Following the November 20 market close, A released its Q4 and FY2023 results and Q1 and FY2024 guidance. Despite the challenging market conditions, Agilent forecasts strong cash flow in FY2024.

When I reviewed Agilent Technologies (A) in my August 16 post, it had just released its Q3 and YTD2023 results and revised FY2023 guidance. At the time of that review, my exposure consisted of 400 shares at an average cost of ~$122.35 in a ‘Core’ account within the FFJ Portfolio.

I followed up that August 16 post with this September 12 update in which I disclosed the purchase of an additional 100 shares @ ~$113.82 on September 11 thus lowering my average cost to $120.6631.

As I compose this post, A’s share price has rebounded to ~$124. I now revisit this holding to gauge A’s valuation.

Business Overview

I reference my August 16 post in which I provided a business overview.

CEO and NEO Compensation

Please refer to my May 10 post.

Financials

Q4 and FY2023 Results

Material related to A’s Q4 and FY2023 earnings release on November 20 is accessible here.

The following reflects A’s FY2023 results for the company as a whole. Results for each of the 3 business groups in Q4 are found in the Q4 Earnings Presentation.

A continues to experience global macroeconomic challenges and soft market conditions in China. However, A believes it is beginning to see signs of stabilization.

Q4 2023 revenue of $1.688B declined from $1.849B in Q4 2022. The high end of Q4 guidance provided with the release of Q3 results was $1.705B. Page 12 of 19 in A’s Financial Information Package reflects the adjustments used to arrive at Q4 adjusted diluted EPS of $1.38; this exceeded $1.36 which was the high end of guidance. The same page reflects the adjustments from $4.19 in GAAP EPS to $5.44 in non-GAAP EPS. A sizable line item is $0.94/share in asset impairments which I discussed in my August 16 post.

A’s full-year growth was lower than initially expected, however, it met or exceeded every quarterly guidance range provided. Including FY2023 results, A’s 4-year compound annual growth rate is 7%. This is at the high end of our long-term growth guidance.

A delivered operating margins of 27.4%, an increase of more than 400 bps in the last 4 years in FY2023. In addition, A’s 4-year EPS compound annual growth rate is 15%.

In FY2023, all markets grew low to mid-single digits for the year, except for pharma, which was down 2% globally. All geographies grew except China, which was down 5%.

Despite the revenue declines, A’s Q4 gross margin was 55.8% and its operating margin was 27.8% which was slightly better than management’s expectations.

During Q4, A distributed $66 million in dividends and repurchased $80 million of its outstanding shares. In FY2023, it allocated ~$0.84B of capital toward ~$0.265B in dividends and ~$0.575B in share repurchases.

Operating Cash Flow (OCF) and Free Cash Flow (FCF)

In FY2013 – FY2023, A generated OCF of (in millions of $): 1.152, 731, 512, 793, 889, 1.087, 1.021, 921, 1.485, 1.312, and 1.772

In FY2013 – FY2023, A generated FCF of (in millions of $): 957, 526, 414, 654, 713, 910, 865, 802, 1.297, 1.021, and 1.474. FCF increased ~44% from FY2022.

In Q4, A generated $0.516B of operating cash flow which was ~109% of $0.475B of net income. For FY2023, operating cash flow was ~143% of net income ($1.772B versus $1.240B).

Q1 and FY2024 Guidance

A anticipates a slow but steady recovery in FY2024 and remains convinced that the challenging market conditions the industry faces are transient. The rationale for this outlook is that A’s end markets are powered by investments in improving the human condition. Further growth is expected to be fueled as the pace of science, innovation and discovery continues to increase.

From a geographic perspective, expectations are for modest growth in the Americas and Europe. Although A expects to see a recovery during the year in China, the initial view is it will still decline for the full year.

From a business group perspective, we expect growth in both the Diagnostics and Genomics Group and the Agilent CrossLab Group while the Life Sciences and Applied Markets Group will still be pressured.

The first half of FY2024 will likely be similar to the second half of FY2023 with growth in the second half of FY2024.

Source: A – Q4 2023 Earnings Presentation – November 20, 2023

Given the continued market uncertainty, high interest rates, volatile exchange rates, and depressed capital spending, A has taken additional steps to adjust its cost structure. Incorporated into its guidance is ~$0.175B of cost savings.

Roughly 30% of the savings is related to portfolio optimization decisions within the Diagnostics and Genomics Group – the exit of the Resolution Biosciences business I touched upon in my August 16 post.

Another 25% of the savings is material and logistics cost savings and the optimization of its real estate footprint. The remaining savings are tied to continued reductions in discretionary spending and optimizing the workforce. Along with these actions, A has taken a $46 million charge for restructuring and other related costs in its Q4 2023 GAAP results.

Credit Ratings

A has reduced its net debt to adjusted EBITDA ratio to 0.6 from 0.9 as of January 31, 2022.

A does not have debt maturities until April 15, 2025 at which time a $0.6B Term loan matures.

A’s FY2023 Form 10-K is unavailable as I compose this post. The liabilities at the end of Q2 and Q3, however, are relatively similar. I, therefore, reference A’s Q3 2023 Form 10-Q in which we see the maturity dates of A’s Senior Notes (commences on page 26).

Source: A – Q3 2023 Form 10Q

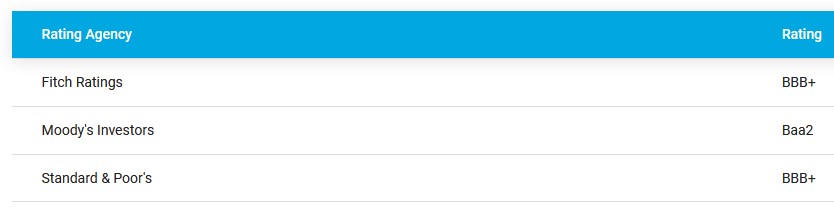

As I compose this post, A’s website reflects the following credit ratings.

Moody’s website, however, indicates that it upgraded A’s assigned credit rating from Baa2 to Baa1 on May 3, 2023. Now, all three ratings are the top tier of the Lower Medium Grade investment grade credit rating.

S&P Global completed its most recent review on July 21 and upgraded A’s outlook from Stable to Positive.

Fitch completed its most recent review on June 30 and affirmed A’s BBB+ rating with a Stable outlook.

All three rating agencies define A as having an adequate capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of A to meet its financial commitments.

Dividend and Dividend Yield

A’s dividend history on its website has not been updated as I compose this post; it does not yet reflect the recently announced dividend increase.

On November 16, A declared a $0.236/share dividend payable on January 24 to shareholders of record on December 29. This represents a ~4.9% increase from the prior $0.225.

With shares trading at ~$124, the dividend yield is negligible. Dividend metrics, however, are of little importance in my investment decision-making process. My interest lies in an investment’s total potential investment return.

I envision the bulk of A’s future total investment return will continue to be predominantly capital appreciation.

A’s weighted average shares outstanding in FY2013 – FY2023 are (in millions of shares) 345, 338, 335, 329, 326, 325, 318, 312, 307, 300, and 296.

Despite the challenging macroeconomic conditions, A maintains its balanced capital allocation strategy. As noted earlier, in FY2023 it repurchased ~$0.575B of its common shares.

Valuation

A’s FY2013 – FY2022 diluted PE levels are 27.23, 27.48, 31.92, 32.54, 31.89, 69.55, 25.31, 51.52, 40.52, and 35.80.

A’s valuation at the time of prior reviews is found in my August 16 post and September 12 post.

Using my $113.82 purchase price on September 11 and the $5.415 current mid-point of management’s FY2023 adjusted diluted EPS guidance, the forward adjusted diluted PE was ~21.

The forward-adjusted diluted PE using current broker estimates was:

- FY2023 – 17 brokers – ~21 using a mean of $5.42 and low/high of $5.40 – $5.46.

- FY2024 – 17 brokers – ~20 using a mean of $5.70 and low/high of $5.58 – $5.82.

- FY2025 – 14 brokers – ~17.8 using a mean of $6.40 and low/high of $6.21 – $6.76.

Looking at A’s valuation from an FCF perspective, management’s revised FY2023 FCF guidance was ~$1.2B. The diluted weighted average shares outstanding for the quarter ended July 31 was ~295 million. Divide the guidance by the shares outstanding and we arrive at ~$4.07. Using my $113.82 purchase price divided by ~$4.07 FCF/share resulted in a forward P/FCF value of ~28.

A’s share price closed at ~$124 on November 21 and management’s FY2024 adjusted diluted EPS guidance is $5.44 – $5.55 giving us a forward adjusted diluted PE range of ~22.3 – ~22.8.

The forward-adjusted diluted PE using current broker estimates is:

- FY2024 – 19 brokers – ~22.5 using a mean of $5.50 and low/high of $5.30 – $5.82.

- FY2025 – 19 brokers – ~20.4 using a mean of $6.09 and low/high of $5.60 – $6.50.

- FY2026 – 12 brokers – ~18.6 using a mean of $6.67 and low/high of $6.28 – $7.10.

Looking at A’s valuation from an FCF perspective, management’s FY2024 FCF guidance is ~$1.2B. Guidance assumes ~293 million shares outstanding in FY2024. Divide the FCF guidance by the shares outstanding guidance and we arrive at ~$4.10. Divide the current ~$124 share price by ~$4.10 FCF/share and we get a forward P/FCF value of ~30.2.

Final Thoughts

Management has provided lacklustre guidance for FY2024. Revenue growth is expected to be -1% to 1% and adjusted EPS is expected to be 0% – 2% YoY. Given expectations for a challenging environment, especially in the first half of FY2024, steps are being taken to adjust the cost structure. I remain confident about the long-term growth prospects of A’s end markets and think the near-term challenges are transitory.

In several posts, I state my desire to acquire shares in high-quality companies that have fallen out of favour. While A is still undervalued, its valuation is slightly less attractive than when I last acquired shares on September 11. With a share price increase of ~22% since the end of October. This suggests that investors are warming up to A.

I think there may be an opportunity to acquire additional A shares at a more favourable valuation if we experience a broad market pullback. I do not, therefore, intend to acquire additional shares at this point.

My current exposure consists of 500 shares in a ‘Core’ account within the FFJ Portfolio.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long A.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your due diligence and research. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.