Goldman Sachs’ (GS) earnings have historically been volatile. Once David Solomon took over CEO responsibilities from Lloyd Blankfein in January 2019, however, the firm embarked on a strategy to generate more durable and sustainable fee-based revenues and to better manage capital efficiency. Significant progress has been made over the past couple of years and GS’s earnings are becoming more resilient and diversified.

Historically, GS’s investing activities were executed with a merchant banking approach. This resulted in a significant reliance on the firm’s Balance Sheet. Now, a significant repositioning is underway toward a full-scale third-party solution and management fee-intensive model.

On April 15, 2022, following the release of GS’s Q1 2022 results, I wrote this post in which I deemed shares to be attractively valued. At the time I had insufficient available funds in the account which holds GS shares to permit the purchase of a reasonable number of additional shares.

I would typically wait for an earnings release (July 18 is the scheduled release date of Q2 2022 results) to write another post. After listening to the June 2, 2022 presentation by GS’s President & Chief Operating Officer at the Bernstein 38th Annual Strategic Decisions Conference, however, I have added to my GS position in one of the ‘Side’ accounts within the FFJ Portfolio.

Asset and Wealth Management

Key Trends

There is continued secular growth in the private markets. Based on industry research, projections call for the worldwide private alternative assets market to grow to $18T which represents a 15% CAGR growth rate over the next 5 years.

Most retail investors have limited exposure to alternative assets. There is, however, an increasing appetite amongst retail investors to add such assets to their investment portfolios.

Clients are also looking for greater customization and there is increasing demand for more planning and holistic advice.

To meet this demand, GS is creating more customized separate accounts for investors willing to invest a minimum of $250,000.

Acquisitions

In order to capture a significant portion of this growing market, accelerate the drive for more durable returns, and enhance its world-class franchise, GS has completed strategic acquisitions in recent years.

Growth Success

In the June 2 presentation, GS updates the investment community on how it is leveraging the power of the ‘1 GS approach’ to execute upon the significant franchise opportunities to unlock significant value creation for shareholders.

GS is currently the 5th largest active asset manager in the world with ~$2.7T in assets under supervision. It is also the world’s 5th largest asset manager with ~$431B in alternative assets of which ~$240B are earning fees at an average rate of 65 bps.

Source: GS – Presentation to Bernstein Strategic Decisions Conference – June 2, 2022

At its Investor Day in early 2020, GS had set a $150B cumulative alternatives fundraising target. By the end of Q1 2022, it had raised ~$131B of which ~$77B is earning fees at a ~80bps fee rate.

Source: GS – Presentation to Bernstein Strategic Decisions Conference – June 2, 2022

In Q1 2022, GS generated new inflows of ~$24B. Given its success at fundraising, the fundraising target is revised to ~$225B by the end of FY2024.

GS is also targeting management fees of $10B by the end of FY2024 with ~$2B of these fees to come from its alternatives franchise. This reflects a double-digit growth rate in management fees.

Source: GS – Presentation to Bernstein Strategic Decisions Conference – June 2, 2022

Differentiation

The asset management and wealth management industries are highly fragmented. The best way for an industry participant to differentiate itself is to generate superior long-term performance.

The following reflects how GS has performed against various benchmarks.

Source: GS – Presentation to Bernstein Strategic Decisions Conference – June 2, 2022

The size, scope, and growth opportunities across GS’s wealth management platform are significant. It has over $1T in client assets that are served by ~2200 advisors and content specialists. These advisors and content specialists serve the ultra-high net worth market

This business currently generates ~$6B of annual revenue which grew by over 25% in the last 12 months.

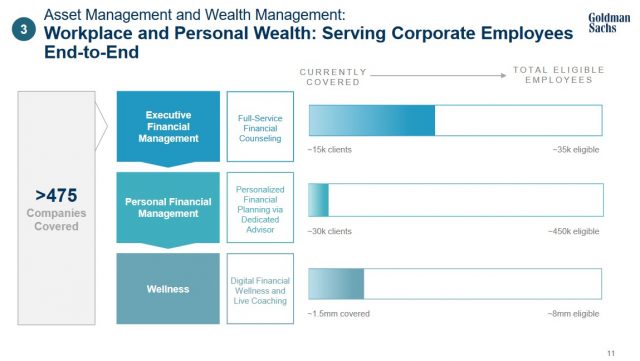

Workplace and Personal Wealth

GS serves ~55% of the Fortune 100 companies and has formed very strong relationships with C-suite clients.

It also has $115B of fee-paying assets under supervision that generated $1.3B of revenue in the last 12 months.

GS has expanded its capabilities to cover employees throughout these corporations.

Following the strategic acquisitions noted earlier, GS now provides advisor-led relationships to ~45,000 employees. It also provides digital financial wellness coaching to ~1.5 million employees. These services are often paid for by the employer.

Despite the inroads made to date, GS has a significant opportunity to expand its number of relationships. GS’s President & Chief Operating Officer has made a commitment to add 30 new client relationships and 80 new programs annually to the existing base of 475 companies served.

Credit Ratings

Investors are encouraged to review GS’s May 10, 2022 Fixed Income Investor Presentation.

I look at a company’s senior unsecured long-term debt and rating outlook to gauge the degree of risk I am assuming as a shareholder.

Ratings for GS and a number of its affiliates as of March 2, 2022 are accessible here.

The long-term debt ratings assigned to Goldman Sachs Group, Inc. are those of interest to me as this is the entity in which I have invested.

- Moody’s assigns an A2 rating with a stable outlook.

- S&P Global assigns a BBB+ rating with a stable outlook.

- Fitch assigns an A rating with a stable outlook.

The Moody’s and Fitch ratings are the middle tier of the upper-medium grade investment-grade category. The rating assigned by S&P is two notches lower at the top tier of the lower-medium grade investment-grade category.

Moody’s and Fitch define GS as having a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

S&P Global defines GS as having an ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

Despite the variance in ratings, all 3 ratings are satisfactory for my purposes.

Dividends and Share Repurchases

Dividend and Dividend Yield

GS does not maintain a dividend history on its website but this history is accessible here.

Included in this June 27, 2022 Press Release is a statement regarding GS’s capital plan that includes an increase in the common stock dividend from $2.00 to $2.50 per share. This proposed increase is subject to approval by GS’s Board at the customary Q3 meeting.

The current $2.00 quarterly dividend yields ~2.7% based on the current ~$296.50 share price. Should GS’s share price remain at roughly the current level and the dividend be increased to $2.50, the dividend yield would rise to ~3.4%.

As noted in several of my previous posts, focusing on dividend income and dividend yield metrics can lead to flawed investment decisions. Investors would be better served by focusing on an investment’s TOTAL potential return.

Share Repurchases

Since March 2000, GS’s Board has approved a repurchase program authorizing repurchases of up to 605 million common shares; it has no set expiration or termination date. The repurchase program is effected primarily through regular open-market purchases. The amounts and timing of these repurchases are determined primarily by GS’s current and projected capital position, but may also be influenced by general market conditions and the prevailing price and trading volumes of GS’s common stock.

In FY2021, repurchased $5.20B of common shares. In Q1 2022, it repurchased $0.5B of common shares (1.4 million shares at an average cost of $363.53).

GS has been a prolific buyer of its issued and outstanding shares over the years with the FY2009 – FY2021 weighted average number of diluted shares outstanding (in millions) being 550.9, 585.3, 556.9, 516.1, 499.6, 473.2, 458.6, 435.1, 409.1, 390.2, 375.5, 360.3, and 355.8 (355.9 in Q1 2022).

Valuation

At the time of my July 28, 2021 post, GS was trading at ~$375 and in the first half of FY2021, it had generated $33.64 in diluted EPS. Management does not provide guidance so using the forward-adjusted diluted PE guidance available from the 2 discount brokerage trading platforms I use, I arrived at the following:

- FY2021: 22 brokers, mean estimate $53.14, low/high range $48.39 – $60. Valuation using the mean estimate is ~7 and ~6.25 using the high end of the range.

- FY2022: 22 brokers, mean estimate $37.31, low/high range $32.98 – $41.50. Valuation using the mean estimate is ~10 and ~9 using the high end of the range.

- FY2023: 11 brokers, mean estimate $39.53, low/high range $34.37 – $43.70. Valuation using the mean estimate is ~9.5 and ~8.6 using the high end of the range.

When I wrote my October 15, 2021 post, GS had just released Q3 and YTD2021 results. Based on a ~$400 share price and adjusted diluted earnings estimates, GS’s adjusted diluted PE levels were:

- FY2021: 28 brokers, mean estimate $53.59, low/high range $48.66 – $58.63. Valuation using the mean estimate is ~7.46 and ~6.82 using the high end of the range.

- FY2022: 28 brokers, mean estimate $38.04, low/high range $32.98 – $43.82. Valuation using the mean estimate is ~10.5 and ~9.1 using the high end of the range.

- FY2023: 15 brokers, mean estimate $40.79, low/high range $34.37 – $46.05. Valuation using the mean estimate is ~9.8 and ~8.7 using the high end of the range.

My valuation calculations when I wrote my January 19, 2022 post were based on a ~$347.50 share price and the following adjusted diluted earnings estimates:

- FY2022: 26 brokers, mean estimate $40.52, low/high range $34.58 – $45. Valuation using the mean estimate is ~8.6.

- FY2023: 24 brokers, mean estimate $42.23, low/high range $37.65 – $48. Valuation using the mean estimate is ~8.2.

When I wrote my April 15, 2022 post, GS was trading at ~$321.60. Its valuation based on current adjusted diluted earnings estimates was:

- FY2022: 27 brokers, mean estimate $37.92, low/high range $31.04 – $44.68. Valuation using the mean estimate is ~8.5.

- FY2023: 28 brokers, mean estimate $40.48, low/high range $34 – $45.30. Valuation using the mean estimate is ~8.

- FY2024: 14 brokers, mean estimate $43.88, low/high range $34.71 – $50.17. Valuation using the mean estimate is ~7.3.

With shares now trading at ~$296.50 and the following current adjusted diluted earnings estimates, GS’s valuation levels are:

- FY2022: 25 brokers, mean estimate $35.19, low/high range $28.70 – $41.25. Valuation using the mean estimate is ~8.4.

- FY2023: 26 brokers, mean estimate $38.70, low/high range $26.10 – $45.30. Valuation using the mean estimate is ~7.7.

- FY2024: 16 brokers, mean estimate $42.72, low/high range $32.56 – $48.50. Valuation using the mean estimate is ~6.9.

Final Thoughts

The COVID-19 pandemic led to high trading activity and record earnings in 2021; economic uncertainty prompted companies to issue debt and equity to initially bolster capital. They later issued debt and equity to take advantage of low interest rates and a strong stock market.

I expect net revenue to pull back in 2022 and 2023. Brokers that cover GS also expect weaker results from those reported in FY2021.

Despite the expectation for lower earnings, I like that GS’s earnings are becoming more resilient and diversified. The investment management business is a relatively stable business and typically generates a high return on capital.

GS has built out a large virtual bank and at FYE2021 it had ~$350B on deposit versus ~$39B at FYE2009. This deposit base and the related net interest income should add more stability to GS’s revenue stream and balance sheet over the medium term.

Since GS is significantly leveraged to rising interest rates, its valuation should not be affected to the same extent as its peers by the uncertainty over inflation and interest rates.

My focus is on increasing exposure to my top 30 holdings; GS was not a top 30 holding when I completed my Mid 2022 Investment Holdings Review. Nevertheless, I acquired additional shares on July 7 at ~$296 because I like the company and its shares are attractively valued. My plan is to periodically add to my GS exposure when its valuation is acceptable.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long GS.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.