I last reviewed Veeva Systems (VEEV) in this August 29, 2024 post at which time the most current financial information was for Q2 and YTD2025. Based on my analysis I opted not to immediately add to my exposure.

On November 7, VEEV held its 2024 Investor Day at which time management disclosed its ambitious target of doubling annual to revenue to $6B by FY2030 while maintaining at 35%+ non-GAAP Operating Margin. VEEV’s share price rocketed higher following this Investor Day. Fortunately, the share price pulled back and I acquired another 100 shares @ ~$210 on November 19 bringing my VEEV exposure to 500 shares in the FFJ Portfolio; I disclose this purchase in my November 23 post.

After the December 5 market close, VEEV released its Q3 and YTD2025 results. As I compose this post on December 6, VEEV’s share price has surged to ~$254. Let’s see how the the increase in the share price and the updated guidance impacts VEEV’s valuation.

Business Overview

VEEV is the leading provider of industry cloud solutions for the global life sciences industry. Its offerings span cloud software, data, and business consulting and are designed to meet customers’ unique needs and their most strategic business functions ranging from R&D through commercialization. These solutions help life sciences companies develop and bring products to market faster and more efficiently, market and sell more effectively, and maintain compliance with government regulations.

The best way to learn about the company is to review the company’s website and Part 1 in the most recent Form 10-K found in the SEC Filings section of the company’s website.

Financial Review

Q3 and YTD2025 Results (VEEV has a January 31 FYE)

Material related to the Q3 2025 earnings release is accessible here.

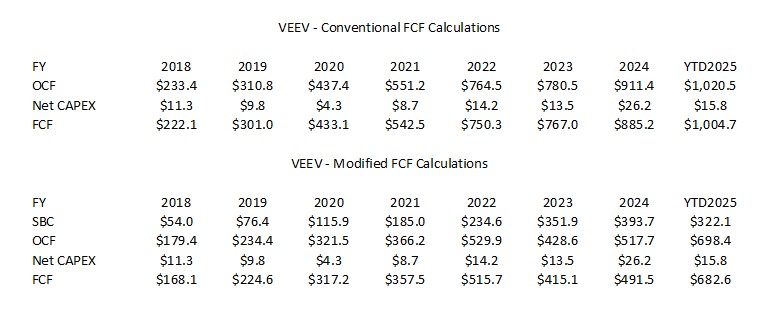

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

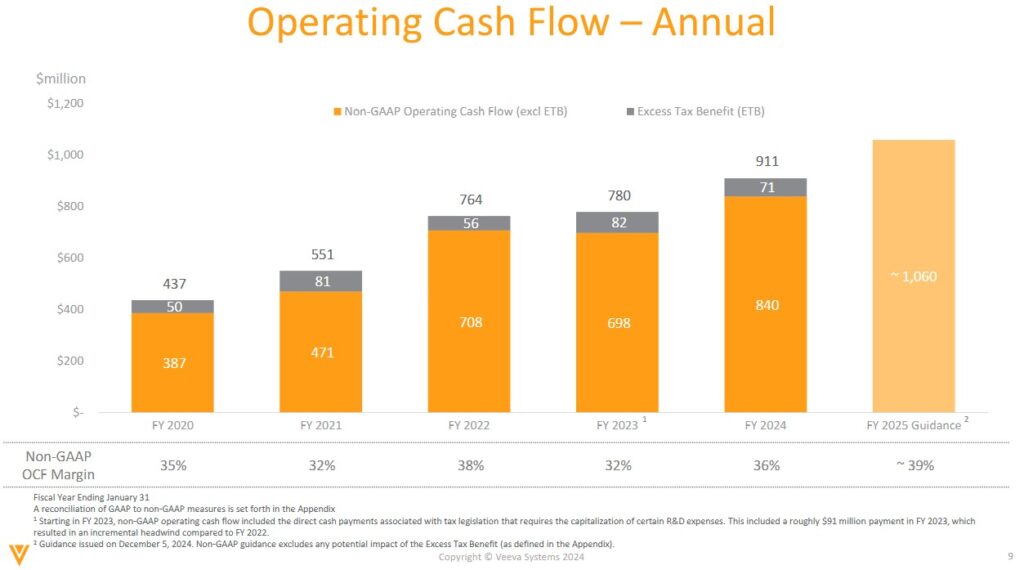

VEEV’s reports the following annual OCF over the past few years.

In my November 26 Zoom Communications (ZM) post, I provide my rationale for adjusting a company’s OCF and FCF to account for stock-based compensation (SBC).

Many technology companies reward their employees with SBC. Some companies (Salesforce, Workday, and Zoom for example) are scaling back the extent to which they issue SBC because the growth in issued and outstanding shares is not sustainable.

VEEV’s CEO is on ZM’s Board. He very likely had input in ZM’s decision to scale back ZM’s SBC. I suspect VEEV may eventually also scale back its SBC at some point.

If VEEV were to completely replace its SBC with wages and salaries, these wages and salaries would not be added back in the Consolidated Statement of Cash Flows. By relying on SBC as part of its employee compensation, OCF is inflated.

Deducting VEEV’s annual SBC from OCF, we see a substantial difference in FCF using the conventional and modified methods.

FY2025 Outlook

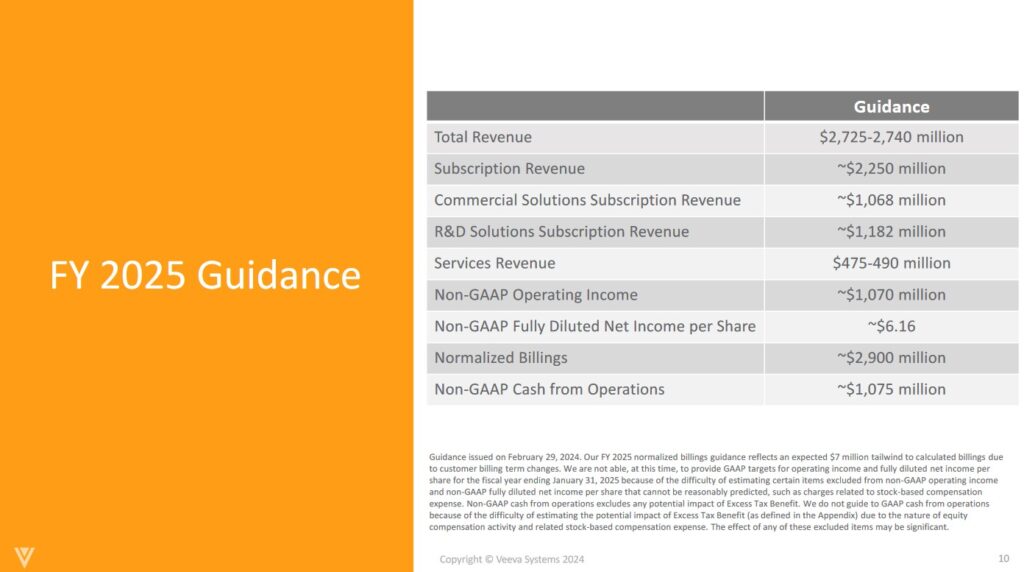

The following reflects VEEV’s FY2025 guidance when it released its Q4 and FY2024 results on February 29, 2024.

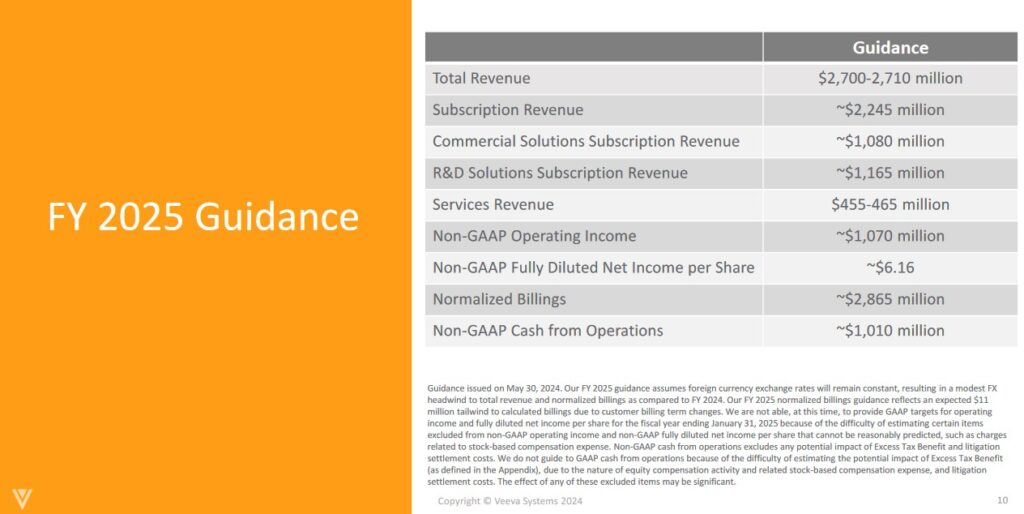

The FY2025 guidance was subsequently revised with the release of Q1 2025 results on May 30, 2024.

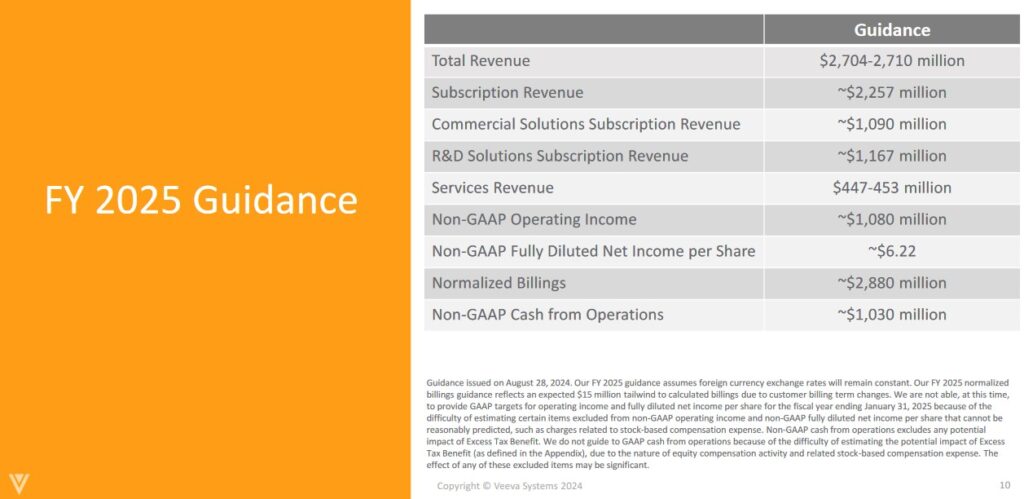

The FY2025 guidance was subsequently revised with the release of Q2 2025 results on August 28, 2024.

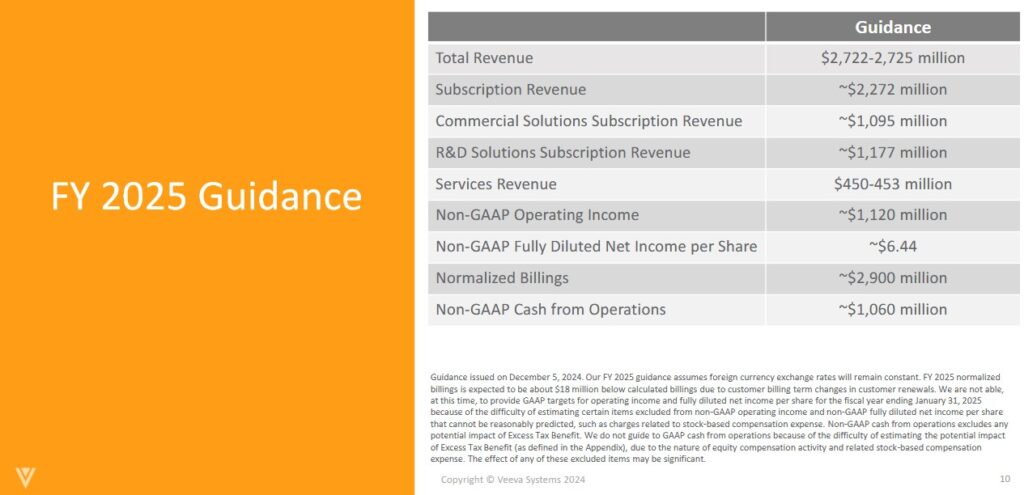

The most current guidance released with Q3 and YTD2025 results is as follows.

Risk Assessment

VEEV has no debt to rate.

At the end of Q3, VEEV had ~$1.045B in cash and cash equivalents and ~$4.018B in short-term investments for a total of ~$5.063B.

Its total liabilities were ~$0.951B of which ~$0.740B was deferred revenue leaving ~$0.211B in all other liabilities; deferred revenue represents funds received from clients in advance in services being provided.

VEEV satisfies my risk-averse investor profile.

Dividends and Dividend Yield

VEEV does not distribute a dividend.

The weighted average number of diluted shares outstanding (in millions rounded) in FY2021 – 2024 is 160.7, 162.2, 162.4, and 163.5. In Q3 2025 this was ~164.979.

VEEV typically does not repurchase shares to offset the shares it issues annually as part of its employee compensation structure.

Valuation

My estimate of VEEV’s valuation at the time of prior posts can be found in my August 29, 2024 post.

As I compose this post on December 6, the share price is ~$254. On November 19, I acquired another 100 shares @ ~$210. Has VEEV fundamentally changed in roughly half a month to warrant a ~$44 share price increase? I think not.

Using the current ~$254 share price and management’s FY2025 revised adjusted diluted EPS guidance of ~$6.44 (raised from ~$6.22) gives us a forward adjusted diluted PE of ~39.4.

Some of the brokers are currently increasing their earnings estimates and I anticipate further changes over the coming weeks. For now, however, the following are VEEV’s forward adjusted diluted PE levels using the current broker estimates and a ~$254 share price.

- FY2025 – 30 brokers – mean of $6.29 and low/high of $4.27 – $6.53. Using the mean estimate, the forward adjusted diluted PE is ~40.4.

- FY2026 – 30 brokers – mean of $6.85 and low/high of $5.18 – $7.26. Using the mean estimate, the forward adjusted diluted PE is ~37.1.

- FY2027 – 21 brokers – mean of $7.65 and low/high of $6.01 – $8.28. Using the mean estimate, the forward adjusted diluted PE is ~33.2.

These valuations are higher than the ~35.5, ~32.2, and ~29.3 when I wrote my August 29, 2024 and the share price was ~$218. Furthermore, these valuations are even higher than when I purchased shares on November 19 at which time my purchase price was ~$210.

In the first 3 quarters of FY2025, VEEV’s FCF was ~$1.005B when we do not deduct SBC. If VEEV generates a similar amount of FCF in Q4 as it generated on average in the first 3 quarters, it should generate ~$1.34B of FCF in FY2025.

The diluted weighted average shares outstanding in FY2024 was 163.486 million and in Q3 2025 it had risen to 164.979 million. Let’s be conservative and estimate 164.5 million as being the weighted average for FY2025.

Divide ~$1.34B by 164.5 million and we get ~$8.15 of FCF/share. Divide the current ~$254 share price by ~$8.15 and the forward P/FCF is ~31.2.

VEEV’s valuation changes dramatically for the worse if we use the modified FCF where we deduct SBC.

In the first 3 quarters of FY2025, VEEV’s FCF was ~$0.683B when we deduct SBC. If VEEV generates a similar amount of FCF in Q4 as it generated on average in the first 3 quarters, it should generate ~$0.911B of FCF in FY2025.

Using 164.5 million as the weighted average number of shares outstanding for FY2025, we divide ~$0.911B by 164.5 million and get ~$5.54 of FCF/share. Divide the current ~$254 share price by ~$5.54 and the forward P/FCF is ~45.8.

Final Thoughts

Veeva continues to generate strong results and I like its long-term outlook. Unfortunately, we continue to experience a period of irrational exuberance. Many investors appear to be making investment decisions solely on the news of the day and share price behavior.

I can not justify add to my exposure at the current valuation and shall bide my time in the hopes of an improved valuation.

When I completed my 2024 Mid Year FFJ Portfolio Review, VEEV was not a top 30 holding. It is likely a top 30 holding at the moment. I will not know for certain, however, until I complete a similar portfolio review at the end of 2024.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long VEEV.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.