In my August 14th Brookfield Asset Management (BAM) stock analysis I disclose the purchase of additional BAM shares through various accounts. I conclude that post stating:

‘I have no interest in investing in cryptocurrencies, SPACs, or complex derivative products. I do, however, want exposure to alternative assets thus my reason for investing in BAM.’

Having said this, my plan has been to also have exposure to another leading asset manager.

After reviewing several Blackstone (BX) 10-K and 10-Qs, listening to multiple interviews with Stephen Schwarzman (BX’s Chairman and CEO) and Jonathan Gray (BX’s President and COO), reading Schwarzman’s autobiography (What It Takes – Lessons in the Pursuit of Excellence) and King of Capital – The Remarkable Rise, Fall, and Rise Again of Steve Schwarzman and Blackstone by David Carey and John E. Morris, I initiated a position on August 19 @ ~$110/share within one of the ‘Core’ accounts in the FFJ Portfolio; I now hold 500 BX shares and will reflect same in my FFJ Portfolio – August 2021 Report.

While BX does invest client money through SPACs, not all SPACs are created equal. A BX related SPAC is a far cry from some of the garbage SPACs that have a remote, if any, probability of ever generating a profit.

Depending on the terms of the SPAC, BX can generate income through various means. The same can not be said from acquiring shares in a SPAC.

We also have to consider that BX has ‘only’ $120B of its $684B in Assets Under Management (AUM); these assets are within BX’s Corporate Private Equity line of business. BX generates income from other lines of business so BX investors are not totally dependent on whether these SPACs are successful or not.

Blackstone – Stock Analysis – History

In the Fall 1985, Schwarzman and Pete Perterson each invested $200,000 of their own personal capital and founded BX. The books I mention above go into detail on their respective backgrounds and the challenges they faced when starting BX.

BX’s partnership structure since inception limited the market for its shares. Management recognized this and on July 1, 2019, it was converted from a publicly traded partnership to a corporation. More details on this conversion is accessible in a video, presentation, and a series of FAQs.

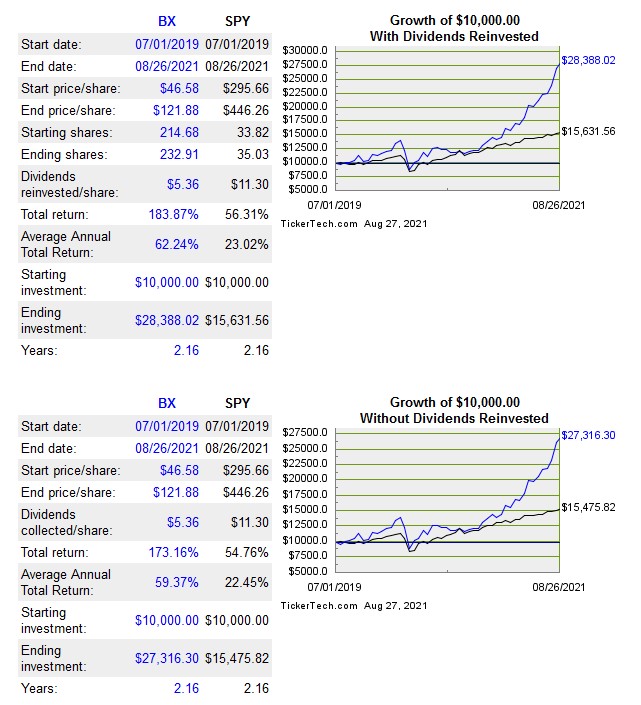

Although BX was highly successful as a publicly traded partnership, the true underlying value of the company has been unleashed following this conversion. This is borne out in BX’s share price far outperforming the S&P 500 in the ~2 years following this conversion.

I can not possibly cover the firm’s entire history but suffice it to say, BX has been remarkably successful for much longer than a couple of years!

How successful? Well…as of the time I compose this post on August 27, 2021…

- BX has in excess of $684B of AUM as at the end of Q2 2021. By comparison, BAM’s website reflects $625B in AUM.

- Schwartzman’s net worth is estimated to be in excess of $36B; he is ranked #79 on Forbes’ 2021 list of billionaires.

- Pete Peterson passed away in in March 2018 at the age of 91. At his time of passing, his net worth was estimated to be ~$2B.

- Jonathan Gray, named BX’s President and COO in February 2018 and considered a potential successor to Steve Schwarzman, ranks #638 on Forbes’ 2021 list of billionaires with an estimated net worth of $7.1B.

It doesn’t take much to put 2 and 2 together to see that BX’s business is extremely lucrative and rewards patient and disciplined investors.

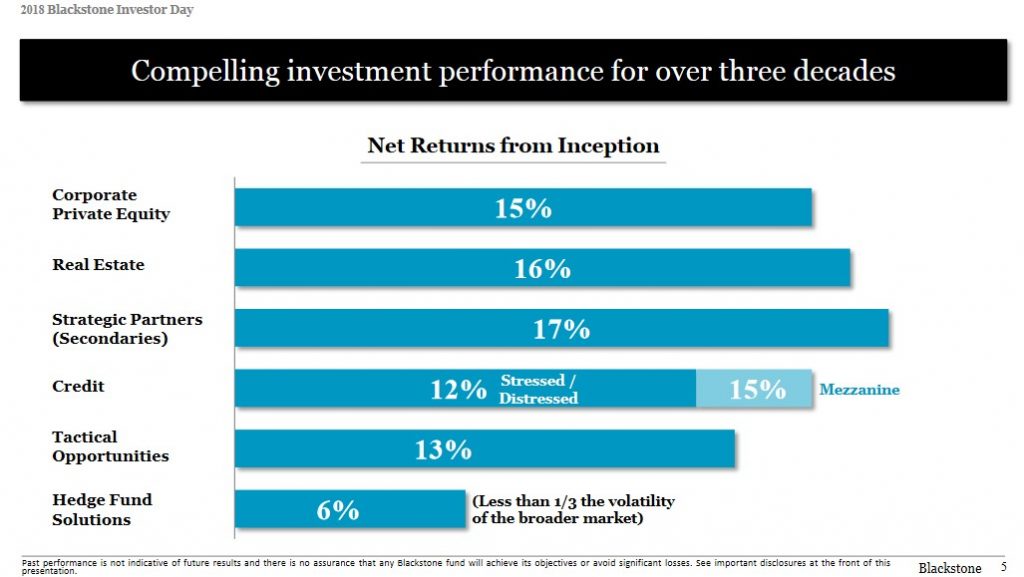

Furthermore, while past performance is not indicative of future performance, BX’s successful track record of over 3 decades gives us a degree of comfort that BX is not simply a ‘flash in the pan’.

Obviously, investment returns are not predictable. However, if BX can generate a conservative 12% net return then, using the Rule of 72, investors can estimate their investment to double in 6 years.

I will gladly accept this rate of return!

Blackstone – Stock Analysis – Industry Overview

The Asset Management industry is fragmented and highly competitive. A few other well-known publicly traded companies in this space are BlackRock (BLK), Brookfield (BAM), KKR & Co (KKR), Apollo (APO), and The Carlyle Group (CG). In addition, there are privately held competitors such as ThomaBravo; Intercontinental Exchange (ICE) – one of my holdings – acquired Ellie Mae from ThomaBravo for $11B.

While this is a highly competitive space, BX is arguably the leader. Its market cap is currently more than $142B and it has the wherewithal to complete transactions that many of its peers can not. By way of comparison, BAM’s market cap is currently ~$87B!

Blackstone – Stock Analysis – Business Overview

Unlike BAM, BX does not hold an Investor Day every year. BX last held an Investor Day on September 21, 2018 (click here for access to the presentation and webcast).

Much has changed since this presentation…in a good way. At the time of the presentation, BX had $439B in AUM versus the current $684B. Despite this $245B increase in AUM, BX has sold multiple investments resulting in highly attractive investment returns for its shareholders and sophisticated investors. This list of investors includes the world’s largest institutional investors such as endowments, sovereign wealth funds and pension funds that provide retirement benefits for over 31 million teachers, firefighters, nurses and others.

Although BX faces significant competition from asset managers with extremely bright individuals, BX is unique from many of its peers.

In addition to the above, BX is known as the place to work if you want to be in the asset management space. BX attracts and retains incredible talent having hired only 86 from 14,906 applicants in 2018. Academic standing is not the only consideration when it comes to hiring candidates. Strong people skills and the ability to work as part of a team are critical.

In Schwarzman’s autobiography ‘What It Takes’, he discusses his formative years with Donaldson, Lufkin & Jenrette (DLJ) and Lehman Brothers. Reading about his years with Lehman explains why it is no longer in existence!

Blackstone – Stock Analysis – Investments

The ‘Our Businesses‘ section of BX’s website has a menu of the areas of business in which BX invests. As noted earlier, BX has just under $120B in AUM in 98 portfolio companies and has $35B of capital to invest.

The June 30, 2021 Form 13-F reflects the companies in which BX has invested. We see from this list that many are SPACs. As much as some SPACs are ‘toxic’, we must be careful not to paint every SPAC with the same brush. Some SPACs will be very profitable.

In the case of BX’s SPAC investments, BX has a reputation to uphold. The reason BX is arguably the leader in its space is that it has demonstrated to its sophisticated clients and prospective clients that it knows how to generate attractive investment returns. If it starts investing in SPACs which do not have a hope of ever generating a positive investor return, BX will tarnish its reputation.

In Canada, there are asset managers which manage portfolios that include SPACs. These firms, however, are minuscule and are unable to compete at the same level as BX. Furthermore, I can not hold a direct stake in these asset managers since they are private entities.

If I am going to have exposure to SPACs, I want ways to make money even if the SPACs are not highly successful. In the case of BX, it structures deals so it generates a combination of:

- management fees;

- incentive fees;

- carried interest (performance allocations); and

- advisory and transaction fees

It also has a reputation at the upper echelons throughout the world that it must uphold. Its sheer size also allows it to do deals that are far too large for many other asset managers.

Do you want to invest in this…..

or a much smaller asset manager that can not compete in the same space as BX?

Another key consideration is risk mitigation. This is an important component of BX’s investment philosophy!

The same can not be said about many other companies in the asset management space.

Blackstone – Stock Analysis – Recent Transactions

BX is continually active. Press Releases about recent investment activity are accessible here.

Strategic Partnership with AIG

Much like BAM, BX is also expanding into the insurance business. It recently announced its expansion into the retail and insurance channels via the impending acquisition of a 9.9% equity stake in AIG’s Life & Retirement business for $2.2B in an all-cash transaction. As part of this agreement, AIG also agreed to enter into a long-term strategic asset management relationship with BX to manage an initial $50B of AIG’s Life & Retirement existing investment portfolio upon closing of the equity investment. This amount is to increase to $92.5B over the next 6 years.

Included in this announcement is a definitive agreement for Blackstone Real Estate Income Trust (BREIT), a long-term, perpetual capital vehicle affiliated with BX to acquire AIG’s interests in a U.S. affordable housing portfolio for approximately $5.1B; this is also an all-cash transaction and closing is expected in Q4 2021.

The retail and insurance channels have approximately $110T in assets globally – nearly double the size of the institutional channel in which BX has exclusively focused.

BX has identified these two channels as being dramatically underpenetrated in their allocations to alternative investments. While BX has invested significantly over the last decade to build out its distribution capabilities in these channels, it has incurred significant costs but has not generated commensurate revenue. This should change as it expands its product lineup, including moving into lower-risk return areas like core-plus real estate and private credit.

In retail, an $80T addressable market, BX’s long-term strategy was to develop the highest-quality support organization for retail customers and to service the largest private wealth distribution systems globally. BX is now establishing a leading platform in the asset management industry with a menu of products that include BX’s non-traded REIT, BREIT, and its new BDC, BCRED.

On the Q2 call with analysts, management indicated the response from individual investors for Blackstone-managed private real estate and

credit has been excellent. In this regard, BX is raising nearly $4B/month for BREIT and BCRED.

The demand for these products is expected to continue to grow and management believes this powerful distribution channel is ideal for other products under development. In fact, BX is currently launching a new vehicle in Europe that is similar to BREIT. Sales are expected to start in September and additional products are in the planning and development stage.

On the insurance front, BX will become the exclusive external manager of a significant portion of AIG’s life and retirement portfolio. This will rank BX as the 3rd largest US public life insurer. This partnership accelerates BX’s growth in the $30T global insurance market, with BX becoming one of the two largest alternative managers in this space.

Blackstone – Stock Analysis – Financials

Q2 2021 and YTD Results

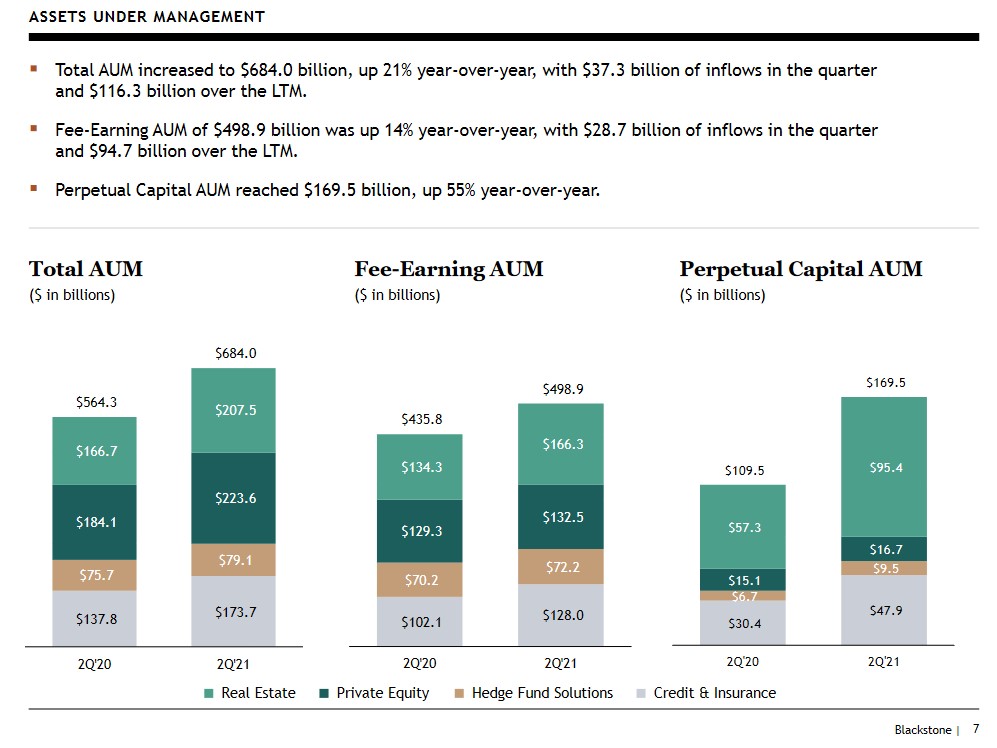

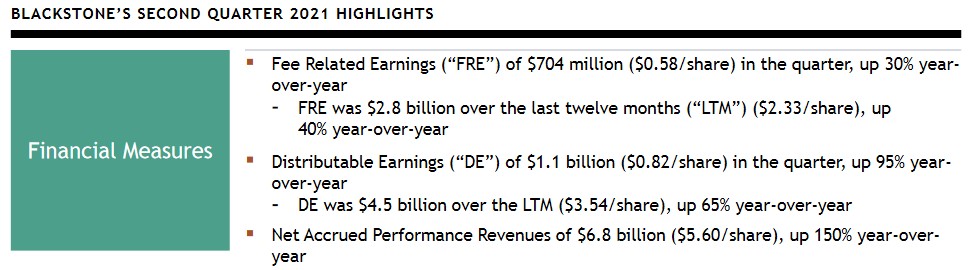

On July 22, BX released Q2 2021 and YTD results in which it reported distributable earnings (DE) that nearly doubled year-over-year to $1.1B, while fee-related earnings (FRE) increased 30% to over $0.7B. Both DE and FRE for the last 12 months reached record levels. In fact, BX’s investment performance represented the best quarter and 12-month period of fund appreciation in the firm’s 35.5-year history. Furthermore, AUM grew 21% year-over-year to $684B which is another record.

In Q2, total inflows were $37B and $116B over the past 12 months. Perpetual AUM increased 55% year-over-year to nearly $170B. Growth in perpetual capital is like planting perennials, which have a recurring and compounding contribution to BX’s financials, and meaningfully accelerates growth in fee-related earnings.

The largest single-engine of perpetual capital and fee-related earnings is the real estate Core+ business. AUM has grown to $85B across 5 vehicles. The largest of these, BREIT, raised ~$6B in Q2 and an additional $2.6B of monthly subscriptions after quarter end on July 1, bringing it to $34B in total size. BX will also be launching a 6th Core+ vehicle, BEPIF, which like BREIT will target high-quality, income-producing assets on behalf of retail investors; the focus will be on European real estate.

A host of other activities contributed to BX’s strong Q2 results. Additional information is found in the Q2 Earnings Presentation and the Supplemental Financial Data.

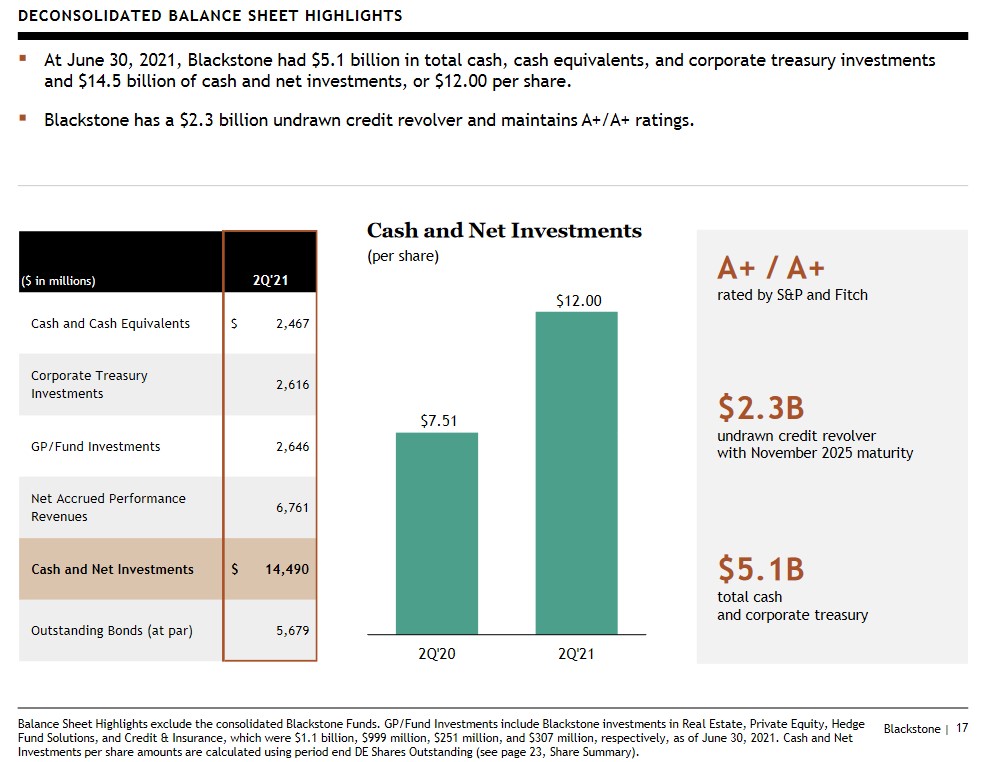

Blackrock – Stock Analysis – Credit Ratings

One might expect BX to have significant long-term debt. This, however, is not the case. Schwarzman learned from his experiences that risk must be tightly controlled. Failure to properly control risk leads to the likes of Lehman and Bear Stearns. Here today…gone tomorrow.

Looking at page 7 of 189 in BX’s Q2 10-Q, we see ‘Loans Payable’ of $5.6B and ~$2.5B of ‘Cash on Hand’. Net the two and you get ~$3B. Not bad for a company that has ~$684B in AUM.

Note 12 – Borrowings in the Q2 10-Q reflects a schedule of Senior Notes Payable. The interest rates are very attractive and the amount repayable in any given year is extremely manageable.

The senior unsecured domestic long-term debt ratings assigned by the major rating agencies are:

- S&P Global assigns an A+ long-term unsecured debt credit rating with a stable outlook; and

- Fitch assigns an A+ long-term unsecured debt credit rating with a stable outlook;

S&P Global’s and Fitch’s ratings are the top tier in the upper-medium-grade investment-grade tier. Surprisingly, I am unable to locate ratings assigned to BX by Moody’s and I see from page 21 of 41 in the Q2 2021 Earnings Presentation that no mention is made of a rating by Moody’s.

S&P Global and Fitch define BX as having a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

The deconsolidated Balance Sheet highlights reassure me that my BX investment is within my risk tolerance.

Blackrock – Stock Analysis – Dividends and Share Repurchases

Dividend and Dividend Yield

BX distributes a quarterly dividend. Using the last 4 quarterly dividend payments totalling $3.02, we arrive at a ~2.4% dividend yield based on the current ~$124.24 share price.

Investors who limit their investments to companies with a track record of dividends that increase annually, however, may shy away from an investment in BX. This is because BX’s quarterly dividend fluctuates.

BX’s dividend is dependent upon DE. Management states that DE is meaningful as it increases comparability between periods and more accurately reflects earnings that are available for distribution to shareholders.

Given this, BX’s dividend policy is based on this metric:

‘Our intention is to pay to holders of common stock a quarterly dividend representing approximately 85% of The Blackstone Group Inc.’s share of Distributable Earnings, subject to adjustment by amounts determined by our board of directors to be necessary or appropriate to provide for the conduct of our business, to make appropriate investments in our business and funds, to comply with applicable law, any of our debt instruments or other agreements, or to provide for future cash requirements such as tax-related payments, clawback obligations and dividends to shareholders for any ensuing quarter. The dividend amount could also be adjusted upward in any one quarter.’

Page 124 of 366 in BX’s FY2020 10-K reflects a reconciliation of Net Income Attributable to The Blackstone Group Inc. to Distributable Earnings, Total Segment Distributable Earnings, Fee-Related Earnings and Adjusted EBITDA. A similar table is on page 117 of 189 in the Q2 2021 10-Q.

NOTE: DE is a pre-tax non-GAAP financial measurement. It differs from Economic Net Income because it only includes the cash-generating portion of the performance and investment-related revenues and compensation expenses. Investors use DE as a proxy for cash earnings. However, DE includes some non-cash expenses – equity compensation from annual employee grants as well as depreciation.

Personally, BX’s dividend is not a factor in my decision to invest in the company. I am investing in BX from a total return perspective and envision long-term capital gains will form the bulk of my investment return.

Share Repurchases

On July 16, 2019, BX’s board of directors authorized the repurchase of up to $1.0B of Class A common stock and Blackstone Holdings Partnership Units. The repurchase program may be changed, suspended or discontinued at any time and does not have a specified expiration date.

- During FY2018, BX repurchased 16.0 million shares of Blackstone Class A common stock at a total cost of $0.5415B.

- In FY2019, BX repurchased 12.8 million shares of Blackstone Class A common stock at a total cost of $0.5619B.

- During FY2020, BX repurchased 9.0 million shares of Blackstone Class A common stock at a total cost of $0.474B.

- In Q1 2021, BX reported the repurchase of 4.0 million common shares over the last 12 months.

- In Q2 2021, BX repurchased 3.2 million common shares and it has repurchased 5.2 million common shares over the last 12 months; the available authorization remaining was $0.758B at June 30, 2021.

While the Diluted Weighted-Average Shares of Common Stock Outstanding was ~1.207B in FY2018, 676.2B in FY2019, 697.3B in FY2020, and increased to 715.6B in Q2 2021, I have no qualms about the increase in the number of outstanding shares as long as the underlying value of each share appreciates over the long term.

Blackrock – Stock Analysis – Valuation

As with BAM, some portfolio managers shy away from BX because it is not easy to value; BX is continually making sizable investment transactions so earnings estimates can quickly become outdated.

BX is much like BAM in that it raises pools of funds from clients in the tens of billions of dollars. It then deploys these funds thus resulting in multiple billion-dollar acquisitions annually; the size of these acquisitions has grown significantly over the years.

BX uses its expertise to improve the performance of the companies in which it invests with the intent of monetizing these assets as part of its capital recycling programs. It is not, therefore, unusual to see wide swings in YoY GAAP results.

While diluted EPS and adjusted diluted EPS is a metric I typically use to value most of the companies I analyze, these metrics are not appropriate for BX; BX uses the following 2 key metrics to more accurately measure its performance.

- Distributable Earnings (DE)

- Fee Related Earnings (FRE)

A definition of these terms and other terms are found at the end of the Q2 2021 Earnings Presentation and within the FY2020 10-K.

I do not try to estimate the following year’s DE and FRE nor does BX provide guidance.

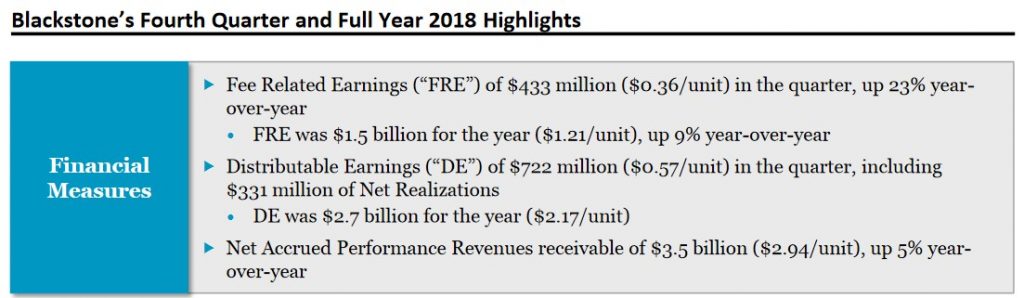

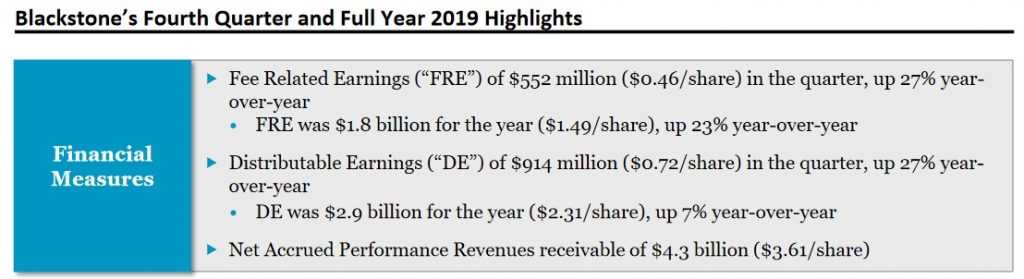

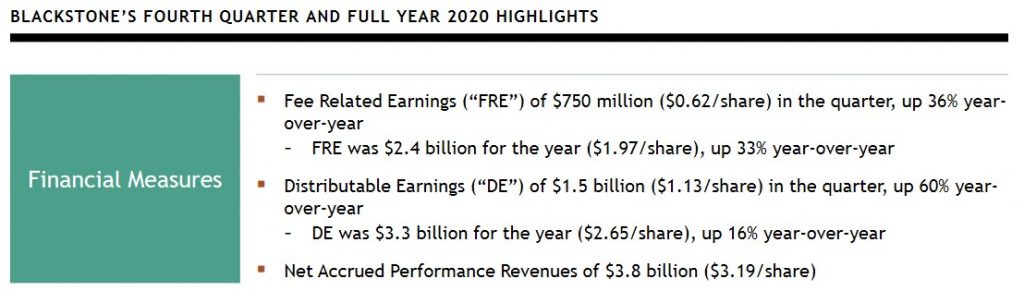

Looking at DE and FRE results extracted from the Q4 and FYE 2017 – FY2020 and Q2 2021 Earnings Presentations, however, we can see that BX generates impressive results.

Blackrock – Stock Analysis – Final Thoughts

I am a staunch believer in investing in high-quality companies for the long term. Investing in BX with this in mind is doubly important because BX’s investments typically do not generate peak results until several years into the future. The Strategic Partnership with AIG section of this post (see above) is an example of BX investing in an opportunity for a decade without anything to show for its investment up to the present. Now, however, this investment is highly likely to generate very significant returns.

Although BX’s share price has increased slightly after my purchase, I envision BX’s share price appreciating significantly over the next decade or two. I, therefore, intend to continue to acquire shares; I also intend to continue to acquire BAM shares.

My reasoning for investing in these two companies is that I want exposure to alternative assets. I, however, do not have the resources to identify what are good and terrible alternative assets. By investing in BX and BAM, I benefit from their expertise and minimize my risk.

As far as the unreliability of the value of the quarterly dividend, this is a non-issue for me. I am investing for the capital gains potential and not for the dividend income.

Stay safe. Stay focused.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BX and BAM.

Disclaimer: I do not know your individual circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.