Contents

I last reviewed Lockheed Martin (LMT) in this January 24 , 2024 post at which time the most currently available financial information was for Q4 and FY2023. With the release of Q1 results and a revised FY2024 outlook on April 23, I revisit this existing holding.

Business Overview

Global conflict benefits LMT because its largest client, the US Government, has the world's largest military budget. Its defense budget that is more than 2.5 times larger than that of China, the second largest military budget.

In FY2023, LMT derived ~75% of its $67.6B 2023 sales by servicing contracts from the US Department of Defense (DoD).

The very nature of LMT's products is such that switching costs are prohibitive. If a country is using F-35 military aircraft, for example, it can not quickly/easily transition to something else; the F-35 defense procurement program is the largest the DoD has ever awarded and this program is expected to continue until the 2060s.

In addition to having to meet its obligations under existing long-term contracts, LMT continues to win new contracts (see Recent Contract Wins below). The bidding process is a drawn out and costly process. However, when LMT is awarded a sizable contract, it is generally for a period of several years.

The approved 2024 US defense budget is a huge positive for LMT. Included in the budget are:

- significant funding for munitions multiyear procurement;

- continued investment in hypersonics; and

- classified activities and ongoing support for programs such as Black Hawk, CH-53K heavy lift helicopter, the fleet ballistic missile, C-130 and F-35.

Furthermore, there are additions to the original budget submission, including F-35 aircraft, C-130s and combat rescue helicopters.

The initial budget request for FY2025 is still very early in the process but it includes continued support of many existing major programs. These include the F-35, CH-53K, UH-60M and others as well as emphasis on advanced munitions programs such as JASSM and LRASM, PrSM, Javelin, GMLRS and PAC-3 as well as hypersonic conventional prompt strike and the long-range hypersonic weapon. The next-generation Interceptor is also receiving support.

Most recently, $95B of funding for Ukraine, Israel and Indo-Pacific security passed the House and is currently under consideration in the Senate.

I recommend you review LMT's website. In addition, Part 1 of the 2023 Form 10-K and the 2024 Proxy Statement (accessible here) provide a wealth of information.

The Risk Factors section within LMT's Form 10-K provides a good overview of various risks that could impact its business, financial condition, operating results and cash flows.

Recent Contract Wins

While the United States DoD is not LMT's sole customer, it is its largest customer.

The United States has the world's largest military budget (military spending by country is accessible here). Since LMT is a dominant aerospace and defense industry participant, it is inevitable that it will have a robust order pipeline.

Within the past month, LMT was awarded the following two sizable contracts.

$17.7B US missile defense contract

LMT has been awarded a multi-year ~$17.7B contract to develop the next generation of interceptors to defend the US against an intercontinental ballistic missile attack. This contract covers the development of the Next Generation Interceptor (NGI) to modernize the Ground-Based Midcourse Defense (GMD) program.

These interceptors are aimed at defeating current ballistic missile threats and future technological advances from countries such as Russia, North Korea, and Iran.

The first interceptor is expected to be operational in 2028.

$4.1B battle command system contract

The Missile Defense Agency has awarded LMT an indefinite-delivery/indefinite-quantity contract with a maximum ceiling of ~$4.1B to accelerate innovation and continue leading the development of the Command and Control, Battle Management and Communications (C2BMC) system.

The ordering period is from May 1, 2024 through April 30, 2029, with an option to extend through April 30 2034.

Financials

Q1 2024 Results

I reference the material available in the Quarterly Results section of LMT's website.

First quarter sales of $17.2B increased ~14% YoY. The results benefited from an extra calendar week compared to 2023 but normalized YoY sales growth was still 5%.

The supply chain challenges experienced in prior quarters are slowly being eliminated. LMT continues to work closely with its supply chain partners to enhance quality and performance proactively and, as needed, expand the breadth and depth of its engagement at supplier locations.

The following is a very high level recap of LMT's Q1 2024 results.

GAAP EPS of $6.39 was down 3% as YoY benefits from higher profit and lower share count were more than offset by higher interest expense, lower pension income and mark-to-market gains.

In Q1, LMT generated $1.3B of free cash flow (FCF) after investing $0.36B in R&D and ~$0.38B in capital expenditures.

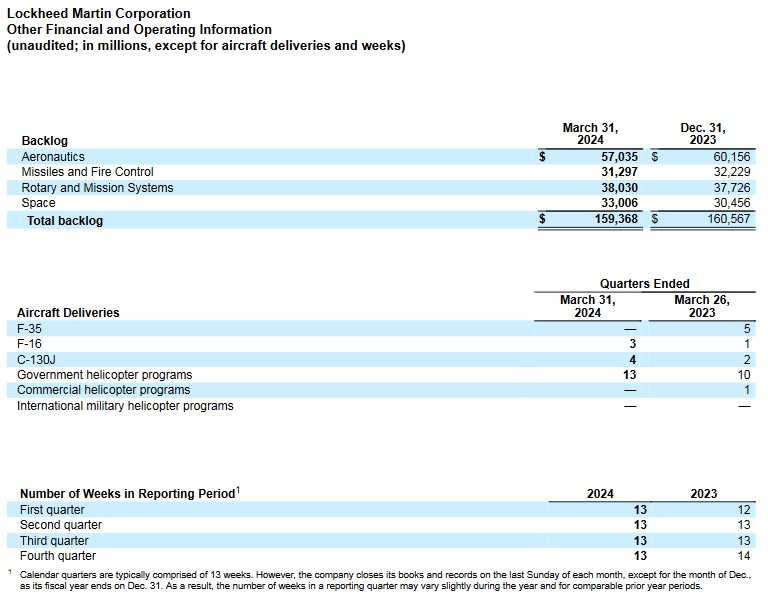

Order Backlog

LMT continues to be awarded significant contracts and its FYE2023 order backlog is the highest in the company's history. The following is LMT's order backlog at recent FYEs (expressed in $B).

- 2017 $105.5

- 2018 $130.5

- 2019 $144

- 2020 $147

- 2021 $135.4

- 2022 $150

- 2023 $160.6

The following reflects the order backlog in Q4 2023 and Q1 2024 and the aircraft deliveries in Q1 2023 and Q1 2024.

NOTE: There is one extra week in the Q1 2024 reporting period relative to Q1 2023. There will, however, be one week less in the Q4 2024 reporting period relative to Q4 2023.

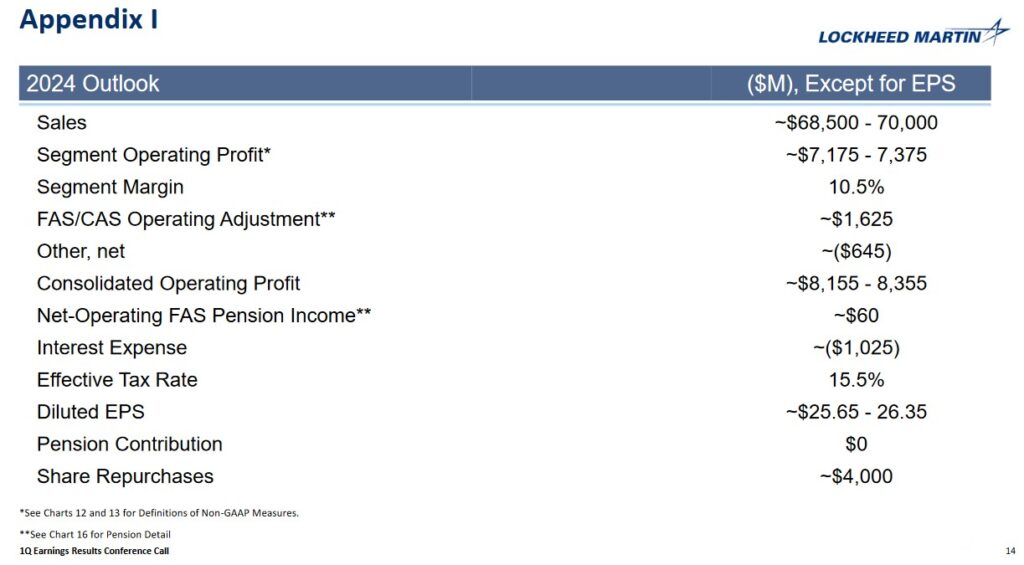

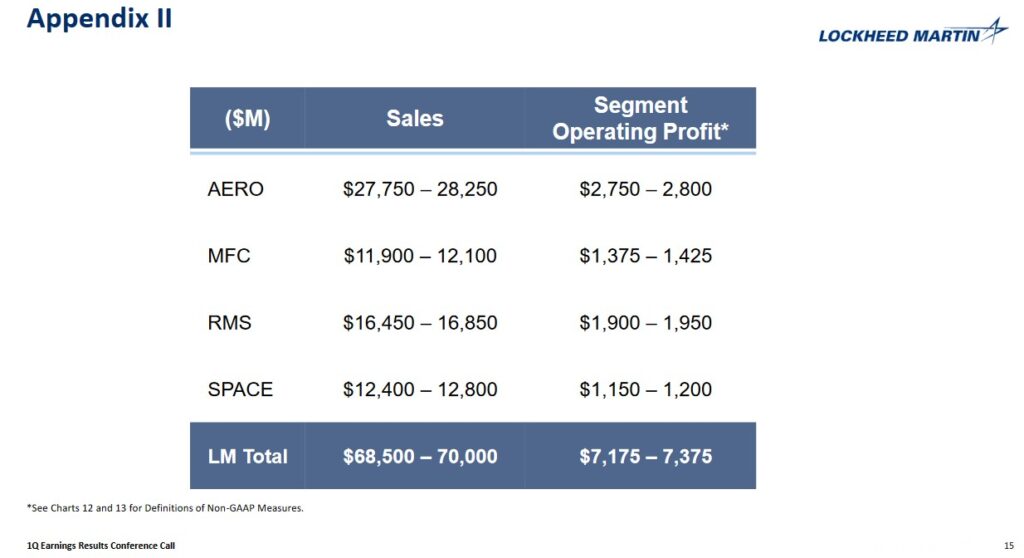

FY2024 Outlook

There is no change to LMT's FY2024 outlook from that presented when FY2023 results were released on January 23.

LMT's FY2024 consolidated operating profit margin (GAAP) outlook of 11.9% is lower than what it achieved in recent years:

- 2017 13.5%

- 2018 13.6%

- 2019 14.3%

- 2020 13.2%

- 2021 13.6%

- 2022 12.7%

- 2023 12.6%

Its FY2024 business segment operating profit margin (non-GAAP) outlook of 10.5% is also lower than what it achieved in recent years with the exception of FY2017:

- 2017 10.2%

- 2018 10.9%

- 2019 11.0%

- 2020 10.9%

- 2021 11.0%

- 2022 11.3%

- 2023 10.9%

Credit Ratings

LMT's senior unsecured domestic currency debt ratings are:

- Moody's: A2 (stable outlook)

- S&P Global: A- (stable outlook)

- Fitch: A- (stable outlook)

The ratings from S&P Global and Fitch are the lowest tier of the upper-medium investment grade level; the rating assigned by Moody's is one tier higher.

All 3 ratings define LMT as having a STRONG capacity to meet its financial commitments. LMT is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Dividend and Dividend Yield

LMT's dividend history is accessible here.

Within the next few days, LMT will declare its third consecutive $3.15/share quarterly dividend.

I envision LMT will increase the quarterly dividend from $3.15 to at least $3.30 in October. Should this materialize, the total value of the 4 quarterly dividend payments subsequent to the declaration of the imminent third $3.15 quarterly dividend, will amount to $13.05 (($3.15 x 1) + ($3.30 x 3)). Using the ~$460 closing share price on April 23, the forward dividend yield is ~2.8%.

LMT is a prolific acquirer of its shares as borne out by the reduction in the weighted average number of issued and outstanding shares in FY2011 - FY2023 (in millions rounded): 340, 328, 327, 322, 315, 303, 291, 287, 284, 281, 277.4, 264.6, and 251.2. The weighted average number of outstanding common shares in Q1 2024 was 241.6.

In Q1, LMT repurchased 2.3 million shares for $1B in open market purchases. The total remaining authorization for future common stock repurchases under the share repurchase program was $9B as of March 31, 2024.

The FY2024 outlook calls for the repurchase of another ~$3B as LMT continues to focus on returns to shareholders.

Valuation

In FY2013 - FY2023, LMT's diluted PE levels were 16.02, 19.47, 19.27, 18.81, 26.04, 24.80, 18.51, 15.16, 16.38, 22.37, and 16.59.

When I composed my September 6 post, I used the forward-adjusted diluted earnings estimates from the brokers which cover LMT and my ~$430 purchase price:

- FY2023 - 22 brokers - mean of $27.14 and low/high of $26.76 - $27.46. Using the current mean, the forward adjusted diluted PE was ~15.84.

- FY2024 - 23 brokers - mean of $28.10 and low/high of $27.16 - $28.75. Using the current mean, the forward adjusted diluted PE was~15.3.

- FY2025 - 18 brokers - mean of $29.05 and low/high of $26.74 - $31.25. Using the current mean, the forward adjusted diluted PE was ~14.8.

Although LMT's FY2023 adjusted diluted EPS forecast was $27.00 - $27.20, I looked at LMT's valuation if it were to only generate adjusted diluted EPS of $26.50 in FY2023. Using this estimate, I determined the forward adjusted diluted PE would be ~16.23.

When I composed my October 18 post, LMT shares were trading at ~$446. Its valuation using this share price and the currently available forward-adjusted diluted earnings estimates from the brokers which cover LMT was:

- FY2023 - 22 brokers - mean of $27.24 and low/high of $27.00 - $28.00. Using the current mean, the forward adjusted diluted PE was ~16.4.

- FY2024 - 22 brokers - mean of $27.23 and low/high of $25.26 - $28.96. Using the current mean, the forward adjusted diluted PE was ~16.4.

- FY2025 - 19 brokers - mean of $28.74 and low/high of $24.97 - $31.19. Using the current mean, the forward adjusted diluted PE was ~15.5.

I concluded that LMT was slightly undervalued.

At the time of my January 24 post, LMT had just reported FY2023 diluted EPS of $27.55 and adjusted diluted EPS of $27.82. With shares trading at ~$440 on January 23, the diluted PE and adjusted diluted PE levels were ~16 and ~15.8.

The company's FY2024 adjusted diluted EPS outlook was currently $25.65 - $26.35 thus giving us a forward adjusted diluted PE range of ~16.7 and ~17.2.

Its valuation using the ~$440 share price and the current broker forward-adjusted diluted earnings estimates were:

- FY2024 - 22 brokers - mean of $26.46 and low/high of $25.68 - $28.50. Using the current mean, the forward adjusted diluted PE was ~16.

- FY2025 - 18 brokers - mean of $28.14 and low/high of $26.02 - $29.53. Using the current mean, the forward adjusted diluted PE was ~15.6.

- FY2026 - 10 brokers - mean of $29.03 and low/high of $26.61 - $31.20. Using the current mean, the forward adjusted diluted PE was ~15.2.

With shares trading at ~$460 and no change to LMT's FY2024 adjusted diluted EPS outlook of $25.65 - $26.35, the current forward adjusted diluted PE range is ~17.5 - ~18.

The following reflects LMT's valuation using a ~$460 share price and the current broker forward-adjusted diluted earnings estimates.

- FY2024 - 21 brokers - mean of $26.10 and low/high of $25.57 - $26.63. Using the current mean, the forward adjusted diluted PE is ~17.6.

- FY2025 - 21 brokers - mean of $27.77 and low/high of $26.21 - $28.90. Using the current mean, the forward adjusted diluted PE is ~16.6.

- FY2026 - 12 brokers - mean of $29.47 and low/high of $26.64 - $31.40. Using the current mean, the forward adjusted diluted PE is ~15.6.

Lookin at LMT's valuation from a FCF perspective, let's assume LMT repurchases 2.3 million shares for $1B in open market purchases as it did in Q1 in each of the next 3 quarters. This would amount to 6.9 million shares.

LMT will undoubtedly issue additional shares as part of its stock based compensation arrangements so let's suppose it reduces the 241.6 million weighted average number of outstanding common shares outstanding in Q1 2024 by 6.8 million shares thereby giving us 234.8 million FY2024 weighted average shares outstanding.

The FY2024 FCF outlook is $6B - $6.3B. Divide the $6.15B mid point by 234.8 million shares and we get FCF/share of ~$26.2. Divided the current ~$460 share price by ~$26.2 and we get a forward P/FCF of ~17.56. LMT's P/FCF in FY2014 - FY2023 was 12.46, 19.49, 13.17, 16.48, 30.94, 13.78, 12.72, 14.67, 12.89, and 15.40. My rough calculation of the ~17.56 forward P/FCF is greater than recent historical levels other than in FY2015 and FY2018.

Final Thoughts

Global conflict benefits LMT and it should continue to benefit from foreseeable increases in US defense spending. In the short term, for example, LMT benefits from orders to resupply munitions to Ukraine; these munitions are being expended faster than they can be produced.

In the long term, the US is prioritizing modernization of the US military's ability to counter aggression from China and Russia and terrorism threats from countries such as North Korea and Iran.

This is one of the primary reasons LMT was my 7th largest holdings when I completed my 2023 Year End FFJ Portfolio Review; I hold shares in one of the 'Core' accounts within the FFJ Portfolio.

As noted in prior posts, the ability to generate an attractive total investment return depends heavily on the entry point. The acquisition of fairly valued or overvalued shares reduces the probability of generating an attractive rate of return diminishes, and therefore, current market conditions have made it exceedingly difficult for me to identify companies in which I am prepared to deploy fresh capital.

When I analyzed LMT in my January 24 post, I considered shares to be slightly undervalued. With no change in the FY2024 outlook and a ~$14 higher share price from the time of my last review, I now view shares as being fairly valued and do not intend to immediately acquire additional shares. If the share price were to retrace to ~$430, LMT's valuation based on FY2024 forward adjusted diluted EPS and forward FCF would be ~16.5 which I consider somewhat more reasonable.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to [email protected].

Disclosure: I am long LMT.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.