Contents

On July 25, I added to my RTX Corporation (RTX) exposure with the purchase of 100 shares @ $85.67. I subsequently acquired another 100 shares @ ~$78.02 on September 11; I disclosed these purchases in posts that can be found in the FFJ Archives.

When I wrote my January 24, 2024 RTX Corporation post, however, I concluded its valuation was not justified. At the time of that post, the most current financial information was for Q3 and YTD2023.

On April 23, RTX released Q1 2024 results and affirmed its FY2024 outlook which it provided with the release of its Q4 and FY2023 results on January 23. I, therefore, revisit this existing holding.

Business Overview

RTX has 3 business segments (Collins Aerospace, Pratt & Whitney, and Raytheon). Investors unfamiliar with RTX should review the company's website and Part 1 Item 1 within the 2023 Form 10-K.

RTX's revenue is almost evenly split between commercial and defense revenue. Most of its competitors, however, derive their revenue from either commercial or defense.

In my prior post, I discuss the Pratt & Whitney's challenges resulting from microscopic contaminants in a metal used in part of the Geared Turbofan (GTF) engines that power Airbus' popular A320neo jets. Up to this point, RTX appears to have contained the financial fallout from this recall. The maintenance plan, however, is slated to continue for a few more years.

In Q1, Pratt & Whitney delivered 65 more large commercial engines than in Q1 2023. This increase is partially attributed to deliveries to alleviate stress on customers who can use extra spare engines to keep planes operational while existing engines undergo inspection and servicing of the metallurgically affected engine components. This boosted Q1 revenue but not operating profit because RTX derives profits from after-market service and not from engine deliveries; original equipment sales typically generate low or no margins while the recurring servicing and parts revenue often generates high margins.

A very high level overview of the Q1 2024 results for each business segment is presented in the Q1 Form 10-Q and in the April 23 Press Release and Earnings Presentation.

Much like Lockheed Martin (LMT) which I reviewed in this April 24 post, RTX benefits from global conflict although not nearly to the same extent as LMT.

Financials

Q1 2024 Results

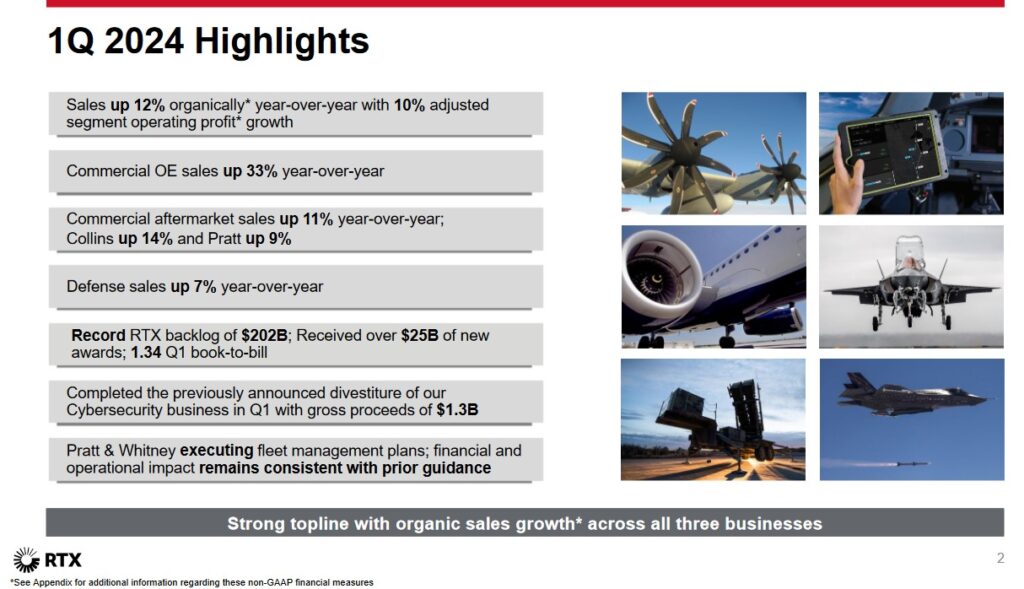

RTX reported organic sales growth of 12% relative to Q1 2023, adjusted diluted EPS growth of 10% relative to Q1 2023, and $125M negative free cash flow (FCF). This negative FCF was in line with expectations and was a $1.3B YoY improvement.

The commercial aerospace industry is still working through supply chain constraints and other challenges. This is leading to some production rate uncertainty.

On the defense side, RTX will benefit from the approved 2024 US defense budget. This budget supports RTX's key programs and technologies, including next-generation propulsion, critical munitions and upgrades to the F135, ensuring it remains the only engine powering every variant of the F-35 Joint Strike Fighter. The budget also supports investment in key capabilities to address current and future threats such as systems that counter unmanned aircraft and hypersonics, where RTX provides leading technologies.

RTX also stands to benefit from the Ukraine supplemental bill, which the Department of Defense will use to further deepen critical U.S. munition stockpiles and provide needed air defense capabilities to the region with NASAMS and Patriot. Internationally, RTX continues to see heightened demand from U.S. allies. In Q1, RTX was awarded a $1.2B contract to supply Germany with additional Patriot air and missile defense systems.

During the quarter, RTX completed the sale of Raytheon's cybersecurity business with gross proceeds of $1.3B.

It also made progress on deleveraging the balance sheet, having paid down over $2B of debt since it initiated the Accelerated Share Repurchase in late 2023.

The overall backlog is at a record $202B and RTX remains focused on meeting its customer commitments.

RTX is investing over $10B R&D, modernization and digital capabilities and it continues to evaluate its portfolio for incremental opportunities to further enhance its focus and prioritize future investments.

On the Q1 earnings call, management stated that RTX remains on track to return $36B - $37B of capital to shareholders from the date of the United Technologies/Raytheon merger through 2025.

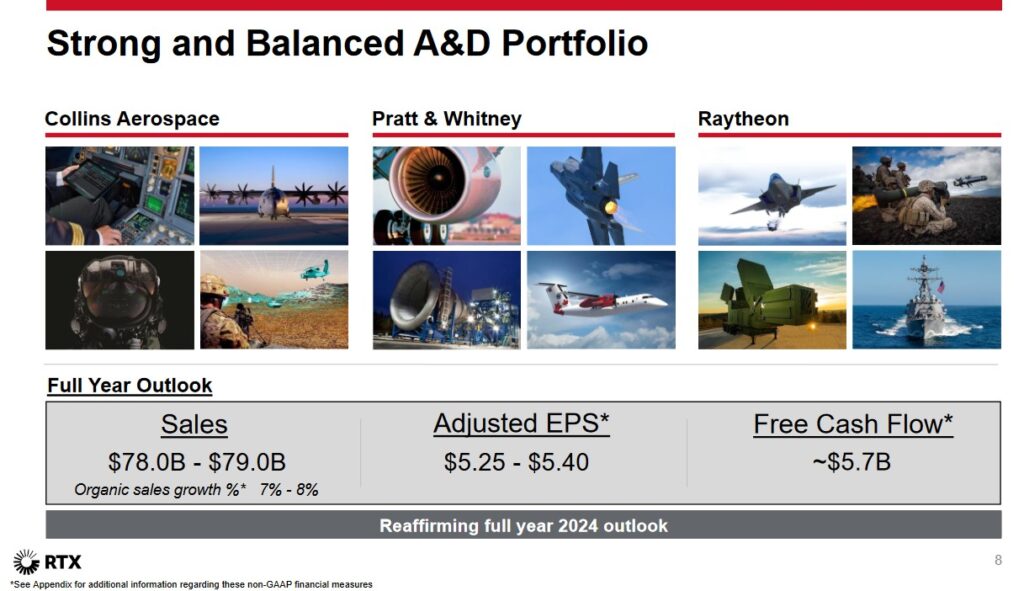

FY2024 Outlook

RTX's FY2024 outlook presented on April 23 is unchanged from that presented with the release of FY2023 results on January 23.

Credit Ratings

Moody's continues to assign a Baa1 rating to RTX's senior unsecured domestic currency debt with a stable outlook.

S&P Global assigns a BBB+ for RTX Corp.'s senior unsecured notes with a negative outlook. This rating is equivalent to that assigned by Moody's.

Both ratings are the top tier of the lower medium-grade category and define RTX as having an ADEQUATE capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity to meet its financial commitments.

Both ratings are investment grade and are acceptable for my purposes.

Dividend and Dividend Yield

RTX's dividend history, reflects the recent disbursement of the 4th consecutive $0.59/share quarterly dividend.

I anticipate RTX will soon declare an increase in its quarterly dividend to $0.63/share. If this does materialize, the next 4 quarterly dividend distributions will total $2.52. Using the ~$101.40 share price as I compose this post, the estimated forward dividend yield is ~2.5%. This is somewhat lower than the dividend yield at the time of my July and September 2023 purchases.

Dividend metrics, however, have little influence on my investment decision making process. I am interested in an investment's total potential shareholder return.

RTX's weighted average number of issued and outstanding shares in FY2010 - FY2023 (in millions rounded) is 923, 907, 907, 915, 912, 883, 826, 799, 810, 864, 1,358, 1,509, 1,486, and 1,435. In Q4, however, RTX repurchased $10.283B of its shares by way of an accelerated share repurchase (ASR) program. This reduced the weighted average number of shares outstanding in Q4 2023 to 1,361.7. In Q1 2024, the weighted average fell to 1,337.3.

Given the significant ASR is late 2023, RTX is unlikely to make any significant share repurchases in FY2024. The priority is to reduce the debt taken on for this ASR.

Valuation

Please refer to my January 24, 2024 post which reflects RTX's valuation at the time of prior posts.

With shares trading at ~$101.40 and no change to RTX's FY2024 adjusted diluted EPS outlook of $5.25 - $5.40, the current forward adjusted diluted PE range is ~18.8 - ~19.3.

The following reflects RTX's valuation using a ~$101.40 share price and the current broker forward-adjusted diluted earnings estimates.

- FY2024 - 23 brokers - mean of $5.39 and low/high of $5.17 - $5.55. Using the current mean, the forward adjusted diluted PE is ~18.8.

- FY2025 - 23 brokers - mean of $6.13 and low/high of $5.24 - $6.78. Using the current mean, the forward adjusted diluted PE is ~16.6.

- FY2026 - 15 brokers - mean of $6.83 and low/high of $5.38 - $7.40. Using the current mean, the forward adjusted diluted PE is ~14.8.

Looking at RTX's valuation from a FCF perspective, it repurchased $10.283B of its shares by way of an ASR in late 2023, and therefore, I expect no significant share repurchases in FY2024; the weighted average number of shares outstanding in FY2024 was 1,337.3 million. Additional shares may be issued as part of the company's stock based compensation arrangements so let's suppose this increases the weighted average to 1,340 million shares in FY2024.

The FY2024 FCF outlook is ~$5.7B. Divide $5.7B by 1,340 million shares and we get FCF/share of ~$4.25. Divide the current ~$101.40 share price by ~$4.25 and we get a forward P/FCF of ~23.8. RTX's P/FCF in FY2014 - FY2023 was 13.81, 14.16, 19.81, 20.84, 12.46, 15.83, 16.99, 24.53, 26.62, and 15.84; United Technologies and Raytheon merged on April 3, 2020 so we can't make a direct comparison between the current P/FCF and levels prior to the merger.

Final Thoughts

RTX's FY2024 outlook has not changed yet the share price has risen ~$11 from ~$90 from when I analyzed it in my January 24 post. From a forward adjusted diluted EPS perspective, RTX's valuation is now slightly less attractive.

LMT and RTX both operate in the aerospace and defense industry. LMT, however, focuses heavily on defense while RTX derives roughly an equal amount of revenue from both. Nevertheless, I compare their respective valuation and expect them to be somewhat similar. Currently, RTX's forward adjusted diluted PE and forward P/FCF is somewhat higher than that of LMT. I consider LMT to be fairly valued and while RTX is also fairly valued, it is slightly less so than LMT.

I hold RTX shares in a 'Core' account and a 'Side' account within the FFJ Portfolio and when I completed my 2023 Year End FFJ Portfolio Review, it was not a top 30 holding.

The ability to generate an attractive total investment return depends heavily on the entry point. While RTX appears to be fairly valued, I wish to invest in companies that are undervalued, and therefore, do not intend to immediately acquire additional shares.

If the share price were to retrace to ~$90, RTX's valuation based on FY2024 forward adjusted diluted EPS would be ~16.7 and ~21 on a forward FCF basis. At $90 or less, I would consider adding to my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to [email protected].

Disclosure: I am long RTX.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.