Summary

Summary

- This Bank of New York Mellon (NYSE: BK) stock analysis is based on Q4 and FY2016 results reported on January 19, 2017.

- BK does not have a record of steadily increasing its dividends annually.

- The number of shares outstanding as at FYE2016 exceeded that as at FYE2007!

- Shares are currently overpriced. I would not consider acquiring additional shares unless they retraced to a level closer to $41.52.

Introduction

In 2011, I acquired several hundred The Bank of New York Mellon Corporation (NYSE: BK) shares at an average cost of $20.4554; these shares are held in my wife’s Registered Retirement Savings Plan (RRSP) as opposed to the FFJ Portfolio. By holding US listed shares in an RRSP we avoid the 15% withholding tax Canadians incur on US dividend income. In addition, all quarterly dividends are automatically reinvested.

While I would like to say that I was an extremely astute investor when I acquired these shares, nothing could be further from the truth. When I decided to invest in BK, this is what I saw:

- BK maintained leading and broad-based positions in Investment Services and Investment Management.

- The client base was comprised of financial market leaders – buy side, sell side, governments and market infrastructure providers. It included more than three-quarters of all Fortune 500 companies, central banks that hold more than 80% of all reserves and 85% of the top 100 pension and employee benefit funds.

- Most of BK’s clients utilized many of its major business lines which enabled it to generate multiple streams of income from the same customer.

- Growth of assets under custody and administration of approximately $25.8T outpaced its closest trust and custody peers.

- Average active clearing accounts, average collateral management balances, and average total Investment Services deposits were all on pace to experience double digit % growth.

- Assets under management (AUM) were on target to grow 8% to over $1.25T (this figure is now in excess of $1.6T).

Perhaps the best thing I noticed was that BK’s stock was getting hammered. Times really were not good for BK and shortly after I acquired shares, Robert Kelly (then CEO of BK) was axed.

In essence, 2011 was a difficult year for BK. In fact, “2011 was a difficult year” are the exact words BK’s new Chairman, President and Chief Executive Officer used to start his “Dear Fellow Shareholders” letter in BK’s 2011 Annual Report!

Times like late 2011 are exactly what investors want when seeking possible long-term investment opportunities. Such is not the case at the moment, and therefore, I do not view BK as an attractive investment opportunity.

Business Overview

BK is a global investments company which services and manages much of the world’s financial assets. It has a comprehensive array of investment management strategies for virtually every risk profile, strategy and asset class. In addition, it has a broad set of capabilities and advanced technology platforms which enable speed to market and also drive innovative, cost-effective solutions and growth opportunities. These have all enabled BK to become the seventh largest investment manager in the world.

BK operates businesses through two segments: Investment Management and Investment Services. And also has an “Other” segment, which includes credit-related services; the leasing portfolio; corporate treasury activities, including its investment securities portfolio, its equity interest in ConvergEx Group, business exits, and corporate overhead.

FY2016 Financial Results vs. 3 Year Goals set in 2014

BK 2016 results can be found in this Press Release and in the following recap extracted from BK’s January 19, 2017 Earnings release.

BK Q4 and FY2016 Financial Highlights – Jan 19 2017 Press Release

BK improved upon 2015 results in the key metrics reflected in the following diagrams and is trending well relative to the Goals set out in 2014 with the exception of Adjusted Revenue growth where it is falling short. NOTE: these 3 year goals were based on a flat rate environment and in a normalized rate environment.

BK Investor Day Goals and Progress Toward Goals

BK 2016 vs. 2015 Key Results

BK is currently in the process of establishing new goals which will be communicated to shareholders later this year.

Valuation

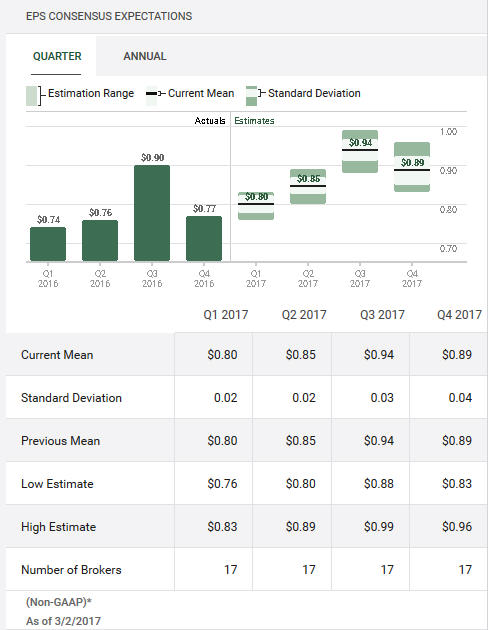

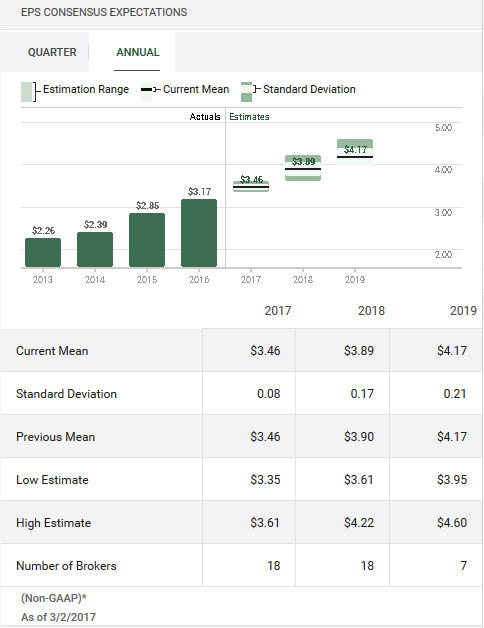

As I compose this post, BK is trading at $47.90. FY2016 adjusted EPS was $3.17 resulting in a current PE of 15.11. If I use the $3.46 Mean 2017 EPS estimate from 25 brokers and a market price of $47.90, I get a forward PE of 13.84.

Source: TD WebBroker – BK quarterly EPS estimate

Source: TD WebBroker – BK annual EPS estimate

Source: ValuEngine – BK quarterly EPS estimate

Source: ValuEngine – BK annual EPS estimate

This seems a bit rich for my liking considering BK:

- is not high growth;

- has a less than stellar dividend history;

- the dividend yield is a paltry ~1.6%;

- the outstanding shares have not declined to an extent I would consider acceptable to offset its dividend track record. In fact, the number of shares outstanding as at FYE2016 exceeded the number of shares outstanding as at FYE2007!

As an investor I look for two things from an equity investment. I look for growth in the underlying value of the shares owned and a consistent increase in dividends.

BK’s shares have certainly increased in value relative to our average cost of $20.4554. BK has not, however, satisfied my requirement on the dividend front. I have relaxed this requirement given that it has repurchased a significant number of shares subsequent to our 2011 acquisition date and BK’s performance has evidenced improvement is the past few years.

In FY2016, BK returned $3.2B to shareholders. $2.4B consisted of share repurchases and $0.778B represented common stock dividends. While there is certainly room to increase the dividend payout ratio beyond FY2016’s sub 25% level, I suspect the focus will be on reducing the number of shares outstanding to at least the FYE2007 level before any significant dividend increase is entertained.

Given the above, I would be reluctant to acquire any additional BK shares unless the PE ratio was to drop to 12. Using the $3.46 Mean 2017 EPS estimate previously noted and this PE ratio, I would not be prepared to pay more than ~$41.52/share. This means BK’s stock price would need to drop just over 13% from the current level before I would even consider acquiring more shares.

I recognize some readers may be of the opinion that I might be waiting a long time before BK’s stock price reaches this level. If such is the case, then so be it. BK’s historical performance is such that I am not prepared to chase BK.

Option Strategy

If you currently own BK shares like me, you may wish to consider generating additional income through the use of a relatively plain vanilla option strategy. You could write a covered call with an out-of-the-money strike price.

Let’s say you wrote 9 covered call contracts with a $50 strike price and a September 15, 2017 expiry. You would generate a premium of about $1,620 less commission (each contract represents 100 shares so 900 X $1.80).

Source: Scotiabank – BK Covered Call Option Strategy

You would keep your shares and the option premium if BK stays below $50 between now and September 15, 2017.

Should BK rise above this level, you could get called away. This means you would receive $50/share and you would retain your option premium. You would, however, no longer own the shares.

If you thought you were going to get called away because BK’s stock price exceeded $50 and you really did not want to part with your BK shares, you could close your option contracts at whatever the going rate is at the time; you could end up paying more than you received when you first wrote the contract. You could then write new contracts further out into the future at a higher strike price. The premiums you receive for these new contracts could cover whatever money you laid out to close out your first set of contracts.

NOTE: As the owner of BK shares, you receive the dividends during the period in which your option contracts are open.

Bank of New York Mellon Stock Analysis – Final Thoughts

My rationale for acquiring BK shares in 2011 was because I had no intention of investing in a company which:

- was constantly in the news extolling the virtues of its new products/services which would supposedly revolutionize the world;

- traded at stratospheric earnings multiples;

- required an inordinate amount of my time to dissect the financial statements;

- could easily be displaced by a new competitor.

While we have certainly had a positive experience with BK given that it has appreciated 140% in value from our average cost, BK has not met my steady dividend growth requirement. I relaxed this condition because I felt BK was “on the ropes” during the Financial Crisis but it would be a “survivor” thus allowing us to benefit from the growth in price.

If you are not in our position of having invested in BK at depressed prices, however, be forewarned.

BK’s stock price has been in an upward trajectory since late 2011. While some of this increase can definitely be attributed to its success in meeting targets it set for itself in 2014, I suspect BK’s stock price has been caught in the updraft experienced by the stock market subsequent to the November 2016 US Presidential election (look at BK’s stock chart starting mid October 2016). I also suspect BK’s stock price has already baked in an impending increase in interest rates in the not too distant future; an increase in interest rates bodes well for BK because of the sizable deposits it holds for clients.

Go to the company’s website and plug in various dates into their “Total Return Calculator”. Buy at the wrong time and it could be years before you generate a reasonable return on your investment!

As previously noted, don’t expect BK’s dividend policy to ease your pain and sorrow if you overpay when acquiring your shares.

Clearly, an investment of any sort depends upon your unique circumstances. If you feel BK might fit your investor profile and would be a suitable holding within your overall portfolio, I suggest you sit tight and wait for its stock price to retrace to more favorable valuation levels.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I am long BK.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.