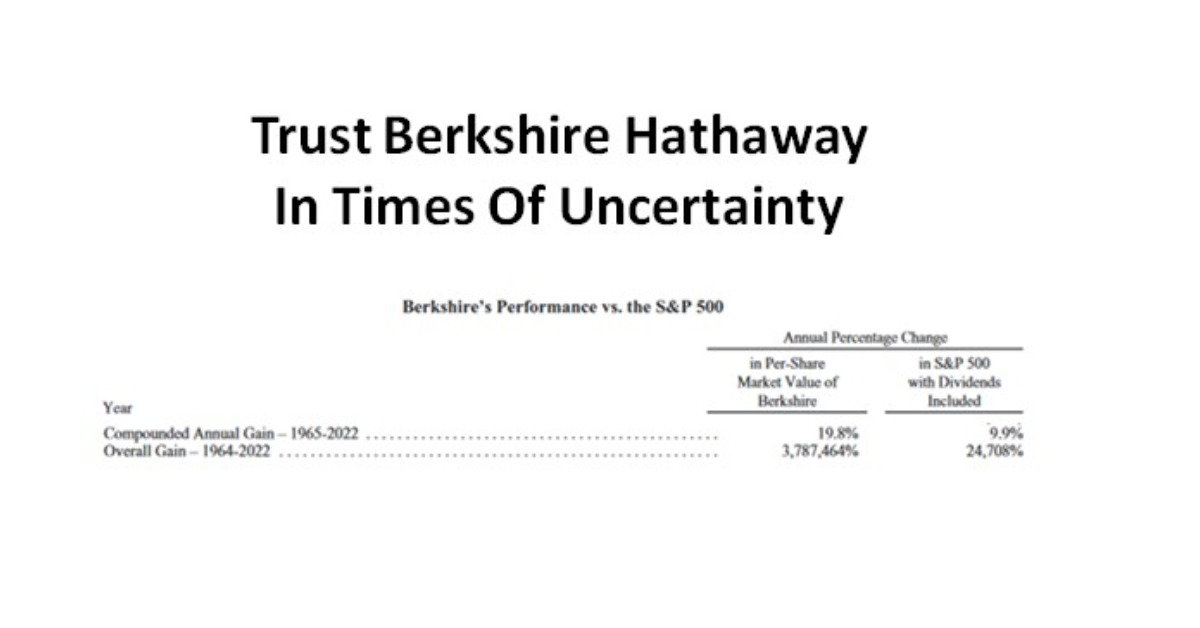

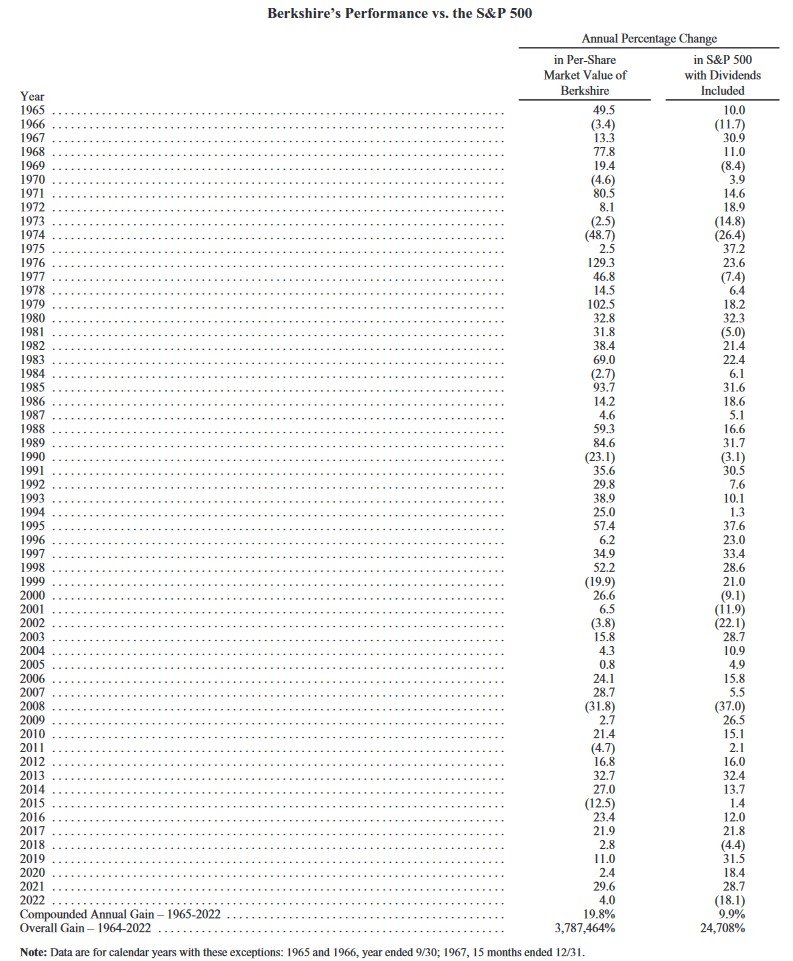

I can’t think of a more fitting image for this post than to show how Berkshire Hathaway (BRK) has performed relative to the S&P500 (with dividends included) in just under 60 years.

For several years I have trusted BRK in times of uncertainty. Now that I am helping a couple of young investors with minimal investment knowledge, I am suggesting they also trust BRK to help them achieve their financial objectives and goal.

I last reviewed BRK in this May 4, 2022 post; my thoughts about BRK as a long-term investment remain the same.

The Case Against Mutual Funds and ETFs

Neither of these young investors is in a position to be analyzing financial statements. While I do help them identify great companies in which to invest, I want them to have investment portfolios where they do not have to rely on my recommendations.

Some investors may suggest these young investors invest through mutual funds. I completely disagree and have a strong opinion about how little value many (most) mutual funds truly bring to the table.

Companies which manage mutual funds are in the business of making money. They are essentially a layer between the value of the underlying businesses held in the funds they manage and the mutual fund investor.

Ask any mutual fund manager if they are willing to waive all fees if they underperform specific benchmarks. I doubt many would find this to be an acceptable arrangement.

Next, many mutual funds have holdings that, in my opinion, belong in the ‘scrap heap’.

Who in their right mind, for example, would remotely consider investing in Carvana (CVNA)? 514 institutional owners and shareholders that have filed 13D/G or 13F forms with the Securities Exchange Commission (SEC) disclosing holdings totalling 137,444,123 shares have seen fit to invest in a company in which one of the majority shareholders has a criminal record.

Think this is an isolated case? Not a chance. 415 institutional owners and shareholders have filed 13D/G or 13F forms with the Securities Exchange Commission (SEC) in which they disclose holding a total of 149,627,610 Nikola (NKLA) shares. NKLA is a company that can’t manufacture an electric-powered truck so they resort to filming a truck rolling down a hill which gives viewers the impression the truck is on a flat surface; Hindenburg exposed NKLA as an outright fraud on September 10, 2020. Trevor Milton, the founder of NKLA, was found guilty of fraud in October 2022 and while new management is desperately trying to remake NKLA into a legitimate company, the odds are greatly stacked against them. However, 415 institutional owners and shareholders remain delusional despite NKLA having the dubious distinction of reporting losses of ~$1.845B in FY2020 – FY2022.

Another train wreck is Clover Health Investments (CLOV). A little bit of research about the company and its founders sets off ‘red flags’. This company has incurred losses of $1.063B in FY2020 – FY2022. Nevertheless, 288 institutional owners and shareholders that have filed 13D/G or 13F forms with the Securities Exchange Commission (SEC) in which they see fit to hold a total of 131,500,214 Clover Health Investments (CLOV) shares.

Institutions which have been entrusted with the responsibility of managing investor money should not remotely consider investing in the companies referenced above. However, we see that the likes of BlackRock, State Street, Vanguard, Goldman Sachs, and PNC Financial Services have invested in these companies. These firms’ investors suffer a permanent erosion of their capital. The investment managers, while they also take a hit because the assets under management (AUM) drop in value, continue to collect fees despite having invested in outright frauds or companies where a little bit of analysis should have set off the alarm.

Other investors may argue that a broad-based Exchange Traded Fund (ETF) is appropriate for these young investors as opposed to mutual funds. Looking at the holdings in BlackRock’s iShares Core S&P 500 ETF (IVV), I see several companies in which I would not remotely consider investing. General Motors (GM), Ford Motor Company (F), Moderna (MRNA), 3M (MMM), and Boeing (BA) are just a few of the companies that should be avoided.

The Case For Investing in Berkshire Hathaway

‘You’re looking for three things, generally, in a person. Intelligence, energy, and integrity. And if they don’t have the last one, don’t even bother with the first two.’

– Warren Buffett – Chairman and CEO, Berkshire Hathaway

I can not comment on the intelligence and energy of the founder of CVNA, NKLA, and CLOV. From the research I have conducted on these companies, however, the integrity aspect appears to be completely absent. When a founder of a company is intelligent and has a considerable amount of energy but no integrity, there is a very strong probability this individual will rob you blind.

To date, I have found nothing to suggest that I should question the integrity of Warren Buffett and Charlie Munger (Vice Chairman of Berkshire Hathaway).

Business Overview

BRK is a holding company that owns subsidiaries engaged in a large number of diverse business activities. The most important of these are primary and reinsurance businesses, a freight rail transportation business (BNSF Railway), and a group of utility and energy generation and distribution businesses. It also owns and operates numerous other businesses engaged in a variety of activities.

The best way to learn about BRK is to read the Chairman’s Letter to Shareholders and Part 1 of the FY2022 Form 10-K.

Historical Performance

Past results do not predict future performance. I feel far more comfortable investing in a company, however, whose overall gain over a ~60-year timeframe far exceeds that of the S&P500 (with dividends reinvested) than I would if the historical performance was reversed.

It is not unreasonable to question how BRK will perform once Buffett and Munger are no longer in the picture. After all, Buffett was born on August 30, 1930 and Munger was born on January 1, 1924 and they can’t live forever.

Both Buffett and Munger, however, have often reassured investors that the team designated to assume their respective roles and responsibilities are trustworthy and quite capable. I can only take their word that BRK will continue to perform how investors have come to expect.

Diversification

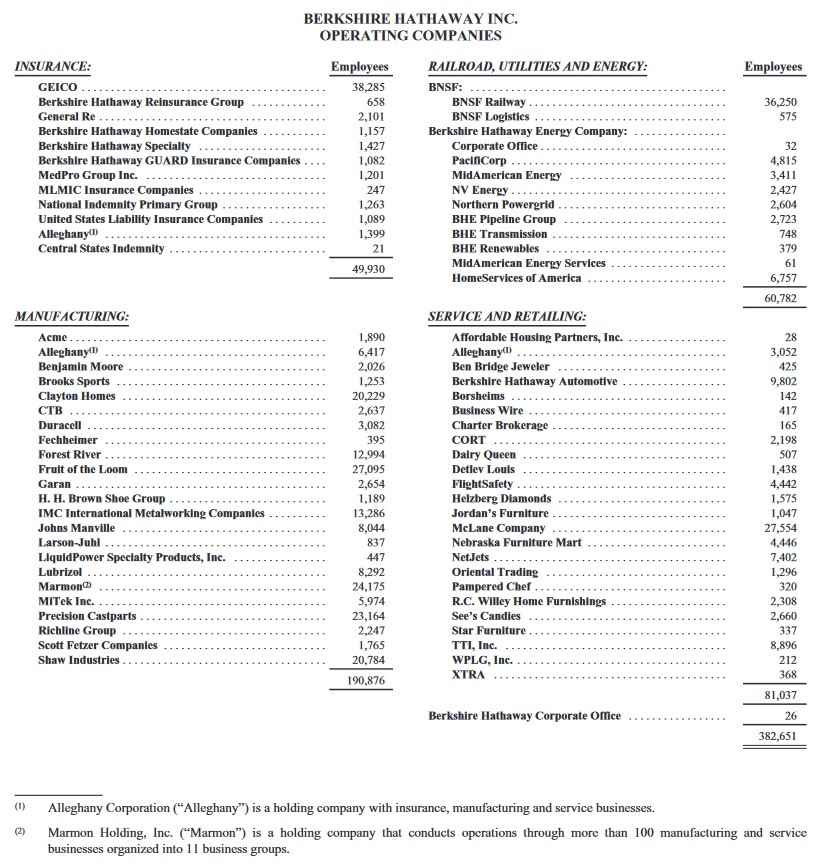

BRK is comprised of hundreds of legal entities. The following table, however, lists the Operating Companies within the group. None of these companies are publicly traded so a mutual fund or ETF investor can not acquire shares in any of these companies.

This page on BRK’s website provides links to the companies reflected above.

We also see from the most recent Form 13-F filing on the Securities and Exchange Commission (SEC) website that BRK has extensive investments in publicly traded companies.

BRK also owns 100% of New England Asset Management (NEAM). This entity also has extensive investments in multiple publicly traded companies.

By investing in BRK-b, the young investors I am helping on their journey to financial freedom benefit from exposure to a host of companies that give them broad exposure to the global economy.

Financials

Q4 and FY2022

BRK’s FY2022 Form 10-K is accessible here and its Earnings Release is accessible here.

While BRK reported a ~$22.82B net loss on a GAAP basis, I caution you that an accounting rule requires BRK to report unrealized gains and losses (a ~$67.9B loss in FY2022).

A GAAP rule imposed in 2018 requires a company holding equity securities to include in earnings the net change in the unrealized gains and losses. These unrealized gains and losses are paper losses and not actual realized gains and losses that come from the sales of the securities.

Because of the accounting rule change, BRK’s reported net earnings have become significantly more volatile because of fluctuations in the stock market and not because of major shifts in the company’s operations. Buffett urges investors to ignore such gains and losses.

FY2023 Guidance

BRK’s management does not provide guidance.

Credit Ratings

In my The Importance Of Margin Of Safety post, I state that every investment carries a degree of risk. It is up to the investor to determine if the potential investment return outweighs the potential risks.

BRK is a conglomerate overseen by a small group of highly sophisticated investors who properly assess risk/reward!

BRK’s unsecured long-term debt credit ratings are unchanged from my last review.

- Moody’s: assigns an Aa2 rating.

- S&P Global assigns an AA rating.

- Fitch assigns an AA- rating; this rating is one notch lower than that assigned by Moody’s and S&P.

All 3 ratings are high-grade investment-grade credit ratings and define BRK as having a VERY STRONG capacity to meet its financial commitments. It differs from the highest-rated obligors (AAA) only to a small degree.

Dividends and Share Repurchases

Dividend and Dividend Yield

BRK does not distribute a dividend.

Share Repurchases

BRK’s common stock repurchase program permits it to repurchase its Class A and Class B shares any time that Warren Buffett, Chairman of the Board and Chief Executive Officer, and Charlie Munger, Vice Chairman of the Board, believe that the repurchase price is below the company’s intrinsic value, conservatively determined. The program allows share repurchases in the open market or through privately negotiated transactions and does not specify the maximum number of shares to be repurchased. However, repurchases will not be made if they would reduce the total value of BRK’s consolidated cash, cash equivalents and U.S. Treasury Bills holdings below $30B. The repurchase program does not obligate BRK to repurchase any specific dollar amount or number of Class A or Class B shares and there is no expiration date to the program.

For many years, BRK never repurchased shares. In FY2018, however, BRK embarked on a repurchase program. The ramp-up in share repurchases is because management felt BRK was undervalued at a time when other companies were grossly overvalued.

- FY2018 – $1.346B

- FY2019 – $4.85B

- FY2020 – $24.706B

- FY2021 – $27.061B

- FY2022 – $7.854B

Valuation

I pay almost no attention to BRK’s valuation for reasons explained in Warren Buffett’s FY2020 Letter to Shareholders (starts on page 5 of 148).

Final Thoughts

I remain confident in BRK’s ability to continue to reward long-term shareholders despite the probability that Buffett and Munger will not be around for many more years. As a result, I encouraged a young investor to acquire several more BRK-b shares @ $297/share on March 24.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BRK-b.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.