Summary

Summary

- Thermo Fisher has a dominant position in the Medical Laboratories and Research segment of the healthcare industry with annual revenues of ~$23B.

- It has an industry-leading presence in high-growth / emerging markets; ~21% of its annual revenue is derived from these markets.

- There is the possibility that the Chinese government could ramp up their retaliatory tariffs on goods imported from the US thus impacting results from one of TMO’s high-growth / emerging markets.

- The low interest rate environment over the last several years has aided Thermo Fisher’s rapid growth through acquisitions.

- Growth through acquisition comes with risks and TMO’s Net Acquisition Related Intangible Assets and Goodwill are now ~1.65 times Shareholders’ Equity.

Introduction

Becton Dickinson (NYSE: BDX), a company in which I have held a position since February 17, 2009, announced on September 6 that it had signed a definitive agreement to sell its Advanced Bioprocessing business to Thermo Fisher Scientific (NYSE: TMO). This business combines a strong technical services program with a variety of peptones that enhance cell culture media formulations to improve yield and reduce variability in biopharmaceutical applications.

This announcement has prompted me to look at TMO as a potential investment for the purposes of increasing my exposure to the Healthcare sector.

In reviewing TMO, it appears it has ample opportunities for growth; annual revenue is ~$23B but its addressable market is ~$150B and annual projected growth is 3 – 5 %.

It is the largest supplier of research instruments and consumables and is among the industry leaders in nearly every product category with its product catalog found in a significant percentage of research labs throughout the world.

TMO has certainly grown considerably in recent years.

TMO is positioned to take advantage of various tailwinds in that it has an industry leading presence in high-growth/emerging markets.

TMO is positioned to take advantage of various tailwinds in that it has an industry leading presence in high-growth/emerging markets.

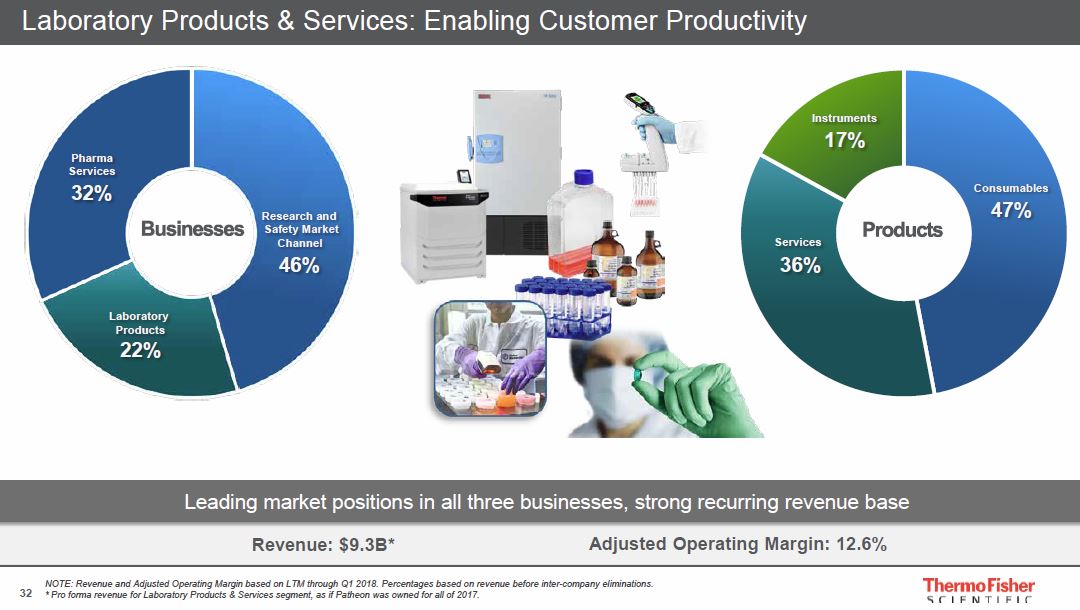

Source: TMO – Analyst Meeting – May 23, 2018

Much of TMO’s growth has some by way of acquisitions. This has resulted in a considerable change to TMO’s balance sheet.

As at December 31, 2009, TMO had Net Acquisition Related Intangible Assets of ~$6.337B, Goodwill of ~$8.983B, Long-Term Obligations of ~$2.064B, and Shareholders’ Equity of ~$15.431B. In essence, Net Acquisition Related Intangible Assets and Goodwill were almost equivalent to TMO’s Shareholders’ Equity.

Fast forward to December 31, 2017, and TMO had Net Acquisition Related Intangible Assets of ~$16.684B, Goodwill of ~$25.29B, Long-Term Obligations of ~$18.873B, and Shareholders’ Equity of ~$25.413B. Net Acquisition Related Intangible Assets and Goodwill totalling ~$41.974 is now ~1.65 times TMO’s Shareholders’ Equity.

Looking at the most recent schedule of TMO’s Debt and Other Financing Arrangements, we see that TMO has certainly taken advantage of the low interest rate environment over the past several years!

Source: TMO – GAAP/Non-GAAP Reconciliation and Financial Package – July 25 2018

Fortunately, TMO’s all important Free Cash Flow (FCF) has grown consistently in recent years (2010 – 2017): ~$1.2B, ~$1.4B, ~$1.7B, ~1.7B, ~$2.2B, ~$2.4B, ~$2.7B, and ~$3.5B.

Investors interested in investing in TMO should take into consideration the impact of a rising interest rate environment given that TMO has relied so heavily on low interest debt.

Another point to consider is that as an aggressive acquirer, its GAAP and non-GAAP results are often impacted by significant non-GAAP adjustments.

Source: TMO – GAAP/Non-GAAP Reconciliation and Financial Package – July 25 2018

Business Overview

TMO’s mission is to enable its customers to make the world healthier, cleaner and safer.

It employs ~70,000 and serves more than 400,000 customers within pharmaceutical and biotech companies, hospitals and clinical diagnostic labs, universities, research institutions and government agencies, as well as environmental, industrial quality and process control settings.

Customers are served through the following 5 premier brands.

Thermo Scientific – This brand is the research, diagnostics, industrial, and applied markets are offered a complete range of high-end analytical instruments as well as laboratory equipment, software, services, consumables and reagents.

The product portfolio includes innovative technologies for mass spectrometry, chromatography, elemental analysis, electron microscopy, molecular spectroscopy, sample preparation, informatics, chemical research and analysis, cell culture, bioprocess production, cellular, protein and molecular biology research, allergy testing, drugs-of-abuse testing, therapeutic drug monitoring testing, microbiology, anatomical pathology, as well as environmental monitoring and process control.

Applied Biosystems – This brand offers customers in research, clinical and applied markets integrated instrument systems, reagents, and software for genetic analysis. The portfolio includes innovative technologies for genetic sequencing and real-time, digital and end point polymerase chain reaction (PCR), that are used to determine meaningful genetic information in applications such as cancer diagnostics, human identification testing, and animal health, as well as inherited and infectious disease.

Invitrogen – This brand offers life science customers a broad range of consumables and instruments that accelerate research and ensure consistency of results. The product portfolio includes innovative solutions for cellular analysis and biology, flow cytometry, cell culture, protein expression, synthetic biology, molecular biology and protein biology.

Fisher Scientific – This is TMO’s channels brand. Customers have access to a complete portfolio of laboratory equipment and consumables, chemicals, supplies and services used in scientific research, healthcare, safety, and education markets. These products are offered through an extensive network of direct sales professionals, segment-relevant printed collateral and digital content, a state-of-the-art website, and supply-chain management services. We also offer a range of biopharma services for clinical trials management and biospecimen storage.

Unity Lab Services – This is TMO’s instrument and equipment services brand. There is a complete portfolio of services from enterprise level engagements to individual instruments and laboratory equipment, regardless of the original manufacturer. Through TMO’s network of service and support personnel, it provides services that are designed to help customers improve productivity, reduce costs, and drive decisions with better data.

Products and services are marketed and sold through a direct sales force, customer-service professionals, electronic commerce, third-party distributors and various catalogs.TMO has ~12,000 sales personnel including highly trained technical specialists. It also provides customers with product standardization and other supply-chain-management services to reduce procurement costs.

New Products and Research and Development are instrumental to TMO’s growth. The nature of TMO’s business is such that continual development and introduction of new products is essential and this includes the possible entry into new business segments.

In fiscal 2015 – 2017, TMO incurred $0.692B, $0.755B, and $0.888B of R&D expenses. Management fully anticipates it will need to make significant R&D expenditures to maintain and improve its competitive position.

Source: TMO – Analyst Meeting – May 23, 2018

Q2 2018 Results

TMO’s Q2 Earnings Release can be accessed here with further important information available in the GAAP/Non-GAAP Reconciliation and Financial Package presentation.

Projections

At TMO’s recent Analyst Day meeting, management provided the following.

Source: TMO – Analyst Meeting – May 23, 2018

Subsequent to the Analyst Meeting, TMO has revised its Adjusted EPS guidance upward to $10.89 – $11.01 from $10.80 – $10.96 for 15 – 16% year over year growth. If we take the $10.95 mid-point of the new guidance and use a 15% annual growth level, we get adjusted EPS guidance of ~$12.59 for FY2019, ~$14.48 for FY2020, and ~$16.65 for FY2021.

Credit Ratings

TMO’s long-term unsecured credit rating was upgraded by Moody’s from Baa3 to Baa2 in August 2016 and this rating was reaffirmed May 16, 2017. This rating is the middle tier of the lower medium grade within the investment grade category.

S&P Global has accorded a BBB+ long-term unsecured credit rating. This rating is one notch higher than that accorded by Moody’s; it is the upper tier of the lower medium grade within the investment grade category.

Both ratings are currently acceptable from my perspective.

Valuation

GAAP Earnings for the first 6 months of the current fiscal year amount to $3.28 while adjusted earnings (Non-GAAP) amount to $5.25.

This is certainly not an exact science but if GAAP earnings for the first half of the year are ~62.5% of non-GAAP earnings and I use this ratio with the new adjusted EPS guidance then I arrive at GAAP earnings of ~$6.84; I used the $10.95 mid-point of the revised adjusted EPS guidance and multiplied it by 62.5%.

With TMO currently trading at ~$236, the forward PE is ~34.5 ($236/~$6.84); TMO’s 5 year PE is ~29.

The forward adjusted PE is ~21.55 ($236/$10.95). In the Projections section of this article, I endeavored to ascertain TMO’s projected adjusted non-GAAP earnings based on management’s recent guidance and arrived at adjusted EPS guidance of ~$12.59 for FY2019, ~$14.48 for FY2020, and ~$16.65 for FY2021.

I am prepared to use the FY2019 guidance but am reluctant to use guidance beyond such time. Using the ~$12.59 guidance and employing the same 62.5% multiple to estimate GAAP earnings I arrive at FY2019 GAAP earnings of ~$7.87. With TMO currently trading at ~$236 and estimated GAAP earnings of ~$7.87 I get a forward PE of ~30. That level is a bit high for my liking.

If TMO were to drop to ~$210 (I don’t think an 11% pullback is totally out of the realm of possibility) then I would be looking at a forward PE of ~26.7 ($210/~7.87) which, while not a bargain, seems fair for a company with TMO’s long-term growth potential.

Dividends

Investors looking to purchase TMO primarily for its dividend would be well advised to look at alternate investments. TMO’s dividend history can be found here.

Shares Outstanding

TMO’s share count (expressed in millions of shares) during the 2008 – 2017 is as follows: 434, 423, 409, 385, 367, 366, 402, 397, and 398.

On September 7, TMO announced that its Board of Directors has authorized the repurchase of $2.0B of shares of its common stock in the open market or in negotiated transactions; the authorization has no expiration date.

The previous repurchase authorization of $1.5B of shares, approved in July 2016, has $0.25B remaining. TMO plans to deplete this amount later this year.

Final Thoughts

I do not dispute that TMO has certainly been a wonderful investment for long-term investors. My concern at this stage is that its current valuation is somewhat lofty. There are sufficient risks (ie. potential additional tariffs and retaliatory tariffs, rising interest rate environment, mid-term US elections, etc.) to give me cause for concern.

TMO has identified China as a key growth market and with the risk of additional tariffs on Chinese imports, it remains to be seen if China will introduce retaliatory tariffs and the extent to which they will impact TMO.

I looked at the possibility of selling at a $210 December 2018 PUT but the premium I would receive is negligible (~$2.30/share) which is a ~1.1% return for a little over 3 months. This is not an attractive return, and therefore, I will just patently wait for TMO to retrace to a level close to $210.

I hope you enjoyed this post and I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I do not currently hold a position in TMO and do not intend to initiate a position within the next 72 hours.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.