When I published my Copart Is A Great Company. Can’t Say The Same For Its Valuation post on November 24, 2024, shares were trading at $62.70.

Following the February 20, 2025 market close, CPRT released its Q2 and YTD2025 results. After reviewing its results, I acquired an additional 400 shares @ ~$56.29 in a ‘Side’ account within the FFJ Portfolio.

Business Overview

Section 1 of CPRT’s Form 10-K provides a good overview of the company (refer SEC Filings).

I encourage you to watch some ‘live’ CPRT auctions.

Financials

Q2 and YTD2025 Results

CPRT’s financial results are available through the SEC Filings section of the company’s website.

Q2 2025 Earnings Call Transcript

The following is CPRT’s CEO commentary from the Q2 2025 earnings call which addresses key topics that impact CPRT’s performance and outlook.

We continue to grow our insurance volume, our auction liquidity and the returns we’re generating for our sellers.

Our insurance carriers with each passing day are entrusting us with more of the workflow that they once handled in-house, both day-to-day and in storm events as well.

As one very visible example, now that we are processing well over 1 million titles per year via our Title Express platform, no carrier who has started with Copart has taken it back in-house.

We also continue to grow our volume with our non-insurance sellers, benefiting, of course, from the flywheel effects of our auctions. And finally, we continue to invest proudly and aggressively in our business in the form of technology, real estate and people to fuel our future growth.

I wanted to provide a few brief comments on our insurance business specifically before turning it over to Leah to review the financial results and to take a few of your questions.

First, on our insurance business.

Our global volume grew 8% for the quarter in comparison to the same quarter last year, a little over half of this was attributable to the catastrophic events in the second half of last year. That has been true since the dawn of our industry, we continue to experience increases in total loss frequency, of course, with the singular exception of the blip from 2021 to 2022 when ACVs (actual cash value) or pre-accident values increased more than they ever had previously in Copart’s history.

For the fourth quarter in the United States, total loss frequency hit 23.8%, an all-time high, though a portion of that is attributable to those storm events in the second half of last year, which tend to have very high total loss frequency rates. Nonetheless, the full year trend of 22.2% represents an all-time annual high and the total loss frequency drivers certainly continue unabated.

Repairing cars becomes less attractive as time passes as labor cost increase, repair, parts cost increase and rental car rates do as well, while totaling vehicles becomes more attractive given the liquidity of our auctions, demand for our vehicles by international buyers and the salvage returns we’re able to generate for our sellers.

A couple of inquiries we’ve received in recent days that I thought might be worth addressing today.

First is the question about whether insurance coverage in general has changed. And I would note that over the past 2 years, the insurance industry has generally achieved rate relief through state regulatory bodies and consumers have certainly felt those changes in the form of higher rates for their auto policies. This has caused a modest increase in the uninsured population relative to pre-COVID levels, certainly. Over many years, we’ve observed this to be a cyclical trend, meaning the uninsured motorist rates tends to go up and down over the years. And given where we sit right now, it likely is a modest — it represents a modest offset to the growth in our insurance business.

The second topic I wanted to address briefly is the question of what potential tariffs mean for our business, and I’ll take a U.S.-centric view first to addressing this question. It’s frankly similar to an inquiry that we get from time to time about whether high used car prices or low used car prices are better for our business. The reality is that we’re somewhat ambivalent. And in this case, the bottom line of a potential tariff-oriented approach would be that it’s largely neutral to our business, though with a complex tapestry of offsetting forces, some of which we’ll briefly touch on today.

As you know, in general, the effects of tariffs are largely inflationary for each of the factors that in turn affect our business with the corresponding downstream effects on our unit volume, our selling prices and our operating profit.

Here are a few such examples. Inbound tariffs in isolation would increase the cost of repair parts for vehicles, which all else equal, would increase total loss frequency and drive increased volume to Copart. Inbound tariffs, however, would also increase pre-accident values or actual cash values to use the American [ parlance ], which in isolation would increase the cost of total losses to insurance carriers, reducing total loss frequency and suppressing volume to Copart. But those inbound tariffs would also increase the selling prices for the vehicles that we sell at auction for the very same reason, yet again, driving total loss frequency up and improving our unit economics as well.

If the story is stopped there, I’d characterize the effect of tariffs as being modestly positive to Copart. The great unknown, however, is what inbound tariffs for shipments to the United States, whether those tariffs could precipitate retaliatory tariffs from the same countries against whom we are imposing them. On its face, those tariffs might appear to suppress selling prices for our vehicles at auction.

However, for the automotive industries, the countries that would face the most substantial tariff burdens such as Germany, Japan, Mexico and Canada are generally not the providers of critical high-value liquidity for our auctions. Those nations are typically in Eastern Europe, the Middle East and Africa, as has been true now for many years, economic outcomes for our sellers and for Copart at our auctions are largely driven by the cars that we are selling as repairable drivable cars, not as parts to be harvested nor as metal to be scrapped. The countries who are hungriest for these types of cars generally do not have substantial domestic auto manufacturing capabilities and as such, are not likely to be subject to significant automotive tariffs against which to retaliate in the first place. That’s a bit of a long-winded answer. But in sum, I think we believe the tariffs would have a likely neutral to modestly positive effect on our business, and we based it on such inquiries that I thought it was worth exploring in greater detail.

The company’s cash, cash equivalents, and restricted cash and investment in held to maturity securities increased to ~$3.8B versus ~$3.7B at the end of Q1 2025 and ~$3.4B at FYE2024 (July 31). This increase is despite YTD2025 net CAPEX of ~$0.353B!

In addition to its ~$3.8 billion in cash, CPRT has an unused revolving credit facility of over $1.2B.

It continues to have no debt on its Balance Sheet. If it were to collect 100% of its ~$0.883B of accounts receivable in one fell swoop, it could wipe out ALL liabilities.

YTD2025, net cash provided by operating activities was ~$0.660B versus ~$0.537B during the same period in the prior fiscal year.

Capital Allocation Strategy

CPRT does not repurchase shares nor does it issue a dividend. Reinvesting in the business is CPRT’s capital allocation priority.

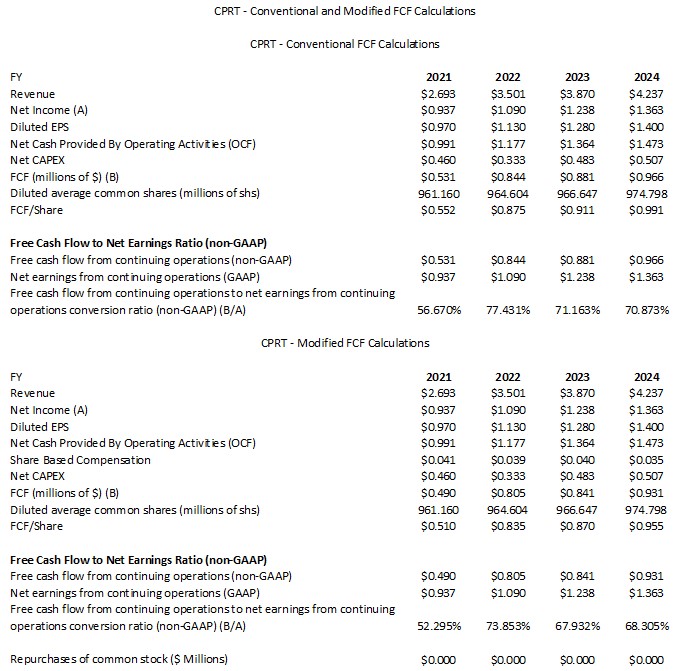

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In various prior posts, I deduct stock-based compensation (SBC) when determining a company’s net cash provided by operating activities. This is particularly important when a significant component of a company’s employee compensation is in the form of SBC.

Let’s suppose a company grants a significant number of company shares to employees as part of its various compensation packages. This form of remuneration is not reflected on the Income Statement to determine Net Earnings. If the company did not grant this SBC, however, you would think it would need to boost salaries/wages in order to retain its employees. These higher wages/salaries WOULD be reflected within the Income Statement thus having an impact on earnings.

Some investors may resort to the argument that a company is issuing shares to its employees but is often offsetting these new shares by repurchasing an equal or greater number of shares.

Having looked at countless Form 10-Ks over the years, I see companies granting stock options at prices that are often far below current share prices. So….you have a company repurchasing a boatload of shares at $X but it is issuing shares to employees (with a significant component to senior management) at a small fraction of $X. As a retail investor with an insufficient number of shares to sway the decision making at the Board level, I have no choice but to watch my investment in a company being eroded while insiders and employees are being enriched.

CPRT is unlike companies in the technology sector that have a substantial component of its employee remuneration in the form of share-based compensation. Although CPRT issues shares to its employees, the amount of annual SBC results in a moderate difference in FCF when calculated under the conventional and modified methods.

FY2025 Outlook

CPRT does not provide any outlook.

Risk Assessment

CPRT has no debt to rate.

Dividend and Dividend Yield

CPRT has not paid a cash dividend since becoming a public company in 1994.

Stock Splits

Since becoming a shareholder on January 18, 2022, CPRT has had two 2 for 1 stock splits (November 3, 2022 and August 21, 2023).

In FY2013 – FY2024, CPRT’s weighted average number of outstanding shares (in millions of shares rounded) was 1,038, 1,050, 1,051, 977, 948, 968, 962, 955, 961, 965, 967, and 975.

On September 22, 2011, CPRT’s Board authorized a 320 million share increase in the stock repurchase program, bringing the total current authorization to 784 million shares.

Share repurchases were made in:

- 2013: $572 thousand

- 2014: $15,009 million

- 2015: $233,484 million

- 2016: $442,855 million

- 2018: $364,997 million

No repurchases were made in FY2017, FY2018, FY2020 – FY2024, and YTD2025.

Valuation

My November 24, 2024 post analyzes CPRT’s valuation at various prior points in time. For ease of comparison, however, I provide CPRT’s valuation at the time of my last review.

In Q1 2025, CPRT generated $0.37 EPS versus $0.34 in Q1 2024.

Using the current broker estimates and the $62.70 share price at the November 22 market close, the forward-adjusted diluted PE levels are:

- FY2025 – 10 brokers – ~40.5 based on the mean of $1.55 and low/high of $1.48 – $1.61.

- FY2026 – 10 brokers – ~36 based on the mean of $1.74 and low/high of $1.68 – $1.81.

- FY2027 – 3 brokers – ~32 based on the mean of $1.96 and low/high of $1.95 – $1.97.

CPRT generated ~$0.244B of FCF in Q1 2025. Let’s estimate that CPRT will generate ~$0.96B of FCF in FY2025.

The weighted average shares outstanding in FY2022 – FY2024 and Q1 2025 (in millions) are 964.6, 966.7, 974.8, and 976.5. Repurchasing shares is not a capital allocation priority so let’s presume the weighted average shares outstanding in FY2025 will be 978 million.

Divide ~$0.96B by 978 million shares and we get ~$0.98 FCF/share. With a current $62.70 share price, the estimated P/FCF is ~64.

In the first half of FY2025, CPRT generated $0.77 EPS versus $0.68 in the same period in FY2024.

Using the current broker estimates and my February 21 ~$56.29 purchase price, the forward-adjusted diluted PE levels are:

- FY2025 – 11 brokers – ~35.6 based on the mean of $1.58 and low/high of $1.54 – $1.64.

- FY2026 – 11 brokers – ~31.6 based on the mean of $1.78 and low/high of $1.72 – $1.91.

- FY2027 – 4 brokers – ~25.2 based on the mean of $2.23 and low/high of $1.96 – $2.23.

CPRT generated ~$0.306B of FCF in the first half of 2025. I do not envision FY2025 FCF dropping much below FY2022’s modified FCF level of $0.805B. I am, therefore, revising my FCF estimate to $0.8B from my previous ~$0.96B estimate.

The weighted average shares outstanding in FY2022 – FY2024 and Q2 2025 (in millions) are 964.6, 966.7, 974.8, and 977.9 (977.2 for the first half of FY2025). My prior FY2025 estimate was 978 million. I am revising my estimate to 980 million.

Divide ~$0.8B by 980 million shares and we get ~$0.816 FCF/share. Using my ~$56.29 purchase price, the estimated P/FCF is ~69.

I find it extremely difficult to estimate CPRT’s FCF resulting in my valuation estimates being ‘all over the map’.

Final Thoughts

I initiated a position on February 17, 2022 in one of the ‘Core’ accounts within the FFJ Portfolio. Following subsequent purchases including that on February 21, 2025, I now own:

- 2,600 shares at an average cost of ~$35.4537 in a ‘Core’ account;

- 400 shares at an average cost of ~$54.60 in a different ‘Core’ account;

- 400 shares at an average cost of ~$56.29 in a ‘Side’ account;

- 540 shares at an average cost of ~$53.93 in a different ‘Side’ account.

CPRT was my 12th largest holding when I completed my 2024 Year End Review and my 10th largest when I completed my 2024 Mid Year FFJ Portfolio Review. Unless I complete another similar review I do not know its current ranking. I do know, however, that it is still a top 20 holding.

In addition, a couple of young investors I am helping on their journey to financial freedom have CPRT exposure; I do not disclose details of their investments and exclude these shares when I complete my Mid Year and Year End FFJ Portfolio Reviews.

Not all earnings – the ‘E’ component of the PE ratio – are of equal value. Some companies produce their earnings with significantly less capital intensity and deliver more of their earnings in cash. Furthermore, such companies are apt to have more predictable earnings. Such is CPRT.

It might not appeal to investors because it is in the business of selling damaged vehicles (not exactly a ‘sexy’ industry). The company, however, is growing, makes money, generates FCF, has no debt, and is relatively recession and tariff resistant. Given this, I am willing to ‘pay up’ to acquire shares.

My preference is to invest in companies that can retain earnings to generate attractive returns. Furthermore, my investment time horizon is well beyond my lifetime.

If your investment objectives are similar to mine, you may wish to consider CPRT as a long-term investment.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CPRT.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.