As a follow up to my Investing Should be Like Watching Paint Dry post, this post provides tips to achieve investment success. Success, however, can be as much about what to do as it is what not to do because our emotions lead us to make decisions that are not always rational.

The following are a few rules to follow to ‘come out ahead’.

Never Lose Money

Warren Buffett and Charlie Munger of Berkshire Hathaway boil down investing into two very simple rules.

- Rule #1 – Never lose money

- Rule #2 – Never forget rule #1

Losses hurt our future earning power. The more money working on our behalf, the greater probability we have of making more money.

These two rules communicate the need to look at the potential downsides and upsides of an investment with a focus on potential downsides being a priority.

Think Like An Owner

Our mindset should be that of a business owner when we acquire shares in a business.

Many investors treat stock investing like gambling. Shares in a company, however, represent a fractional ownership interest in a business. Depending on how a company performs over time, the company’s stock performance is likely to follow the direction of its profitability. This is why we must be fully aware of our motivation when investing.

Investing involves an analysis of fundamentals, valuation, and an opinion about how the business will perform in the future. In addition to assessing a company’s financial and competitive positions, we must also determine if the management is strong and that their interests are aligned with those of shareholders.

Stick To An Investing Process That Works For You

Develop and stick to an investing process that works for you regardless of market conditions.

If you have the time and the willingness to delve into the details, then use that strength.

Not everyone, however, has the desire or the time to read SEC Filings and research a company. Investors with neither the interest nor time to conduct proper analysis may be best served by investing through exchange traded funds.

Buy When Others Are Fearful

Bargains arise when the majority of investors become fearful.

‘Be fearful when others are greedy, and greedy when others are fearful.’ – Warren Buffett

Invest in great companies when they fall out of favor because of circumstances that do not permanently impair the business.

Remain Disciplined

Save and invest through good and tough times. This forces us to live below our means.

Diversify But Only Up To A Point

Highly experienced investors might be able to hold a very concentrated portfolio. Most retail investors, however, should maintain a reasonable level of diversification.

The level of diversification depends on a host of factors. As a result, the extent to which one investor diversifies their portfolio might be completely inappropriate for another investor.

Diversification is good but up to a point. Once diversification reaches the stage where it is somewhat like throwing mud against a wall, it is time to scale it back.

An investor with a $300,000 portfolio spread over 100+ companies, for example, may want to give their head a shake. The same applies for an investor with a portfolio with significant exposure to one industry.

Similarly, if an investor has very significant exposure to the shares of their employer, it would be prudent to consider some diversification.

I know people who were employed with Nortel during the dot com period. A significant component of their net worth was tied up in Nortel shares. They were downsized and their Nortel investment tanked.

I also know long time BCE employees who have accumulated a significant number of BCE shares over the years. In April 2022, BCE shares reached a high of ~$73. As I compose this post on February 12, 2025, shares trade @ ~$33 (no, there has been no stock split). The dividend yield? Almost 12.4%. A dividend cut is virtually guaranteed.

Timing The Market Is A Fool’s Game

Time is your greatest ally. Stay invested. Do not frequently enter and exit your investments.

Fight emotion with discipline and invest regularly over time. Do not try to anticipate market conditions.

Understand Your Investments

Do not invest in any investment product or any company you do not fully understand. Look at the potential downsides and ensure the risks of the investment are clearly disclosed to you before investing. If you intend to invest in a company, know why it makes sense to do so.

Regularly Review Your Investment Plan

Circumstances in life change, and therefore, it is imperative that we review our investment plan at least annually.

I am at the life stage where circumstances do not change dramatically from year to year. Nevertheless, I have a discussion with our tax accountants twice a year.

Maintain An Emergency Fund

We are susceptible to making irrational financial decisions during periods of financial stress. Reduce the risk of financial stress by having an emergency fund. This reduces the risk of making financial decisions that upend long-term investment plans.

Some advisors recommend keeping 5% – 10% of total assets in cash. This is extremely simplistic and does not take into consideration a host of factors that influence what is a reasonable/unreasonable amount.

The amount held in an emergency fund will differ for everyone and depends on a host of factors (eg. income stability, family dynamics, health conditions, economic conditions, etc.).

A cash flow analysis will aid in the creation of an emergency fund that is appropriate for your circumstances.

Do Not Ignore The Impact Of Inflation

Evaluate the after tax rate of return of your investments relative to the rate of inflation.

Inflation wreaks havoc on the value of our investments. Investors holding investments generating a rate of return similar to the rate of inflation are essentially ‘treading water’.

Understand the risk/return trade-off

The greater the potential return, the greater the risk.

The U.S. Securities and Exchange Commission (SEC) defines risk as ‘an investor’s ability and willingness to lose some or all of an investment in exchange for greater potential returns.’

When assessing our personal risk tolerance, we must assess our ability AND willingness.

Quite often, we tend to focus just on willingness or our comfort level with risk. Our ability to assume risks based on our personal financial situation, however, is equally important.

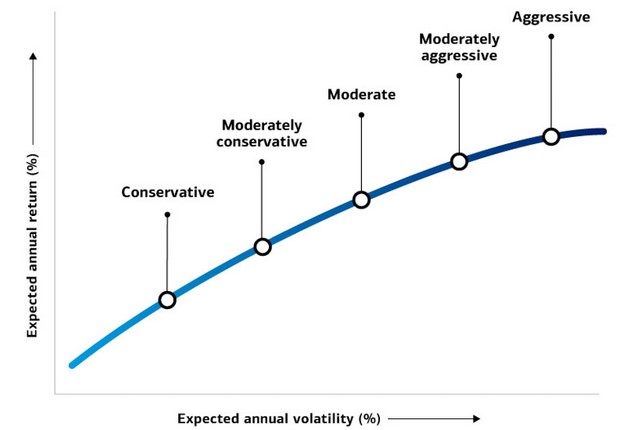

Source: Merrill – A Bank of America Company

In considering the pursuit of greater potential returns, we must determine our level of comfort should the investing environment become more volatile.

As noted earlier, our respective circumstances are unique. What may be an appropriate investment strategy for one investor may be totally inappropriate for another even though, on the surface, the circumstances appear similar.

Our willingness to take risk is subjective. Our ability to take risk, however, will shift as our circumstances change.

Factors to consider when determining our ability to assume risk include:

Liquidity requirements

A host of factors impact our risk tolerance. Income stability is important. It is essential, however, to consider that what might appear to be a steady and reliable stream of income can be upended unexpectedly. This is particularly apparent given the downsizing/restructuring in certain business sectors where employment stability seemed all but certain.

As we approach the time by which funds will be required for a specific goal, our risk tolerance should diminish. If, for example, a pool of cash is earmarked for a home purchase it would be imprudent to ‘take undue risk’ shortly before ‘closing’.

Investment Time Horizon

It stands to reason that an investor’s investment time horizon will impact the ability to assume risk.

An investor embarking on their journey to financial freedom has time on their side. An investor nearing retirement and at the risk of relying on a fixed income for possibly another 2 decades has pretty much run out of time. This person nearing retirement does not have the luxury of being able to move to the right on the expected annual volatility axis (see graph above) in order to try and achieve a higher expected annual return.

The Importance Of The Goal

If an investor is rational, the level of risk is apt to decrease as the importance of an investment increases.

The ability to take on a level of risk is likely to be very different when managing a pool of investments to finance:

- a child’s education;

- long-term care expenses;

- a home purchase

versus managing a pool of assets to purchase a non-essential luxury item.

Past Performance Is A Very Poor Guide To Future Performance

In 1992, I met with a rookie investment advisor after attending an investment presentation. This person tried to steer me into a mutual fund that had an obscene fee structure. The selling feature was that the mutual fund had reported a ~75% rate of return in the prior year; I have not inadvertently omitted a decimal in that rate of return.

Obviously, it is unrealistic for a legitimate investment bearing a reasonable level of risk to consistently generate this type of return.

I passed on this advisor’s recommendation but monitored the mutual fund’s rate of return over the next several years to gauge what I had ‘missed’.

The mutual funds rate of return over the next several years was abysmal.

Final Thoughts

For a variety of reasons, not everyone has the time, desire, or aptitude to manage their own investments.

- Your time may be so valuable that focusing on your profession is a priority.

- Family circumstances might be such that you have NO free time.

- Family dynamics may be very complicated.

Whatever the case may be, seeking help from a reputable investment professional may be the best route to adopt. This investment professional should, as required, be able to pull tax and legal specialists into the picture because investing should not be mutually exclusive of tax and legal planning. Disregard the tax and legal implications of your investments and you can end up with more headaches than you thought possible.

Will these professionals charge fees for their services? Of, course. But if you are ‘Penny wise but pound foolish’ you are likely focusing so much on saving money in the short term that you fail to strategize and end up spending more money in the long term as a result of your decisions.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.