Contents

I last reviewed Lockheed Martin (LMT) in this January 24, 2024 post at which time the most currently available financial information was for Q4 and FY2023. At the time of that post, LMT shares were trading at ~$440 and it was was my 7th largest holdings when I completed my 2023 Year End FFJ Portfolio Review; I hold shares in one of the 'Core' accounts within the FFJ Portfolio.

When I completed my 2024 Mid Year FFJ Portfolio Review, LMT was my 6th largest holding. This review was prepared using the June 28 closing share prices at which time LMT was trading at ~$467.10.

As I compose this post on July 24, LMT's share price is ~$511 and we now have LMT's Q2 and YTD2024 results and revised guidance. Given the ~$71 share price increase since the end of 2023 I take this opportunity to determine the extent to which LMT's valuation has changed.

Business Overview

LMT is a global security and aerospace company that operates in 4 business segments: Aeronautics, Missiles and Fire Control (MFC), Rotary and Mission Systems (RMS) and Space. Its main areas of focus are in defense, space, intelligence, homeland security and information technology, including cybersecurity.

It is engaged in the research, design, development, manufacture, integration and sustainment of advanced technology systems, products and services.

Principal customers are agencies of the U.S. Government, however, it also serves international customers with products and services that have defense, civil and commercial applications.

A good way to learn about a company is to review the company's website and Part 1 Item 1 - Business and Item 1A - Risk Factors in the FY2023 Form 10-K that is accessible through the SEC Filings section of the company's website.

Financials

Q2 and YTD2024 Results

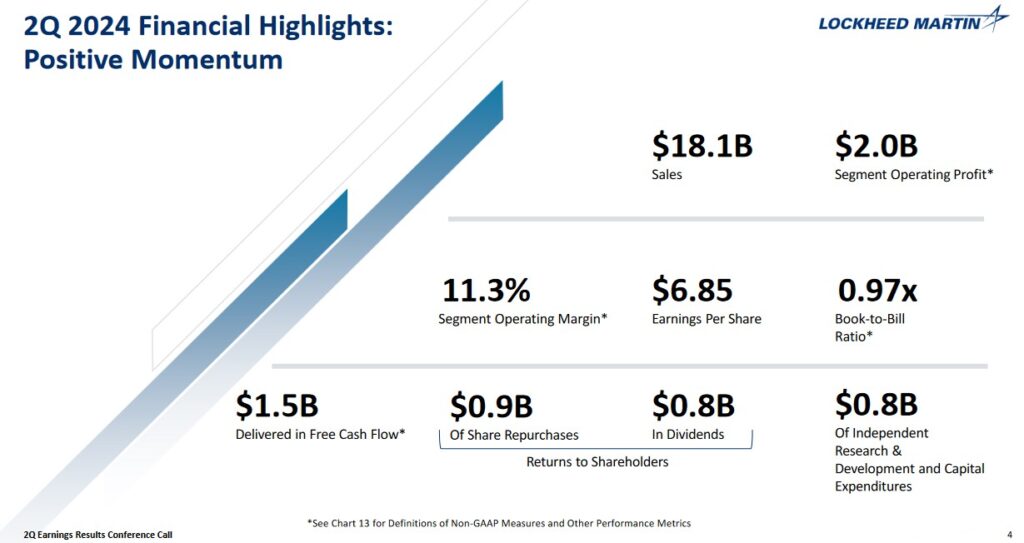

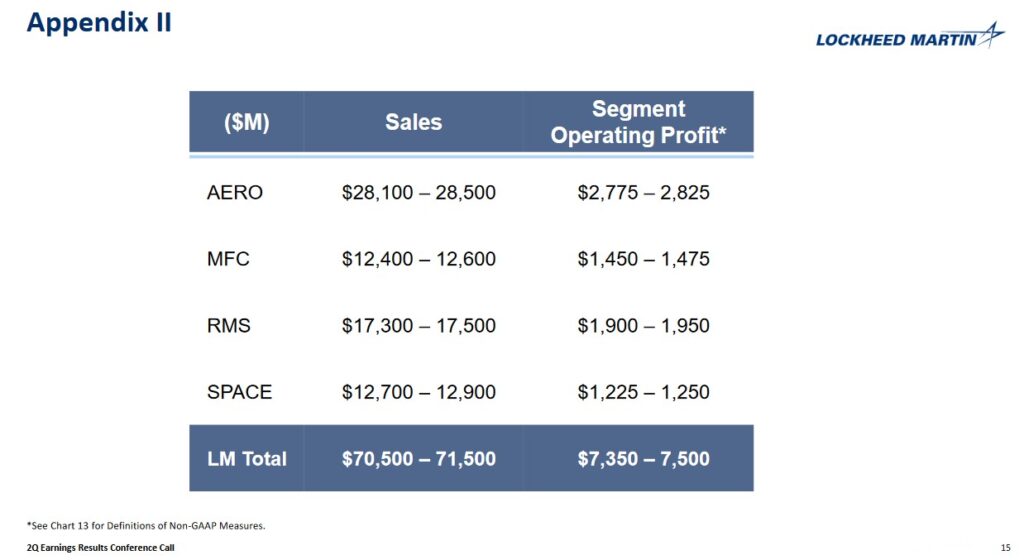

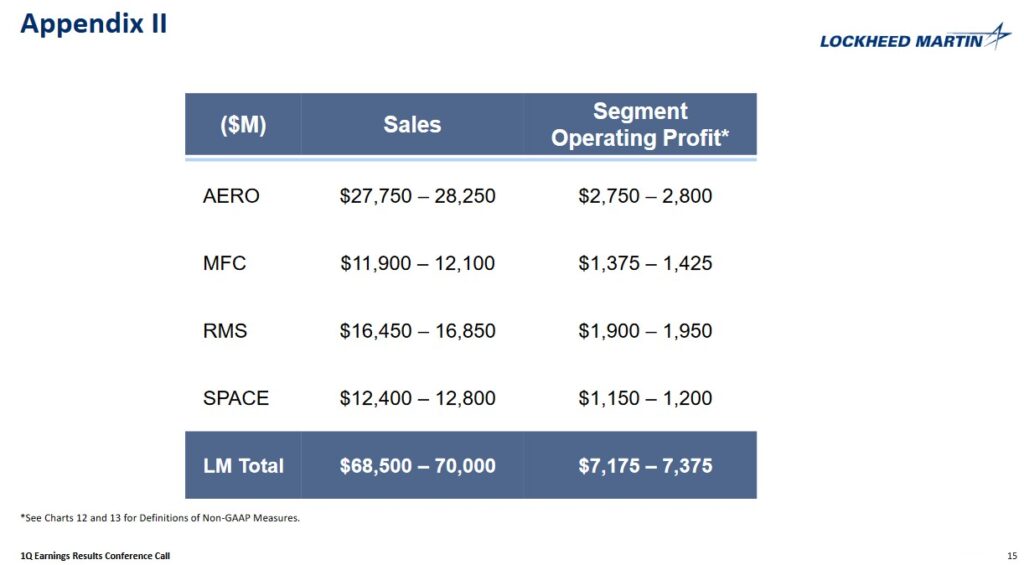

I reference the material available in the Quarterly Results section of LMT's website. The following reflects the Q2 2024 highlights for LMT as a whole. The Q2 2024 Earnings Presentation, however, provides Sales and Operating Profit results for each of LMT's 4 business segments.

In Q2, LMT recorded over $17B of orders for a book-to-bill ratio just below 1.

It generated $1.5B of free cash flow (FCF) in the quarter bringing YTD FCF to ~$2.8B.

LMT consistently makes the necessary investments in innovation and infrastructure and Q2 was no exception with ~$0.405B and ~$0.37B spent on R&D and CAPEX, respectively.

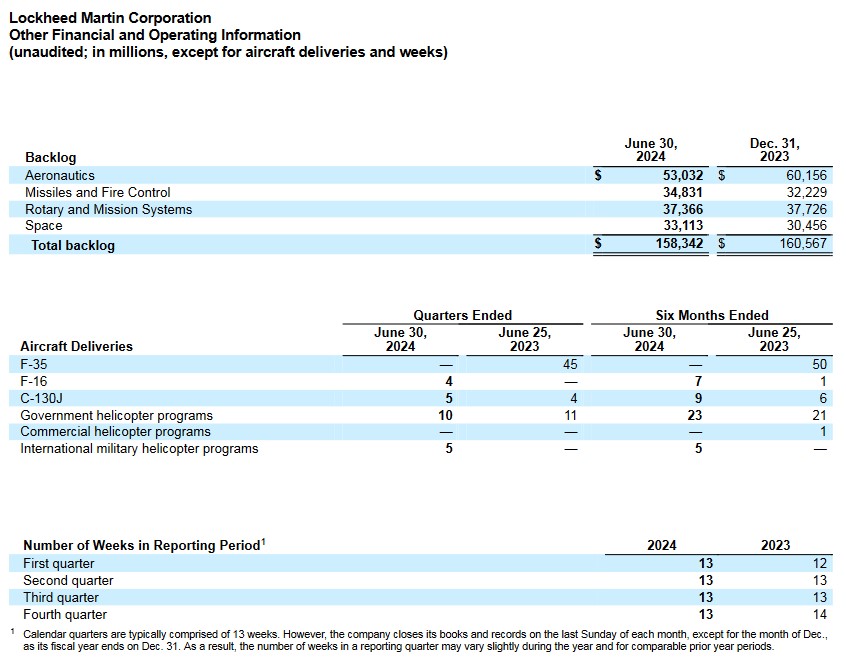

Order Backlog

LMT continues to be awarded significant contracts. The following is LMT's order backlog at recent FYEs (expressed in $B).

- 2017 $105.5

- 2018 $130.5

- 2019 $144

- 2020 $147

- 2021 $135.4

- 2022 $150

- 2023 $160.6

Looking at LMT's aircraft deliveries we see that F-35 deliveries have fallen off the map in the current fiscal year; the backlog and deliveries in Q4 2022 and 2023 and FY2022 and FY2023 are provided below for comparison.

In the FY2023 Annual Report from the Director, Operational Test & Evaluation, an entire section of this report is devoted to the F-35 Joint Strike Fighter (JSF) program (commences on page 52 of 446).

This report notes that the US fleet of F-35 fighters suffered from reliability, maintainability, and availability problems with the fighters being available for operations only 51% of the time compared to a goal of 65%.

LMT paused all deliveries to focus on rectifying the issues leading to substandard performance which explains no deliveries of its signature product in several months.

Fortunately, the issues have been rectified and in early Q3 2024, LMT commenced delivery of the first Technology Refresh 3 (TR3) configured F-35 aircraft to the U.S. government. The TR3 upgrade and further Block IV enhancements represent a critical evolution in capability and their full development remains LMT's top priority.

Despite the higher sales outlook, LMT expects its backlog to grow. It is continuing to produce 156 aircraft per year, expects to deliver 75 - 100 aircraft in the second half of 2024, and also expects deliveries of F-35 aircraft to exceed production for the next few years.

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

In the FY2014 - FY2023 time frame, LMT's:

- OCF was (in B$) 3.866, 5.101, 5.189, 6.476, 3.138, 7.311, 8.183, 9.221, 7.802, and 7.920.

- CAPEX was (in B$) 0.845, 0.939, 1.063, 1.177, 1.278, 1.484, 1.766, 1.522, 1.670, and 1.691.

- FCF was (in B$) 3.021, 4.162, 4.126, 5.299, 1.860, 5.827, 6.417, 7.699, 6.132, and 6.229.

The Q2 2024 Consolidated Statement of Cash Flows reflects YTD ~$3.511B of OCF, ~$0.748B of CAPEX thus giving us ~$2.763B of FCF.

Return On Invested Capital (ROIC)

LMT's ROIC (%) in FY2014 - FY2023 is 37.28, 27.17, 35.01, 15.89, 38.68, 43.43, 43.14, 33.27, 26.48, and 31.34.

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company's cost of capital will be lower than this level. LMT's ROIC often exceeds this level.

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

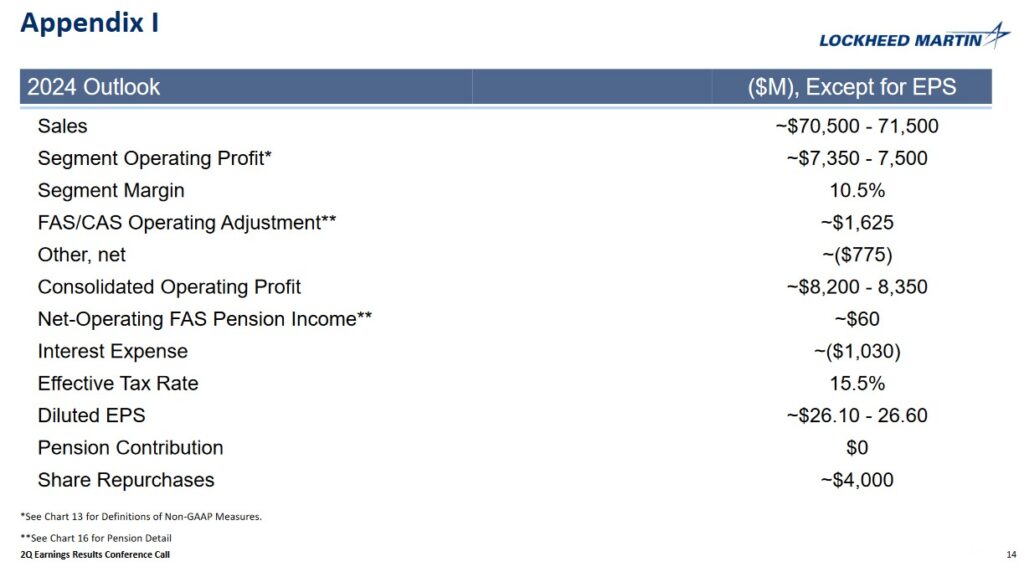

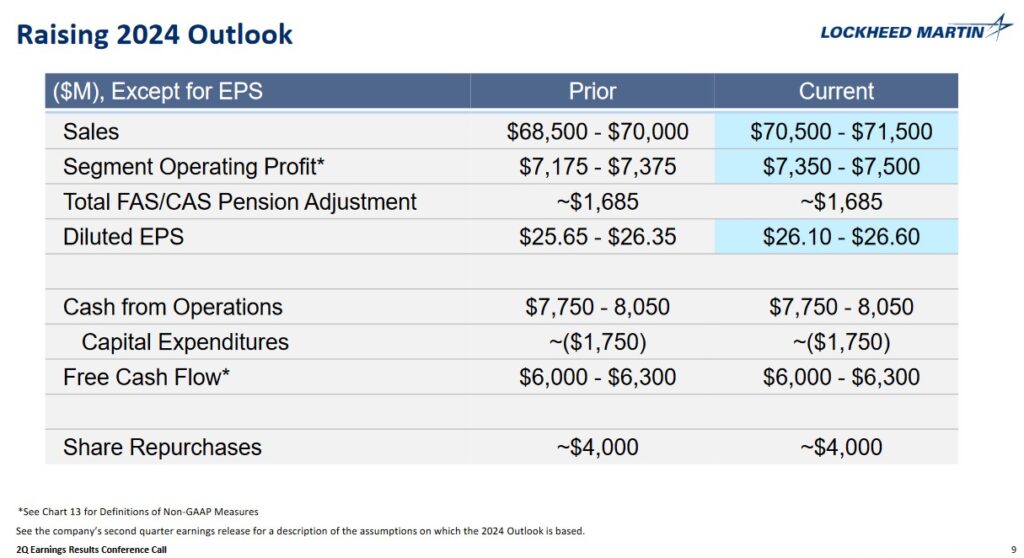

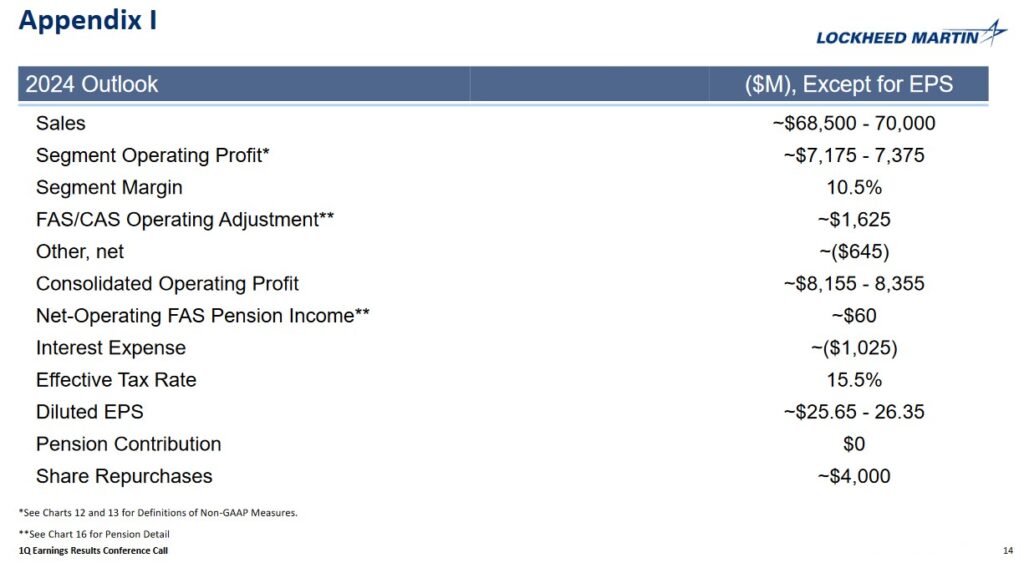

FY2024 Outlook

This is LMT's current FY2024 outlook.

The changes from the prior outlook are highlighted below.

The outlook provided with the release of Q1 2024 results is provided below for comparison. This outlook was identical to that provided when it released its Q4 and FY2023 results in January 2024.

Credit Ratings

LMT's senior unsecured domestic currency debt ratings are:

- Moody's: A2 (upgrade from A3 on August 14, 2023)

- S&P Global: A- (assigned on May 2 2019 and currently assigns a stable outlook)

- Fitch: A (upgrade from A- on June 3, 2024)

The rating assigned by S&P Global is the lowest tier of the upper-medium investment grade level; the rating assigned by Moody's and Fitch is one tier higher.

All 3 ratings define LMT as having a STRONG capacity to meet its financial commitments. LMT is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Dividend and Dividend Yield

As noted in several previous posts, dividend metrics are irrelevant in my investment decision making process. Nevertheless, I include a section about a company's dividend in every post since I know many followers have an interest in these metrics.

LMT has increased its dividend for 22 consecutive years; its dividend history is accessible here.

On September 27 it will distribute its 4th consecutive $3.15 quarterly dividend. I envision LMT will increase the quarterly dividend from $3.15 to at least $3.30 in October. Should this materialize, the total value of the 4 quarterly dividend payments subsequent to the disbursement of the September dividend would be $13.20 ($3.30 x 4)). Using the current ~$511 share price as I compose this post on July 24, the forward dividend yield is ~2.6%.

The following are LMT's approximate dividend yields at the time of prior reviews.

- January 25, 2022: shares were trading at ~$380 - the $2.80 quarterly dividend yielded ~3%.

- April 19, 2022: shares were trading at ~$460 - the $2.80 quarterly dividend yielded ~2.4%.

- July 19, 2022: shares were trading at ~$390 - the $2.80 quarterly dividend yielded ~2.9%.

- October 18, 2022: shares were trading at ~$432 - the $3.00 quarterly dividend yielded ~2.78%.

- January 25, 2023: shares were trading at ~$452.50 - the $3.00 quarterly dividend yielded ~2.65%.

- April 18, 2023: shares were trading at ~$501.50 - the $3.00 quarterly dividend yielded ~2.40%.

- July 18, 2023: shares were trading at ~$455.70 - the $3.00 quarterly dividend yielded ~2.63%.

- September 7, 2023: shares were trading at ~$430 - the $3.00 quarterly dividend yielded ~2.8%.

- October 18, 2023: shares were trading at ~$446 - the $3.15 quarterly dividend yielded ~2.83%.

- January 24, 2024: shares were trading at ~$440 - the $3.15 quarterly dividend yielded ~2.86%.

LMT is a prolific acquirer of its shares as borne out by the reduction in the weighted average number of issued and outstanding shares in FY2011 - FY2023 (in millions rounded): 340, 328, 327, 322, 315, 303, 291, 287, 284, 281, 277.4, 264.6, and 251.2. The weighted average in Q2 2024 is 239.6.

In FY2023, LMT repurchased $6B of its issued and outstanding shares.

During the six months ending June 30, 2024, LMT repurchased 4.2 million shares of its common stock for ~$1.9B in open market purchases; the FY2024 outlook includes the repurchase of $4B of outstanding shares.

The total remaining authorization for future common stock repurchases under its share repurchase program was $8.2B as of June 30, 2024.

Valuation

In FY2013 - FY2022, LMT's diluted PE levels were 16.02, 19.47, 19.27, 18.81, 26.04, 24.80, 18.51, 15.16, 16.38, and 22.37. When I composed my September 7, 2023 post, I used the following forward-adjusted diluted earnings broker estimates and my ~$430 purchase price:

- FY2023 - 22 brokers - mean of $27.14 and low/high of $26.76 - $27.46. Using the current mean, the forward adjusted diluted PE was ~15.84.

- FY2024 - 23 brokers - mean of $28.10 and low/high of $27.16 - $28.75. Using the current mean, the forward adjusted diluted PE was~15.3.

- FY2025 - 18 brokers - mean of $29.05 and low/high of $26.74 - $31.25. Using the current mean, the forward adjusted diluted PE was ~14.8.

Although LMT's FY2023 adjusted diluted EPS forecast was $27.00 - $27.20, I looked at LMT's valuation if it were to only generate adjusted diluted EPS of $26.50 in FY2023. Using this estimate, I determined the forward adjusted diluted PE would be ~16.23. When I composed my October 18, 2023 post, LMT shares were trading at ~$446. Its valuation using this share price and the currently available forward-adjusted diluted earnings broker estimates was:

- FY2023 - 22 brokers - mean of $27.24 and low/high of $27.00 - $28.00. Using the current mean, the forward adjusted diluted PE was ~16.4.

- FY2024 - 22 brokers - mean of $27.23 and low/high of $25.26 - $28.96. Using the current mean, the forward adjusted diluted PE was ~16.4.

- FY2025 - 19 brokers - mean of $28.74 and low/high of $24.97 - $31.19. Using the current mean, the forward adjusted diluted PE was ~15.5.

I concluded that LMT was slightly undervalued. When I completed my Januayr 24, 2024 post, LMT had reported FY2023 diluted EPS of $27.55 and adjusted diluted EPS of $27.82. Using the ~$440 closing share price on January 23, the diluted PE and adjusted diluted PE levels were ~16 and ~15.8. The company's FY2024 adjusted diluted EPS outlook was $25.65 - $26.35 thus giving us a forward adjusted diluted PE range of ~16.7 and ~17.2. Its valuation using the ~$440 share price and the current broker forward-adjusted diluted earnings estimates were:

- FY2024 - 22 brokers - mean of $26.46 and low/high of $25.68 - $28.50. Using the current mean, the forward adjusted diluted PE is ~16.

- FY2025 - 18 brokers - mean of $28.14 and low/high of $26.02 - $29.53. Using the current mean, the forward adjusted diluted PE is ~15.6.

- FY2026 - 10 brokers - mean of $29.03 and low/high of $26.61 - $31.20. Using the current mean, the forward adjusted diluted PE is ~15.2.

Shares currently trade at ~$511 and the adjusted diluted EPS outlook for FY2024 is $26.10 - $26.60 thus giving us a forward adjusted diluted PE range of ~19.21 - ~19.58. Using the ~$511 share price and the current broker forward-adjusted diluted earnings estimates we get:

- FY2024 - 22 brokers - mean of $26.31 and low/high of $25.76 - $26.98. Using the current mean, the forward adjusted diluted PE is ~19.4.

- FY2025 - 22 brokers - mean of $28.09 and low/high of $26.70 - $29.12. Using the current mean, the forward adjusted diluted PE is ~18.2.

- FY2026 - 16 brokers - mean of $29.90 and low/high of $26.78 - $31.30. Using the current mean, the forward adjusted diluted PE is ~17.1.

LMT's FY2024 outlook includes $6B - $6.3B of FCF. If it continues to repurchase shares as planned, the weighted average diluted outstanding shares in FY2024 should be ~239.6 million. This gives us a FCF/share range of ~$25 - ~$26.3. With shares trading at ~$511, the forward P/FCF is ~19.4 - ~20.4. LMT's P/FCF in FY2014 - FY2023 is 12.46, 19.49, 13.17, 16.48, 30.94, 13.78, 12.72, 14.67, 12.89, and 15.40.

Final Thoughts

LMT was undervalued for the majority of the last several years with the exception of a brief period in late 2022 - mid 2023; I was buying when shares were, in my opinion, deeply undervalued in 2020 - 2021.

Now? I am not interested. There is too much irrational exuberance.

I currently hold 565 shares in a 'Core' account in the FFJ Portfolio at an average cost of ~$378.38 and am merely automatically reinvesting the dividend income.

Based on LMT's FY2024 adjusted diluted EPS outlook of $26.10 - $26.60 and a more reasonable adjusted diluted PE level of ~17, I would want the share price to retrace to ~$450 or less.

Using my forecast FCF/share range of ~$25 - ~$26.3, a ~$450 share price would give us a P/FCF range of ~17 - ~18.

I remain cautious in this environment and have raised liquidity in the hope that I will be able to acquire shares in companies that appeal to me at more favorable valuations. LMT is one such company.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to [email protected].

Disclosure: I am long LMT.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.