In 2020, Becton Dickinson (BDX) embarked on its 5-year BD2025 strategy. Although BDX’s total investment return over the past ~8 – ~9 years is disappointing, its transition into a pure-play medtech company is approaching an end. I am, therefore, sticking with this investment since I think future performance will be superior to that of recent years.

In my December 12 post, I disclose the purchase of an additional 100 shares @ ~$227.56 bringing my exposure in one of the ‘Core’ accounts within the FFJ Portfolio to 536 shares.

BDX’s share price surged to ~$250 following that purchase. The share price, however, has subsequently retraced to ~$227. Following the recent release of Q1 2025 results and the announcement of BDX’s intent to separate its Biosciences and Diagnostics Solutions business, I acquired another 100 shares @ ~$226.86 on February 6.

Business Overview

Good sources of information to learn about BDX are its website and its FY2024 Annual Report/Form 10-K.

On April 1, 2022, BDX divested itself of its diabetes management segment. A newly created company, Embecta (EMBC), is now a medical device company, focusing on the provision of various solutions to enhance the health and well-being of people living with diabetes. Its products include pen needles, syringes, and safety injection devices, as well as digital applications to assist people with managing patient’s diabetes.

On September 3, 2024, BDX completed the acquisition of Edwards Lifesciences’ Critical Care product group. This business has been renamed BD Advanced Patient Monitoring.

Biosciences & Diagnostic Solutions Separation

On February 5, 2025, BDX announced its intent to separate its Biosciences & Diagnostic Solutions segment as it approaches the finish line in its 5-year ‘BD 2025’ strategy. A high level overview of the planed separation is accessible here.

The 5-year BD2025 strategy kicked off in 2020 and set goals of long-term, compounded annual revenue growth of 5.5% or more while focusing on high-growth and high-margin markets.

In addition, activist investor Starboard Value took a stake in BDX and was pushing the company to sell its life sciences unit. BDX’s management, however, states that the decision to separate the Biosciences & Diagnostic Solutions was in the works since early 2024. The proposed separation is part of the company’s plans to pursue more tuck-in acquisitions, while focusing primarily on healthcare providers and patient end markets.

Following the separation, the ‘New BD’ will be a pure-play medtech company focusing on:

- medical essentials such as its ubiquitous hardware for collecting blood samples and delivering IV medications which number in the tens of billions of units per year; and

- interventional devices and connected care programs with the latter including the recent acquisitions from Edwards Lifesciences.

- pharmaceutical systems, to be renamed biopharma systems, which focuses on developing delivery devices for the makers of drugs and biologics that include GLP-1s and patient-operated injectors. BDX estimates this will grow into a billion-dollar business by 2030.

Post separation, BDX is expected to have FY2024 revenue of ~$17.8B, with a $70B+ addressable market growing at ~5%. The ‘New BD’ expects to benefit from strong, durable cash flow with recurring revenue over 90%.

Post-separation, the Biosciences & Diagnostic Solutions company will have a catalog that generated ~$3.4B of revenue in FY2024. This includes tests for infectious disease and cervical cancer screening as well as flow cytometry instruments and single-cell multiomics tools used in research.

BDX’s Board has approved the transaction and is open to pursuing a Reverse Morris Trust, spin-off spinoff, or an outright sale. More specifics will be communicated by the close of FYE2025 (September 30) with the separation to be completed by FYE2026.

NOTE: A Reverse Morris Trust is a corporate finance strategy that allows a company to sell a division or unwanted assets to another company without incurring taxes on the sale. The first step in the process is to spin-off the assets into a separate subsidiary. This subsidiary then merges with the acquiring company. This process transfers ownership to the buyer while the original owners maintain control through a majority stake in the newly merged entity.

A Reverse Morris Trust is often used to minimize tax liabilities on asset sales. As a result of the potential for tax avoidance, it is subject to scrutiny from tax authorities and may have complex regulatory requirements.

Financials

Q1 2025 Results

BDX’s Q1 2025 results are accessible here.

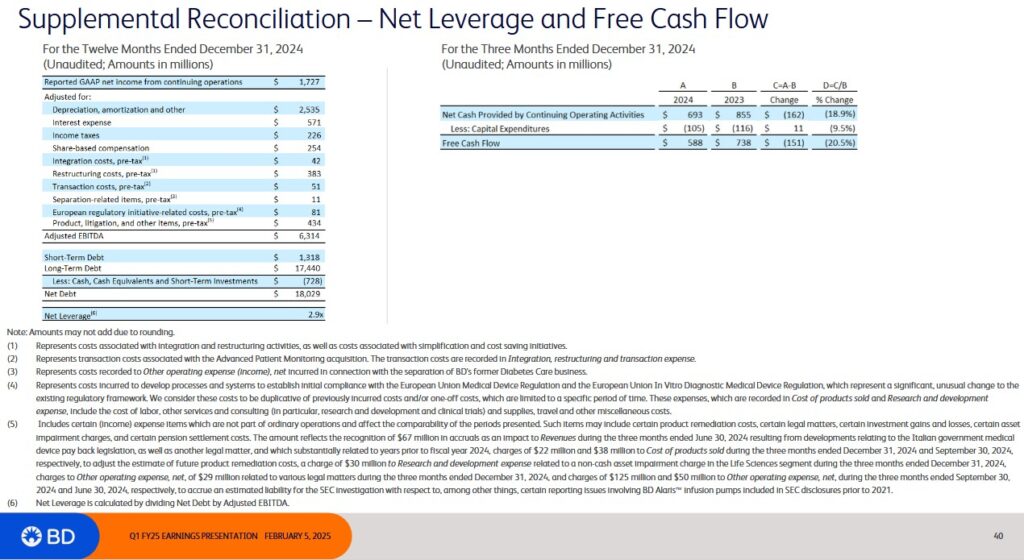

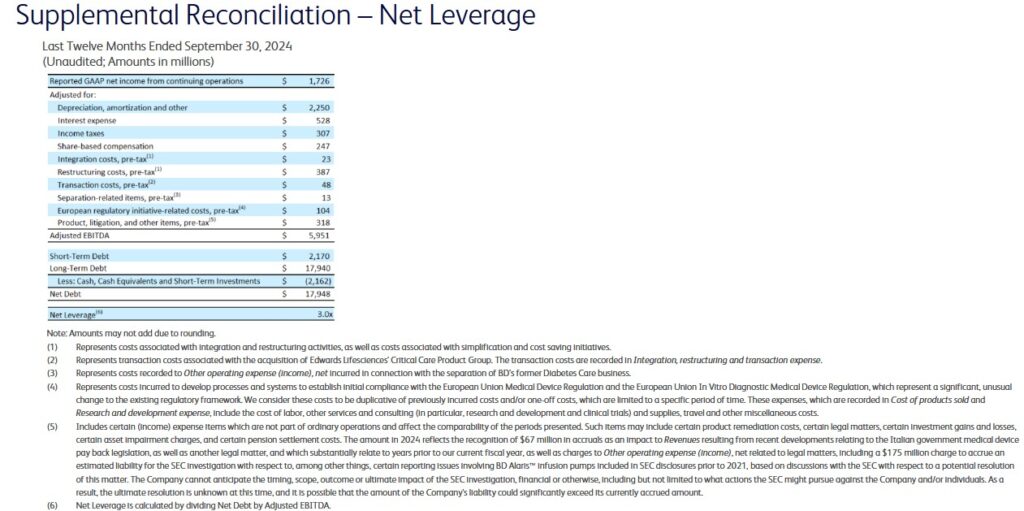

Net leverage (Net Debt/Adjusted EBITDA) at FYE2021, FYE2022, FYE2023, and FYE2024 was 2.6x, 2.8x, 2.6x, 2.6x, and 3.0x. This had been reduced to 2.9x at the end of Q1 2025. Management’s expectation, however, is to reduce this to 2.5x within 12 – 18 months.

The following reflects BDX’s net leverage at FYE2024.

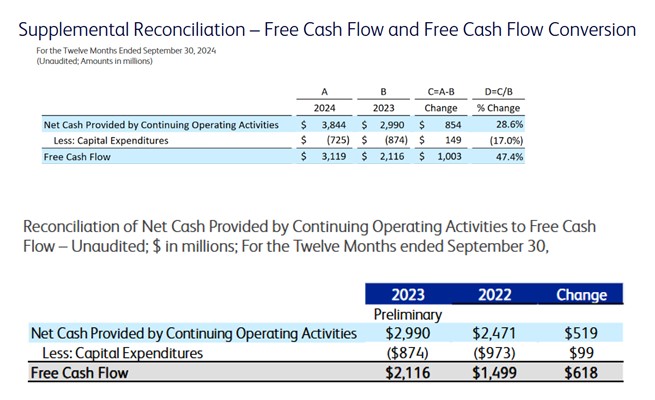

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

The following reflects the manner in which BDX calculates its FY2022 – FY2024 FCF; BDX’s earning presentations did not include FCF prior to FY2022.

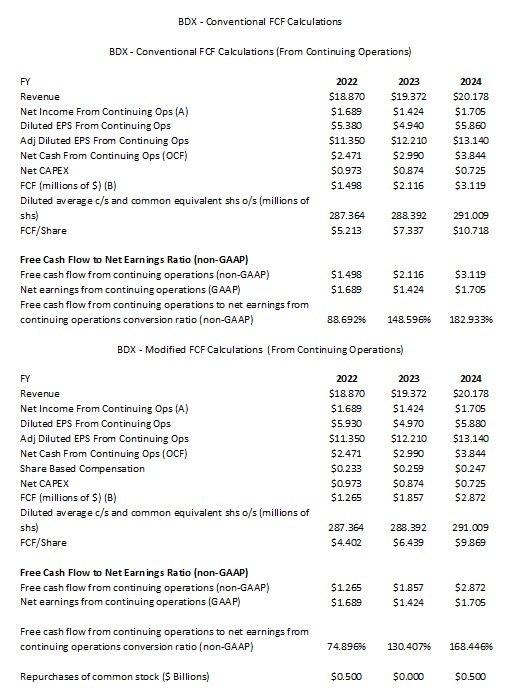

My recent Danaher (DHR) post explains my rationale for deducting share based compensation (SBC) when determining FCF.

The following table reflects BDX’s FCF using the conventional method used by BDX and the modified method where I deduct SBC. We see from the calculations that FCF exceeds net income from continuing operations in FY2023 and FY2024 but not in FY2022.

In Q1 2025, BDX generated $0.693B of cash from continuing operations and incurred CAPEX of $0.105B. The currently available earnings material does not reflect the SBC component. We can, however, approximate the Q1 2025 SBC component by taking 1/4 of the $0.247B for FY2024 thus giving us ~$0.062B. On this basis, Q1 2025’s FCF is ~$0.526B.

BDX’s cash used for financing activities in Q1 greatly exceeds this amount. The cash used to repay debt was ~$0.8B. In addition, ~$0.75B went toward the accelerated repurchase of shares, and ~$0.302B of dividends were distributed. A significant component of this cash shortfall came from the ~$1B reduction in cash.

I expect that over the remainder of FY2025, BDX’s FCF will improve.

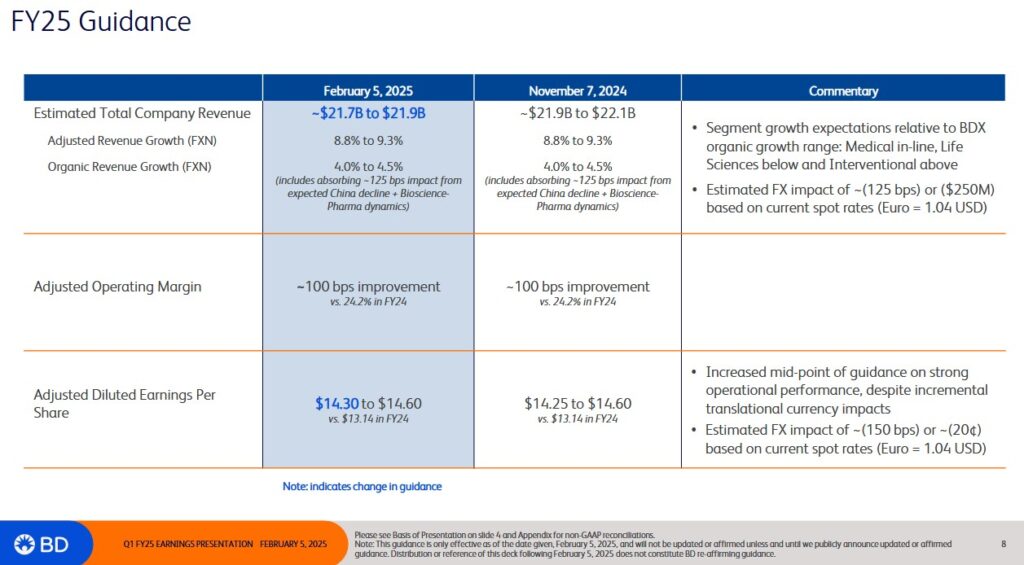

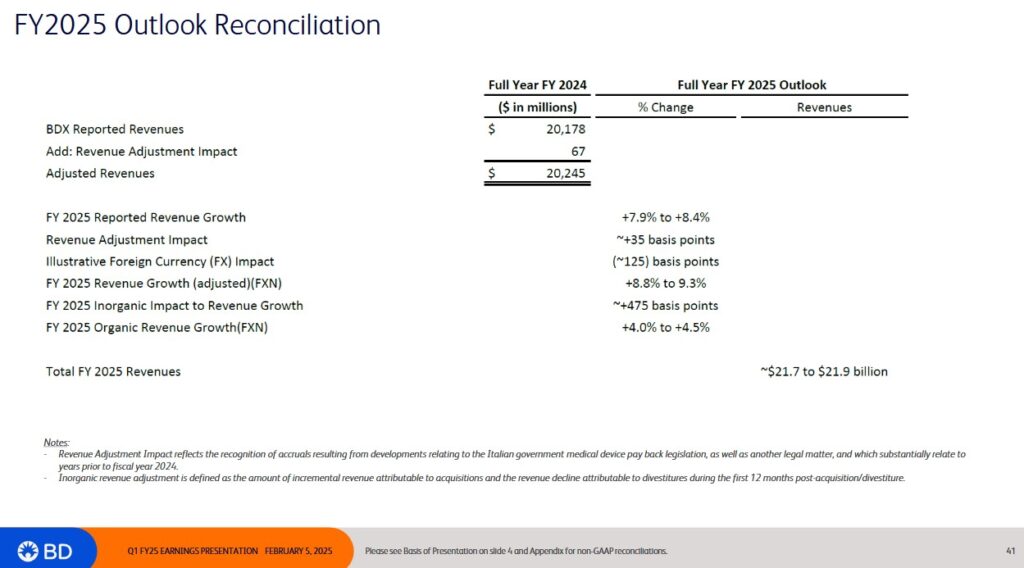

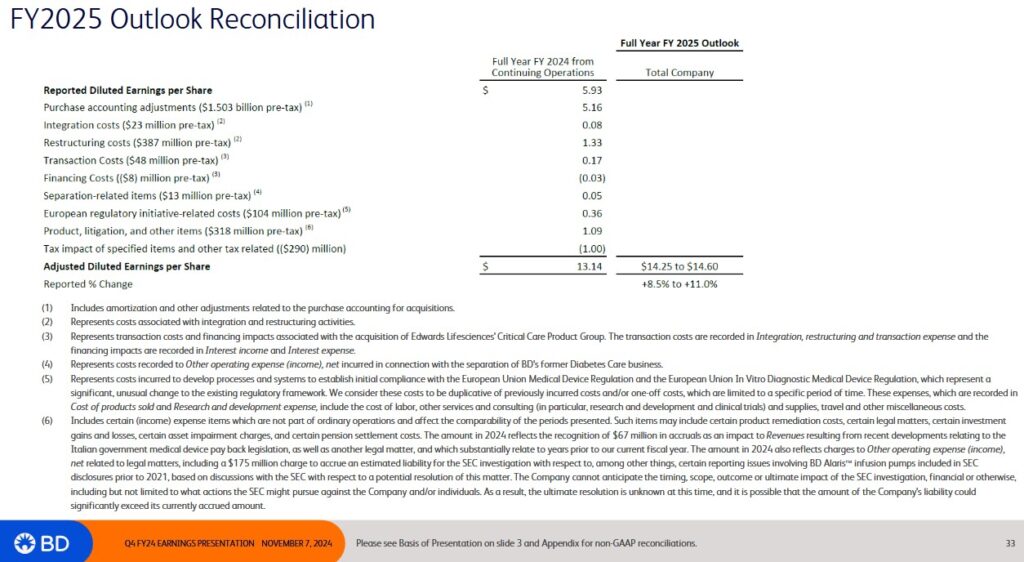

FY2025 Outlook

The following is BDX’s current FY2025 outlook.

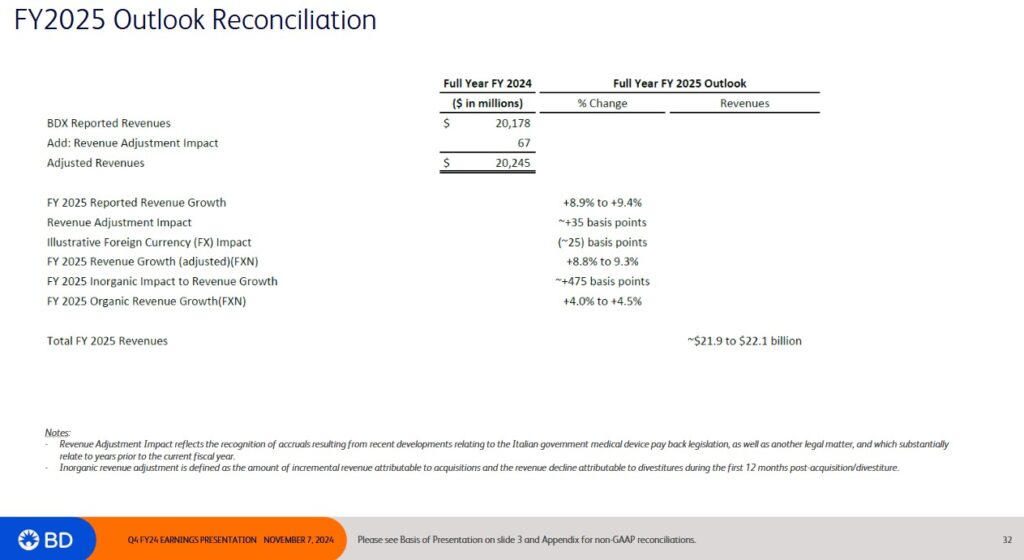

This is BDX’s prior FY2025 outlook.

Risk Assessment

BDX’s net leverage ratio (Net Debt/Adjusted EBITDA) at FYE2021, FYE2022, FYE2023, and FYE2024 was 2.6x, 2.8x, 2.6x, and 3.0x. BDX’s target is under 3.0x. At the end of Q1 2025 is was 2.9x.

There are no changes to BDX’s domestic senior unsecured debt ratings from the time of my August 6, 2024 and December 12, 2024 posts.

All 3 ratings are the middle tier within the lower medium grade category. They define BDX as having an ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity for BDX to meet its financial commitments.

These ratings are satisfactory for my purposes.

Dividend and Dividend Yield

BDX’s dividend history is accessible here.

BDX is somewhat trapped because with 53 consecutive years of dividend increases, its shareholder base EXPECTS dividend increases. If BDX were to re-prioritize its capital allocation and to lower the importance of dividend increases, the shareholder base will most likely revolt. Any dividend cut/freeze would most likely lead to a drop in BDX’s share price.

As per prior posts, a company’s dividend metrics are of little importance in my investment decision making process. My interest lies in the total potential investment return and whether the return is commensurate with the risk I am assuming.

BDX’s share repurchases over the years have been ‘all over the map’. During the FY2010 – FY2024 time frame, BDX repurchased (in $B) 0.75, 1.5, 1.5, 0.45, 0.4, 0, 0, 0.22, 0, 0, 0, 1.75, 0.5, 0, and 0.5 for a total of $7.57B.

The diluted average common shares outstanding (millions of shares) in FY2010 was 240.136. In FY2024, this had ballooned to 291.009 and in Q1 2025 it was 290.389.

In addition to the issuance of shares as part of its various SBC programs, BDX has made several acquisitions (eg. Carefusion, C.R. Bard, Parata Systems, Edwards LifeSciences’ Critical Care) over the years. These acquisitions have been funded through the use of debt and the issuance of new shares. A history of BDX’s recent mergers and acquisitions is accessible here.

The years in which BDX repurchased no shares (or few shares) is because the priority was to reduce debt taken on for acquisition purposes.

In FY2024, BDX executed and settled accelerated share repurchase agreements for the repurchase of 2.118 million shares of its common stock for total consideration of ~$0.5B. The purchase was made pursuant to the repurchase program authorized by the Board on November 3, 2021, for 10 million shares for which there is no expiration date.

When I wrote my prior post, I noted that BDX’s FY2025 outlook included plans to deploy ~$1B towards share repurchases over the next 12 – 18 months. In Q1 2025, BDX repurchased $0.75B of its shares through an accelerated share repurchase arrangement.

Valuation

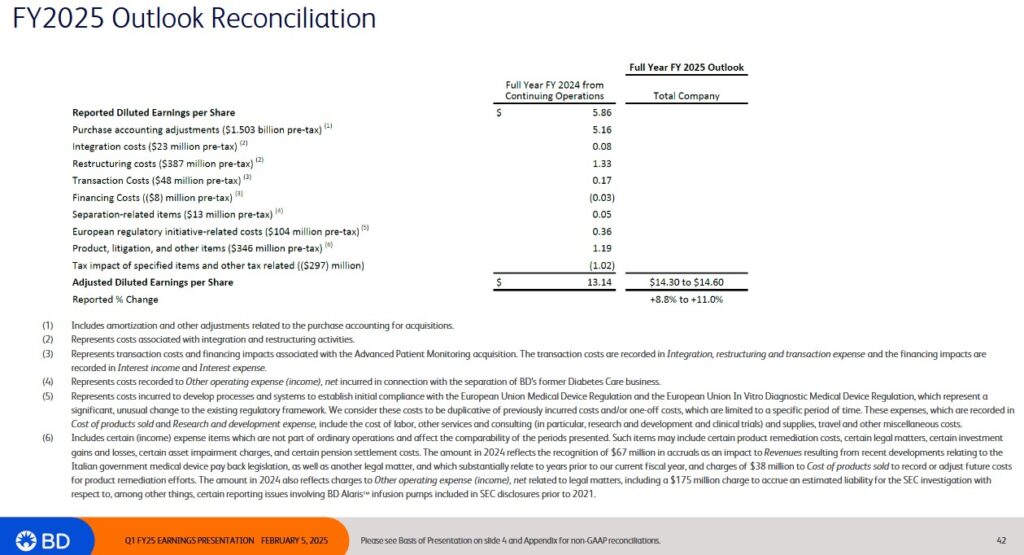

For roughly the past decade, there has been a significant variance between GAAP and non-GAAP earnings. Each year’s Q4 earnings presentation has a reconciliation of Reported Diluted EPS to Adjusted Diluted EPS.

The variances are primarily attributed to purchase accounting adjustments, restructuring costs, and integration costs. There may have been variances prior to BDX embarking on the path of major acquisitions (the first major acquisition post Financial Crisis was the 2015 acquisition of Carefusion) but nothing like in FY2015 – FY2024. In the past decade, BDX has reported significant earnings adjustments. At some point in time, investors begin to wonder whether these adjustments should really be considered ‘adjustments’ or whether there are really part of normal business operations.

With the BD2025 strategy nearing its end, I hope these annual adjustments become less significant.

At the time of my December 11, 2024 purchase, management’s FY2025 outlook was for ~$14.25 – ~$14.60 adjusted diluted EPS. Using my ~$227.56 purchase price, the forward adjusted diluted PE range was ~15.6 – ~16.

Using the adjusted diluted EPS broker estimates, BDX’s forward adjusted diluted PE levels were:

- FY2025 – 14 brokers – mean of $14.42 and low/high of $14.31 – $14.52. Using the mean, the forward adjusted diluted PE is ~15.8.

- FY2026 – 13 brokers – mean of $15.73 and low/high of $15.51 – $15.97. Using the mean, the forward adjusted diluted PE is ~14.47.

- FY2027 – 5 brokers – mean of $16.54 and low/high of $14.52 – $17.56. Using the mean, the forward adjusted diluted PE is ~13.8.

BDX’s share price surged to ~$250 following my December 11 purchase. Following the recent release of Q1 2025 results, however, the share price plunged. I, therefore, acquired another 100 shares @ ~$226.86 bringing my exposure to 636 shares.

Using management’s revised FY2025 outlook of ~$14.30 – ~$14.60 adjusted diluted EPS and my purchase price, the forward adjusted diluted PE range is ~15.5 – ~15.9.

BDX’s current forward adjusted diluted PE levels using the adjusted diluted EPS broker estimates are:

- FY2025 – 15 brokers – mean of $14.41 and low/high of $14.12 – $14.53. Using the mean, the forward adjusted diluted PE is ~15.74.

- FY2026 – 15 brokers – mean of $15.66 and low/high of $15.33 – $15.92. Using the mean, the forward adjusted diluted PE is ~14.48.

- FY2027 – 6 brokers – mean of $16.94 and low/high of $16.61 – $17.42. Using the mean, the forward adjusted diluted PE is ~13.4.

Revisions to these estimates are likely over the next several days.

BDX’s YTD FY2025 FCF falls short of its Q1 disbursements (share repurchases, debt repayment, and dividends). I, however, envision an improvement in FCF over the remainder of the current fiscal year.

Following the separation of the Biosciences & Diagnostic Solutions segment in FY2026, I expect proceeds from the separation will be reinvested in the business (acquisition, debt reduction, share repurchases). At this point, I have no way of determining BDX’s financials post FYE2026 and am merely hoping management will do what is best for its shareholders.

Final Thoughts

I initiated a BDX position on February 17 , 2009 @ $70.5499 in a retirement account for which I do not disclose details. Over the years, I increased my exposure but on October 1, 2022 I sold shares @ ~$223.27 as part of our Registered Retirement Savings Plan meltdown strategy.

I also acquired BDX shares in November 2019 and February 2020 @ ~$249 in an account in the FFJ Portfolio. My return on this investment has been less than impressive!

BDX has been transitioning since it acquired Carefusion for $12.2B in 2015 and C. R. Bard in 2017 for $24B. Hopefully its transition is coming to an end.

Tempting as it may have been to exit this holding, I have opted to remain patient and have increased my exposure with two 100 share purchases (December 2024 and February 2025). Here’s hoping these were the right decisions given that I think ~$270 is a fair value.

BDX was my:

- 27th largest holding when I completed my 2023 Year End Review;

- 24th largest holding when I completed my 2024 Mid Year Review; and

- 25th largest holding when I completed my 2024 Year End Review.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BDX.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.