![]()

Summary

- MMM released its Q1 2018 results on April 24, 2018 and revised its projected FY2018 GAAP EPS while leaving its adjusted projected EPS estimate unchanged.

- In my opinion, MMM was overvalued earlier in 2018 and the recent pullback has prompted me to increase my position.

- The company’s stock price could certainly pullback further but I don’t invest for the short-term. I am reasonably confident MMM’s stock price and dividend will be far greater 10, 20, 30 years into the future.

Introduction

In my October 9, 2017 I Applaud JP Morgan Analyst for Downgrading 3M (NYSE – MMM) article I agreed the company’s stock was richly valued. At the time of the article MMM was trading at $216.50.

It certainly was interesting to see how euphoric investors ran MMM’s stock price up to ~$260 toward the end of January 2018. I was puzzled as to how some investors would think a ~20% price appreciation in a span of ~3.5 months could be justified for a behemoth like MMM. The company is certainly not a small cap stock that has created a revolutionary product or service that is going to make the world stand on end.

The stock’s price appreciation certainly did wonders for my portfolio given that it is my 3rd largest holding. Truthfully, however, I paid very little attention to the rapid price appreciation; I don’t look at the value of my portfolio every day.

Some would argue that I should have sold my position when I felt MMM was exceedingly overvalued. There is some merit to this argument but that would have attracted a significant tax obligation given that my average cost prior to my most recent purchase was ~$109.

Others may offer that I should have written covered calls if I was so confident MMM was overvalued. In hindsight, I should have…but I didn’t. You win some, you lose some but I take comfort knowing that Messrs. Buffett and Munger most likely do not always write covered calls when they think one of their holdings is overvalued.

Now that MMM has released its Q1 2018 results and the stock has retraced to ~$199 I thought I would have another quick look at MMM.

Q1 2018 Results and 2018 Outlook

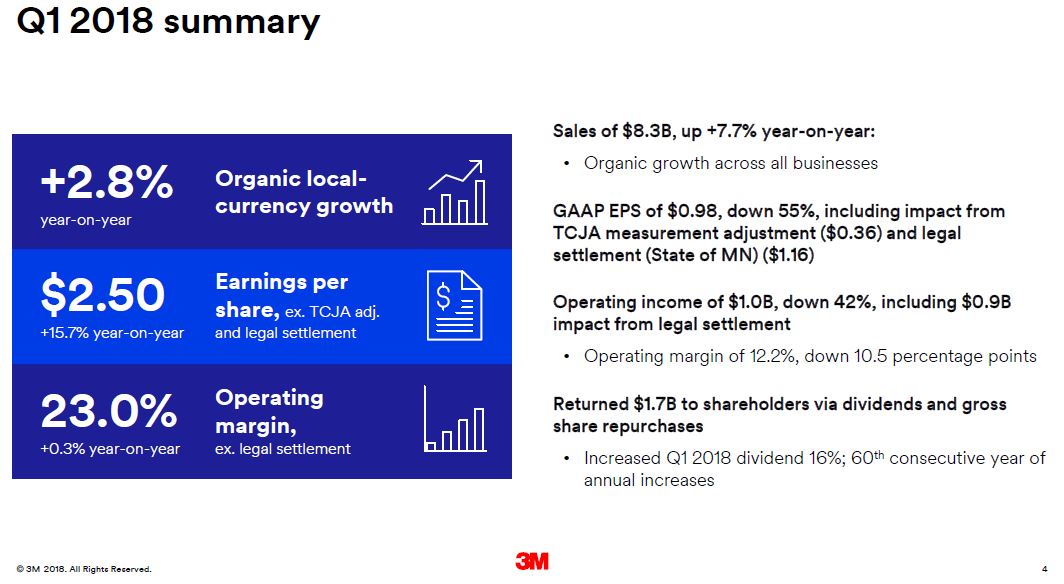

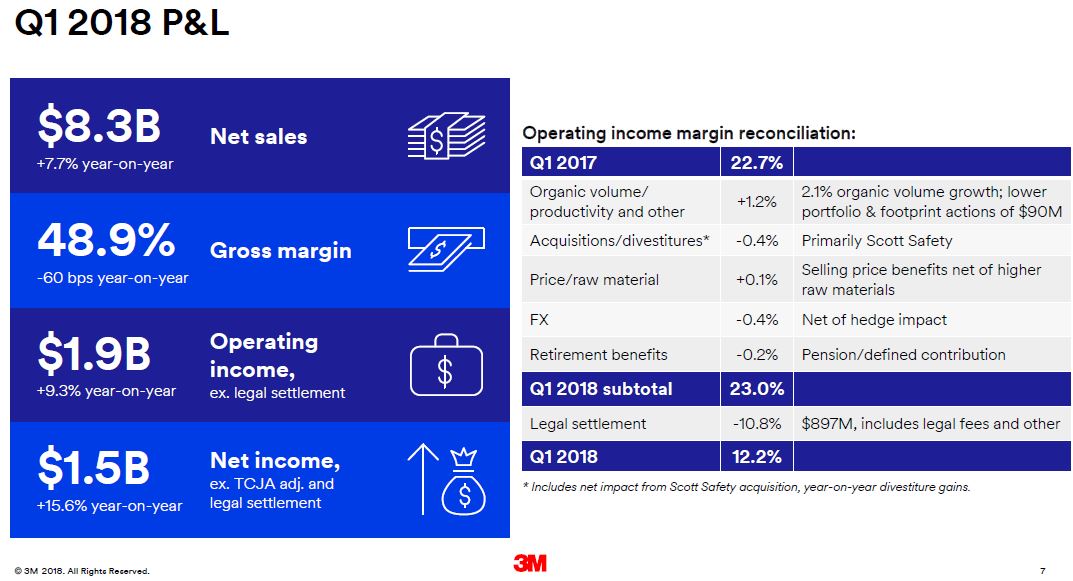

On April 24, 2018, MMM released its Q1 2018 results.

While MMM experienced a 60 bps YoY gross margin reduction, investors need to take this in stride. I don’t think there has been a company which has continuously experienced an increase in gross margin over an extended period.

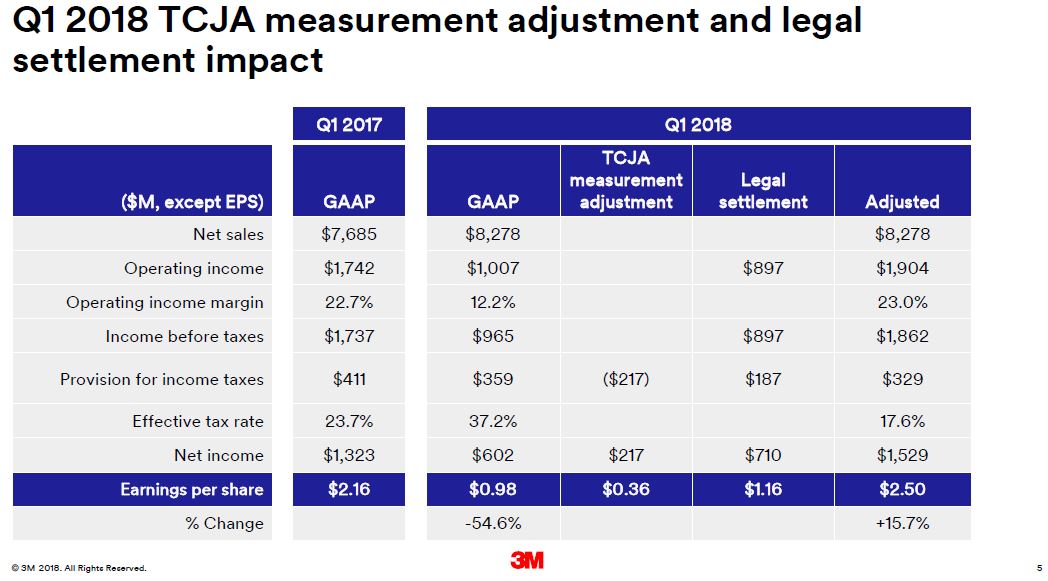

In my opinion, MMM’s results were positive but there were a couple of sizable one-time charges which negatively impacted MMM’s results thus resulting in a downward revision of projected earnings for FY2018. These two charges are the:

- $0.897B settlement in February 2018 related to a lawsuit commenced in 2010;

- $0.217B charge related to the Tax Cuts and Job Act (TCJ).

The February 2018 settlement relates to a lawsuit with Minnesota’s Attorney General Lori Swanson for $0.897B (this includes legal fees). In 2010, the State of Minnesota launched a lawsuit over a former Scotchgard ingredient that entered the state’s drinking water. At the time, the state indicated it would seek punitive damages that would bring its total demand in the lawsuit to $5B.

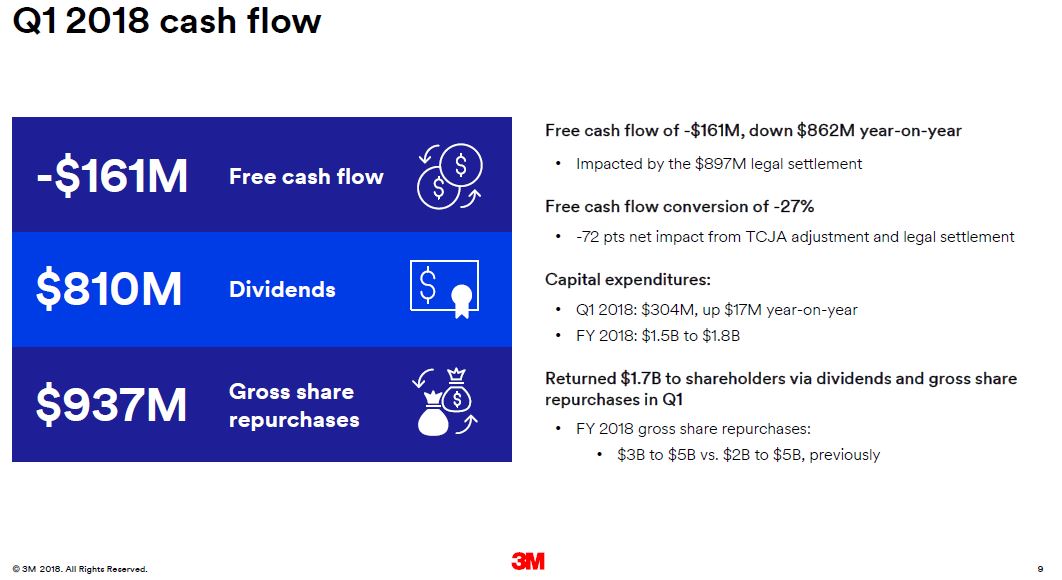

These two one-time items amount to $1.114B. Investors would be naïve to think that one-time charges of this magnitude would not have an impact on earnings.

Although no investor likes to see a one-time hit of this magnitude I choose to view this settlement from a positive perspective. Now MMM no longer needs to incur significant legal costs. Secondly, the magnitude of the settlement is far less than what MMM could have incurred.

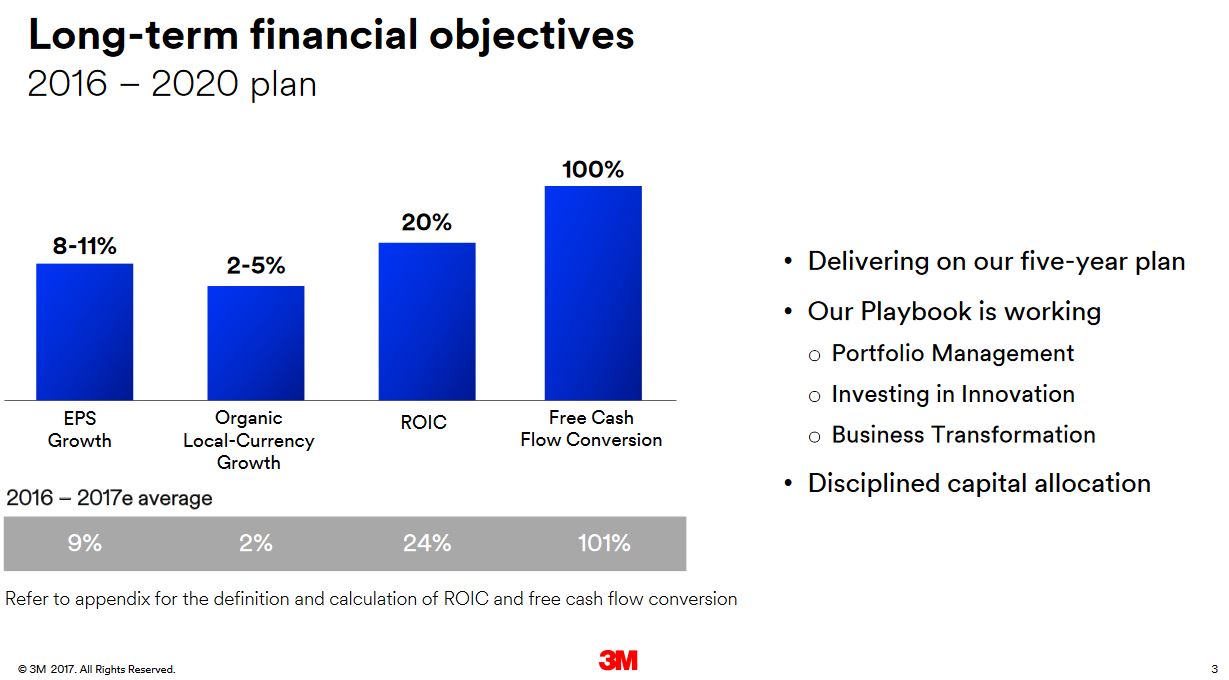

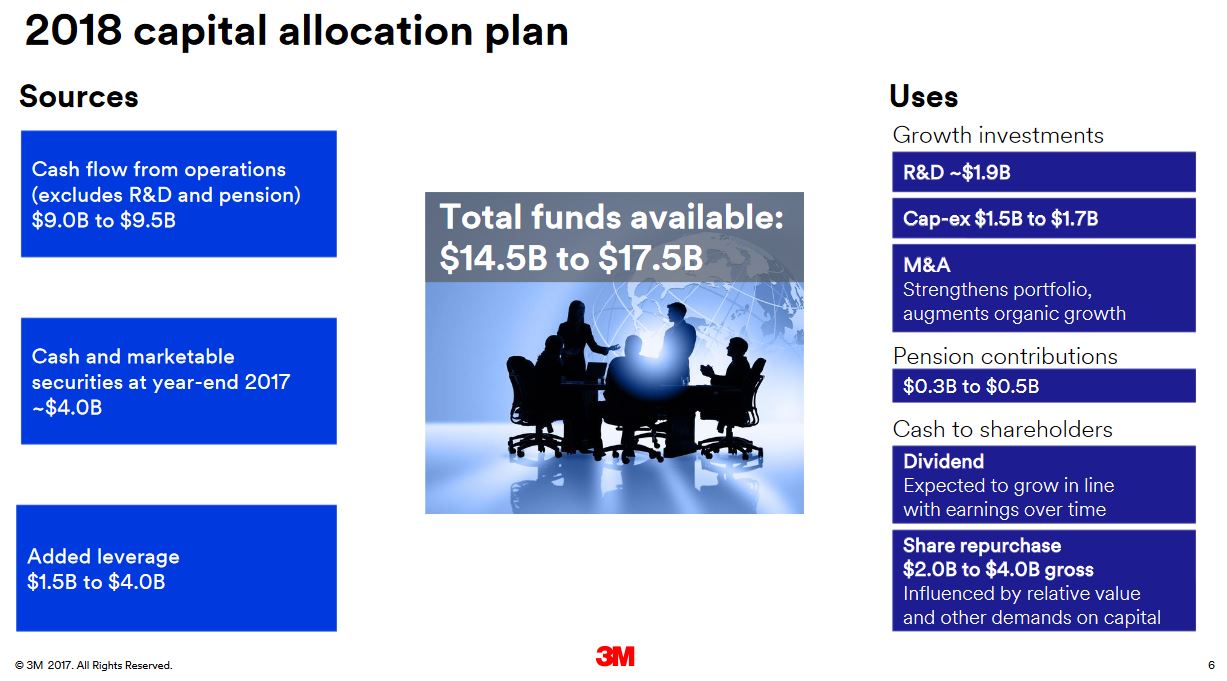

By way of background, let’s look at management’s projections for FY2018 which were presented December 12, 2017.

Source: MMM – 2018 Financial Outlook Presentation – December 12, 2017

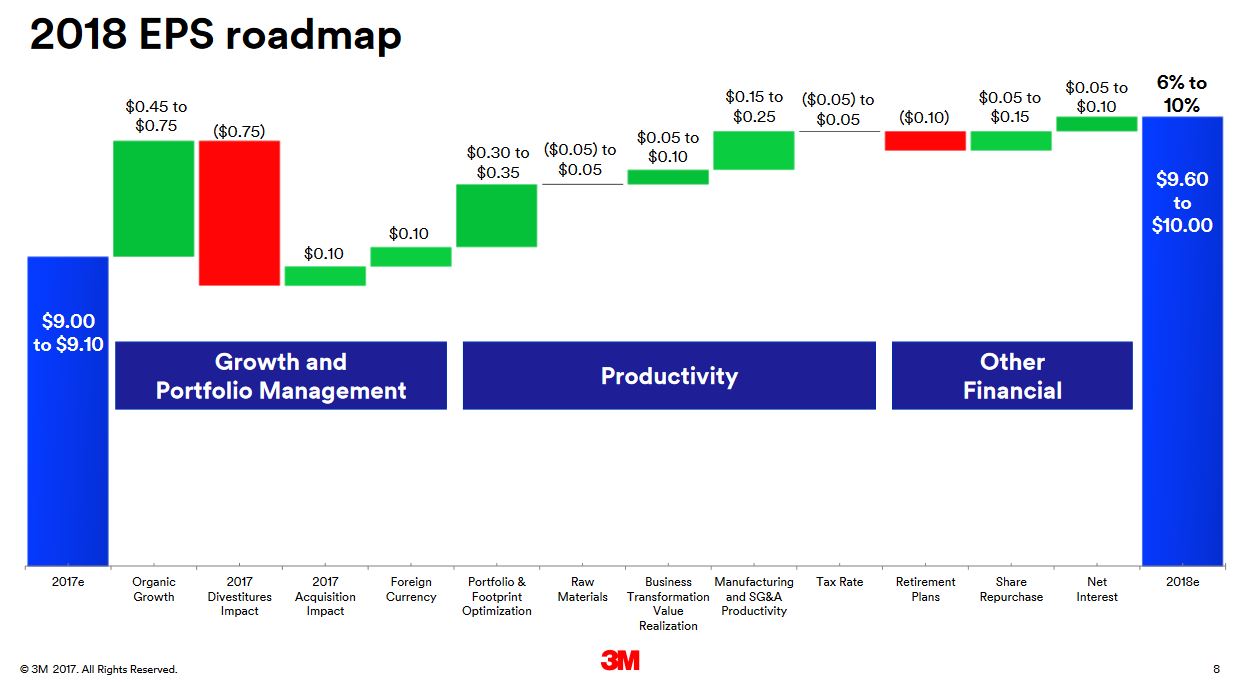

Less than one and a half months later, management projected an increase in earnings from those presented in December 2017. Clearly management was optimistic about FY2018.

Source: MMM – Q4 2017 Financial Results Presentation – January 25, 2018

Subsequent to the release of the revised projections on January 25, 2018, MMM incurred the one-time charges reflected above. Given these charges, GAAP projections have been revised downward but I think investors need to look at adjusted estimates since the sizable one time charges are expected to be non-recurring.

Source: MMM – Q1 2018 Financial Results Presentation – April 24, 2018

Credit Ratings

In 2007, Moody’s rated MMM’s senior unsecured long-term debt Aa1 (upper tier of the ‘high grade’ rating). It now rates this debt A1 (upper tier of the ‘upper medium grade’ rating).

S&P Global rates MMM’s senior unsecured debt AA- which is the lowest tier of the ‘high grade’ rating.

Neither agency has MMM’s credit ratings under review.

The attractive credit ratings confirm that neither agency is of the opinion MMM will have any difficulty in servicing its obligations.

Valuation

If we look at management’s FY2018 forecast presented December 2017 we see that GAAP EPS estimates were $9.60 – $10. On the date of that presentation, MMM was trading at ~$237. On this basis, the forward PE was ~23.7 – ~24.7.

Fast forward to January 25, 2018 at which time MMM was trading at ~$252; it subsequently jumped to ~$258 following the Q4 and FY2017 earnings release. The GAAP EPS range was revised to $10.20 – $10.70 thus giving us a forward PE of ~23.55 – ~24.7 which was almost identical to that in December 2017.

Now we have a projected GAAP EPS range of $8.68 – $9.03 and the stock is trading at ~$199 as at April 25, 2018. This gives us a forward PE range of ~22.04 – ~22.93. On the basis of adjusted forward EPS of ~$10.20 – ~$10.55 (we’re backing out the one-time charges), we get a forward adjusted PE range of ~18.86 – ~19.5. Personally, I view this as an acceptable valuation for a company of MMM’s pedigree.

I will readily admit that I cannot consistently accurately predict the direction of a company’s stock price over the short-term. I am, however, reasonably confident that I have a better than 50-50 chance of predicting whether a company’s stock price will be lower/higher 10, 20, 30 years into the future given that I invest in high quality companies. In the case of MMM, I think my odds are far greater than 50-50 of being accurate when I say the stock price will be higher in those 3 timeframes.

Dividend, Dividend Yield, Dividend Payout Ratio, and Share Repurchases

MMM’s dividend history can be found here and its stock split history can be found here.

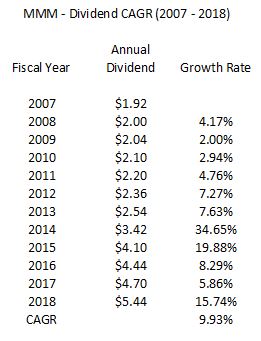

The following is MMM’s dividend compound annual growth rate for the 2007 – 2018 period.

Subsequent to my previous MMM article dated October 9, 2017, MMM increased its $1.175 quarterly dividend to $1.36 starting with the dividend which was distributed March 12, 2018. MMM’s $5.44 annual dividend now provides investors with a ~2.73% dividend yield. While many investors will scoff at this level considering we are in a rising interest environment, I view this yield as acceptable. I do not merely invest in a company for the sake of its dividend. I invest for the dividend income and capital gains potential. The dividend merely allows me to be patient while management navigates the company over an extended period.

On the basis of projected GAAP EPS of $8.68 – $9.03, the $5.44 annual dividend represents a ~60% – ~62.7% dividend payout ratio. This is somewhat elevated but if we take into consideration the significant one-time charges and use the projected adjusted EPS range of ~$10.20 – ~$10.55, the dividend payout ratio is reduced to a more respectable range of ~51.6% – ~53.3%.

As at the end of FY2010 (page 46 of 138 of the 10-K) the weighted average number of diluted shares outstanding amounted to 725.5 million. As at the end of FY2017 (page 57 of 176 of the 10-K) the weighted average number of diluted shares outstanding had been reduced to 612.7 million.

Long-term debt has certainly ballooned during this time frame as MMM has not only raised debt to finance its growth but is has also resorted to issuing debt to repurchase outstanding shares. Having said this, MMM has certainly raised debt at extremely attractive interest rates (refer Note 11 on page 91 of 176 in MMM’s FY2017 10-K for which a link has been provided above).

Management has clearly communicated that it intends to reward shareholders through share repurchases and dividend increases. I have absolutely no idea whether management intends to increase its debt level to repurchase shares going forward. I am confident, however, that management will continue to do what is right for MMM and its shareholders.

Source: MMM – 2018 Financial Outlook Presentation – December 12, 2017

Final Thoughts

In late 2017, and earlier in 2018, I viewed MMM as being somewhat expensive. I, therefore, chose to bide my time to wait for more attractive valuations so as to increase my MMM position.

MMM has now retraced to a level I view as reasonable based on management’s updated projections for FY2018. It is entirely possible MMM’s stock price could experience further weakness but I have no way of knowing this. Given that I am happy to acquire additional shares at ~$199, I just recently acquired another 200 shares. All dividends will be automatically reinvested.

Hopefully one day, well into the future, my wife’s/my beneficiary will be grateful for this recent purchase.

I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this post. As always, please leave any feedback and questions you may have in the “Contact Me Here” section to the right.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long MMM.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.