![]()

Chevron (CVX) and Exxon Mobil (XOM) released their Q2 and YTD 2024 results on August 2. I reviewed XOM’s results in this post and concluded that investor sentiment is insufficiently negative to increase my exposure.

Looking at CVX’s Q2 2024 results, we see that they fell short of investors’ expectations and investor sentiment is somewhat negative. In addition, the delay of the Hess acquisition arbitration adds an element of uncertainty. I think this is creating an opportunity for anyone seeking to acquire CVX shares.

I last reviewed CVX in this November 6, 2023 post at which time the Q3 and YTD2023 results were the most current. Since a few quarters have elapsed since my last analysis, it is an opportune time to revisit this existing holding.

Business Overview

The 2023 Form 10-K and Annual Report has a wealth of information from which you can familiarize yourself with the company.

Hess Acquisition

In my November 6, 2023 post, I touched upon the ~$53B Hess acquisition announced in November 2023; a closing date in the first half of 2024 was targeted. This proposed acquisition was what would be CVX’s biggest takeover in two decades.

CVX’s had identified $1B of run-rate cost synergies it expected to realize within a year of closing. The transaction was also to become accretive to cash flow per share in 2025 after achieving synergies and start-up of the fourth floating production, storage and offloading vessel (FPSO) in Guyana.

In making the acquisition announcement, CVX indicated it would be repurchasing shares at a rate of ~$17.5B/year meaning the shares to be issued for the Hess acquisition would be repurchased in 2 – 3 quarters. The rationale for this was to alleviate any concern shareholders may have about dilution.

Furthermore, commodity prices can be quite volatile. If the purchase were to consist of a significant cash component, commodity prices could swing considerably higher or lower between the acquisition announcement and closing. The use of equity for the purchase, however, locks in the exchange ratio. This essentially creates a hedge against commodity price movement.

Not everything, however, has gone according to plan.

XOM operates and owns 45% of a deep-water oil block in Guyana known as Stabroek, a 6.6 million acre offshore oil reservoir off Guyana’s Atlantic coast; this is the largest oil discovery of the past decade. Hess and China’s CNOOC Ltd. (the third-largest national oil company in China) own the remaining 30% and 25%, respectively.

In early 2024, XOM accused CVX of attempting to circumvent XOM’s right-of-first-refusal provision by negotiating the Hess deal and announced its decision to seek arbitration on this proposed acquisition. CNOOC joined XOM by moving to arbitration to assert its right over Guyana’s oil field.

XOM and CNOOC are confident their interpretation of intent in a Guyanese oil contract signed a decade ago will prevail. CVX has countered that after thorough due diligence, the provision does not apply to a corporate merger.

The extent to which oil executives covet Stabroek is borne out by CVX’s CEO’s comment that CVX would walk away from the entire Hess deal if the Guyana stake is excluded.

The arbitration case is to be held in the International Chamber of Commerce in Paris in May 2025. This delay is yet another blow to the embattled deal, which is still under review by the U.S. Federal Trade Commission; the FTC plans to delay its decision whether to try to block the merger until after the arbitration case is settled.

US Shale Oil Industry Rebuilding Well Productivity

US shale oil and gas companies have experienced years of productivity declines. This is because fracking, the extraction method that emerged in the mid-2000s, has become less efficient. In fracking, water, sand and chemicals are injected at high pressure underground to release the trapped resources. Two decades of drilling wells relatively close together, however, has resulted in hundreds of thousands of wells. This has, inevitably, interfered with underground pressure thus making it more difficult to extract oil out of the ground.

Technological advances, however, are making it possible for US shale oil and gas companies to reverse years of productivity declines. The new oilfield innovations which began being implemented more widely in 2023 have made it possible for fracking to be faster, less expensive, and higher yielding. Advances made in the past few years include the ability to double the length of lateral wells to 3 miles. In addition, equipment can simultaneously frack 2 – 3 wells and electric pumps can replace high-cost, high maintenance diesel equipment.

The drawback is that the related requirement to frontload costs by drilling many more wells is deterring some companies from doing so.

Mid-sized shale firms like Pioneer Natural Resources that can afford the costs were first to embrace these new methods; Pioneer has recently been acquired by XOM.

Whether XOM and CVX embrace these new methods is up for debate. Both have committed to using oil revenue to increase shareholder returns rather than drilling expansion and have missed targets for Permian production in the past years.

XOM has stated that its own new fracking technology will allow it to extract an extra 700,000 barrels of oil equivalent per day (boepd) from Pioneer’s assets by 2027, tripling output to 2 million boepd.

CVX is increasing the use of simul fracturing operations in which it pumps down two wells while perforating the other two. The simul fracturing technique is expected to help CVX increase Permian production by 10% in 2024 to 900,000 boepd. It also allows CVX to complete more lateral footage in the same amount of time compared to zipper fracturing operations.

Zipper fracturing is a method to improve production performance in wells in pad-drilling applications. This method refers to fracturing two or more parallel horizontal wells. The fracturing treatment is performed stage by stage alternatively along the two wells.

CVX is also in various stages of piloting different chemicals and using gas injection and gas lift in different ways to improve flow in the Permian. The meaningful effects these pilot projects are having on CVX’s overall Permian productivity, however, are still relatively muted.

Financials

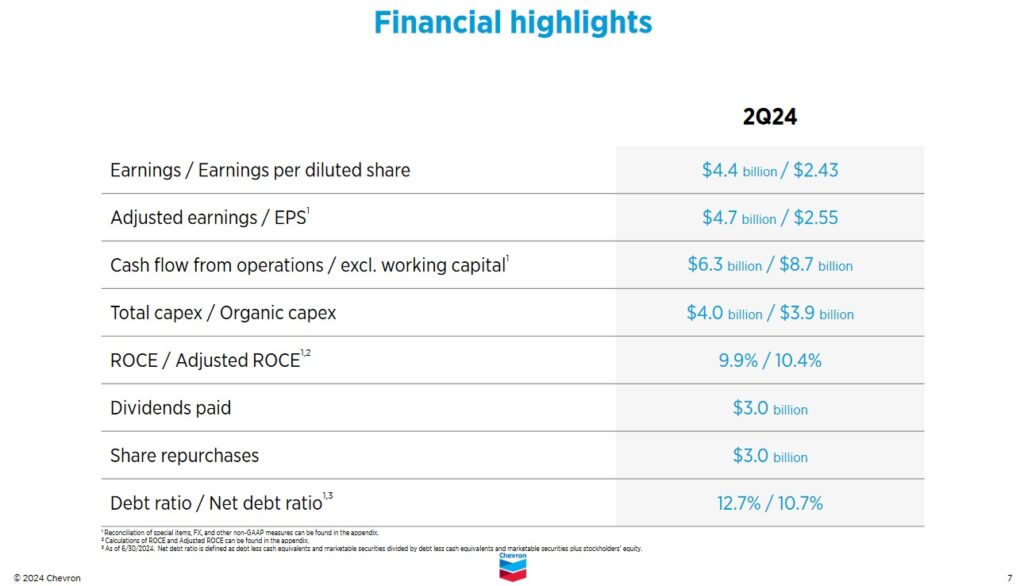

Q2 and YTD2024 Results

Material related to CVX’s Q2 and YTD2024 earnings release is accessible here. The Q2 2024 Form 10-Q is currently unavailable. When published, it will be available here.

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

CVX is a highly capital intensive business as borne out by its annual CAPEX levels. High CAPEX has its advantages and disadvantages. A key advantage is the high barriers to entry. You may get new industry participants but they can not compete directly with CVX. Going forward, we will witness more industry consolidation with CVX likely to be an acquirer.

In the FY2014 – FY2023 time frame, CVX’s:

- OCF was (in B$) 31.48, 19.46, 12.85, 20.52, 30.62, 27.31, 10.58, 29.19, 49.60, 35.61.

- CAPEX was (in B$) 35.41, 29.50, 18.11, 13.40, 13.79, 14.12, 8.92, 8.06, 11.97, 15.83 .

- FCF was (in B$) -3.65, -8.04, -4.82, 7.20, 17.13, 11.27, 3.26, 22.79, 35.56, 23.12.

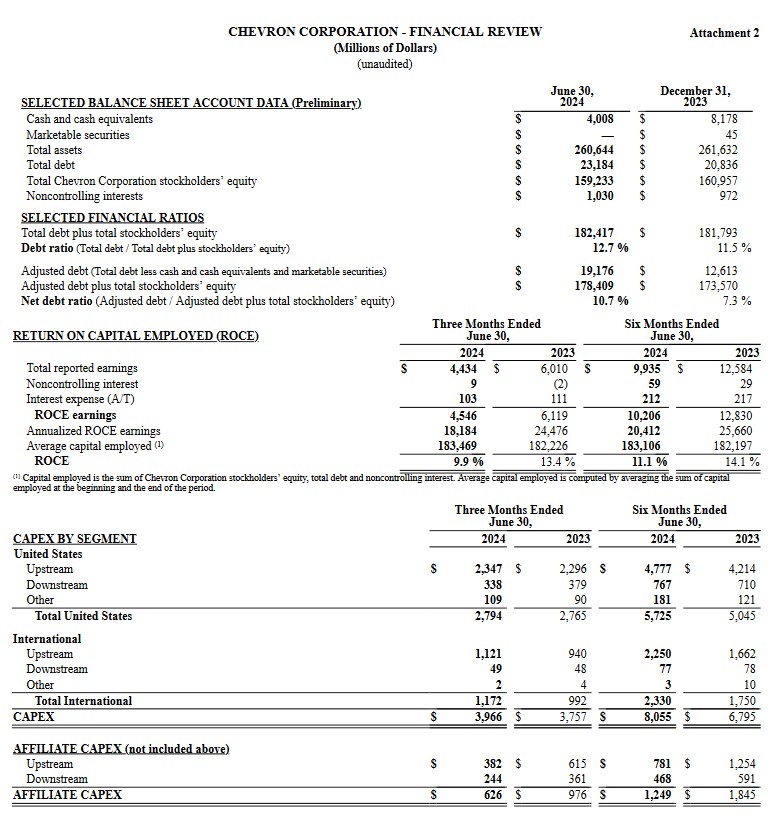

In the first half of FY2024, CVX generated OCF of ~$13.1B, incurred ~$7.9B of net CAPEX, and generated FCF of ~$5.2B.

Return On Invested Capital (ROIC)

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company’s cost of capital will be lower than this level.

CVX’s FY2014 – FY2023 ROIC (%) was 10.87, 2.39, -0.24, 4.96, 8.10, 1.95, -2.89, 9.32, 20.30, and 11.91.

CVX’s historical ROIC is not impressive but this metric has improved in recent years.

FY2024 Outlook

Q3 2024 will have heavier-than-usual maintenance with several turnarounds at upstream assets, including TCO and Gorgon. Impacts from refinery turnarounds are mostly driven by El Segundo.

There will be a onetime ~$0.6B payment related to discontinued operations.

Dividends payable to affiliates will be ~$1B in Q3.

Risk Assessment

Some investors fixate on an investment’s potential return and overlook the various risk aspects of the investment to their detriment. This is why I strongly encourage investors to read the ‘Risks’ section of a company’s Form 10-K.

While I try to assess a company’s risk, I also look at how the rating agencies perceive the company’s risk.

CVX’s current domestic long-term unsecured debt ratings and outlook are:

- Moody’s: Aa2 (stable) last reviewed November 14, 2023.

- S&P Global: AA- (stable) last reviewed September 18, 2023.

The rating assigned by Moody’s is the middle tier of the high-grade investment-grade category. It is one tier above the rating assigned by S&P Global.

Both ratings define CVX as having a very strong capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

Dividend and Dividend Yield

Dividend metrics are of little relevance in my investment decision making process. Nevertheless, these metrics matter to some investors. I, therefore, include a brief section on this topic.

CVX’s dividend history is accessible here.

The Board declared a quarterly dividend of $1.63/share, payable September 10, 2024, to all holders of common stock at the close of business on August 19, 2024.

This marks the 3rd consecutive quarterly dividend at this rate.

I think there is a reasonable probability CVX will increase the quarterly dividend to $1.66 when it declares its dividend in January 2025. If this materializes, investors can expect the next 4 dividends to total $6.58 ((2 x $1.63) + (2 x $1.66)). Using this and the current ~$148.55 closing share price on August 2, the forward dividend yield is ~4.4%.

CVX’s diluted weighted average shares outstanding in FY2011 – FY2023 (in millions) is 2,001, 1,965, 1,932, 1,884, 1,875, 1,873, 1,898, 1,914, 1,895, 1,870, 1,920, and 1,940, and 1,880.

On January 25, 2023, CVX announced that its Board authorized a new $75B share repurchase program (the ‘2023 Program’) with no fixed expiration that took effect on April 1; the previous authorization was $25B. The plan is to steadily repurchase shares across commodity cycles. With a breakeven Brent price of around $50/barrel to cover CAPEX and the dividend and with excess balance sheet capacity, CVX is positioned to return more cash to shareholders in any reasonable oil price scenario. Rather than the Board having to revisit the share repurchase authorization every few years, the repurchase authorization has been set where this matter does not need to be revisited as frequently.

In Q2 and YTD2024, CVX repurchased $3B and $6B of its shares lowering the weighted average to 1,833 in Q2 2024.

CVX is targeting share repurchases of ~$17.5B in FY2024 meaning it expects to repurchase another ~$11.5B.

Assuming the weighted average share price of all shares repurchased in FY2024 is ~$150 and CVX repurchases ~$17.5B shares, it will end up repurchasing ~116,666,667 shares in the year.

The weighted average shares outstanding for the 3 months ending December 31, 2023 was 1,868 million. Deduct ~116.7 million shares from the outstanding number of shares in the last quarter of FY2023 and CVX should have ~1,751 million shares outstanding at FYE2024. Average 1,868 million and 1,751 million and we get ~1,810 million shares as the weighted average shares outstanding in FY2024.

Valuation

CVX’s FY2011 – FY2023 PE levels are 7.88, 8.12, 10.22, 10.33, 19.51, N/A, 36.50, 14.64, 17.29, N/A, 22.65, 10.21, and 11.07. The years in which PE levels are N/A are when CVX reported a loss.

At the time of my November 6, 2023 post, shares traded at ~$147.60. CVX’s forward-adjusted diluted PE levels using available broker estimates were:

- FY2023: ~11 using a mean of $13.51 and a low/high range of $12.82 – $14.33 from 16 brokers.

- FY2024: ~9.9 using a mean of $14.88 and a low/high range of $11.52 – $20.75 from 14 brokers.

- FY2025: ~9.6 using a mean of $15.36 and a low/high range of $12.07 – $20.51 from 10 brokers.

Now, CVX’s forward-adjusted diluted PE levels using a ~$148.55 share price and the current broker estimates are:

- FY2024: ~12.06 using a mean of $12.32 and a low/high range of $10.91 – 14.00 from 23 brokers.

- FY2025: ~10.6 using a mean of $14.02 and a low/high range of $8.80 – $17.20 from 23 brokers.

- FY2026: ~10.2 using a mean of $14.63 and a low/high range of $10.11 – $17.98 from 16 brokers.

CVX has generated YTD diluted EPS and adjusted diluted EPS of $5.40 and $5.48, respectively. I think the high end of the broker estimates for FY2024 is optimistic and am opting to use an adjusted diluted EPS value of ~$12. On this basis and using the current ~$148.55 share price, the forward adjusted diluted PE is ~12.4.

Using the FY2024 CAPEX guidance of ~$15.5 – ~$16.5B and asset sales of ~$1B – ~$2B, I envision FY2024 net CAPEX being ~$15B. YTD FCF is ~$5.2B but I think CVX will be able to generate at least ~$11B of FCF in FY2024.

Based on my calculations in the Share Repurchases section of this post (see above), the weighted average diluted shares outstanding for the year may be ~1,810 million. Using this to forecast CVX’s FY2024 FCF/share, I get ~$6.08 (~$11B/1.810B shares). With shares currently trading at ~$148.55, the estimated forward P/FCF is ~24.4. This level is high but we need to consider that CVX:

- is experiencing heavier-than-usual maintenance which is impacting FCF; and

- continues to target $17.5B in annual share repurchases despite its headwinds.

Final Thoughts

Following various changes made for tax planning purposes, I now hold 684 shares in one ‘Core’ account, 1,376 shares in a second ‘Core’ account, and 337 shares in a third ‘Core’ account in the FFJ Portfolio for a total of 2,397 shares.

CVX was my 3rd largest holding when I completed my 2023 Year End FFJ Portfolio Review and my 2nd largest holding when I completed my 2024 Mid Year FFJ Portfolio Review. When I completed the 2023 YE and 2024 Mid Year reviews, CVX’s share price was ~$149 and ~$156, respectively.

Some investors may wonder if there is a long-term future for oil and gas companies. In my August 17, 2022 post, I touch upon why I think the demise of oil and gas is overblown. Since CVX is very likely to prosper well beyond my lifespan, I choose to have exposure.

Given the risk of CVX being unable to complete the Hess acquisition, investor sentiment is negative; the time to invest in great companies is when they experience temporary headwinds and negative investor sentiment.

For example, CVX’s results and share price were decimated during COVID so I made the following purchases:

- 18 shares on July 22, 2020 @ ~$85.4377 in one of the ‘Core’ accounts in the FFJ Portfolio;

- 50 shares on January 12, 2021 @ ~$93.1491 in one of the ‘Core’ accounts in the FFJ Portfolio; and

- 100 shares on July 22, 2021 @ ~$98.9072 in one of the ‘Core’ accounts in the FFJ Portfolio;

I was acquiring shares in other companies which limited how much I could invest in CVX.

A young investor I am helping on the journey to financial freedom also acquired shares, at my suggestion, on September 16, 2021 @ $97.0996.

Despite CVX’s attractive valuation, I do not intend to purchase additional shares. I will, however, continue to increase my exposure through the automatic reinvestment of the quarterly dividend income.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CVX and XOM.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.