I last reviewed Zoom Video Communications (ZM) in my May 21, 2024 post. At the time, the most currently available financial information was for Q1 2025. With the release of Q2 and YTD2025 results following the August 21 market close, I revisit this existing holding.

WARNING: ZM is not to be confused with ZoomInfo Technologies Inc. (ZI). ZI is toxic!

Business Overview

Part 1, Item 1 in ZM’s FY2024 Form 10-K (see SEC Filings) provides a comprehensive overview of the business, competition, and risks.

ZM has Class A (publicly traded shares) and Class B shares. The Class A and B shares have 1 and 10 votes per share, respectively.

The Class B shareholders have significant influence over the management and over all matters requiring stockholder approval, including the election of directors and significant corporate transactions, such as a merger or other sale of ZM or its assets, for the foreseeable future. Within the Risk Factors section of ZM’s Form 10-Q and Form 10-K, there is commentary regarding this dual class structure.

Financials

Q2 and YTD2025 Results

ZM’s Q2 Earnings material (including the transcript of the earnings call) is accessible here.

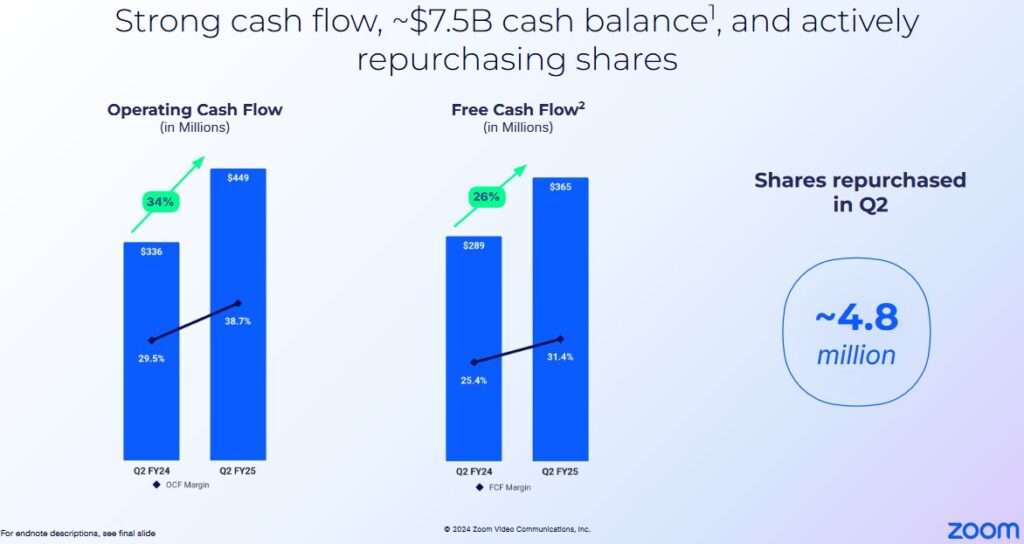

At the end of Q2, ZM had in excess of $7.5B of cash and cash equivalents and marketable securities versus ~$7B at FYE2024. This increase is impressive considering YTD2025 share repurchases of ~$0.438B.

The current liabilities at the end of Q2 total ~$1.841B of which ~$1.391B is deferred revenue that will be realized within the next 12 months. Deduct the short-term deferred revenue from the total current liabilities and we get ~$0.45B.

Total liabilities of ~$1.982B less ~$1.407B of short- and long-term deferred revenue leaves ~$0.575B of total liabilities. This could easily be fully retired while leaving ZM with ~$7B of liquidity.

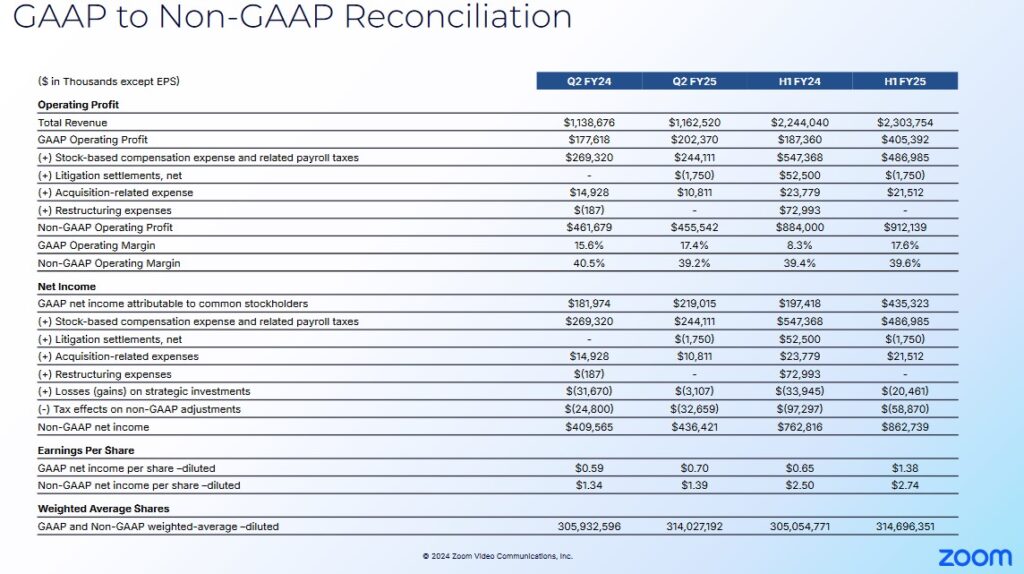

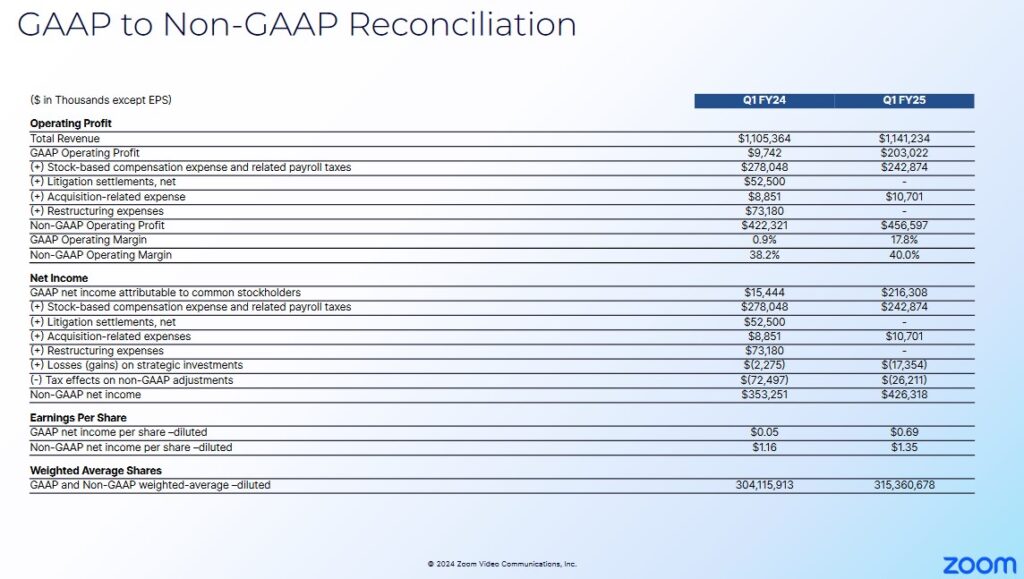

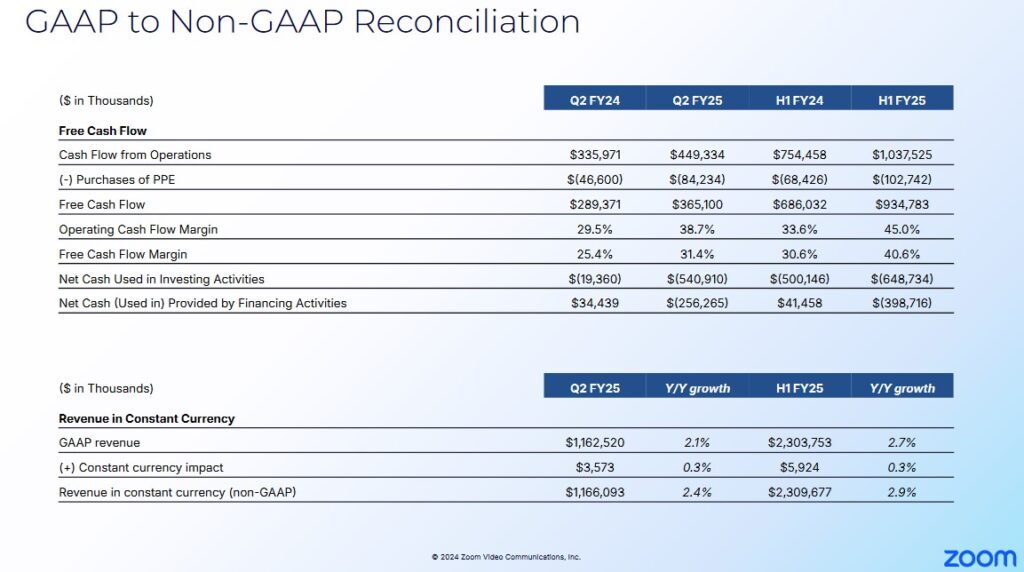

The Q2 and YTD2024 and Q2 and YTD2025 results are provided below along with Q1 2024 and Q1 2025 results for comparison.

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In FY2018 – FY2024, OCF, CAPEX, and FCF were:

- OCF was (in millions of $) 19.43, 51.33, 151.89, 1,471.18, 1,605.27, 1,290.26, and 1,598.8. ZM generated ~$1.038B in the first half of FY2025.

- CAPEX was (in millions of $) 9.74, 28.4, 38.00, 80.00, 132.6, 103.8, and 127. ZM incurred ~$0.103B CAPEX in the first half of FY2025.

- FCF was (in millions of $) 9.69, 22.93, 113.89, 1,391.18, 1,472.7, 1,186.46, and 1,471.8. ZM generated ~$0.935B in the first half of FY2025.

ZM’s annual CAPEX is negligible. It does, however, spend a considerable amount on research and development (R&D). In FY2022 – FY2024 and the first half of FY2025, it spent ~$0.363B, ~$0.774B, ~$0.803B, and ~$0.412B. These expenses are deducted from earnings to determine Net Income so they come into the equation when determining ZM’s OCF and FCF.

Capital Allocation

The capital allocation priority is to retain funds for growth and M&A. The opportunistic repurchase of Class A shares comes next. Dividend distributions are non-existent.

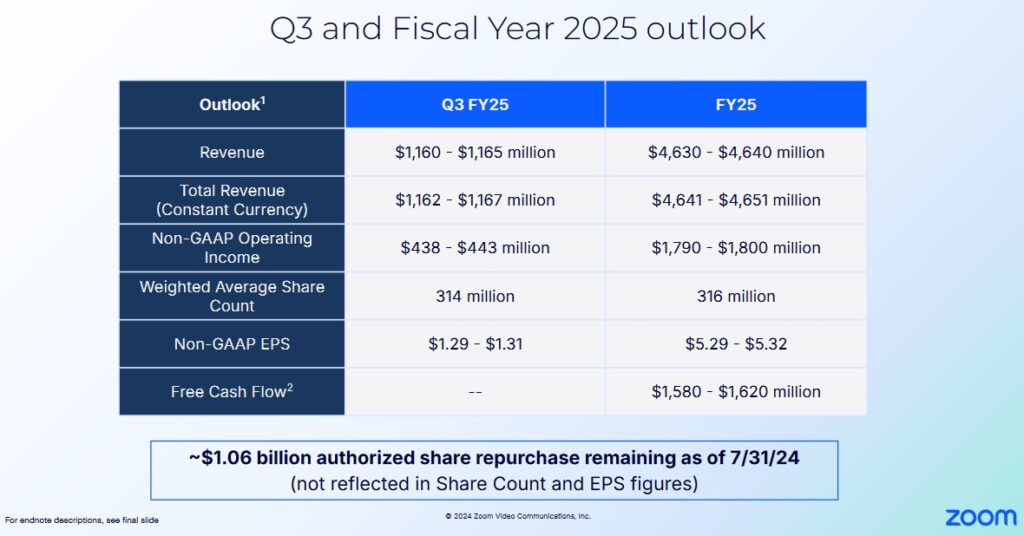

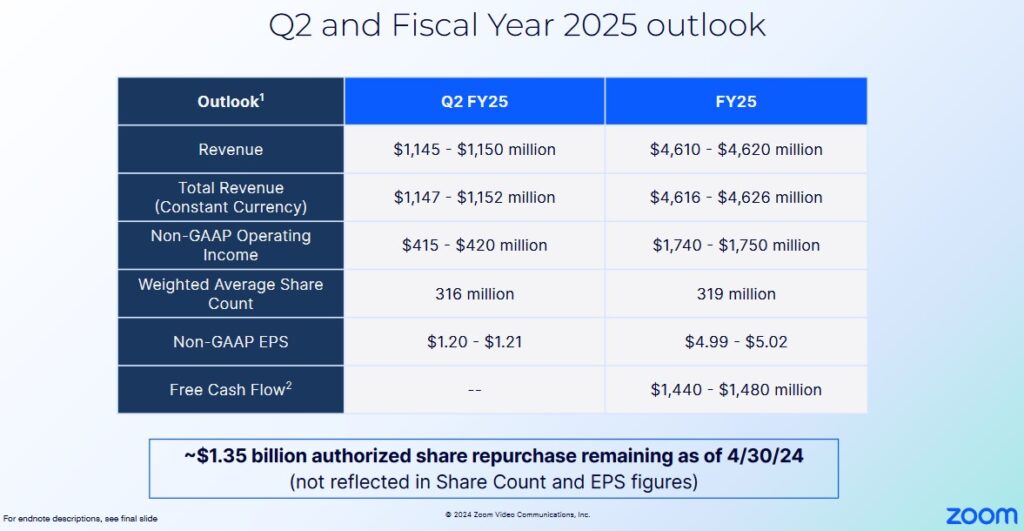

Q3 and FY2025 Outlook

An encouraging trend is evident when we compare ZM’s current outlook with the outlook provided with the release of FY2024 and Q1 2025 results.

Risk Assessment

ZM has no debt to be rated.

Dividends and Share Repurchases

Dividend and Dividend Yield

ZM does not distribute a dividend.

Share Repurchases

Details of ZM’s Stockholders’ Equity and Equity Incentive Plans are in Note 10 (commences on page 92 of 124) in the FY2024 Form 10-K.

ZM’s weighted average shares outstanding in FY2017 – FY2024 are (in millions of shares) 269, 269, 269, 254, 298, 306, 304, and 308.5. The weighted average for the first half of FY2025 is ~$314.7.

ZM’s Board has authorized a stock repurchase program of up to $1.5B of the outstanding Class A common stock in FY2025. Under this repurchase program, ZM purchased 4.8 million shares for $0.288B, up from 2.4 million shares for $0.150B in Q1. YTD2025, it has repurchased ~$0.438B. The weighted average shares outstanding, however, is increasing because the YTD stock-based compensation expense is ~$0.468B.

Management expects to opportunistically repurchase shares over the remainder of FY2025 with the weighted average share outlook now ~316 million shares versus ~321 million provided earlier in the year.

Valuation

In FY2020 – FY2024, ZM generated $0.09, $2.25, $4.50, $0.34, and $2.07 in diluted EPS and $0.35, $3.34, $5.07, $4.37, and $5.21 in adjusted diluted EPS.

When I wrote my May 21, 2024 post, ZM’s FY2025 adjusted diluted EPS guidance was $4.99 – $5.02. On May 21, I acquired an additional 100 shares @ just under $63. Using this price and the $5.005 mid-point, the forward adjusted diluted PE was ~12.6.

Using adjusted diluted EPS broker estimates, ZM’s forward adjusted diluted PE levels were:

- FY2025 – 28 brokers – ~12.7 using a mean of $5.00 and low/high of $4.86 – $5.36.

- FY2026 – 31 brokers – ~ 12.4 using a mean of $5.08 and low/high of $4.67 – $5.58.

- FY2027 – 13 brokers – ~ 12.1 using a mean of $5.20 and low/high of $4.54 – $5.95.

These adjusted diluted earnings estimates do not account for any share repurchases which are to occur in FY2025.

I indicated that if ZM continued to repurchase shares quarterly over the remainder of FY2025, it was possible for the share count to be reduced to slightly below 300 million shares. ZM, however, issues shares as part of its employee compensation structure. I, therefore, expected the weighted average number of outstanding shares in FY2025 to likely be closer to 300 – 305 million.

ZM’s FY2025 FCF outlook was that it would generate FCF close to the upper end $1.44B – $1.48B. Using $1.47B and 300 million weighted average shares outstanding, I envisioned the projected FCF/share would be ~$4.90. $63 divided by $4.90 resulted in a P/FCF valuation of ~12.9.

I was cautiously optimistic ZM would repurchase more shares than it issues under its various employee compensation programs. In hindsight, I should have used 319 million shares instead of 300 million weighted average shares outstanding. Had I done this, $1.47B of FCF divided by 319 million shares would have given me a projected FCF/share of ~$4.61. $63 divided by $4.61 would have resulted in a P/FCF valuation of ~13.7.

ZM’s revised FY2025 adjusted diluted EPS is $5.29 – $5.32. Unfortunately, ZM’s share price has surged following its earnings release and shares now trade at ~$67.30 as I finalize this post thus giving us a forward adjusted diluted PE range of ~11.3 – ~11.4.

Using the current adjusted diluted EPS broker estimates, ZM’s forward adjusted diluted PE levels are:

- FY2025 – 30 brokers – ~12.65 using a mean of $5.30 and low/high of $5.00 – $5.72.

- FY2026 – 30 brokers – ~ 12.90 using a mean of $5.22 and low/high of $4.87 – $5.83.

- FY2027 – 17 brokers – ~ 12.77 using a mean of $5.27 and low/high of $4.75 – $5.94.

ZM’s FY2025 FCF outlook is now $1.58B – $1.62B. Using $1.60B and the updated 316 million weighted average shares outstanding outlook, the projected FCF/share is ~$5.06. $67.30 divided by $5.06 results in a P/FCF valuation of ~13.3.

If ZM’s share price were to rise to a fair valuation of ~$75 (a ~11.4% increase from the current $67.30 share price), the PE and P/FCF would still be under 15!

Final Thoughts

There is no change to the final thoughts in my May 21, 2024 post.

I currently only hold 900 shares in a ‘Core’ account within the FFJ Portfolio at an average cost of ~$63.34, making it too small to have been a top 30 holding when I completed my 2024 Mid Year FFJ Portfolio Review. Despite this negligible exposure, Zoom Video Communications continues to impress me. Investors who are relatively risk averse may want to consider ZM as a potential investment.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ZM.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.