In my April 10 post, I reviewed Zoom Video Communications’ (ZM) FY2024 results and FY2025 guidance. With the release of Q1 2025 results and updated FY2025 outlook following the May 20 market close, I revisit this existing holding.

Business Overview

I recommend you review Part 1, Item 1 in ZM’s FY2024 Form 10-K which provides a comprehensive overview of the business, competition, and risks. This is accessible through the SEC Filings section of the company’s website.

The developments ZM has made to its suite of products has led to strong growth in the number of deals in which it has beat or displaced a leading Contact Center as a Service (CCaaS) participant.

CCaaS is deployed over the internet thereby eliminating the need for physical hardware or on-site systems. Its distinguishing feature is its ‘as-a-service’ model which offers businesses the flexibility to scale contact centre operations based on seasonal demand, customer preferences, or industry trends.

While a cloud contact center uses cloud technology, CCaaS specializes in offering the solution as a subscription service. The CCaaS architecture empowers businesses with the agility to adapt to shifting demands, sidestepping the high costs and upkeep of traditional on-premises systems.

CCaaS also bolsters two crucial areas:

- disaster recovery; and

- business continuity.

This ensures operations run smoothly even amidst unexpected disruptions. Furthermore, contact center compliance guarantees customer interactions remain safe and compliant with regulations.

ZM has also strengthened its channel partnerships thus leading to a significant increase in channel wins and a greater ability to compete for larger deals. Expedia and Major League Baseball are recognizable names to most investors, however, Centerstone is lesser known. It is a a nonprofit health system specializing in mental health and substance use disorder treatments for individuals, families, and veterans.

ZM has also greatly expanded its footprint with Capital One which doubled its Zoom Phone seats to over 100,000.

In addition, Meta Platforms has announced that it is shutting down Workplace, its business communication platform, in a push to prioritize artificial intelligence and other investments. In 2021, this platform had reached 7 million paid subscribers.

Workplace will be phased out over 2 years, with customers still able to use the platform as usual until August 2025; the product will no longer function after August 31, 2025, but data will be accessible until May 2026.

Meta has indicated it will provide Workplace customers the option to migrate to Workvivo for the next 2 years. Workvivo, a business communication tool ZM acquired in 2023, has been named as Meta’s only preferred migration partner for customers.

In March 2024, ZM and Avaya announced a new strategic partnership to deliver enhanced collaboration experiences; Avaya is an American technology company that provides cloud communications and workstream collaboration services. It specializes in business communications services such as unified communications (UC) and contact center (CC). Services are provided to ~220,000 customer locations in 190 countries.

Competition

ZM operates in highly competitive markets. In the ‘Our Competition’ section of ZMs’ FY2024 Form 10-K we find the following:

We face competition from legacy web-based meeting services providers, including Cisco Webex and GoTo, bundled productivity solution providers with video functionality, including Google Workspace and Microsoft Teams, and UCaaS and legacy PBX providers, including 8×8, Avaya, and RingCentral, as well as consumer- facing platforms that can support small- or medium-sized businesses, including Amazon, Apple, and Facebook. Additionally, as we build out Zoom Contact Center, we may face additional competition, including from Five9, Inc., Genesys and NICE inContact.

ZM, however, believes it competes favorably based on the following competitive factors:

- video-first platform;

- cloud-native architecture;

- functionality and scalability;

- ease of use and reliability;

- brand awareness and preference;

- ability to utilize existing infrastructure, such as legacy conference room hardware; and

- low total cost of ownership.

While ZM certainly has some formidable competitors, it continues to:

- win new business;

- generate positive Operating and Net Profit margins;

- generate positive Free Cash Flow (FCF); and

- is working on improving its Return on Invested Capital (ROIC).

At the other end of the spectrum from Microsoft, for example, ZM competes against unprofitable companies with negative margins, negative FCF, and negative ROIC.

Financials

Q1 2025 Results

Refer to material related to ZM’s Q1 Earnings which is accessible here.

In Q1, ZM saw additional traction in Zoom Contact Center as it reached 90 customers with over $100,000 in annual recurring revenue, representing a 246% YoY growth.

With the addition of Capital One, ZM now has 5 customers with 100,000 or more Zoom Phone seats.

Zoom AI companion has grown significantly in just 8 months with over 700,000 customer accounts enabled. These customers range from solo entrepreneurs up to enterprises with over 100,000 users.

Online average monthly churn was 3.2% versus 3.1% in Q1 2024. The slight uptick in churn was related to tightening up the grace period for unmade payments. Absent this change, online average monthly churn would remain consistent with the last 2 quarters at 3.0%, the lowest churn ZM has ever reported.

ZM also reported 8% YoY growth in the upmarket with 3,883 customers contributing more than $100,000 in trailing 12 months revenue. These customers represented 30% of revenue, up from 29% in Q1 2024.

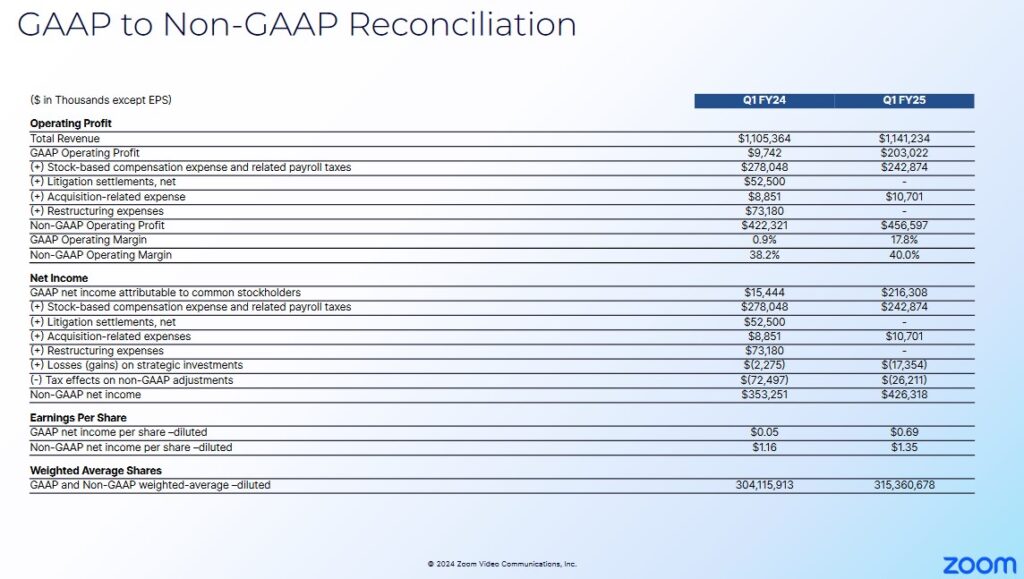

ZM’s non-GAAP results exclude stock-based compensation expense and associated payroll taxes, acquisition-related expenses, net gains on strategic investments and all associated tax effects. Its Q1 non-GAAP gross margin was 79.3%, which was slightly lower than 80.5% in Q1 2024. This was mainly due to ZM’s investments in AI innovation.

In Q2, ZM will incur onetime investments to upgrade its data center backbone and the gross margin is expected to dip to ~78% for the quarter. For FY2025, however, the gross margin is expected to be ~79%.

Non-GAAP income from operations grew by 8% YoY to $457 million, exceeding the high end of guidance of $415 million. This translates to a 40% non-GAAP operating margin for Q1, an improvement from 38.2% in Q1 2024.

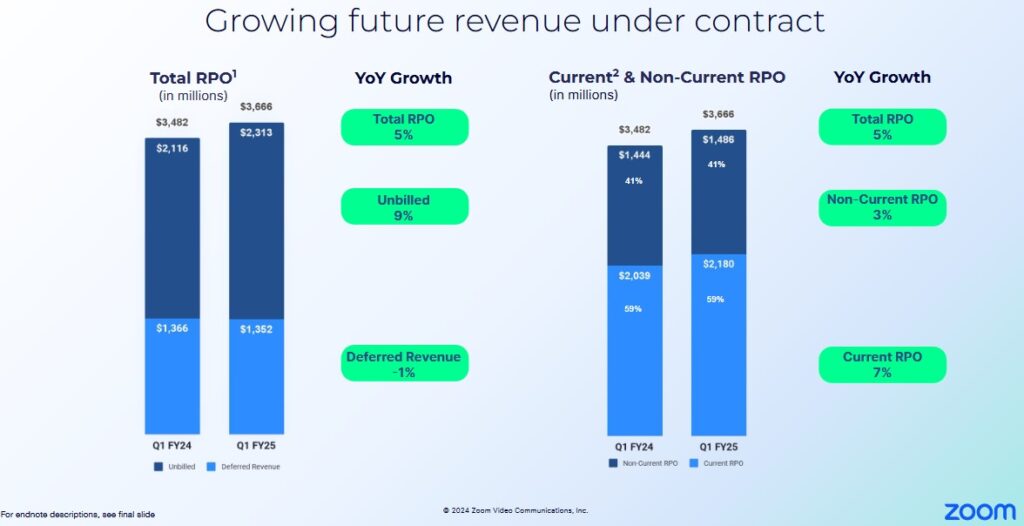

Deferred revenue at the end of Q1 was $1.35B, down ~1% from Q1 of last year. This was roughly 3 percentage points higher than the range provided in the prior quarter, partially due to tightening up ZM’s discounting practices.

The Remaining Performance Obligations (RPO) increased 5% YoY to ~$3.67B. ZM expects to recognize ~59% of the total RPO revenue over the next 12 months which is consistent with Q1 2024.

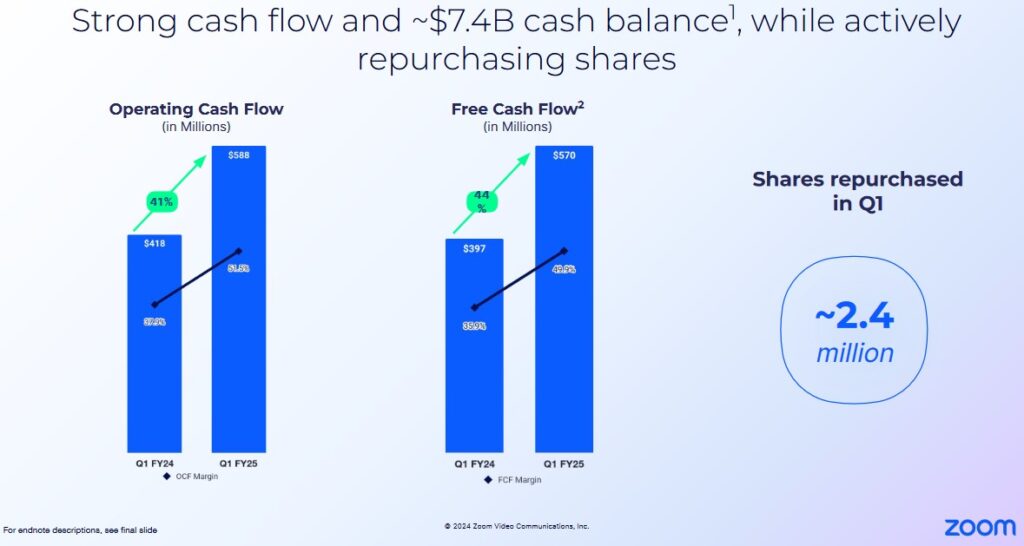

ZM ended Q1 with ~$7.4B in cash, cash equivalents and marketable securities, excluding restricted cash.

Operating Cash Flow (OCF) and Free Cash Flow (FCF)

In FY2017 – FY2024, ZM generated OCF of (in millions of $) 9.36, 19.43, 51.33, 151.89, 1,471.18, 1,605.27, 1,290.26, and 1,598.8. ZM generated ~$0.588B in Q1 2025 – a ~41% increase over Q1 2024.

In FY2017 – FY2024, ZM generated FCF of (in millions of $) $4.54, $9.69, $20.88, $113.67, $1,385.36, $1,459.66, $1,186.4, and $1,471.9. ZM generated ~$0.570B in Q1 2025 – a ~44% increase over Q1 2024.

The sharp increase in ZM’s cash flow metrics was due to stronger collections, targeted expense management and higher interest income.

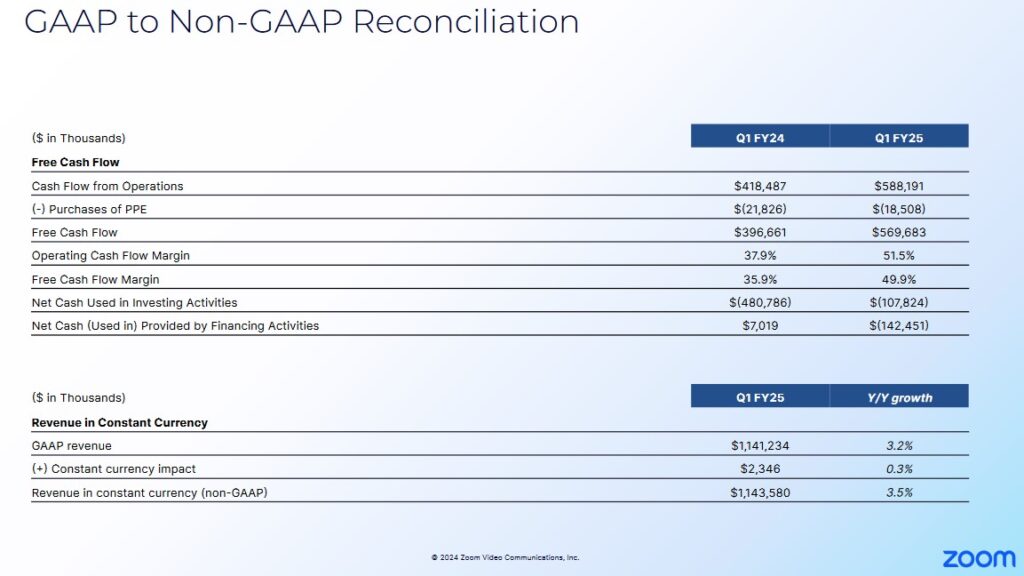

In FY2017 – FY2024, ZM’s annual CAPEX was (in millions of $) 4.82, 9.74, 30.45, 38.23, 85.82, 145.61, and 115.09. In Q1 2025, it was 18.5. While ZM’s annual CAPEX is negligible, it spends a considerable amount on research and development. In FY2022 – FY2024, it spent ~$0.363B, ~$0.774B, and ~$0.803B. In Q1 2025, it spent ~$0.206. These expenses, however, are deducted from earnings to determine Net Income so these R&D expenses are relevant when it comes to determining ZM’s OCF.

Given the nature of ZM’s business and formidable competition, it is essential that it incur significant R&D expenses!

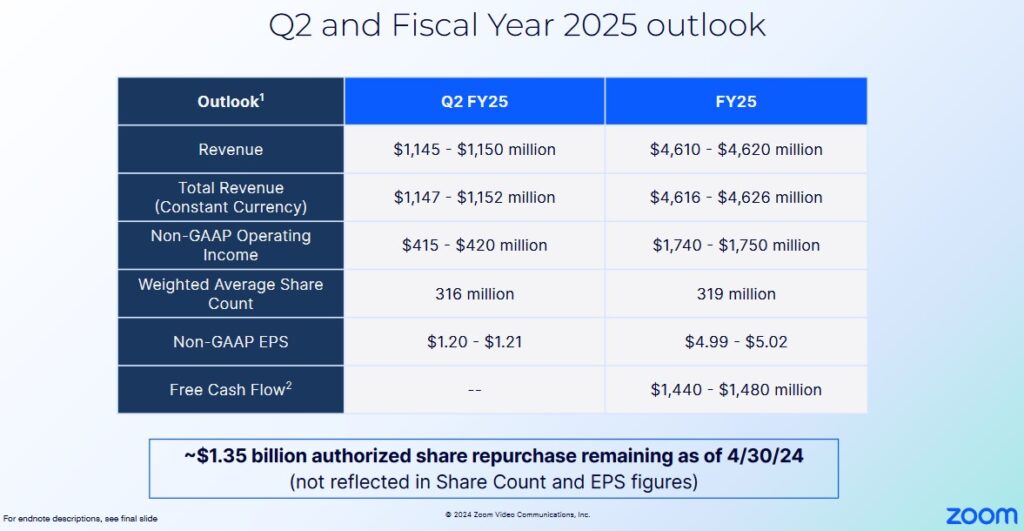

FY2025 Outlook

The following reflects ZM’s current outlook.

Expected Q2 revenue is ~$1.145B – ~$1.15B, representing ~1% YoY growth. Management continues to be of the opinion that Q2 will be the low point from a YoY growth perspective.

FY2025 revenue is now expected to be ~$4.61B – ~$4.62B which represents ~2% YoY growth.

The non-GAAP operating income forecast is ~$1.74B – ~$1.75B representing an operating margin of 37.8%, at the midpoint.

Due to timing of US federal and state tax payments, ZM paid minimal taxes in Q1. It will, however, pay 2 quarters worth of tax payments in Q2. Primarily due to this seasonality and AI-related CAPEX, FCF in Q2 is expected to decrease by ~50% – 60% quarter over quarter, before normalizing in Q3 and Q4.

ZM’s prior outlook is provided below for ease of comparison.

Risk Assessment

ZM has no debt, and therefore, no rating agency covers it.

Dividends and Share Repurchases

Dividend and Dividend Yield

ZM does not distribute a dividend.

Share Repurchases

ZM’s weighted average shares outstanding in FY2017 – FY2024 are (in millions of shares) 269, 269, 269, 254, 298, 306, 304, and 308.5. This increased to ~$315.4 in Q1.

In November 2018, ZM implemented a dual-class common stock structure. A Class A common stock entitles the shareholder to one vote per share. The Class B common stock entitles the shareholder to 10 votes per share. The Class A and Class B common stock have the same dividend and liquidation rights.

Details of ZM’s Stockholders’ Equity and Equity Incentive Plans are in Note 10 (commences on page 92 of 124) in the FY2024 Form 10-K.

ZM’s Board has authorized a stock repurchase program of up to $1.5B of the outstanding Class A common stock in FY2025. In Q1, ZM repurchased ~2.4 million shares for a total of ~$0.15B. At the end of Q1, $1.35B authorization remained. Management expects to opportunistically repurchase shares over the remainder of FY2025.

Valuation

In FY2020 – FY2024, ZM generated $0.09, $2.25, $4.50, $0.34, and $2.07 in diluted EPS and $0.35, $3.34, $5.07, $4.37, and $5.21 in adjusted diluted EPS.

My calculations of ZM’s valuation at the time of prior posts is found in my November 21, 2023 post.

At the time of my April 10 post, I wrote the following:

ZM’s adjusted diluted EPS guidance for FY2025 was $4.85 – $4.88. Using my $61.695 purchase price on April 10, the forward adjusted diluted PE was ~12.7.

Using my purchase price and the adjusted diluted EPS broker estimates at the time, ZM’s forward adjusted diluted PE levels were:

- FY2025 – 29 brokers – ~12.5 using a mean of $4.92 and low/high of $4.83 – $5.46.

- FY2026 – 29 brokers – ~12.4 using a mean of $4.98 and low/high of $4.58 – $5.50.

- FY2027 – 9 brokers – ~12.1 using a mean of $5.09 and low/high of $4.38 – $5.69.

These adjusted diluted earnings estimates do not account for any share repurchases which are to occur in FY2025.

If ZM repurchases $1.5B at ~$65/share in equal quarterly tranches, we can expect a total repurchase of ~23.077 million shares.

The FY2025 weighted average shares outstanding forecast is 321 million shares. If we subtract ~23.077 million shares, we get slightly below 300 million shares. ZM, however, issues shares as part of its employee compensation structure. We can, therefore, expect the weighted average number of outstanding shares in FY2025 to likely be closer to 300 million.

Taking into consideration $1.5B of share repurchases in FY2025, ZM could generate $4.96 – $5.00 of non-GAAP EPS. Using the $4.98 mid-point and my $61.695 purchase price, the forward adjusted diluted PE is ~12.4.

ZM’s FY2025 FCF outlook is $1.44B – $1.48B. Using a $1.46B mid point and 300 million weighted average shares outstanding, the projected FCF/share is ~$4.89. $61.695 divided by $4.89 gives us a P/FCF valuation of ~12.6.

Rough estimates suggest that ZM’s valuation based on forward adjusted diluted earnings and FCF is in the very low teens.

ZM has now revised its adjusted diluted EPS guidance for FY2025 to $4.99 – $5.02. On May 21, I acquired an additional 100 shares @ just under $63. Using this price and the $5.005 mid-point, the forward adjusted diluted PE is ~12.6.

Using adjusted diluted EPS broker estimates, ZM’s forward adjusted diluted PE levels are:

- FY2025 – 28 brokers – ~12.7 using a mean of $5.00 and low/high of $4.86 – $5.36.

- FY2026 – 31 brokers – ~ 12.4 using a mean of $5.08 and low/high of $4.67 – $5.58.

- FY2027 – 13 brokers – ~ 12.1 using a mean of $5.20 and low/high of $4.54 – $5.95.

These adjusted diluted earnings estimates do not account for any share repurchases which are to occur in FY2025.

The FY2025 weighted average shares outstanding forecast is now 319 million shares. If ZM continue to repurchase shares quarterly over the remainder of FY2025, it is possible for the share count to be reduced to slightly below 300 million shares. ZM, however, issues shares as part of its employee compensation structure. We can, therefore, expect the weighted average number of outstanding shares in FY2025 to likely be closer to 300 – 305 million.

ZM now expects its FY2025 FCF to come in close to the upper end of its FY2025 $1.44B – $1.48B outlook. Using $1.47B and 300 million weighted average shares outstanding, the projected FCF/share is ~$4.90. $63 divided by $4.90 gives us a P/FCF valuation of ~12.9.

My rough estimates suggest that ZM’s valuation based on forward adjusted diluted earnings and FCF is still in the very low teens.

Final Thoughts

While ZM may occasionally experience lacklustre quarterly growth, I remain confident in its long-term outlook. It continues to be profitable and I am impressed with its margins. Having said this, ZM has formidable competition and must continue to incur significant research and development expenses (eg. artificial intelligence development costs). I, therefore, do not think there is much room to expand margins. This is, perhaps, one reason why ZM’s valuation is so attractive.

Investing in ZM is 2019 – 2021 at lofty valuation levels was imprudent. At the current valuation, however, I think ZM has a realistic chance to generate a low double-digit average annual rate of return over the next several years.

I view ZM to currently be undervalued and have acquired an additional 100 shares @ in a ‘Core’ account within the FFJ Portfolio bringing my exposure to 900 shares.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ZM.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.