I last reviewed Danaher (DHR) in this February 1, 2024 post at which time the Q4 and FY2023 results had just been released. Prior to this post, I published Danaher Consistently Generates Strong Free Cash Flow and Danaher – Current Weakness Is A Buying Opportunity following the release of Q2 and Q3 results, respectively.

In my October 25, 2023 post I stated that DHR had embarked on a journey to strategically enhance its portfolio and strengthen growth and earnings trajectories.

On September 30, 2023, it spun-off Veralto (VLTO) thus becoming a focused life sciences and diagnostics innovator. Establishing Veralto as a stand-alone public company was the first step in the portfolio transformation process.

DHR completed the acquisition of Abcam on December 6, 2023 thus further increasing its focus on the highly attractive life sciences and diagnostics markets.

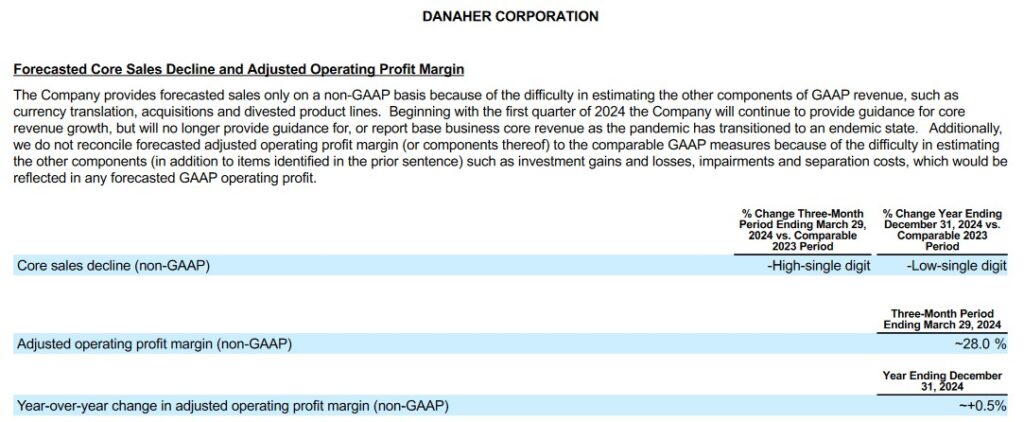

FY2023 was a challenging year operationally as pandemic tailwinds became headwinds. When DHR released its initial FY2024 outlook on January 30 together with its FY2023 results, the expectation was that core revenue would decline in the:

- low single-digit percent range in FY2024; and

- first half of the year before returning to growth in the second half of 2024.

On a positive note, the outlook called for the FY2024 adjusted operating profit margin to improve by ~50 bps versus the FY2023. Over the long-term, however, management expects DHR to be a faster-growing business with higher margins and stronger free cash flow generation.

Overview

DHR operates several businesses within 3 business segments. You can explore these businesses here.

The Form 10-Q and Form 10-K available through the SEC Filings section of the company’s website provide the necessary information to learn about the company, its recent performance, and risks.

Financials

Q2 and YTD2024 Results

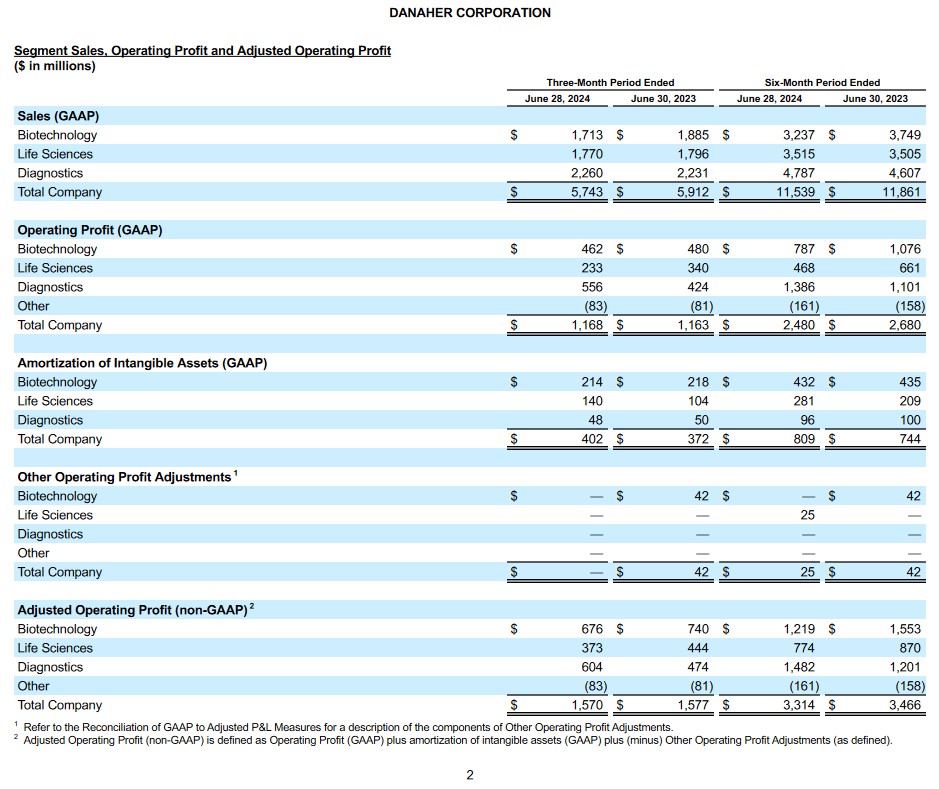

The following reflects DHR’s Q2 and YTD2024 Sales, Operating Profit, and Adjusted Operating Profit. Commencing on page 29 of 48 in the Q2 Form 10-Q is a detailed explanation of DHR’s results.

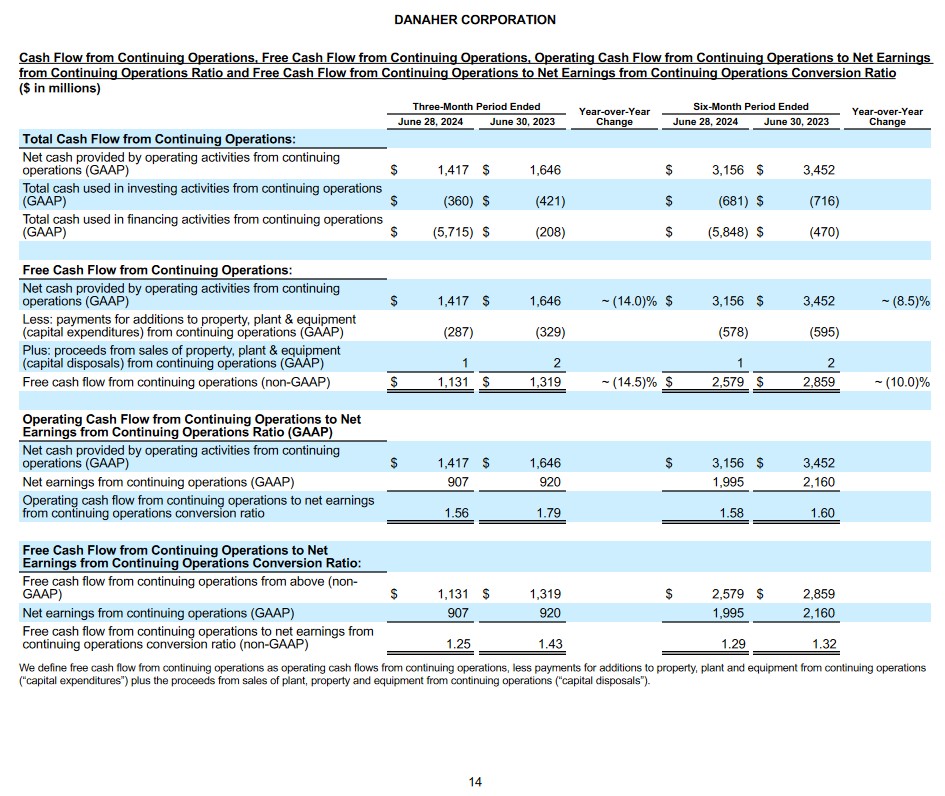

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

DHR views FCF generation as one of the most important metrics. Investors, much like DHR’s management, should pay particularly close attention to DHR’s OCF and FCF.

Since DHR actively acquires and divests assets, its diluted EPS is deceiving. ‘Amortization of intangible assets’ and ‘amortization of acquisition-related inventory fair value step-up’ are line items that consistently appear in the Consolidated Condensed Statements of Cash Flows.

DHR’s FCF/Net Income (FCF conversion ratio) typically exceeds 100%. FY2023 was the 32nd consecutive year DHR’s FCF to net income conversion ratio exceeds 100%. We see that the Q2 and YTD2024 results continue this trend.

FY2024 Guidance

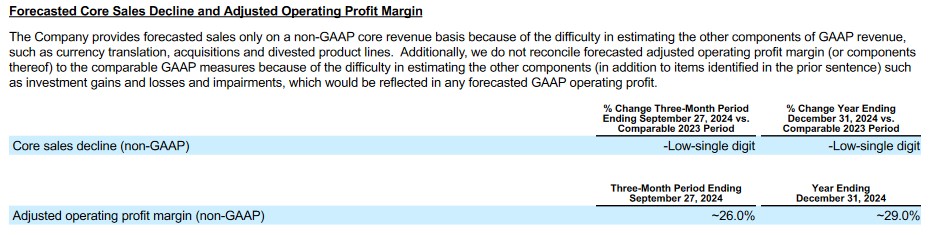

In Q3, DHR expects an adjusted operating profit margin of ~26% and core revenue to decline in the low single-digit percent range.

There is, however, no change to previous guidance for FY2024. DHR still anticipates a core revenue decline in the low single-digit percent range and a full year adjusted operating profit margin of ~29%.

The following reflects guidance provided at the beginning of FY2024.

DHR’s emerging biotech customers continue to prioritize projects, particularly for cell and gene therapies in an effort to manage liquidity. There is, however, an improvement in the overall funding environment which is a positive leading indicator for these biotech customers.

Based on the trends through the first half of the year, DHR continues to expect a low single-digit core revenue decline in its bioprocessing business for FY2024. There is also no change to the assumption of a bioprocessing core revenue growth rate of high single digits or better as the year approaches a conclusion.

The Biologics market remains healthy as evidenced by the increasing number of treatments under development and in production. The number of new FDA approvals for biologic and genomic medicines in the first half of 2024 is double compared to the first half of 2023 and the full year 2024 is on track to set another record. Underlying demand for biologic medicines also remains on track to grow at a high single digit or better rate again for FY2024.

The Life Sciences segment remains challenged with Q2 trends largely consistent with those in Q1. Global pharma and biotech demand remains weak. Academic markets are weaker and applied markets performed comparatively better, particularly for DHR’s advanced solutions.

An improvement in the sales funnels and quoting activity in China is being driven by recently announced stimulus measures. DHR, however, does not anticipate an improvement in orders until 2025 as these programs are in the early stages of implementation. In the meantime, many customers are delaying purchasing decisions as they await funding.

Credit Ratings

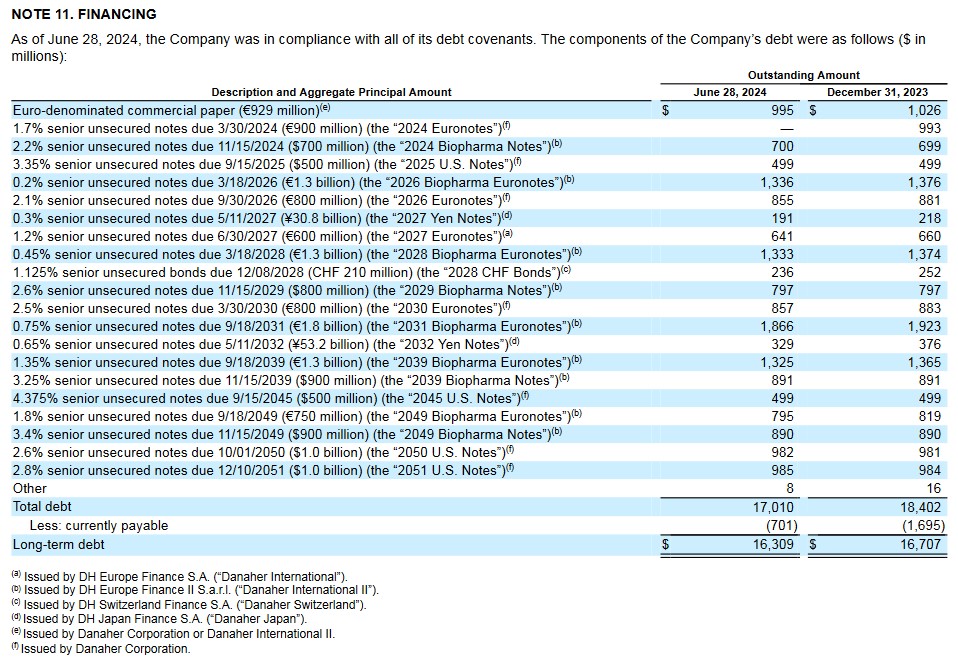

The following schedule reflects DHR’s long term debt at the end of Q2 2024. DHR borrows at very attractive rates and the scheduled maturity dates are well staggered.

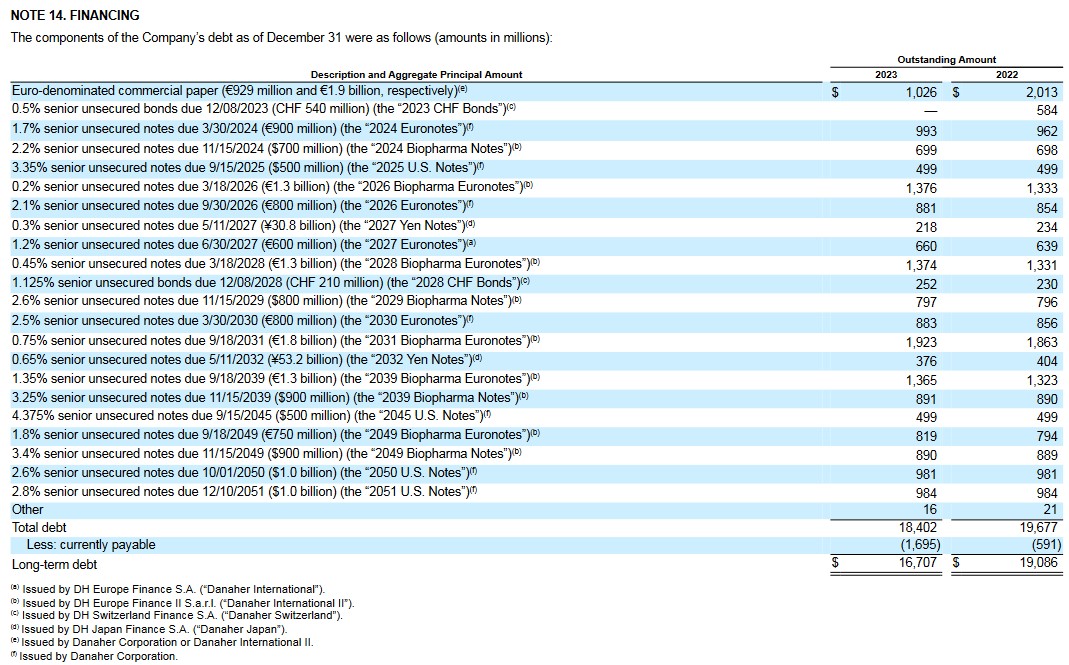

DHR’s debt schedule at FYE2022 and FYE2023 are provided for comparison.

DHR’s credit ratings are unchanged from my last review.

- Moody’s: Upgraded to A3 from Baa1 on October 10, 2022. This rating was recently affirmed and the outlook is stable.

- S&P Global: Upgraded to A- from BBB+ on June 11, 2022. This rating was recently affirmed and the outlook is stable.

Both ratings are at the bottom tier of the upper-medium investment-grade tier and define DHR as having a STRONG capacity to meet its financial commitments. However, DHR is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

These ratings satisfy my conservative investment profile.

Dividend and Dividend Yield

DHR’s quarterly dividend is likely to remain a negligible portion of the total investment return.

DHR distributed its 3rd consecutive $0.27/share quarterly dividend on October 27, 2023. When it declared its quarterly dividend in December, however, it lowered the quarterly dividend to $0.24. This arose because of the Veralto spin-off.

The $0.27/share quarterly dividend was restored with the declaration dividend payable on April 26, 2024.

I remain of the opinion that investors who fixate on dividend metrics are missing the ‘big picture’; the focus should be on total potential long-term investment returns!

The diluted average common stock and common equivalent shares outstanding (in millions) in FY2012 – FY2023 are 713, 711, 716, 709, 700, 706, 710, 726, 719, 737, and 737. The increase in diluted average common stock and common equivalent shares outstanding in recent years is primarily the result of the conversion of On April 15, 2022, all outstanding shares of the 4.75% MCPS Series A converted and on April 15, 2023, the 5% MCPS Series B converted.

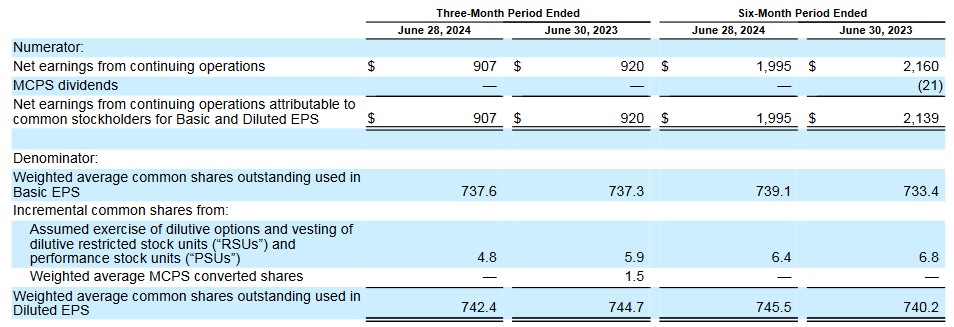

The weighted average rose to ~748.6 in Q1 2024 but dropped to 742.4 in Q2 2024.

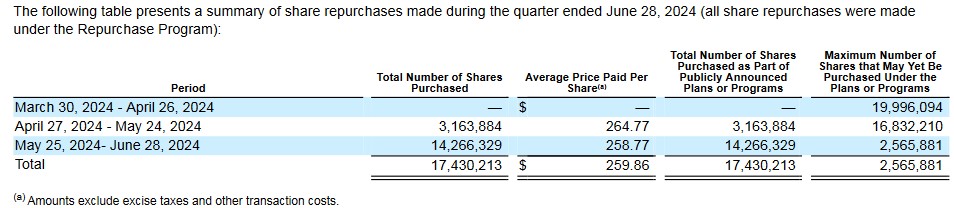

The following tables reflect repurchases in Q2 and the impact on the weighted average number of outstanding shares.

Subsequent to the end of Q2 2024, DHR repurchased 1.9 million shares of the remaining shares available for repurchase under the Repurchase Program for $0.467B, excluding excise taxes and other transaction costs.

On July 22, 2024, DHR’s Board approved a new repurchase program authorizing the repurchase of up to an additional 20 million shares of common stock from time to time on the open market or in privately negotiated transactions.

DHR is hyper-focused on capital allocation and the Board feels superior long-term investor returns can be generated by retaining funds in the company. On the Q2 earnings call, management states:

While M&A remains our bias for capital deployment, we believe these repurchases will provide an attractive return given the strength of our long-term organic growth, earnings and cash flow outlook.

Valuation

As noted in previous DHR posts, comparing Danaher’s valuation relative to its historical valuation is difficult. This is because it has undergone a radical transformation over the last few years after having divested slower-growing businesses and acquiring several faster-growing businesses.

When I last reviewed DHR, it had reported a YTD2023 FCF to net income conversion of 124% in the first 9 months of FY2023. I elected, however, to stick with my arbitrary 120% FCF to net income conversion ratio to gauge DHR’s valuation. I then:

- multiplied the the FY2023 $8.57 mean adjusted diluted EPS guidance from analysts by 120%, thereby giving me $10.28 FCF/share; and

- divided the ~$197 share price by $10.28 thus giving me a ~19.2 P/FCF.

At the same time, I took the ~$197 share price and the forward-adjusted diluted EPS broker estimates to calculate DHR’s forward-adjusted diluted PE.

- FY2023 – 29 brokers – mean of $8.57 and low/high of $8.21 – $9.01. Using the mean estimate, the forward adjusted diluted PE was ~23.

- FY2024 – 14 brokers – mean of $8.05 and low/high of $7.27 – $9.80. Using the mean estimate, the forward adjusted diluted PE was ~24.5.

- FY2025 – 11 brokers – mean of $8.95 and low/high of $8.14 – $10.19. Using the mean estimate, the forward adjusted diluted PE was ~22.

DHR has now reported diluted EPS of $2.68 and $3.63 of adjusted diluted EPS for the first half of FY2024. Should DHR generate $2.90 and $3.85 in diluted EPS and adjusted diluted EPS in the second half of FY2024, we are looking at $5.58 and $7.48. Using my estimates and the current ~$264 share price, the forward diluted PE is ~47.3 and the adjusted diluted PE is ~35.3.

Broker estimates are likely to be adjusted over the next several days but using the current estimates, DHR’s forward adjusted diluted PE levels and the current ~$264 share price are:

- FY2024 – 24 brokers – mean of $7.59 and low/high of $7.46 – $7.94. Using the mean estimate, the forward adjusted diluted PE is ~34.8.

- FY2025 – 24 brokers – mean of $8.69 and low/high of $8.26 – $9.49. Using the mean estimate, the forward adjusted diluted PE is ~30.4.

- FY2026 – 18 brokers – mean of $9.74 and low/high of $9.07 – $10.96. Using the mean estimate, the forward adjusted diluted PE is ~27.1.

Since the active acquisition/divestiture of businesses distorts EPS, I prefer to look at DHR’s Price/FCF to gauge its valuation.

The YTD Free Cash Flow from Continuing Operations to Net Earnings from Continuing Operations Conversion Ratio is currently 129%. If we conservatively lower this to 125% and multiply this by my FY2024 $7.48 mean adjusted diluted EPS estimate, we get $9.35 FCF/share. Divide ~$264 by $9.35 and we get a ~28.2 P/FCF.

DHR’s P/FCF in FY2014 – FY2023 is 17.40, 18.82, 16.14, 17.33, 17.69, 27.86, 34.02, 28.79, 20.46, and 19.83. It is difficult to draw a comparison with these historical results because DHR has changed considerably in the last few years.

I consider a fair value to be closer to ~$250 – ~$255. If I use my $9.35 FCF/share estimate for FY2024 this gives me a P/FCF of ~26.7 – ~27.3.

Final Thoughts

Despite challenges throughout 2023, DHR continues to strengthen its portfolio with M&A and through proactive steps to improve its cost structure. It has exited the pandemic as a stronger company having replaced revenue contribution from spun-off entities (Envista in 2019 and Veralto in 2023) with higher growth, higher-margin annuities with the Cytiva, Aldevron and Abcam acquisitions. In addition, Cepheid’s respiratory franchise is now 6x larger than it was prior to the pandemic; the acquisition of Cepheid closed at the beginning of November 2016.

I currently hold 445 shares in a ‘Core’ account in the FFJ Portfolio. It was my 28th largest holding when I completed my 2023 Year End FFJ Portfolio Review and my 22nd largest holding when I completed my 2024 Mid Year FFJ Portfolio Review.

As noted in several previous posts, I prefer to acquire shares in wonderful companies whose valuation has come under pressure because of short-term headwinds.

My last 3 DHR purchases were in January, April, and July 2023 at which time shares were attractively valued. Now, business conditions appear to be improving and recently reported better than expected results has led to a ~$40 surge (~$224 – ~$264) in DHR’s share price since early July. I think this share price increase is overdone and now Danaher is marginally overvalued.

I remain cautious in this environment and have raised liquidity in the hope that I will be able to acquire shares in companies that appeal to me at more favorable valuations. DHR is one such company.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long DHR.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.