Contents

![]()

On October 29, 2020, Church & Dwight Co., Inc. (CHD) released Q3 and YTD 2020 results and included raised growth guidance for FY2020 Reported Sales, Organic Sales, Adjusted EPS, and Cash from Operations.

CHD's valuation is currently elevated. On the bright side, it continues to maintain an impressive Cash Flow Conversion Cycle relative to its peer group and it continues to strengthen its Balance Sheet.

Although CHD's dividend yield is typically ~1.00% or lower, the company has consistently paid a quarterly dividend. In fact, it has just declared its 479th regular quarterly dividend.

Summary

- CHD released Q3 and YTD2020 results and provided revised FY2020 guidance on October 29th.

- It continues to generate strong Free Cash Flow and has an exemplary cash conversion cycle.

- Founded in 1846, CHD has acquired 11 of its 12 Power Brands since 2001 and the plan is to increase this to 20 Power Brands in the years to come.

Introduction

If you have been investing for a number of years you undoubtedly have had your share of 'winners'. In my case, Church & Dwight Co., Inc. (CHD), my second largest holding, happens to be one of my 'winners'; my average cost is sub $15.60 and shares closed at ~$87 on October 29th.

As luck would have it, CHD crossed my path through work in late 2005. I knew little about this company but I was certainly familiar with its logo and decided to delve into the numbers. I was so impressed with what I saw that I decided to initiate a position!

When I initiated a position, CHD had a limited portfolio of brands. Fast forward to the present day and we see the extent to which CHD has grown through acquisition over the past ~15 years. In fact, CHD has acquired 11 of its 12 Power Brands since 2001 and the plan is to increase this to 20 Power Brands in the years to come.

Source: CHD – Barclays Global Consumer Staples Virtual Conference Presentation – September 9, 2020

Source: CHD – Barclays Global Consumer Staples Virtual Conference Presentation – September 9, 2020

And the future looks even brighter! In fact, in the Q3 2020 Press Release, CHD's CEO stated:

'TROJAN® launched the TROJAN G SPOT™ condom featuring a unique shape for targeted stimulation. FLAWLESS® launched NU RAZOR™, a waterless whole-body hair removal product for women to use anywhere, anytime.'

I mean, seriously! When a company introduces a condom featuring a unique shape for targeted stimulation and a waterless whole-body hair removal product for women to use anywhere, anytime....how can you not be upbeat about such a company! This is a company which brings pleasure to people's lives.

So...even though I disclosed in this article that CHD is already my 2nd largest holding, I am prepared to increase my exposure if I remain confident in the company's future and its products bring pleasure to so many.

Q3 2020 Results and FY2020 Guidance

CHD's Q3 2020 results and guidance for FY2020 can be accessed here. There is currently no accompanying Investor Presentation to the release of Q3 2020 results, and therefore, I draw yuor attention to CHD’s September 9, 2020 Barclays Global Consumer Staples Virtual Conference Presentation.

Despite the challenges presented by the COVID-19 pandemic, CHD has raised its full year outlook for sales, EPS, and cash flow.

Free Cash Flow

CHD continues to consistently generate strong Free Cash Flow (FCF) and to tightly manage its cash conversion cycle. This consistency provides CHD with the ability to acquire additional brands, reduce debt, develop new products, make capital expenditures for growth purposes, and/or increase dividends or repurchase shares.

These are the screenshots from CHD's September 9, 2020 presentation at the Barclays Global Consumer Staples Virtual Conference.

Source: CHD – Barclays Global Consumer Staples Virtual Conference Presentation – September 9, 2020

Source: CHD – Barclays Global Consumer Staples Virtual Conference Presentation – September 9, 2020

Compare the most recent results presented on September 9, 2020 with those presented at the September 3, 2020 Barclays Global Consumer Staples Conference.

Source: CHD – Barclays Global Consumer Staples Conference Presentation – September 3, 2019

Source: CHD – Barclays Global Consumer Staples Conference Presentation – September 3, 2019

While the FCF conversion and cash conversion cycle presented in September 2019 was impressive, CHD has improved upon those results!

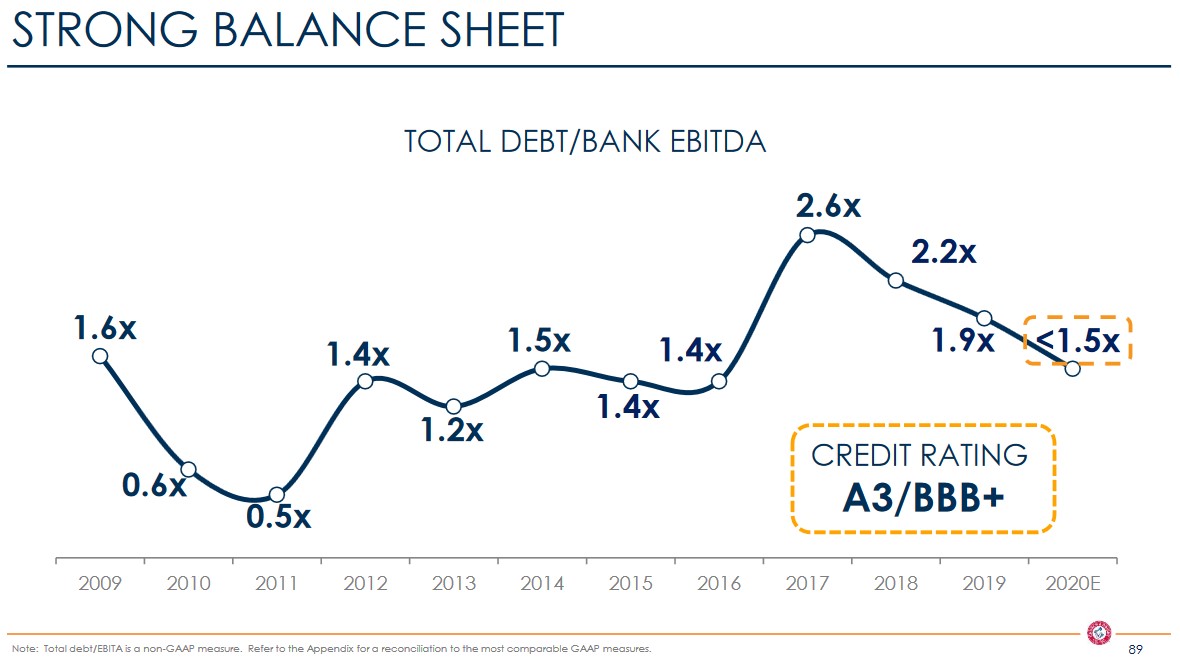

Credit Ratings

On October 7, 2019, Moody’s upgraded CHD’s long-term debt one notch to A3 (lowest tier upper medium grade) from Baa1 (top tier lower medium grade). This rating remains in place.

Standard & Poor’s assigned a BBB+ rating to CHD on June 28, 2013 and this rating remains in effect; this is one notch lower than Moody’s rating.

Looking at CHD's September 9, 2020 presentation we see the extent to which CHD's Balance Sheet has improved in a span of 1 year.

Source: CHD – Barclays Global Consumer Staples Virtual Conference Presentation – September 9, 2020

For comparison purposes, the following is what CHD's Total Debt / Bank EBITDA when it presented at the Barclays Global Consumer Staples Conference on September 3, 2019.

Source: CHD – Barclays Global Consumer Staples Conference Presentation – September 3, 2019

A noticeable improvement is evident.

Dividend, Dividend Yield, and Dividend Payout Ratio

CHD has paid a dividend for 479 consecutive quarters and its dividend history can be found here.

With shares currently trading at ~$87, the $0.24/share quarterly dividend ($0.96/share annually) provides a yield of ~1.10%. Although the dividend yield is low it is well covered by profits generated from normal business operations. Unlike other companies which have been borrowing to sustain their quarterly dividend, CHD's earnings and cash flow adequately cover the dividend.

On the basis of projected adjusted EPS of $2.79 - $2.81 for FY2020 we see that CHD's quarterly dividend of $0.24 is adequately covered (a ~34.3% dividend payout ratio on the basis of $2.80 in FY2020 adjusted EPS). If we conservatively increase the quarterly dividend by ~5.5% (similar to recent years) we can expect a quarterly dividend of ~$0.254 in FY2021 (~$1.02/year). Earnings and cash flow should easily cover this FY2021 projected quarterly dividend.

My existing CHD holdings are held within a Registered Retirement Savings Plan (RRSP) so I incur no withholding tax on the dividends received. The newly acquired shares are held in a taxable account so my quarterly dividend income will be reduced by 15% to $0.204/share/quarter or $0.816/share/year. On the basis of my $86.12 purchase price my dividend yield is ~0.95%. I am certain this low dividend yield will likely disway many investors from initiating a position in CHD. In hindsight I am thankful I did not let CHD's low dividend yield be a roadblock to investing in the company when I first analyzed it in 2005.

In my November 1, 2018 article I indicated that in fiscal 2011, the weighted average shares outstanding (Basic and Diluted) amounted to 286.4 million and 291.6 million, respectively. In fiscal 2017, these figures were 250.6 million and 256.1 million. At the end of FY2018...245.5 million and 250.7 million. As at September 30, 2019....246.4 million and 252.5 million. As at September 30, 2020....246.5 million and 252 million.

Stock repurchases were put on hold as a result of COVID-19 but in the Q3 2020 Earnings Release management indicated CHD's cash position is strong and stock purchases may resume in the future.

Valuation

At the time of my February 7, 2018 CHD article I had just acquired another 200 CHD shares on February 6th at $48.0799 and CHD’s management had just forecast 2018 adjusted EPS of $2.24 - $2.28. Using this range and the stock price of ~$48, I arrived at a forward adjusted PE range of ~21 - ~21.4.

When I wrote my May 8, 2018 article, management still had the same adjusted EPS outlook and CHD was trading at $47.73. As a result, there was negligible difference in valuation between February and May.

After the Q3 2018 earnings release, CHD’s stock price jumped to $64.87 and at the time of my November 1, 2018 article, the EPS and adjusted EPS outlook for FY2018 was $2.27 (a decline of 22% due to 2017 tax law changes and adjusted EPS growth of 17%). That meant CHD’s forward PE and forward adjusted PE was ~28.6 which was much higher than that I reported in my February and May 2018 articles.

When I wrote my February 2019 article, CHD had just released Q4 and FY2018 results and FY2019 guidance. With the drop in CHD’s share price to $60.46 I arrived at a valuation of ~26.6 based on $2.27 EPS; the forward valuation amounted to ~24.48 - ~24.9 based on $2.43 - $2.47 guidance.

When I wrote my November 1, 2019 article CHD was trading at ~$68.25 and guidance called for $2.47 in adjusted diluted EPS giving us a forward adjusted diluted PE of ~27.6. Using my conservative ~$2.40 - ~$2.45 in diluted EPS for FY2019 I arrived at a forward diluted PE range of ~27.9 - ~28.4.

Fast forward to October 29, 2020 when I acquired shares at $86.12. Using FY2020 adjusted EPS guidance of $2.79 - $2.81 ($2.80 mid-point) we get a forward adjusted PE of ~30.76. CHD is richly valued, and therefore, this is why I have limited my purchase to only 100 shares.

Final Thoughts

In several previous articles I have expressed my concern about what I perceive to be an element of irrational exuberance on the part of many investors. As a result, I have been extremly reluctant to deploy funds I have sitting on the sidelines. Today, I debated on whether to acquire additional CHD shares given that they are richly valued even after the recent share price pullback. As a satisfied consumer of several of CHD's products and as a long-term shareholder, I decided to acquire another 100 shares at $86.12 despite the lofty valuation. The newly acquired share are held in an account which I include when reporting my FFJ Portfolio holdings.

Stay safe. Stay focused.

I wish you much success on your journey to financial freedom!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to [email protected].

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long CHD.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.