Cyber criminal activity is becoming increasingly common and damaging. Cybersecurity companies, therefore, have captured the interest of many investors. While investment opportunities abound, it is important not to overlook the risks when investing in this sector. This is a highly fragmented industry. While many companies offer compelling solutions, some have yet to demonstrate consistent profitability and the ability to generate strong free cash flow (FCF).

Palo Alto Networks (PANW) is one industry participant that is profitable and which generates strong FCF.

I do not currently have exposure to PANW. With the release of Q4 and FY2024 results and FY2025 guidance on August 19, 2024 this is an opportune time to analyze this company.

Business Overview

PANW is a global cybersecurity provider.

Its cybersecurity platforms and services help secure enterprise users, networks, clouds, and endpoints. It focuses on delivering value in 4 fundamental areas:

- Network security;

- Cloud security;

- Security operations; and

- Threat Intelligence and Security Consulting (Unit 42)

PANW has built a broad cloud-based security platform through acquisitions; cloud software revenue is becoming a larger part of overall sales.

The FY2024 Form 10-K is unavailable as I compose this post. Until such time as it becomes available, I recommend reviewing Part 1, Item 1 in the FY2023 Form 10-K for a comprehensive overview of the business, competition, and risks.

PANW/IBM Partnership

In May 2024, PANW and IBM announced a broad-reaching partnership to deliver AI-powered security outcomes for customers.

This deal is expected to close by the end of September, depending on the timing of regulatory approvals and other customary closing conditions.

Competition

PANW operates in the intensely competitive enterprise security industry that is characterized by constant change and innovation. Its main competitors fall into 4 categories:

- large companies that incorporate security features in their products, such as Cisco Systems, Inc. , Microsoft, or those that have acquired, or may acquire, security vendors and have the technical and financial resources to bring competitive solutions to the market;

- independent security vendors, such as Check Point Software Technologies Ltd. , Fortinet, Inc. , Crowdstrike, Inc. , and Zscaler, Inc. , that offer a mix of security products;

- startups and point-product vendors that offer independent or emerging solutions across various areas of security; and

- public cloud vendors and startups that offer solutions for cloud security (private, public, and hybrid cloud).

Financials

Q4 and FY2024 Results

Refer to material related to PANW’s Q4 and FY2024 Earnings.

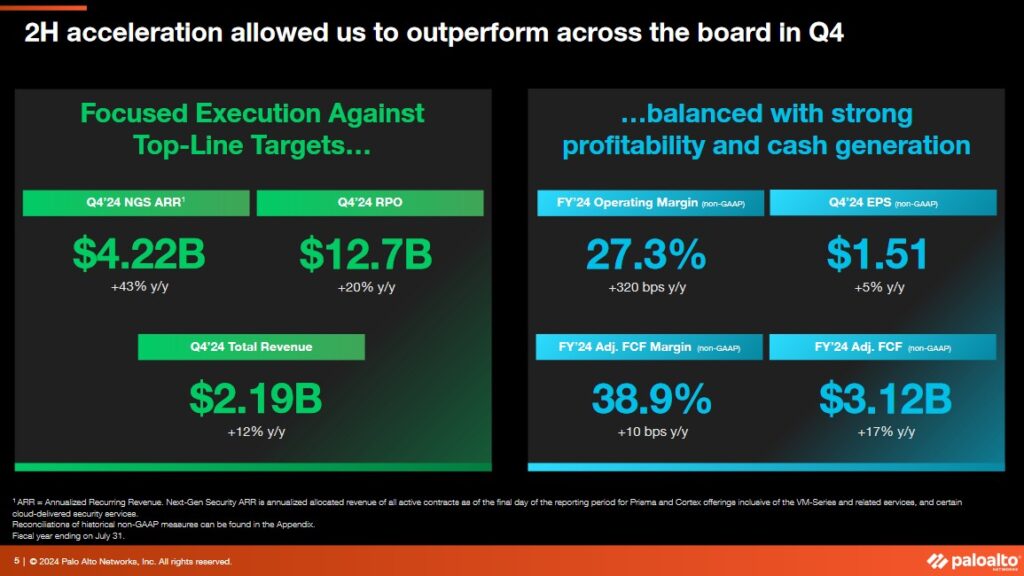

In Q4, PANW reported $4.22B in ‘Next Generation Firewalls‘ (NGS) annual recurring revenue (ARR).

PANW has de-emphasized billings guidance, a sales growth metric. Starting in Q4, it will provide an outlook for remaining performance obligations (RPO) instead. This metric is the total value of contracted revenue PANW has not yet recognized as revenue on its financial statements.

A little over a year ago, PANW began to see the impact of rising interest rates on how customers perceive the cost of money and procurement situations. Many customers started to ask for payments to be spread over multiple years instead of an upfront payment. In response, PANW leveraged programs such as annual billings and its financing capability. The impact on billings varied based on which program the customer chose and how the deal was structured.

In FY2023, PANW rolled out its ‘platformization strategy’ and offered customers more flexibility in payment terms when making large strategic commitments; this rollout has sharpened PANW’s focus on maximizing ARR and now all incentives are aligned to NGS ARR.

NGS ARR shows the return on the significant investments PANW has been making in the next-generation areas of its cybersecurity market that are also growing the fastest. Expectations are for these offerings to disproportionately drive growth as PANW transforms its revenue.

Revenue and RPO are important to understanding PANW’s business momentum. Revenue gives the near-term view of PANW’s growth. RPO, however, helps in understanding the longer-term trend and the scale of PANW’s book of business that will drive revenue.

The long-term growth in RPO influences revenue growth over time and gives visibility into the future trend; the contracts included in RPO are all non-cancelable and non-refundable in nature.

Commencing with Q4 2024, PANW will focus on NGS ARR as its key top line guidance metric in addition to revenue. Guidance for this metric will be provided quarterly and annually.

The relentless focus on improving operating margins has been the most important driver of FCF margin. Operating margins have improved by over 800 bps since FY2021, which is when PANW began a more intensive focus on profitable growth.

PANW continues to see opportunities to expand its operating margins supporting FCF.

Beyond improvements in operating profitability, the timing of customer cash payments impacts FCF. Over the last four years, PANW has gradually absorbed an increase in customer preference for payments over time, increasing this proportion of bookings from 6% in FY2020 to ~30% in Q4 2024 while maintaining or even increasing FCF margins.

Looking at the FYE2024 Balance Sheet, we see that current assets and current liabilities total ~$6.85B and ~$7.68B, respectively. Of the ~$7.68B in short term liabilities, however, there is ~$5.54B of deferred revenue; PANW also had ~$5.94B in long-term deferred revenue. This deferred revenue is funds received from clients before services are provided; this short-term deferred revenue will convert to revenue within 1 year.

Altogether, PANW had ~$11.48B of client funds with which to funds operations thus explaining why the company has no long-term debt.

I always recommend a review of the Risk section of the Form 10-Q and Form 10-K. It is within this section of the SEC Filing that we see that PANW derives substantially all of its revenue from sales generated through its channel partners, including distributors and resellers. Generally, 3 distributors individually represent 10% or more of PANW’s total revenue and in the aggregate generally represent ~45% – ~47% of total revenue. At the end of Q3 2024, two distributors individually represented 10% or more of PANW’s gross accounts receivable. In the aggregate, they represented over 37% of PANW’s gross accounts receivable.

The Palo Alto Networks 2023 Partner Award Winners announcement gives an indication of who are some of PANW’s top partners.

A list of PANW’s partners is available through this portal.

Goodwill and Intangible Assets at FYE2024 totaled ~$3.625B. Notes 7 and 8 in the Q3 2024 Form 10-Q provide details about some of PANW’s recent acquisitions and related goodwill and intangible assets.

The convertible senior notes dropped ~$1.028B to ~$0.964B at FYE2024 from ~$1.163B at the end of Q3 2024 and ~$1.992B at FYE2023. Details of these convertible senior notes are found in Note 9 with the Q3 2024 Form 10-Q. This reduction was driven by the early conversion of PANW’s convertible debt, which occurred at the option of debtholders. Settlement was through cash and equity. The remaining debt matures in June 2025, although early conversions may occur.

PANW’s adjusted diluted EPS is distorted by ~$2.139B of Income tax and other tax adjustments ($6.04/share). This amount consists of income tax adjustments related to our long-term non-GAAP effective tax rate. During FY2024, it included a tax benefit from a release of PANW’s valuation allowance on U.S. federal, U.S. states other than California, and United Kingdom deferred tax assets.

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

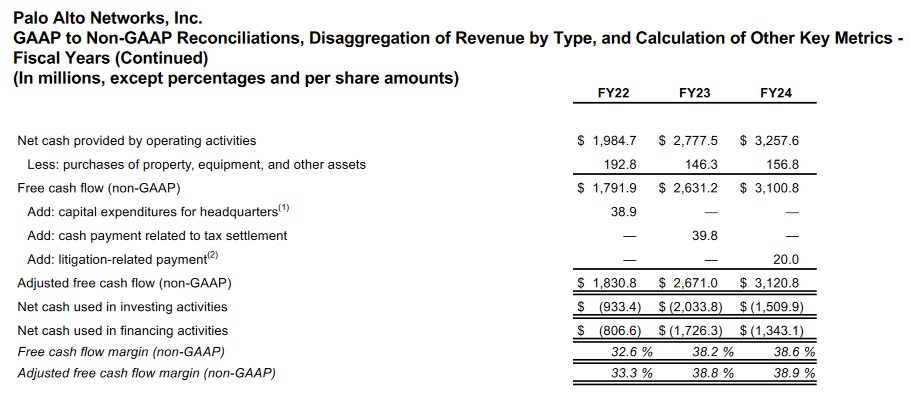

In FY2021 – FY2024, OCF, CAPEX, and FCF were:

- OCF was (in millions of $) 1.503, 1.985, 2.778, and 3.258

- CAPEX was (in millions of $) 0.116, 0.193, 0.146, and 0.157

- FCF was (in millions of $) 1.387, 1.792, 2.632, and 3.101

PANW’s annual CAPEX is negligible. It does, however, spend a considerable amount on research and development (R&D). In FY2021 – FY2024, it spent $1.140B, $1.418, $1.604, and $1.809. These expenses are deducted from earnings to determine Net Income so they come into the equation when determining PANW’s OCF and FCF.

Capital Allocation

PANW’s capital allocation priority is to reinvest in the company to retain its competitive advantage. It could scale back its R&D and increase its share repurchases but this would be detrimental to the long term success of the company.

PANW operates in a highly competitive industry and while CAPEX is relatively negligible, the billions it spends on R&D is akin to a Class A railroad’s annual CAPEX. Both must spend billions just be remain competitive.

PANW also allocates capital toward opportunistic acquisitions.

Opportunistic share repurchases to offset shares issued as part of the company’s various employee compensation plans is the third form of capital allocation.

Q1 and FY2025 Outlook

In Q1 2025, PANW expects:

- Total revenue of $2.10B – $2.13B, representing YoY growth of 12% – 13%;

- Diluted non-GAAP net EPS of $1.47 – $1.49, representing YoY growth of 7% – 8%.

In FY2025, PANW expects:

- Total revenue of $9.10B – $9.15B, representing YoY growth of 13% – 14%;

- Non-GAAP operating margin of 27.5% – 28.0%;

- Diluted non-GAAP net EPS of $6.18 – $6.31, representing YoY growth of 9% – 11%; and

- Adjusted free cash flow margin of 37% – 38%.

The board authorized an additional $0.5B for share repurchases, increasing the remaining authorization for future share repurchases to $1B, expiring December 31, 2025

Risk Assessment

PANW has no debt, and therefore, no rating agency covers it.

Dividends and Share Repurchases

Dividend and Dividend Yield

PANW does not distribute a dividend.

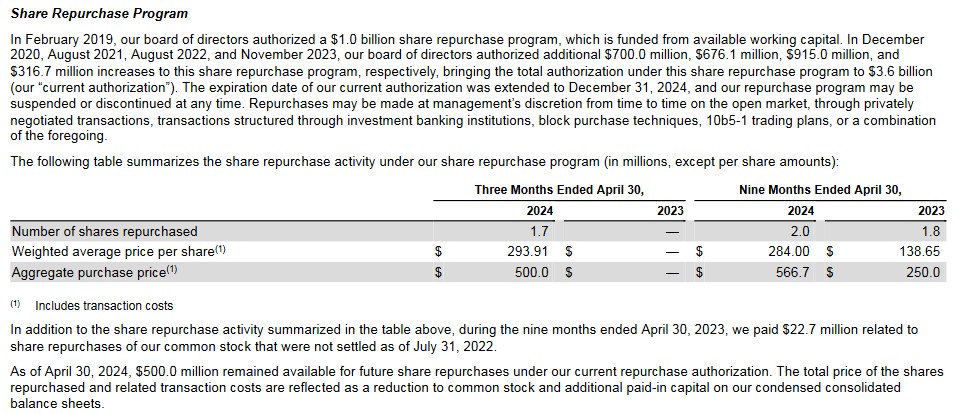

Share Repurchases

PANW’s buyback strategy remains opportunistic and there were no share repurchase in Q4.

The following share repurchase activity is found in the Q3 2024 Form 10-Q.

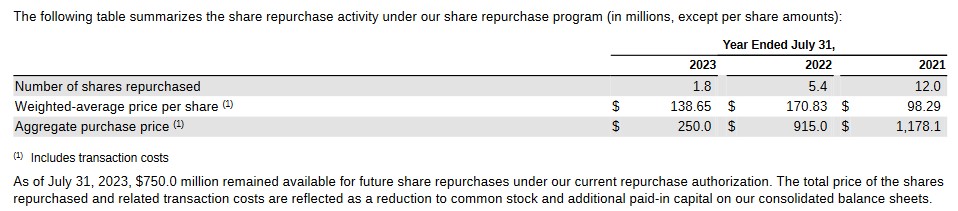

The following share repurchase activity is found in the FY2023 Form 10-K.

In Q4, PANW’s Board authorized an additional $0.5B for share repurchases, increasing the remaining authorization for future share repurchases to $1B, expiring December 31, 2025.

Despite PANW’s share repurchase activity, the weighted average diluted shares outstanding in FY204 rose to ~354 million shares from ~240 million in FY2014.

Valuation

Shares currently trade at ~$368 as I compose this post following the August 20 market close.

The company has just reported FY2024 diluted and adjusted diluted EPS of $7.28 and $5.67; the GAAP EPS reflects $6.04/share of ‘income tax and other tax adjustments’.

With shares trading at ~$368, the diluted PE and adjusted diluted PE are ~50.5 and ~64.9.

Assessing PANW’s valuation using historical results, however, is ill advised since this company is growing rapidly. I also think it is preferable to assess its valuation using FCF as opposed to earnings. We do, nevertheless, need to be cautious when gauging a company’s valuation using a non-GAAP metric because there is no standardization in the calculation of this metric.

In recent years, PANW has had relatively insignificant adjustments to arrive at its adjusted FCF. For my current valuation purposes, I use FCF versus adjusted FCF.

In FY2024, PANW generated $3.101B of FCF.

Using 343.6 million FY2024 diluted Non-GAAP weighted-average shares outstanding that accounts for the weighted-average anti-dilutive impact of note hedge agreements, PANW’s FCF/share is ~$9.03 ($3.101B/343.6 million). Divide ~$368 by ~$9.03 and we get a P/FCF of ~40.8.

Using 354 million FY2024 diluted GAAP weighted-average shares outstanding, PANW’s FCF/share is ~$8.76 ($3.101B/354 million). Divide ~$368 by ~$8.76 and we get a P/FCF of ~42.

PANW’s FY2025 Diluted non-GAAP net EPS outlook is $6.18 – $6.31. Using the current ~$368 share price, the forward adjusted diluted PE is ~58.3 – ~60.

Using adjusted diluted EPS broker estimates, PANW’s forward adjusted diluted PE levels are:

- FY2025 – 47 brokers – ~59 using a mean of $6.26 and low/high of $5.99 – $6.46.

- FY2026 – 42 brokers – ~51.3 using a mean of $7.17 and low/high of $6.05 – $8.43.

- FY2027 – 13 brokers – ~ 42.6 using a mean of $8.62 and low/high of $7.60 – $10.35.

Several broker analysts, whose earnings estimates are included in the above, have yet to updated their estimates. One has not updated its $315 estimate since February, another its $350 estimate since March, 8 ($275 – $350) since May, and 1 ($391.70) since July. Very recently updated estimates range from $330 – $416. This wide range in estimates demonstrates that relying solely on brokers’ estimates is fraught with risk. Furthermore, I have absolutely no idea how anyone can estimate a company’s earnings beyond the current fiscal year. We can use all the fancy formulas developed by academia or the industry but the results all come down to the data plugged into these formulas. This is why I place no reliance on estimates that extend well into the future.

Looking at PANW’s FCF trend over the past few years, I envision ~$3.7B – $3.85B in FY2025. I also think the FY2025 diluted GAAP weighted-average shares outstanding could be 368 million shares. Should these estimates materialize, PANW’s FCF/share would be ~$10.05 – ~$10.46 ($3.7B/368 million and $3.85B/368 million). Divide ~$368 by ~$10.05 and we get a P/FCF of ~36.6. Divide ~$368 by ~$10.46 and we get a P/FCF of ~35.2.

Final Thoughts

In mid-Jul, CrowdStrike’s (CRWD) routine update to its Falcon Sensor software went awry. The resulting ripple effects rapidly reaching across the globe. This prompted me to look into CRWD’s competitors.

I immediately eliminated several companies within the ‘Software – Infrastructure’ industry because their financial metrics did not meet my risk tolerance. PANW, however, piqued my interest. Nevertheless, I chose to wait until the Q4 and FY2024 results and FY2025 outlook were available for review.

My analysis suggests PANW could be a worthwhile long term investment. However, I am concerned that the US equities market is currently much like a casino.

I think PANW’s share price is susceptible to a sharp pullback. The 5 year monthly Beta is ~1.14; Beta measures the risk or volatility of a company’s share price in comparison to the market as a whole. Given a beta of 1.14, we could theoretically see PANW’s stock price increase by 1.14% for every 1% increase in the market or fall 1.14% for every 1% decrease in the market.

Should the broad market experience a 10% correction, PAWN’s share price should theoretically decline 11.4%. An 11.4% drop from $368 should take PANW’s share price down by ~$42 to ~$325.

A 25% tumble would take PANW’s share price to the ~$275 level even though the company’s financial picture is superior to when the share price last hovered around ~$275 for an extended period – share price and financial performance are not necessarily in sync in the short-term.

A retracement to ~$325 seems more plausible than ~$275. If this were to occur, PANW’s P/FCF would be $325/~$10.05 = ~32.3 and $325/~$10.46 = ~31.1. At this level I would consider initiating a position in the FFJ Portfolio. If the share price were to subsequently decline further, I would increase my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I have no exposure to PANW and do not intend to initiate a position within 72 hours

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.