Contents

There is no disputing that Nike (NKE) has experienced its fair share of challenges in recent years. Soft demand for sportswear in key markets and an increasingly competitive industry has resulted in lacklustre top line growth. In FY2020 and FY2024, for example, NKE reported a decline in YoY sales growth. On the Q4 2024 earnings call, management once again warned of a very challenging demand environment for sportswear. The current FY2025 reported revenue outlook even calls for a mid-single digits decline with the first half of FY2025 expected to be down high single digits.

Following the release of the Q4 and FY2024 earnings after the June 27 market close, the share price plunged ~20% on June 28.

NKE's persistent sales weakness is creating uncertainty in the company's turnaround efforts. Why some investors may be reluctant to invest in it is understandable. I, however, think NKE stands to benefit over the next few years from its planned marketing and product initiatives and the growth of the global market. I, therefore, view NKE's current share price weakness and attractive valuation as a buying opportunity.

When I last reviewed NKE in my March 23, 2024 post, I viewed the near term challenges as a buying opportunity. In this post I touch upon why I have increased my NKE exposure following the share price plunge.

Business Overview

The best resource from which to learn about NKE is Part 1 Item 1 - Business in the FY2023 Form 10-K. This section provides a general overview of the company, its products, and markets amongst other pertinent information. I also strongly encourage a review of Item 1A – Risk Factors in the Form 10-K.

Financials

Q4 and FY2024 Results

The most recent results are accessible here.

NKE has certainly felt the impact of inflation, currency volatility, logistical challenges, and conflict in Ukraine. These issues are likely to persist, and therefore, a dramatic turnaround in its results is unlikely to occur in the short term.

China is its 3rd largest market after North America and Europe, Middle East & Africa. This market is becoming increasingly competitive as nationalism is boosting native brands (much like the automotive sector).

Economic headwinds and political controversy are also negatively impacting NKE's performance in China. Many Chinese citizens have chosen to 'lie flat', a term used to describe a personal rejection of societal pressures to overwork and over-achieve. The twelve hour workday 6 days a week system is now often regarded as a rat race with ever diminishing returns.

While the current unemployment rates in urban China are reported as being in the 5% - 6% range, unofficial unemployment rates paint are far gloomier picture. Unofficial ('boots on the streets') statistics suggest China’s unemployment rate for 16 - 24-year-olds exceeds 20%. This embarrassing statistic likely explains why the Chinese central government has stopped publishing employment/unemployment data that excludes young people seeking jobs while studying.

In 2024, China reported a record high of 11.79 million college graduates. Due to the economic circumstances in China, many graduates are unable to find employment. In many instances, they may find employment but the jobs might be 'gig' work.

A number of manufacturers are also relocating their operations to other regions in Asia where the cost of labor is far lower than in China.

The Chinese real estate market is also in shambles. The real estate market in China is very different from that in North America. A citizen requiring financing to assist in the purchase of pre-construction real estate, obtains a mortgage BEFORE acquiring ownership of the property. In essence, the borrower starts making mortgage payments BEFORE the property is ready for occupancy.

A contributor to the implosion of the Chinese real estate values is that once a property reaches a certain percentage of completion, the developers receive the sale proceeds that are held in escrow. While these proceeds should be deployed toward the completion of property #1, developers often divert funds toward the start of property #2. This often leads to the developer having insufficient funds to properly complete property #1. In many cases, properties are uninhabitable yet the purchasers are required to make regular mortgage payments.

Given the financial crisis many Chinese citizens are facing, it is not surprising to see videos of desolate urban areas that were once bustling with activity.

China is not the only region where consumers are cash strapped. In my recent Alimentation Couche-Tard – Headwinds To Persist post, I noted that ATD is experiencing weak same store sales in North America because the financial state of its customer base is deteriorating.

As if the aforementioned headwinds are not enough! NKE also has to contend with relatively newer footwear brands (eg. Hoka and On) that are challenging its dominance.

NKE's management is acutely aware of these challenges and has a strategy to double innovation, speed, and direct connections to consumers. Its plan includes cutting product creation times in half, increasing membership in its mobile apps, and improving the selection of key franchises while reducing the number of styles by 25%.

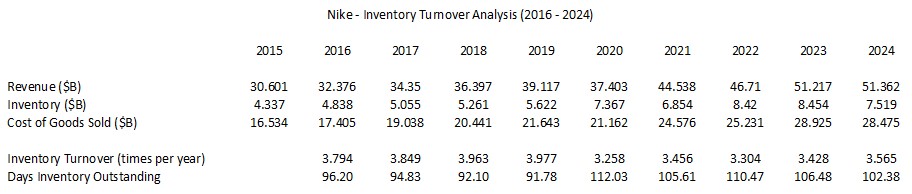

Another issue is NKE's bloated inventory levels which I have touched upon in my previous post; the following table reflects NKE's inventory metrics over the past few fiscal years.

The onset of COVID-2019 led to logistics issues which contributed to NKE's 'days inventory outstanding' ballooning from under 92 days in 2019 to 112 days in 2020.

In FY2024, inventory declined ~11% versus the prior year with continued improvement in days inventory outstanding. Despite a ~$0.935 reduction inventory from the FY2023 level, however, there is no rationale for an inventory level in excess of $7B if FY2025 revenue projections call for a mid single digit decline from FY2024.

If the steps being taken to 'right size' inventory levels are successful, this should greatly contribute to NKE's cash generated from operations.

The changes from Q3 to FYE2024 in other Balance Sheet line items are not alarming.

Operating Cash Flow (OCF) and Free Cash Flow (FCF)

In FY2012 - FY2023, NKE generated (in billions of $) 1.824, 3.032, 3.013, 4.680, 3.399, 3,846, 4.955, 5.903, 2.485, 6.657, 5.188, and 5.841 of OCF. In the first 3 quarters of FY2024 it generated 4.81.

During the same time frame, it generated (in billions of $) $1.261B, $2.434B, $2.133B, $3.717B, $2.256B, $2.741B, $3.927B, $4.784B, $1.399B, $5.962B, $4.43B, and $4.872B of FCF. In the first 3 quarters of FY2024 it generated 4.211.

The FY2024 Form 10-K is currently unavailable but it is not out of the realm of possibility that NKE generated another $1B of FCF in Q4. If this did materialize, NKE will have generated ~$5.21B of FCF in FY2024 which is the second highest level of FCF in the company's history.

FY2025 Guidance

On the Q4 earnings call, management stated:

We are managing a product cycle transition with complexity amplified by shifting channel mix dynamics. A comeback at this scale takes time. With this in mind, we've considered a number of factors and scenarios in revising our outlook for fiscal '25. Most importantly, this includes time lines and pacing to manage marketplace supply of our classic footwear franchises; lower NIKE Digital growth, especially in the first half of the year due to lower traffic on fewer launches, planned declines of classic footwear franchises given Q4 trends as well as reduced promotional activity; increased macro uncertainty, particularly in Greater China, with uneven consumer trends continuing in EMEA and other markets around the world; and sell into wholesale partners as we scale product innovation and newness across the marketplace and finalize second half order books. Taking all of this into consideration, we now expect fiscal '25 reported revenue to be down mid-single digits with the first half down high single digits.

In addition, FX headwinds have worsened and will now have a very marginal impact on FY2025 revenue.

On a positive note, the gross profit margin is expected to expand ~10 - ~30 bps. This reflects benefits from strategic pricing actions and lower product input costs, partially offset by supply chain deleverage, channel mix shifts and net foreign exchange impact.

Full year SG&A growth is expected to be up slightly versus the prior year as NKE increases investments in demand creation while holding operating overhead largely flat. Other income and expense, including net interest income, is expected to be ~$0.25B - ~$0.3B in FY2025.

Risk Assessment

Little has changed subsequent to my March 23 post.

Moody’s continues to assign an A1 rating while S&P Global continues to assign an AA- rating to NKE’s domestic senior unsecured long-term debt. The outlook from both is stable.

Moody’s rating is the top tier of the ‘upper-medium grade’ investment-grade category. S&P Global’s rating is one notch higher at the bottom tier of the high-grade investment-grade category.

Moody’s rating defines NKE as having a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

S&P’s rating defines NKE as having a VERY STRONG capacity to meet its financial commitments with its rating differing from the highest-rated obligors only to a small degree.

NKE's FY2024 Form 10-K has yet to be released and the quarterly financial statements do not include a schedule of long term debt. I, therefore, reference the long-term debt schedule in NKE's FY2023 Form 10-K.

Source: NKE - FY2023 Form 10-K

We see from this schedule that NKE borrows at attractive rates.

At FYE2024, NKE reported ~$7.903B of long-term debt. $1B of its debt matures on March 27, 2025 and is now reflected as a current portion of long-term debt.

We see from NKE's long-term debt schedule that $3B of long term debt is scheduled for repayment before FYE2027. If all goes according to plan, NKE could have as little as $6B of long term debt by FYE2027. This may contribute to an upgrade in its credit ratings.

Dividend and Dividend Yield

On July 1, NKE distributed its 3rd consecutive $0.37/share quarterly dividend; we can expect one more quarterly dividend at this level to be distributed in early October.

In mid-November, NKE is likely to increase its quarterly dividend by ~$0.03/share. Should this materialize, the next 4 quarterly dividend distributions will total $1.57 (($0.37 x 1) + ($0.40 x 3)). With shares trading at ~$76 as I compose this post, the forward dividend yield is ~2%.

Dividend metrics are of little relevance in my investment decision making process. My interest lies in the efficient allocation of capital so as to maximize shareholder value; dividend distributions are not always the most optimal means by which to reward investors.

NKE's capital allocation includes the prolific repurchase of its outstanding shares.

In FY2014 - FY2024, the weighted average diluted shares outstanding (in billions) was 1.812, 1.769, 1.743, 1.692, 1.659, 1,618, 1.592, 1.609, 1.611, 1.570, and 1.530. The weighted average diluted shares outstanding in Q4 2024, however, was ~1.5127B.

NKE repurchased:

- 27.3 million shares for $3.994B (an average price of $146.11/share) in FY2022.

- 50.0 million shares for $5.5B (an average price of $110.32/share) in FY2023.

- 41.4 million shares for ~$4.3B in FY2024. The Form 10-K is currently unavailable but the Q3 2024 Form 10-Q indicates that during the first nine months of FY2024, 30.3 million shares were repurchased for $3.206B (an average price of $105.70/share); NKE's average share price in Q4 was below $105.70 and we know it repurchased 11.1 million shares in that quarter.

At FYE2024 (May 31, 2024), a total of 84.9 million shares had been repurchased under the current $18B program for a total of ~$9.1B.

I hope NKE is aggressively repurchasing its currently undervalued shares.

Valuation

In FY2024, NKE generated $3.73 of diluted EPS. With shares currently trading at ~$76 as I compose this post, NKE's PE is ~20.4.

Its valuation based on forward adjusted diluted earnings estimates from the brokers which cover NKE is:

- FY2025 – 33 brokers – ~24.3 using a mean of $3.13 and low/high of $2.74 – $3.65.

- FY2026 – 31 brokers – ~21.2 using a mean of $3.58 and low/high of $2.67 – $4.12.

- FY2027 – 13 brokers – ~19.4 using a mean of $3.91 and low/high of $2.64 – $4.56.

The data reflected above is likely to change over the coming days as some brokers have likely not yet updated their earnings estimates.

In FY2024, NKE's weighted average number of outstanding shares (in billions) was ~1.530. If it generated ~$5.21B of FCF in FY2024, we get ~$3.40 of FCF/share. Using a $76 share price, the P/FCF is ~22.4.

NKE's FY2025 earnings and FCF will depend on several factors with the reduction of inventory and share repurchases being key.

Looking at the share repurchases in recent years, the remaining ~$8.9B availability under the share repurchase program, current liquidity, the current attractive valuation, and the strong probability NKE will generate at least $5B of FCF in FY2025, I envision share repurchases of $5.5B in FY2025. Should this materialize and the average purchase price is $85, this amounts to ~64.706 million shares.

NKE issues shares as part of its employee compensation. Erring on the side of caution, let's suppose the net share repurchases in FY2025 is ~55 million shares. At FYE2024, the weighted average shares outstanding was ~1.5127B. In order to estimate the weighted average share outstanding in FY2025, I divide ~55 million shares by 2 since not all share repurchases will be made at the beginning or the end of the year. If the weighted average is reduced by 27.5 million shares, the weighted average for the year could be ~1.485B.

If NKE generates $5B of FCF in FY2025 and the weighted average share outstanding is ~1.485B, the FCF/share should be ~$3.37. With shares trading at ~$76, the forward P/FCF is ~22.6. I consider this to be an attractive P/FCF valuation for NKE.

Final Thoughts

On March 25, I acquired 100 shares @ $94.92. On June 28, I acquired an additional 100 shares @ ~$76.26. Both purchases were made through a 'Core' account within the FFJ Portfolio. Following these purchases and the reinvestment of dividend income, my exposure is now 930 shares. Nevertheless, it was not a top 30 holding when I recently completed my 2024 Mid Year FFJ Portfolio Review.

NKE's total shareholder return over the past 5 years is deplorable and its short term outlook is not encouraging. I can, therefore, understand why some investors may be reluctant to invest in the company.

As noted in several previous posts, I am interested in acquiring attractively valued shares of great companies. This often means a company has likely fallen out of favor with investors. NKE is such a company.

While the NKE brand remains strong, headwinds are contributing to the lackluster sale growth. I, however, like that it benefits from the worldwide popularity of athletics and its products are available in more than 190 countries; more than half its sales are outside North America. Its global market share is ~18% and its annual revenue is more than double than that of Adidas, the world's second-largest sportswear firm.

Despite its challenges, NKE continues to generate strong OCF and FCF and the Balance Sheet is strong. Furthermore, its capital allocation is exemplary.

I think NKE should be able to overcome its challenges and hope management is currently aggressively repurchasing shares.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to [email protected].

Disclosure: I am long NKE and ATD.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.