of $9.83 and low/high of $9.40 – $10.01. Using the mean estimate, the forward adjusted diluted PE is ~31.

- FY2022 – 21 brokers – mean of $10.19 and low/high of $9.58 – $10.90. Using the mean estimate, the forward adjusted diluted PE is ~30.

- FY2023 – 15 brokers – mean of $10.65 and low/high of $9.45 – $11.31. Using the mean estimate, the forward adjusted diluted PE is ~29.

Only 4 brokers have provided FY2024 estimates, and therefore, I do not rely on these estimates.

Using YTD FCF of $5.164B and shares outstanding of 736.4 million shares, we get ~$7 in YTD FCF/share versus $6.22 in YTD diluted net EPS. This YTD FCF/share also compares favourably with $6.10 in YTD diluted net EPS from continuing operations and $7.36 in adjusted YTD diluted net EPS from continuing operations.

While DHR might be richly valued, this is a growing high-quality business with a proven track record of success. I am prepared to pay a premium to invest in such a company. Should a long overdue broad market pullback lead to an improvement in DHR’s valuation, I would add to my position.

Danaher – Stock Analysis – Final Thoughts

In July 2016, Fortive Corporation (FTV) was spun off from DHR. It was not until September 2019, however, that I initiated a position in FTV through one of the ‘Side’ accounts in the FFJ Portfolio; FTV articles are accessible through the Archives.

In October 2020, FTV spun off Vontier Corporation (VNT) at which time I received shares in this company; VNT articles are accessible through the Archives.

Based on DHR’s track record and the extent to which the Life Sciences and Diagnostics segments have grown, I would not be surprised to learn of another spin-off in the future.

In addition to my intention to increase my DHR exposure over time, I am helping a couple of young investors create investment portfolios so they can eventually achieve financial freedom. The plan is for both of them to acquire DHR shares in the coming days.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long DHR, FTV, and VNT.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.