Summary

Summary

- BIP adheres to BAM’s 5 core principles and employs a capital recycling program in which it rotates its investment from mature assets with lower IRR potential to new opportunities in which it can generate superior returns.

- BIP’s capital allocation model has three priorities of which the 3rd is to distribute ~60 – 65% of every dollar of FFO to unitholders.

- I view BIP as an attractive long-term investment suitable for investors seeking a safe and steadily increasing stream of quarterly distributions.

- I have just acquired several hundred BIP units for the FFJ Portfolio.

Introduction

As a long time shareholder of Brookfield Asset Management (TSX: BAM-a) (NYSE: BAM), I continue to be impressed with the entire group of companies. It is only recently, however, that I have decided to increase my relatively insignificant exposure to the Limited Partnerships to slightly more meaningful levels.

If your primary objective is to generate long-term capital gains then investing in BAM might be the preferred investment. Should dividend income be of greater importance to you than the potential for capital gains then investing in the higher dividend yielding Limited Partnerships might be your preferred choice.

Another advantage to investing directly in the Limited Partnerships is that you can target your investment to specific sectors. You may, for example, wish to have exposure to the infrastructure space but not the real estate space.

On October 3rd I uploaded a post on Brookfield Property Partners L. P. (TSX: BPY-UN.TO) (NASDAQ: BPY).

After listening to the Brookfield Infrastructure Partners L.P. (TSX: BIP-UN.TO) (NYSE: BIP) component of the September 26th Investor Day presentation and conducting my analysis on this entity, I now provide a brief overview of BIP.

Overview

BIP’s Investor Fact Sheet can be accessed here.

BIP is very much like BPY in that it adheres to BAM’s 5 core principles:

- Acquire high quality assets;

- Invest on a value basis;

- Enhance value through operations;

- Contrarian investing;

- Large-scale and multifaceted.

It is imperative that investors in any one of the BAM companies realize that the manner in which the businesses operate entails the use of a capital recycling program. When an asset is acquired, the intent is not to hold the asset in perpetuity. The capital recycling program instills capital discipline to ensure that businesses are sold when returns are maximized and not when cash is needed.

BAM and its LPs look for assets in which it can use its expertise to enhance the value of the acquired business. Unlike some members of its small peer group and institutional investors, the BAM entities have the expertise to acquire businesses in need of an overhaul and to make enhancements to increase the value of the acquired assets. Once the asset reaches the stage where it is almost ‘bond like’ the objective is to sell the asset and to redeploy the net sale proceeds into other assets where there are opportunities to generate superior returns.

BIP’s track record over the past decade demonstrates how well this strategy has panned out. It:

- has generated ~$3.3B from asset sales;

- has sold 10 businesses;

- the average holding period has been ~8 years;

- has generated a ~25% IRR.

By employing the use of a capital recycling program, BIP has been able to sell assets that are generating 6 – 10% IRRs (internal rate of return) and to redeploy the proceeds into new businesses that have the potential to generate 12 – 15%+ IRRs. In essence, it continually recycles capital from stabilized assets at or near peak values into higher-yielding strategies.

Investors have in the past expressed the following concerns about BIP’s capital recycling strategy.

The sale of assets can be lengthy and there is an element of uncertainty;

There may be a perception that BIP’s risk profile has changed when businesses are sold;

The need to redeploy capital may result in periods of excess liquidity (ie. cash may be raised from the sale of a business but the reallocation of these funds could take quite some time before BIP is able to redeploy these funds in other attractive investment opportunities).

BIP is well aware of these concerns and has endeavored to dispel them.

- BIP has ample access to capital. It has a $2B line of credit and also has the ability to issue preferred shares, debt, or equity.

- The sale of some businesses should not change BIP’s overall risk profile. BIP has several businesses that are at various stages within the ‘acquisition to sale’ lifecycle. Secondly, it is unlikely that any individual sale represents more than +/-5% of FFO.

- As far as having excess capital sitting around for a prolonged period of time which generates marginal returns, BIP has indicated they have seen no shortage of investment opportunities over the past 10+ years.

Source: BIP Investor Day Presentation – September 26 2018

Source: BIP Investor Day Presentation – September 26 2018

Asset Rotation Strategy Example

The following is an example of BIP’s asset rotation strategy.

The sale of BIP’s Chilean Transmission Business (Transelec) in March 2018 is a great example of a ‘full cycle’ investment.

In 2006, BIP led a consortium to acquire 100% of Transelec for $1.3B; BIP retained a 27.8% interest. At the time of this acquisition, Chile was viewed as an emerging market and capital was scarce. BIP, however, took a contrarian view.

Using its expertise, BIP grew Transelec’s rate base by ~$2B by increasing the number of kilometres of transmission lines from 8,000 to 10,000.

By 2017, BIP decided to exit this business because:

- The business had matured;

- Utilities and investments in Chile were being highly sought after.

Clearly, the following results demonstrate that the Transelec acquisition was highly rewarding for BIP unitholders.

Source: BIP Investor Day Presentation – September 26 2018

Source: BIP Investor Day Presentation – September 26 2018

Using these sale proceeds, BIP has invested/will be investing ~$1.8B into 6 new businesses.

One of the recently acquired businesses is a Colombian regulated utility. There are significant barriers to entry and this company has stable cashflows that are regulated and indexed to inflation. BIP has conducted business in Colombia in the past and is very familiar with that market environment.

Source: BIP Investor Day Presentation – September 26 2018

Source: BIP Investor Day Presentation – September 26 2018

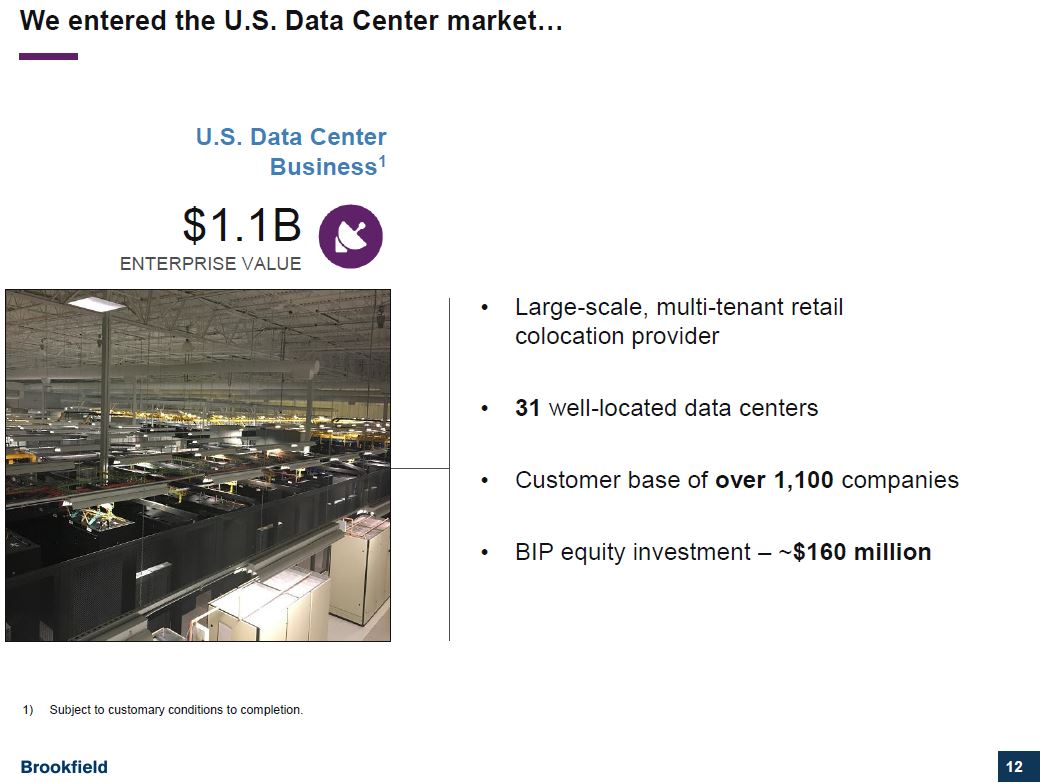

A second recently acquired business has enabled BIP to establish a presence in the Data Center business; this acquisition provides stable and recurring cashflows.

Roughly 85% of the revenue will be generated from the US and the customer base consists of high quality Fortune 500 companies and many government entities.

Source: BIP Investor Day Presentation – September 26 2018

Source: BIP Investor Day Presentation – September 26 2018

BIP has also entered into a joint venture with Digital Realty (NYSE: DLR) with the recent acquisition of Ascenty. This acquisition gives BIP access to markets in South America which are in the early stages of cloud computing. The cashflow from this business is predominantly in USD thus eliminating FX risk. BIP expects tremendous growth from this business.

Source: BIP Investor Day Presentation – September 26 2018

Source: BIP Investor Day Presentation – September 26 2018

Recent Major Acquisitions

BIP’s largest investments in 2018 have been in the energy sector.

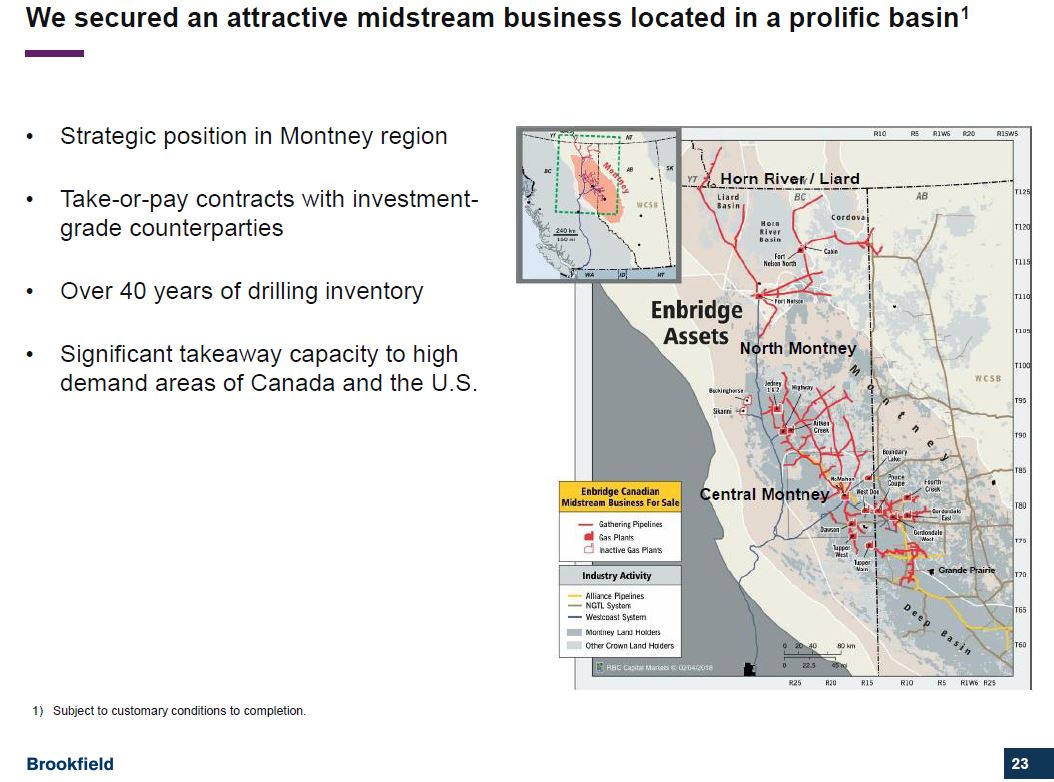

In early July, BIP and its institutional partners announced that they had entered into a definitive agreement to acquire 100% of Enbridge Inc.’s Western Canadian natural gas gathering and processing business for an enterprise value of C$4.31B (~ USD $3.3B) subject to customary closing adjustments; this transaction closed early October 2018.

This asset is well located in the prolific Montney gas basin in Canada. It comes with a strong contracted profile and is a unique and stable business.

Source: BIP Investor Day Presentation – September 26 2018

Source: BIP Investor Day Presentation – September 26 2018

In early August, BIP and its institutional partners announced that they had entered into an arrangement agreement pursuant to which all the issued and outstanding common shares of Enercare would be acquired. Enercare is the unregulated portion of a utility; this business was spun out of Consumers Gas about 20 year ago.

Enercare also has very attractive annuity like cashflows and is similar in this regard to BIP’s UK regulated businesses.

BIP likes this business because it feels it has a reliable business model which can be expanded in other BIP distribution companies in Colombia. It is also of the opinion that there are opportunities in which to leverage other Brookfield companies such as Brookfield Property Partners L. P. (TSX: BPY-UN.TO) (NASDAQ: BPY).

Source: BIP Investor Day Presentation – September 26 2018

Source: BIP Investor Day Presentation – September 26 2018

BIP is currently in advance discussions to enter the Indian energy market. Details are somewhat limited given the stage of the negotiations.

Source: BIP Investor Day Presentation – September 26 2018

Source: BIP Investor Day Presentation – September 26 2018

YTD Financial Performance

The current $3.00 FFO/Unit run-rate as of Q2 2018 is the result of ~8% organic growth but it is 4% lower than the prior year. This is due to the following:

- Foreign exchange –Appreciation of U.S. dollar;

- Timing issues –Redeployment of proceeds from asset sales;

- One-time events –Nation-wide truck driver strike in Brazil.

The outlook, however, is strong and $3.60 in FFO/unit is anticipated by year-end. This level is expected to be achieved as a result of:

- Contribution from newly-acquired businesses;

- Organic growth at mid range of LT target of 6 – 9%;

- Improved foreign exchange hedge rates.

Source: BIP Investor Day Presentation – September 26 2018

Source: BIP Investor Day Presentation – September 26 2018

Cashflows have become more diversified and substantially all of BIP’s FFO outside of South America and India has been hedged for the last 2 years. Recently, a decision has been made to hedge cash coming from Colombia, Peru, and Chile. BIP’s objective is to have 80-85% of FFO be either generated in, or hedged to, USD.

Capital Allocation Priorities

Out of every $1 of FFO, BIP allocates:

- ~20% to maintenance CAPEX obligations;

- ~15 – 20% reinvested in hundreds of smaller very low risk recurring projects that the business is able to predictably source year in and year out;

- ~60 – 65% distributed to unitholders.

Source: BIP Investor Day Presentation – September 26 2018

Source: BIP Investor Day Presentation – September 26 2018

In a nutshell….

- BIP generates significant free cash flow;

- Recurring organic growth is funded by operating cash flows;

- New investment activities and large scale expansions are funded from asset sales and capital market raises.

Distributions

While Adjusted Funds from Operations is a non-IFRS measure it is the measurement of financial performance the BAM group of companies most heavily relies upon. The rationale for using this metric (generally equal to funds from operations (FFO) with adjustments made for recurring capital expenditures used to maintain the quality of the underlying assets) is that it is considered to be a more accurate measure of residual cash flow for unitholders; BAM has specifically stated on multiple occasions that this metric is the closest proxy to cash flow generated from the business on an annual basis.

Source: BIP Investor Day Presentation – September 26 2018

The meaningful adjusted free cash flow from operations has allowed BIP to reward unitholders with steadily increasing distributions.

Source: BIP Investor Day Presentation – September 26 2018

The current USD $1.88 annual distribution is well covered by the current $3.00 FFO/Unit run-rate as of Q2 2018.

In my diversified portfolio I have shares with sub 1% yields and +4% yields; the average yield is ~2.5 – 3%. In the case of BIP, the current yield is ~4.7% ($1.88/$39.68).

Final Thoughts

I have been a long-time BAM shareholder and have closely followed how this group of companies has evolved over the years. In hindsight, I should have taken decent sized positions in the Limited Partnerships much sooner but I was happy to invest primarily in BAM with the prospect of achieving superior capital gains. Having looked at the operating entities more closely, I have come to the realization that holding sizable positions in BAM and the LPs is the appropriate route for me to follow.

I have absolutely no qualms with increasing exposure to the extent where the BAM entities on a consolidated basis are approaching my top 10 holdings.

The BAM executive team is extremely astute and there are very few companies in the world which have the expertise to do what BAM does. This would explain why BAM is able to attract wealthy and financially savvy investors.

As I have indicated in previous BAM related articles, I do not have the resources or skills to remotely come close to consistently generate the returns the BAM group of companies has been able to generate (or is expected to generate). I am, therefore, more than happy to ‘piggy back’ and if I slightly overpay for units in the various BAM entities, I am not overly concerned. I intend to hold these units for the long-term and I strongly suspect that well into the future, the units will be worth far in excess of current prices.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: Long BIP, BPY, and BAM.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.