My primary reason for sharing my thoughts on wealth-destroying mistakes to avoid is to ultimately help you improve your financial well-being.

What I provide is not an all-encompassing list of wealth-destroying mistakes nor are they in any order of severity. Some mistakes can be corrected more easily than others. Much depends, however, on your unique circumstances.

Let’s begin.

Wrong Relationship

Relationships play a critical role in creating/destroying wealth. A relationship with someone who is totally incompatible can set the stage for wealth destruction.

Relationships can help create wealth in the following ways:

- Shared Financial Goals and Planning: The collective efforts, resources, and shared accountability with partners, family members, or even close friends can accelerate wealth accumulation. Better budgeting, saving, and investment strategies happen when all are aligned on financial goals and financial planning.

- Increased Earning Potential: Supportive relationships can encourage individuals to pursue career advancements, take risks in business, or seek higher-paying opportunities. Multiple sources of income when in a committed relationship can significantly increase household wealth compared to a single-income household.

- Economies of Scale: Sharing living expenses with a partner or family can significantly reduce individual costs. This frees up more money for saving and investing.

- Emotional and Practical Support: Strong relationships provide emotional support and practical assistance during financial difficulties thus helping to prevent financial ruin and facilitating recovery.

- Shared Knowledge and Skills: Partners or friends with complementary financial knowledge can educate and empower each other to make smarter financial decisions.

- Business Partnerships: Strong, trusting relationships can form the foundation of successful business ventures, leveraging diverse skills and shared risk to create wealth.

- Inheritance and Generational Wealth Transfer: Positive family relationships often facilitate the transfer of wealth across generations.

- Reduced Stress and Improved Well-being: Healthy relationships contribute to lower stress levels and improved mental and physical health, indirectly impacting financial well-being by reducing healthcare costs and increasing productivity.

Relationships can also destroy wealth.

- Poor Financial Habits and Conflicts: Disagreements about spending, saving, and debt management are major sources of relationship conflicts. Differing financial values and habits can lead to financial strain, overspending, and debt accumulation.

- Financial Infidelity: Hiding debts, secret accounts, or significant purchases from a partner erodes trust and can lead to severe financial consequences and relationship breakdown.

- Supporting Financially Dependent Individuals: Caring for loved ones is important. Enabling chronic financial dependence, however, can drain resources and hinder wealth accumulation.

- Costly Breakups and Divorces: Relationship dissolution can be incredibly expensive. Legal fees, asset division, and the costs of establishing separate households often significantly deplete wealth.

- Enabling Addictions or Poor Choices: Relationships where one partner enables another’s harmful habits (e.g. gambling, excessive spending, drinking, and drugs) can lead to significant financial losses.

- Co-signing Loans or Guarantees: Financially supporting a friend or family member by co-signing loan agreements can be risky. We become responsible for the debt if they default on their obligations.

- Lack of Communication and Transparency: Avoiding crucial financial conversations often leads to misunderstandings, poor decision-making, and a failure to address financial problems before they escalate.

- Power Imbalances: In relationships where one partner controls all the finances, the other may feel disempowered and unable to participate in financial decisions. This can potentially lead to resentment and poor financial management.

- Impact of Others’ Financial Problems: Close relationships with individuals facing severe financial difficulties can sometimes lead us to provide financial assistance thereby potentially straining our resources.

Vices That Become Habits

Vices that become habits act as a persistent leak in the financial bucket. Each indulgence viewed in isolation may seem small. Their repetitive nature and potential for escalating costs, coupled with indirect consequences such as health problems and poor decision-making, can collectively sabotage financial well-being and significantly impede or even destroy wealth over time.

They carry direct and indirect financial costs and can also have a psychological and emotional impact.

Direct financial costs typically involve regular and frequent expenditures. In the case of addictive vices (eg. substance abuse or gambling) the need for increasing amounts to achieve the desired effect leads to escalating financial burdens.

Indirect financial costs consist of health and legal issues, impaired decision-making, reduced savings and investment potential, debt accumulation, and relationship damage.

Vices also have a psychological and emotional impact. Stress and anxiety typically arise and can often lead to guilt and shame which can further impact mental well-being and financial behavior.

Underestimating Your Liquidity Requirements

Liquidity refers to the ease and speed with which we can convert assets into cash without significant loss of value.

Underestimating liquidity leaves us financially fragile and vulnerable to life’s inevitable surprises. It forces us into reactive, often costly, measures that can quickly unravel years of careful saving and investment, leading to a rapid destruction of wealth. Building and maintaining an adequate emergency fund and understanding our ongoing and potential future cash needs are crucial safeguards at every stage of our financial journey.

Early in your career, unexpected Expenses are inevitable. If all our savings are in illiquid investments and we have no emergency fund, we may need to sell investments at a loss and/or accumulate high-interest debt. Furthermore, a lack of liquidity can prevent us from seizing time-sensitive investment or career advancement opportunities.

Your peak earning years is the life stage that often involves significant financial outlays such as down payments on homes, children’s education, or unexpected family needs. Insufficient liquidity can force early retirement account withdrawals, the need to take out large unfavorable loans, or Delay or forgo crucial investments.

If you are an entrepreneur, underestimating working capital or emergency funds for your business can lead to cash flow crises and potential failure thus wiping out your invested capital.

Either late in your career or during retirement, medical expenses can surge. Without sufficient liquid assets, you might need to prematurely sell appreciating assets, become reliant on family or government assistance, or miss out on enjoying retirement.

The cost of long-term care can be substantial and unpredictable and can quickly deplete retirement savings.

Illiquid estates can also create difficulties and delays in settling affairs, potentially leading to forced sales of assets at unfavorable prices to cover taxes and expenses.

Know How To Differentiate An Asset from A Liability

We need to understand the fundamental characteristics of an asset and a liability and how they impact our financial situation in order to differentiate one from the other.

An asset is something you own or control that has the potential to provide future economic benefit. This benefit can come in the form of cash flow, appreciation in value, or the ability to produce goods or services.

Assets generally put money in your pocket or have the potential to do so and increase your wealth over time.

Liabilities, on the other hand, are a present obligation you have to transfer an economic resource to another party in the future as a result of past events. Essentially, it’s something you owe to someone else. They generally take money out of your pocket to settle the obligation thus resulting in a decrease in wealth.

Some people may view a vehicle as an asset. Whether it is considered an asset depends heavily on perspective and how we define an ‘asset’.

The reason some people view their car as an asset is because it has value and they own it. From a strict financial and wealth-building perspective, however, a personal vehicle often behaves more like a liability or a depreciating asset rather than a true wealth-generating asset.

The reasons why I do not view vehicles as a wealth-destroying mistake is because they depreciate in value over time. They are also an ongoing expense since owning a vehicle involves significant and recurring expenses.

If a vehicle is used for personal use, it generates limited or no income.

A vehicle can be considered an asset if it is used to generate revenue. In addition, certain rare or classic vehicles can appreciate in value over time, making them potential assets from an investment standpoint. This, however, requires specialized knowledge and careful maintenance.

A similar argument can be made that your principal residence is NOT an asset.

Some people view it as an asset because it has a market value that can be sold to generate money. An asset appreciates in value over time.

Stories abound of people currently trying to sell their home because it is no longer affordable and/or they are unable to obtain insurance coverage. What may have been viewed as an asset at one time is no longer an asset. It now drains their finances and is illiquid. In many cases, property owners may no longer able to tap into what they thought was equity.

Your principal residence should not be viewed as an asset. Its primary purpose is as your dwelling. It is not an income generating investment.

Market Timing

The overwhelming evidence suggests that time in the market rather than timing the market is far more effective for long-term wealth creation. This involves:

- Investing consistently: Regularly contributing to your investment accounts.

- Diversifying your portfolio: Spreading your investments across different asset classes.

- Holding for the long term: Riding out market fluctuations and allowing the power of compounding to work.

The allure of perfectly timing the market and making quick profits is strong. Reality, however, is a very different story. Market timing is a high-risk, low-probability strategy for most investors that often leads to significant wealth destruction.

Worthless Education

I define worthless education purely from a financial perspective. This is the type of education that consistently leads to:

- High unemployment rates for graduates.

- Low average salaries compared to the cost of education.

- Lack of demand in the job market.

- Skills that are easily automated or outsourced.

- Limited career progression opportunities.

Education generally has societal and personal benefits beyond monetary value. Pursuing education that does not lead to improved financial outcomes, however, can be a significant drain on resources and a major impediment to wealth accumulation. Careful consideration of career prospects and potential return on investment is crucial.

Does it really make sense to incur hundreds of thousands of student debt to pursue a career where the income potential will lead to years of debt repayment? Even pursuing education in a profession that is in high demand is not a guarantee when it comes to wealth creation.

Don’t ask me. Just ask the 5.3 million defaulted student loan borrowers who are about to have their wages garnished.

Failing To Understand Your Risk Tolerance

Failing to understand your risk tolerance is a potent wealth destroyer because it often leads to emotional and impulsive financial decisions that sabotage long-term growth and security.

If your risk tolerance is low, you fear potential losses and hesitate to invest in growth-oriented assets during a market uptrend. At some point, the fear of missing out (FOMO) may lead to the decision to finally invest when valuations are elevated.

When the inevitable market correction occurs, your low risk tolerance kicks in. Witnessing a decline in the value of your investments may trigger anxiety and fear, leading to impulsive selling to ‘stop the bleeding’. By crystallizing losses, you are unable to participate in any subsequent recovery.

Another outcome from failing to understand your risk tolerance may lead to the allocation of a significant portion of your investments in very low-risk assets. They may offer stability but their returns often struggle to outpace inflation over prolonged periods thus eroding your purchasing power.

At the other end of the spectrum are people who claim to have a high risk tolerance who have no idea what they are doing. These are the types of investors who invest in overly speculative or volatile assets and who chase the latest investment fads. If/when these investments inevitably experience downturns, these investors’ true low risk tolerance surfaces, leading to panic and poor decisions.

In essence, failing to accurately assess your risk tolerance creates a disconnect between your investment strategy and your emotional capacity to handle market fluctuations. This disconnect leads to emotional decision-making, suboptimal asset allocation, and ultimately, the erosion of potential wealth over time.

Improper Diversification

Improper investment diversification exposes investors to the following significant risks that can quickly destroy wealth.

Being overexposed to a single asset or sector or type of investment leaves investors exposed to all investments behaving in unison.

On the other hand, diworsification is the process of adding investments to a portfolio in such a way that the risk-return tradeoff is worsened. It occurs from investing in too many assets with similar correlations that add unnecessary risk to a portfolio without the benefit of higher returns.

In essence, diversifying for the sake of diversifying does not necessarily lower the risk of destroying wealth. Proper diversification entails spreading your risk across different assets, sectors, geographies, and even investment strategies thus increasing the likelihood of capturing gains from various sources and cushioning the impact of losses in any single area.

Reliance on Terrible Debt

Wealth destruction is virtually inevitable when we rely on terrible debt. Examples or terrible debt include, but are not limited to, credit card debt, payday loans, and floor plan financing. Some forms of private debt are also terrible.

In essence, terrible debt is the type of debt where the terms and conditions are onerous.

Surprisingly, some people have no qualms about using various social media platforms to broadcast their level of stupidity. Who in their right mind finances a vehicle for life!? I don’t know if these financing situations are legitimate but there is a plethora of videos in which people disclose ridiculous financing terms.

Mindless Media Consumption

The average American spends an inordinate amount of time watching television and on social media. This differs by age group.

This is time that is devoted to passive consumption rather than productive pursuits.

What separates wealthy individuals from others is their intentional approach to media. Instead of endless scrolling or binge-watching, wealthy individuals align their consumption with their goals. They transform it into a tool rather than a time sink. They listen to educational podcasts during commutes, read industry publications, or use social media strategically for networking and learning rather than entertainment alone.

Limiting social media and redirecting time toward productive activities creates opportunities for wealth-building activities.

Avoid Get Rich Quick Schemes

People who build lasting fortunes avoid investment scams that promise ‘guaranteed returns’ and ‘exclusive opportunities’.

Government lotteries are a huge scam most wealthy individuals avoid. The allure of winning a large sum of money is what entices many people to waste their money. The odds of winning, however, are extremely remote. If government lotteries were incredibly lucrative they would be discontinued.

Wealthy individuals prioritize investment strategies with proven track records. They understand that sustainable wealth comes from value creation, compound growth, and time.

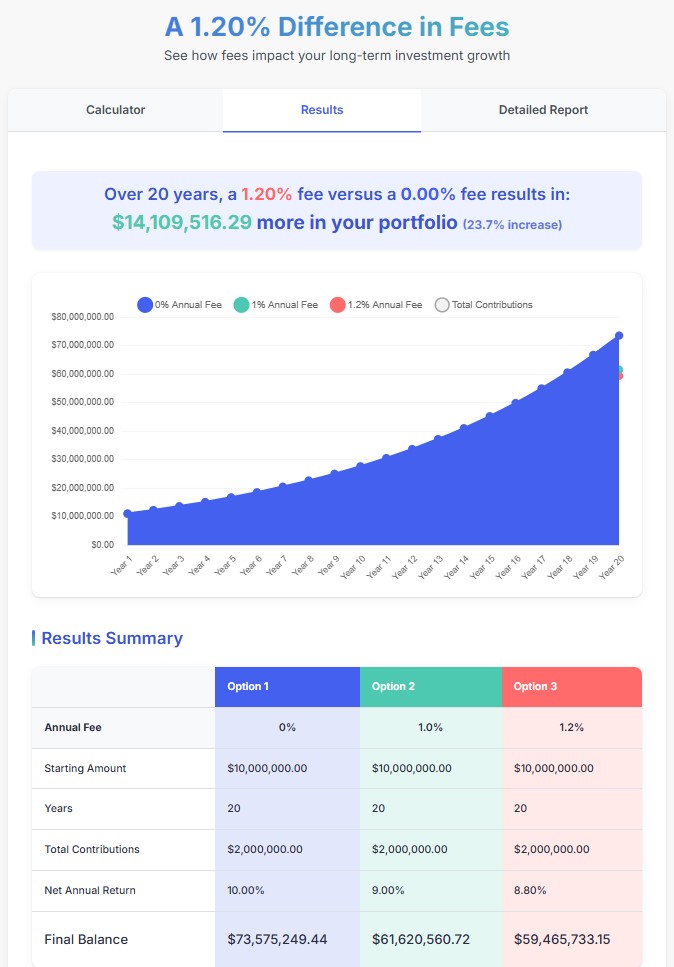

Paying Excessive Fees

A common blunder is paying excessive fees. Because of the power of compounding, the out of pocket expenses and charges can erode the value of your investments by hundreds of thousands of dollars over a lifetime.

Using this calculator, we see the impact fees have on long-term investment growth.

In my example, I use the following metrics:

- Starting amount: $10 million

- Additional annual contributions: $100,000

- Contribution Frequency: Annually at the beginning of every year

- Annual Rate of return: 10%

- Investment Period: 20 years

- Annual Fee scenarios: 0%, 1%, and 1.2%

A 10% annual rate of return before fees over a 20 year time frame might be a stretch. I, therefore, encourage you to use this calculator and to modify the input data as you see fit.

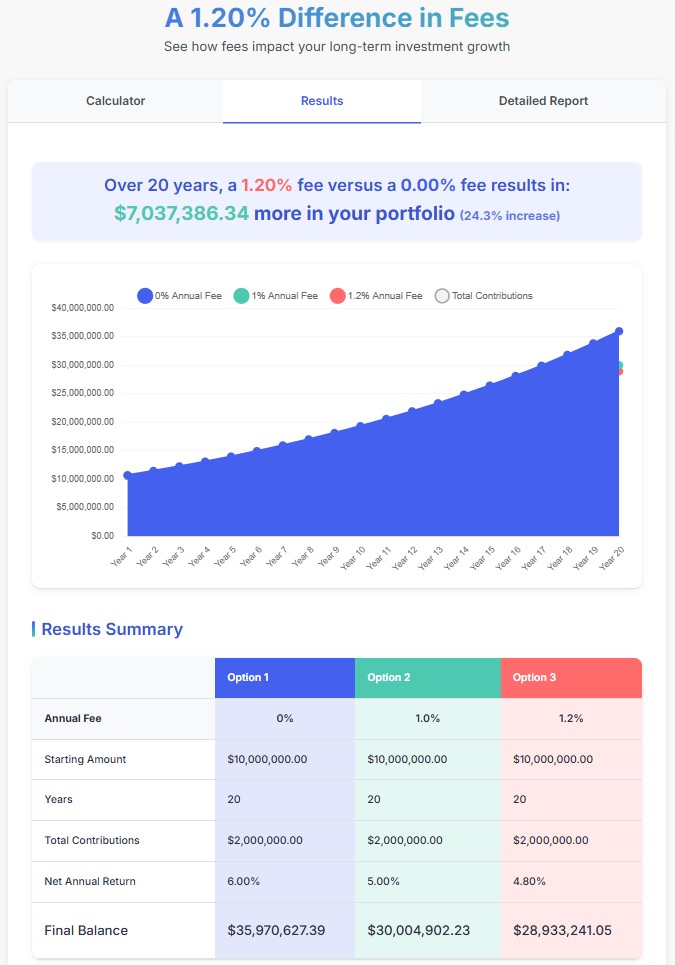

Using the same metrics as those reflected above with the exception that the annual rate of return (before fees) is lowered to 6%, we still see a sizable difference in the portfolio value after 20 years.

Option 1 assumes the investor does not use an advisor, and therefore, fees are kept to a minimum.

The discounted broker I use has various fee structures tailored for different types of investors. The only fees I pay are a $4.99 commission for Canadian and U.S. stock trades. This is regardless of the number of trades per quarter. I trade so infrequently that my annual fee scenario is essentially that reflected in option 1.

Were I to use an investment advisor, I would likely have a tiered fee structure. The fee structure reflected in options 2 and 3 are rough approximations.

I might be wrong but I don’t know if the impact of using an investment advisor is worth the cost.

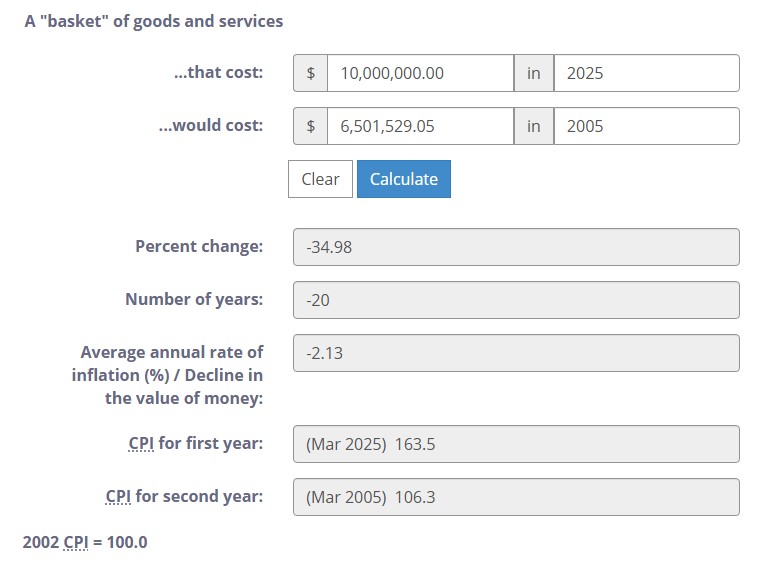

Failing To Account For Inflation

Far too many people fail to account for the erosion in buying power due to inflation.

As a Canadian resident, I turn to The Bank of Canada inflation calculator. I, however, take the results with a ‘grain of salt’; I always think the average annual rate of inflation (%) reflected in the calculator is understated. The rate of inflation used in the calculator is based on a broad base of goods and services. Not everyone, however, consumes goods and services to the same degree.

Since the calculator relies on historical data, I am unable to determine what the value of $10 million in 2025 will be in 2045. I, therefore, use the calculator to determine the value of $10 million in 2025 in terms of 2005 dollars to demonstrate the impact of inflation.

When we consider the considerable deterioration in the value of money over a 20 year span, the results generated from the long-term investment growth calculator is less impressive.

When I view videos of investment advisors on YouTube running through retirement planning scenarios for various clients approaching retirement, I question whether these clients and advisors truly understand the cost of retirement. Naturally, much depends on a clients’ intended lifestyle, future health, and longevity. These are very difficult to forecast, and therefore, retirement planning must be performed for various scenarios (stress test).

Depending on where you end up residing has a huge bearing on whether you will ‘have enough’ during retirement. In our area, independent living in a one-bedroom suite can range from ~$6000 – ~$6500 per month. This jumps to ~$7000 – $8000 per month if assisted living arrangements are required. If a personal support worker is required 24/7, you can tack on another ~$6700 – ~$7500/week.

Everyone’s circumstances are unique. It is not, therefore, my intent to alarm you with these figures. These figures, however, are reality for many Canadians residing in retirement homes.

Lifestyle Creep

In The Millionaire Next Door – The Surprising Secrets of America’s Wealthy by Thomas J. Stanley, Ph.D. and William D. Danko, Ph.D. and The Next Millionaire Next Door – Enduring Strategies For Building Wealth by Thomas J. Stanley, Ph.D. and Sarah Stanley Fallaw, Ph.D., we learn about 4 types of people.

- Low income/low net worth

- Low income/high net worth

- High income/low net worth

- High income/high net worth

Lifestyle creep typically is what causes high income people to have low net worth. For whatever reason, the need to impress others is important to this group of people.

Impressing people you don’t know with the money you don’t have is a surefire way to destroy wealth.

Final Thoughts

We will undoubtedly make good financial decisions during the course of life. This does not, however, mean we are immune from mistakes.

As noted at the outset of this post, my primary reason for sharing my thoughts on wealth-destroying mistakes to avoid is to ultimately help you improve your financial well-being.

Depending on where you reside, the numbers I provide in this post may/may not be realistic for you. As noted earlier, everybody’s circumstances are unique. I, therefore, urge you to use data that may be more relevant to you.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.