I am currently re-reading Richer, Wiser, Happier How the World’s Greatest Investors Win in Markets and Life by William Green, a book listed in the Books section of this blog. Over the years, the author interviewed many of the world’s prominent investors. They spoke candidly about their setbacks and challenges and shared the most valuable lessons they have learned about how to:

- invest intelligently;

- think rationally;

- overcome adversity; and

- stack the odds of building a happy and fulfilling life.

Recurring themes expressed by these great investors are:

- the importance of acquiring undervalued assets; and

- stacking the odds of success in an investor’s favor.

Howard Marks, who publishes insightful Memos that are accessible through the Oaktree Capital website, often says:

The environment is what it is. We can’t demand a more favorable set of market conditions. But we can control our response, turning more defensive or aggressive depending on the climate.

Keeping Marks’s wise words in mind, I have been very defensive in this environment. I did, however, disclose in my November 23, 2024 post the purchase of additional shares in Thermo Fisher (TMO), Danaher (DHR), and Veeva (VEEV) on November 18 and 19 at which time I considered shares to be undervalued.

Following these purchases, the share price of TMO and VEEV have surged; their respective valuation has increased to the extent where I am not prepared to add to my exposure. There has, however, been minimal change in DHR’s share price.

Business Overview

Wide moat DHR, a leading global life sciences and diagnostics innovator, is comprised of a diverse set of businesses across Biotechnology, Diagnostics, and Life Sciences. Information about its various businesses is accessible here.

Through its Danaher Business System (DBS), its strives for continuous improvement of its scientific technology portfolio. It seeks out attractive markets and makes acquisitions to enter or expand within these fields. Once DHR completes an acquisition, it aims to accelerate core growth at acquired companies by making R&D and marketing-related investments. It also implements

lean manufacturing principles and administrative cost controls to boost operating margins.

In addition to making multiple acquisitions over the years, DHR divests itself of assets no longer deemed ‘Core’.

These strategic acquisitions and divestitures have pushed it into attractive end markets with strong growth prospects and sticky, recurring revenue streams. It has now become a major industry participant in the highly fragmented and relatively sticky life science and diagnostic tool markets.

What I particularly like about the life science end market is its:

- strong growth trajectory;

- high margins; and

- high switching costs associated with regulatory and reproducibility concerns of end users.

The industry has experienced headwinds over the past ~1 – 2 years but we must remember that almost everything is cyclical. For example, the economy expands and contracts; consumer spending waxes and wanes; corporate profitability rises and falls; the availability of credit eases and tightens; asset valuations soar and sink.

Howard Marks compares these patterns to the swinging of a pendulum from one extreme to the other.

So while DHR may be experiencing challenging business conditions in the short-term, the long-term outlook is promising.

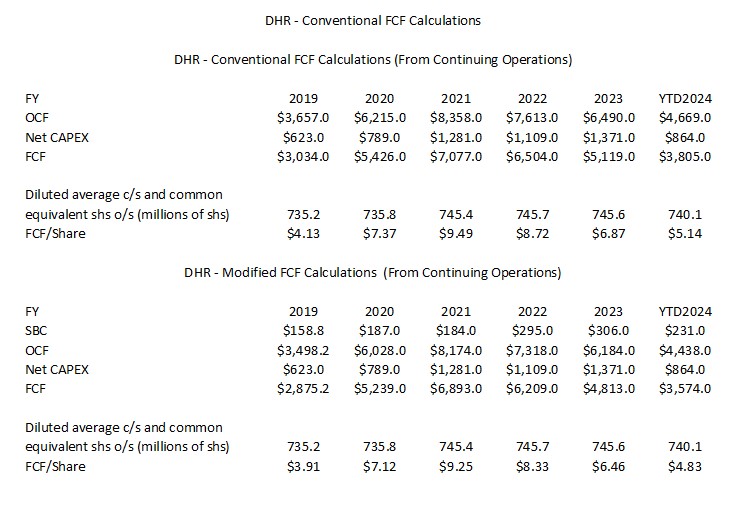

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In several recent posts I express my thoughts about the conventional method by which many companies calculate Free Cash Flow (FCF). Since FCF is a non-GAAP metric, there is no standardization in the calculation of FCF.

In most cases, companies merely deduct net CAPEX from net cash flows from operating activities. I think it is also necessary to deduct share based compensation (SBC).

Many companies employ SBC as part of their employee compensation plans and reflect this cost within the Income Statement. Because SBC involves no cash outlay, however, companies add back SBC to determine net cash flows from operating activities in the Condensed Consolidated Statement of Cash Flows.

Suppose, however, that DHR were to compensate employees 100% by way of SBC. Since there is no cash outlay, the full amount of its employee compensation is added back in the Condensed Consolidated Statement of Cash Flows to determine net cash flows from operating activities.

If, on the other hand, DHR were to have no SBC and were to actually disburse funds to pay its employees, nothing would be added back in the Condensed Consolidated Statement of Cash Flows.

By merely changing the manner in which it compensates its employees we get very different net cash flows from operating activities! How does this make any sense? Is the use of SBC not a form of ‘financing’? Would it be more proper to reflect SBC within the Cash Flows From Financing Activities section of the Condensed Consolidated Statement of Cash Flows? This way, we would arrive at similar FCF results no matter how a company chooses to compensate its employees.

The following table reflects data extracted from the FY2019 – FY2023 and Q3 2024 reconciliation of GAAP and non-GAAP financial measures and supplemental forward-looking information documents that are accessible here. The section with the modified FCF calculations deducts share based compensation (SBC) from total operating cash provided by continuing operations.

NOTE: The YTD2024 data reflects results only for the first 3 quarters of FY2024.

Valuation

DHR generated $3.80 and $5.34 of diluted EPS and adjusted diluted EPS in the first 3 quarters of FY2024. If it were to generate ~$5.07 and ~$7.12 of diluted EPS and adjusted diluted EPS for the year, the forward diluted PE and forward adjusted diluted PE using my December 9 ~$233.97 purchase price is is ~46.1 and ~32.9.

DHR’s valuation using the current broker guidance is:

- FY2025 – 25 brokers – mean of $7.50 and low/high of $7.40 – $7.63. Using the mean, the forward adjusted diluted PE is ~31.2.

- FY2026 – 25 brokers – mean of $8.38 and low/high of $8.08 – $8.73. Using the mean, the forward adjusted diluted PE was ~28.

- FY2027 – 18 brokers – mean of $9.42 and low/high of $8.86 – $10.0. Using the mean, the forward adjusted diluted PE was ~24.8.

DHR typically reports significant depreciation and amortization expenses every year which depresses earnings. In the first 9 months of FY2024, DHR reported ~$1.782B of depreciation and amortization expenses. It also reported ~$0.222B in impairment charges related to an indefinite-lived trade name within the genomics consumable business included in the Life Sciences segment. This determination was primarily the result of softness in the genomics market, including but not limited to the discontinuation of drug development programs announced in the third quarter and weaker demand at some of the business’s larger customers as well as reduced demand due to the reprioritization of drug development programs at other customers.

Essentially, DHR’s earnings were depressed by non-cash items of ~$2B in the first 3 quarters of FY2024.

Looking at DHR’s valuation from a cash flow perspective, suppose DHR generates ~$7.20 and ~$6.54 of FCF/share in FY2024 using the ‘conventional’ and ‘modified’ FCF calculation methods. Based on my recent purchase price, DHR’s P/FCF under the ‘conventional’ and ‘modified’ methods are ~32.5 and ~35.8.

Final Thoughts

The valuations reflected above would suggest that DHR is NOT ‘on sale’. While the release of FY2025 guidance will only happen with the release of Q4 and FY2024 results, I envision that DHR will return to more ‘normal’ growth rates in FY2025. If this does happen, I expect earnings and cash flow to improve.

Keeping in mind that everything is cyclical, I expect business conditions will eventually improve in the healthcare sector and in the life sciences and diagnostics industry in particular. Once this happens, DHR will likely attract greater interest from investors thus pushing up the share price. I do not want to wait for this to happen thus the reason why I have further increased my exposure to this ‘out of favor’ existing holding.

My ~$233.97 purchase price is just a shade above the ~$229 price I paid when I acquired an additional 100 shares on November 18. If DHR reaches ~$280 (what I consider to be a fair price), the difference between the fair price and my recent purchase price is a ~19.7% gain.

The Bank of Canada’s inflation-control target range is 1% – 3%, with a target midpoint of 2%; the bank expects inflation to remain near the middle of this range. Even if the rate of inflation were to unexpectedly surge above 6%, the total rate of return from my recent DHR purchase is likely to far exceed the rate of inflation.

Following my December 9 purchase, my current exposure is 700 shares in a ‘Core’ account in the FFJ Portfolio.

DHR was my 28th largest holding when I completed my 2023 Year End FFJ Portfolio Review and my 22nd largest holding when I completed my 2024 Mid Year FFJ Portfolio Review. I will be performing a similar review at the end of 2024 at which time I will be able to determine its current standing.

On a final note, the return of the Trump administration may present opportunities and challenges to the life science and diagnostic industry. This new administration, however, will only be around for 4 years. Although DHR will certainly need to navigate its way through short and mid-term time frames, it is making strategic investment decisions that bode well for its long-term success. In my opinion, investors should take advantage of DHR’s temporary weakness.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long TMO, DHR, and VEEV.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.