I have covered Copart (CPRT) in several prior posts that are accessible through the Archives.

When I wrote my May 17, 2024 Copart – A Wonderful Wide Moat Company post, CPRT had recently released its Q3 and YTD2024 results. We now have CPRT’s Q4 and FY2024 results (released after the September 4 market close) thus prompting me to revisit this existing holding.

If you have ever toured scrapyards, you have likely never considered that one company in this unglamorous industry could generate just over $4.2B of annual revenue.

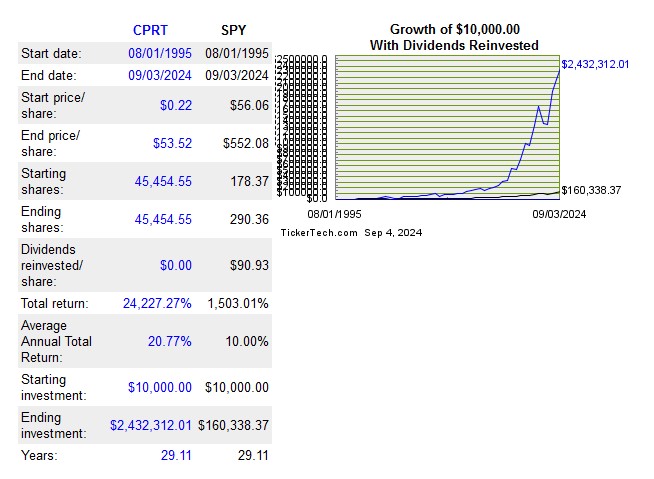

While past performance is not indicative of future performance, it is hard to overlook the extent to which it has rewarded long-term investors.

Source: Tickertech.com

Business Overview

In my May 17 post I note that CPRT has ~19,000 acres (~29.7 square miles or ~76.9 square kilometers) of outdoor vehicle storage of which 90% is owned and 10% is leased. This acreage is more than double what it had in 2015. In addition, it has a robust fleet of transportation assets.

To put this in perspective, the Island of Montreal is 472.55 square kilometers. The total land CPRT owns or leases is ~16.3% of the Island of Montreal. Imagine damaged vehicles neatly arranged that covers an area of this magnitude!

Financials

Q4 and FY2024 Results

CPRT’s financial results are available through the SEC Filings section of the company’s website.

At FYE2024, CPRT had $3.42B in cash and investments and its TOTAL liabilities amounted to ~$0.879B. This is all the more impressive considering purchases of property and equipment in FY2014 – FY2024 amounting to ~$3.6B. All this has been financed from cash flow generated through normal business operations.

CPRT continues to grow its business with insurance sellers.

The recent decline in used vehicle values has driven total loss frequency upwards back in line with pre-pandemic historical norms.

The long-term trends in the repair industry toward increasing vehicle complexity as measured, for example, by the average number of parts to repair a vehicle as well as rising labor rates continue to tip the scales in favor of totaling vehicles rather than repairing them.

CPRT continues to deepen its relationships with its insurance company clients by offering a range of sophisticated tools to assist them with optimizing their decisions. An example of this is the ongoing expansion of CPRT’s Title Express service offering. Historically, auction houses obtained salvage certificates from the states in which business is conducted after the insurance companies first obtained the original title either directly from policyholders if they own their cars outright or from lenders if the vehicles had liens outstanding.

Historically, insurance companies always reasoned it would be best to keep this function in-house. Now, however, CPRT offers an integrated one-stop solution (Title Express) for title procurement.

On behalf of its carrier clients, CPRT obtains original titles from policyholders and from lenders. Each state has its specific nuances regarding its requirements (ie. documentation, signatures, secured forms, powers of attorney.etc). Each lender also has its own requirements for the provision of payoff balances and per diems and the release of titles.

CPRT’s substantially more efficient title procurement process has led to it approaching a run rate of ~1 million titles obtained per year on behalf of its insurance clients.

CPRT benefits from active storm seasons and 2024 is off to an active start. Hurricane Beryl was a deadly and destructive Category 5 Atlantic hurricane that caused widespread damage across Texas, Louisiana and neighboring states in late June and early July 2024; it was the earliest-forming Category 5 hurricane on record and the second such storm in the month of July.

In addition to Hurricane Beryl, Hurricanes Debbie and Ernesto required significant mobilization of CPRT’s resources on behalf of its insurance clients.

CPRT is also growing its business with non-insurance sellers; the non-insurance unit volume growth continues to outpace that of CPRT’s insurance business. This volume growth substantially comes from fleet rental and finance units which increased over 20% in Q4 and ~28% for the year and dealer units, which increased ~10% for the quarter and 15+% for FY2024.

The reason CPRT is able to grow its non-insurance business is that it has the physical storage capacity via its sizable real estate portfolio and a strong network of logistics solutions.

CPRT’s Blue Car business, which serves the bank and finance fleet and rental segments experienced ~20.4% YoY volume growth. The dealer sales volume, the combination of Copart Dealer Services and NPA (CPRT’s Powersports auction platform) increased volumes sold by 9.5% YoY.

CPRT’s partner in the equipment arena (Purple Wave) experienced ~17% YoY growth for the full fiscal year, outpacing industry growth in the equipment auction markets it serves.

Capital Allocation Strategy

CPRT’s capital allocation strategy continues to prioritize the deployment of capital to grow the business. This consists of investing in:

- employees;

- operational capabilities including logistics;

- technology;

- real estate; and

- customer experience.

In FY2024, CPRT acquired more than 1,100 acres of land and 370 transportation assets. This demonstrates how CPRT continues to prioritize investments that grow and diversify the existing businesses including differentiated products and service capabilities. This also includes yard infrastructure investments, which are critical to ensuring that it is positioned to serve its customers’ needs for the long term.

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In FY2014 – FY2024:

- OCF was (in billions of $ approx.) 0.263, 0.265, 0.332, 0.492, 0.535, 0.647, 0.918, 0.991, 1.177, 1.364, and 1.473.

- CAPEX was (in billions of $ approx.) 0.082, 0.079, 0.174, 0.172, 0.288, 0.374, 0.592, 0.463, 0.337, 0.517, and 0.511.

- FCF was (in billions of $ approx.) 0.181, 0.186, 0.159, 0.320, 0.247, 0.273 0.326, 0.528, 0.839, 0.848, and 0.962.

Return On Invested Capital (ROIC)

In FY2014 – FY2023, CPRT’s ROIC (%) was 14.99, 15.86, 18.87, 26.34, 23.28, 29.15, 27.62, 27.03, 25.11, and 22.81.

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company’s cost of capital will be lower than this level. In the past 7 fiscal years, CPRT’s ROIC has exceeded 20%!

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

FY2025 Outlook

CPRT does not provide any outlook.

Risk Assessment

CPRT has no debt to rate.

At FYE2024, CPRT had ~$4.67B of liquidity comprised of ~$3.42B in cash and investments and a ~$1.25B revolving credit facility.

Dividend and Dividend Yield

CPRT has not paid a cash dividend since becoming a public company in 1994.

Stock Splits

CPRT’s stock split history is reflected below.

In FY2013 – FY2024, CPRT’s weighted average number of outstanding shares (in millions of shares rounded) was 1,038, 1,050, 1,051, 977, 948, 968, 962, 955, 961, 965, 967, and 975.

On September 22, 2011, CPRT’s Board authorized a 320 million share increase in the stock repurchase program, bringing the total current authorization to 784 million shares.

Share repurchases were made in:

- 2013: $572 thousand

- 2014: $15,009 million

- 2015: $233,484 million

- 2016: $442,855 million

- 2018: $364,997 million

No repurchases were made in FY2017, FY2018, FY2020 – FY2024 with capital allocation having been focused on expanding operations.

Stock based compensation during the FY2013 – FY2020 time frame has hovered in the $18 – $24 million range. In FY2021 – FY2023, this increased to the $39 – $41 million range before pulling back to ~$35 million in FY2024.

It is readily apparent that CPRT could repurchase a significant number of its shares. Having said this, the most optimal means by which to allocate capital is not always in the form of share repurchases.

Valuation

I reference my September 16, 2023 and May 17, 2024 posts in which I touch upon CPRT’s valuation at the time of prior reviews.

On May 17, I acquired additional shares at ~$53.93. Using this share price and the current broker estimates, the forward-adjusted diluted PE levels were:

- FY2024 – 11 brokers – ~37.2 based on the mean of $1.45 and low/high of $1.43 – $1.49.

- FY2025 – 11 brokers – ~33.1 based on the mean of $1.63 and low/high of $1.55 – $1.68.

- FY2026 – 5 brokers – ~30 based on the mean of $1.79 and low/high of $1.65 – $1.89.

CPRT generated $1.42 of diluted EPS in FY2024. Following the earnings release after the September 4 market close, the share price has fortunately pulled back on September 5 thus prompting me to acquire an additional 200 shares @ $49.16. Using the trailing 12-month EPS, CPRT’s diluted PE is ~34.62.

Broker estimates are currently being updated but as I compose this post on September 5 and using my recent purchase price, the forward-adjusted diluted PE levels are:

- FY2025 – 10 brokers – ~31.1 based on the mean of $1.58 and low/high of $1.48 – $1.67.

- FY2026 – 6 brokers – ~28.25 based on the mean of $1.74 and low/high of $1.65 – $1.89.

- FY2027 – 2 broker – ~25.2 based on the mean of $1.95 and low/high of $1.90 – $2.00.

On a FCF basis, we know that CPRT generated $0.962B in FY2024. The weighted average diluted shares outstanding in Q4 was 976,500 million and 974,798 million in FY2024. If we divided $962 million by 976,500 million shares, we get ~$0.99 FCF/share. Using my $49.16 purchase price, the forward P/FCF is ~50.

If CPRT were to allocate $0.5B toward the repurchase of its shares at ~$50/share, it could repurchase ~10 million shares. In doing so and continuing to issue shares as part of its compensation structure, the FY2025 weighted average could drop to ~967 million shares. If it were to generate $1.1B of FCF in FY2025, we would be looking at FCF/share of ~$1.138. Using my $49.16 purchase price, the forward P/FCF is ~43.2.

Were CPRT to double its repurchases to ~$1B @ ~$50/share, it could repurchase ~20 million shares. At this level, the FY2025 weighted average could potentially drop to ~957 million shares. If it were to generate $1.1B of FCF in FY2025, we would be looking at FCF/share of ~$1.15. Using my $49.16 purchase price, the forward P/FCF is ~42.7.

Were CPRT to generate ~$1.2B of FCF in FY2025 and the FY2025 weighted average were to drop to ~957 million shares, we would be looking at ~$1.254 FCF/share. Using my $49.16 purchase price, the forward P/FCF is ~39.2.

Performing a sensitivity analysis can lead to vastly different results.

Final Thoughts

My final thoughts are unchanged from prior posts.

Despite being richly valued, I like:

- that management is efficiently allocating its capital to retain its industry leadership status;

- the long-term trends continue to tip the scales in favor of totaling vehicles rather than repairing them;

- how the value of the acreage CPRT reflected on the Balance Sheet is well below current market value – CPRT started acquiring land decades ago;

- that senior management has ‘skin in the game’ meaning their interests are closely aligned with long-term investors;

- that growth is not fueled with debt. CPRT has acquired ~$3.6B property and equipment in FY2014 – FY2024 without debt financing;

- ~$4.67B of liquidity; and

- that OCF and FCF are consistently strong.

One of my recommended readings in the Books section of this site is Copart – Junk to Gold – Lessons I Learned as told by Willis Johnson – founder of Copart (CPRT) and written by Marla J. Pugh. I ordered the book from the company’s website and unfortunately, do not have a pdf version.

CPRT was my 23rd largest holding when I completed my 2023 Year End FFJ Portfolio Review and my 10th largest holding when I completed my 2024 Mid Year FFJ Portfolio Review.

Following my September 5 purchase, I own:

- 2,600 shares at an average cost of ~$35.4537 in a ‘Core’ account within the FFJ Portfolio;

- 400 shares at an average cost of ~$54.60 in a different ‘Core’ account; and

- 540 shares at an average cost of ~$53.93 in a ‘Side’ account.

My weighted average cost is ~$40.44.

In addition, a couple of young investors I am helping on their journey to financial freedom have exposure to CPRT; I do not disclose details of their investments and exclude these shares when I complete my Mid Year and Year End FFJ Portfolio Reviews.

I have absolutely no idea whether management is going to repurchase any shares in FY2025.

I know shares appear to be richly valued. Based on CPRT’s track record, however, I envision shares will be worth considerably several years into the future.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CPRT.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.