When I last reviewed Paychex (PAYX) in this March 27, 2025 post, the most current financial information was for Q3 and YTD2025. The March 26, 2025 closing share price was ~$150.20 and I thought a fair value was in the low-mid ~$130s.

When I last reviewed Paychex (PAYX) in this March 27, 2025 post, the most current financial information was for Q3 and YTD2025. The March 26, 2025 closing share price was ~$150.20 and I thought a fair value was in the low-mid ~$130s.

Fast forward to November 5, 2025. We now have PAYX’s Q1 2026 results that were released on September 30. With the current valuation being far more attractive, I have acquired an additional 100 shares @ ~$115.77 in a ‘Core’ account in the FFJ Portfolio.

Business Overview

Please review the company’s website and Part 1 in the company’s Form 10-K.

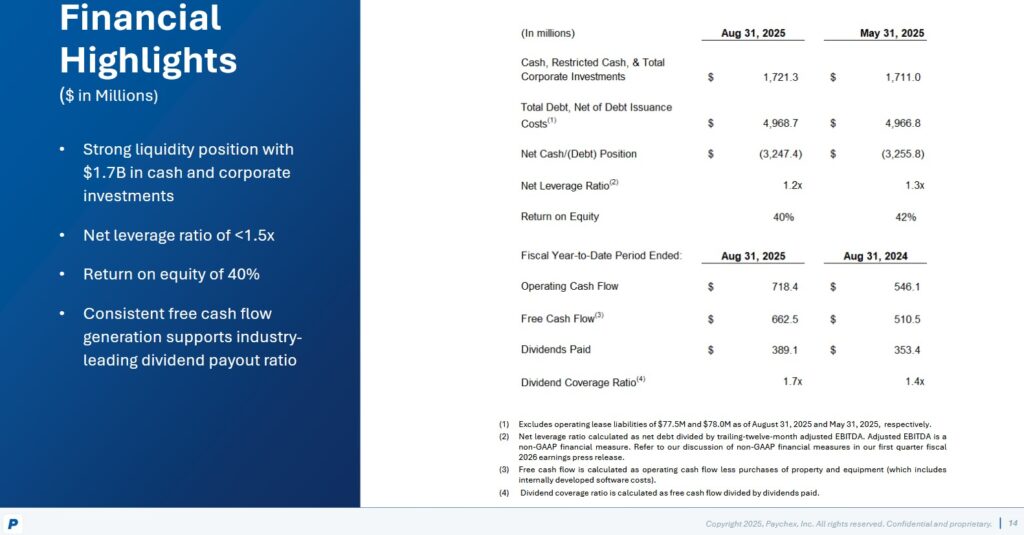

Financial Review

Q1 2026 Results

PAYX’s Q1 2026 and FY2026 outlook are accessible here.

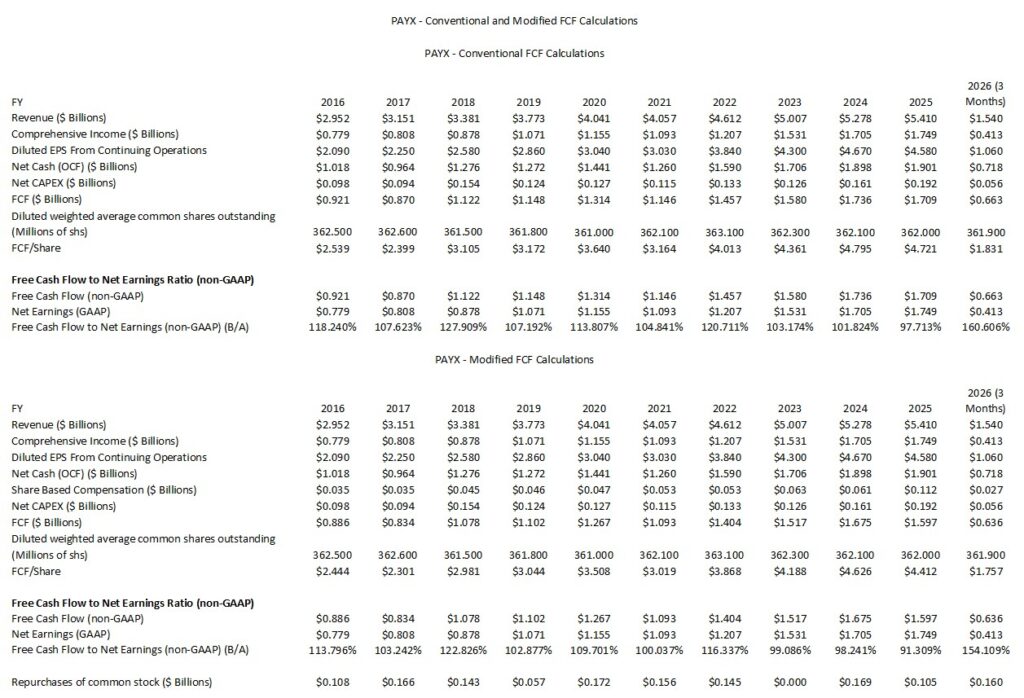

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

The following reflects PAYX’s FCF using the conventional and modified methods. The modified method deducts share-based compensation (SBC) from OCF.

NOTE: I caution not to read too much into the YTD2026 FCF/EPS ratios. As FY2026 progresses, we are likely to witness a regression to the mean. A 1:1 FCF/EPS ratio by the end of FY2026 is likely.

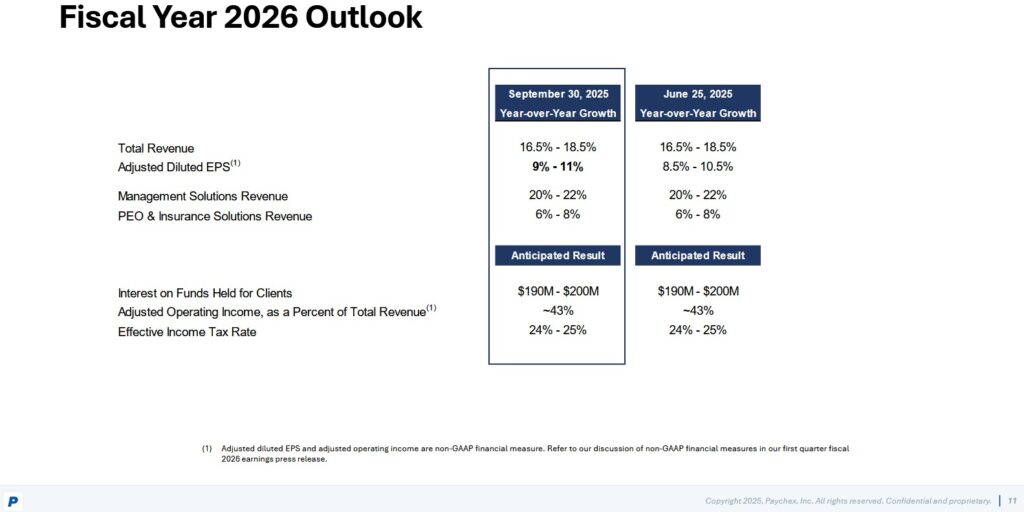

FY2026 Outlook

With the release of Q1 2026 results, we see that PAYX has modestly increased its FY2026 adjusted diluted EPS.

In FY2025, PAYX generated $4.98 of adjusted diluted EPS. Using the 10% growth mid-point outlook, PAYX’s FY2026 adjusted diluted mid-point is likely to be ~$5.478.

Risk Assessment

On March 31, 2025, just days after my prior post, Moody’s and S&P Global initiated PAYX ratings.

Moody’s assigns a Baa1 rating while S&P Global assigns a BBB+ rating.

Both ratings are the top tier of the lower medium grade category. These ratings define PAYX as having an adequate capacity to meet its financial commitments. adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity to meet its financial commitments.

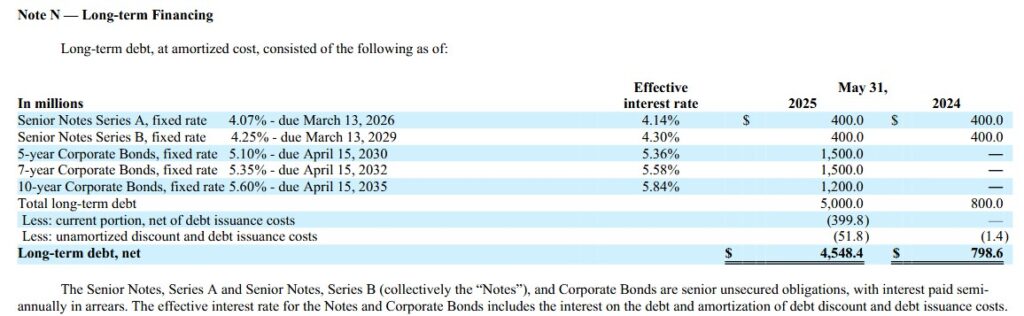

The following is PAYX’s schedule of long-term debt at FYE2024 and FYE2025. There is very little change in the Q1 2026 levels from those at FYE2025.

PAYX is a conservatively managed company. I envision management will continue to structure its finances so its credit ratings do not deteriorate.

Dividends

PAYX’s dividend history is accessible here.

Do not rely on the posted dividend yields on various stock screeners. Investors holding PAYX shares in tax efficient accounts will get a different yield from non-US residents who hold shares in taxable accounts.

My suggestion is to pay little regard to dividend metrics. Focus on an investment’s total potential investment return.

Share repurchases are not a capital allocation priority. PAYX maintains a program to repurchase $0.4B of its common stock, with authorization expiring May 31, 2027. The purpose of this program is to manage common stock dilution.

Share repurchases being low on the list of capital allocation priorities has been beneficial because shares have typically been overvalued for decades. They were, however, briefly undervalued and/or fairly valued through most of 2022 – 2024.

Now that shares are undervalued, this is be an opportune time for PAYX to repurchase shares. PAYX, however, is unlikely to aggressively repurchase shares since it is scheduled to repay ~$0.4B of debt on March 13, 2026.

The next long-term debt repayment is scheduled for March 13, 2029. Perhaps PAYX might be more aggressive with its share repurchases after the March 13, 2026 debt repayment. Much will, however, depend on PAYX’s valuation and what other priorities management has when it comes to capital allocation.

Valuation

On November 5, 2025 I acquired an additional 100 shares @ $115.77 in a ‘Core’ account in the FFJ Portfolio.

Management’s FY2025 outlook calls for a ~9% – ~11% increase from the $4.98 FY2025 adjusted diluted EPS. Using a 10% increase, we get ~$5.478 adjusted diluted EPS in FY2026.

If we use my purchase price and ~$5.478, the forward adjusted diluted PE is ~21.1.

Using the current forward adjusted diluted EPS broker estimates, the following are PAYX’s forward adjusted diluted PE levels:

- FY2026 – 15 brokers – mean of $5.47 and low/high of $5.40 – $5.55. Using the mean estimate, the forward adjusted diluted PE was ~21.2.

- FY2027 – 16 brokers – mean of $5.89 and low/high of $5.76 – $6.03. Using the mean estimate, the forward adjusted diluted PE was ~19.7.

- FY2028 – 6 brokers – mean of $6.23 and low/high of $6.11 – $6.43. Using the mean estimate, the forward adjusted diluted PE was ~18.6.

I think the Q1 2026 FCF conversion ratio (see above) is likely to retrace to ~101% and ~98% as FY2026 progresses (conventional and modified calculations). PAYX’s valuation on a P/FCF basis should, therefore, be relatively similar to its P/E valuation.

I reflected the following assessment of PAYX’s valuation in my prior post:

We now know that in the first 3 quarters of FY2025, PAYX generated $3.76 of diluted EPS and $3.79 of adjusted diluted EPS. The acquisition of PYCR in April 2025 is expected to have minimal impact on PAYX’s adjusted diluted earnings in FY2025.

If PAYX generates a comparable level of earnings in Q4 as in the prior 3 quarters, we can expect diluted EPS and adjusted diluted EPS in FY2025 to be ~$5.00 and ~$5.05. Using the ~$150.20 March 26 closing share price, the forward diluted PE and forward adjusted diluted PE are ~30 and ~29.7.

PAYX’s valuation based on adjusted diluted earnings broker estimates and the current share price is:

- FY2025 – 17 brokers – mean of $4.98 and low/high of $4.73 – $5.06. Using the mean estimate, the forward adjusted diluted PE is ~30.2.

- FY2026 – 17 brokers – mean of $5.30 and low/high of $5.00 – $5.61. Using the mean estimate, the forward adjusted diluted PE is ~28.3.

- FY2027 – 12 brokers – mean of $5.62 and low/high of $5.38 – $5.86. Using the mean estimate, the forward adjusted diluted PE is ~26.7.

I anticipate changes to the broker estimates over the coming days.

In the first 9 months of FY2025, PAYX’s FCF was ~$3.94 and ~$3.80 calculated under the conventional and modified methods. If it generates a comparable amount of FCF in Q4 as in the first 3 quarters of FY2025, I anticipate FY2025 FCF of ~$5.25 and ~$5.07. Using the ~$150.20 March 26 closing share price, PAYX P/FCF is ~28.6 and ~30 .

Final Thoughts

There are multiple instances of major companies announcing a headcount reduction. These headlines are likely spooking some investors thus resulting in the deterioration in the share price of Automatic Data Processing (ADP), Paychex (PAYX), and Paycor (PAYC). All 3 are existing holdings in the FFJ Portfolio.

I view this as good news because my investment time horizon is well beyond a few years. Over the long-term, I envision these companies will be more valuable than they are today.

I am a PAYX shareholder since July 2, 2009. It was my 27th largest holding when I completed my 2025 Mid-Year Portfolio Review.

Based on my experience, shares are generally overvalued. Now that shares are undervalued, I have acquired an additional 100 additional shares on November 5 @ $115.77. My PAYX exposure is now 957 shares (498 and 459 shares in a ‘Core’ and a ‘Side’ account, respectively).

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long PAYX, ADP, and PAYC.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.