S&P Global (SPGI) shareholders should welcome periods of market turmoil. Even if economic conditions deteriorate dramatically, the probability of SPGI having to declare insolvency is extremely low. Given this, we can focus on opportunistic share acquisitions.

In my March 5, 2025 post, I disclosed the purchase of a 100 shares @ ~$518.76 on March 4 in a ‘Side’ account in the FFJ Portfolio. I subsequently acquired another 100 shares on March 7 @ ~$494.18.

When market conditions deteriorated in early April, I acquired SPGI shares @ ~$446.78 for a young investor who is on their journey to financial freedom; I do not disclose details about such purchases.

With the release of Q1 2025 results on April 29, I now revisit this existing holding.

Business Overview

Learn about SPGI’s business and risk factors by reading Part 1 in the FY2024 10-K and the company’s website.

OSTTRA Divestiture

In my recent CME Benefits From Market Volatility post, I touch upon CME’s and SPGI’s announcement that they both signed a definitive agreement to sell OSTTRA, a leading provider of post-trade solutions for the global OTC market, to investment funds managed by KKR, a leading global investment firm. The terms of the deal equals a total enterprise value of $3.1B, subject to customary purchase price adjustments. Proceeds will be divided evenly between SPGI and CME pursuant to their 50/50 joint venture and the transaction is expected to close in the second half of 2025.

SPGI’s management expects to use the proceeds from the OSTTRA sale for additional share repurchases.

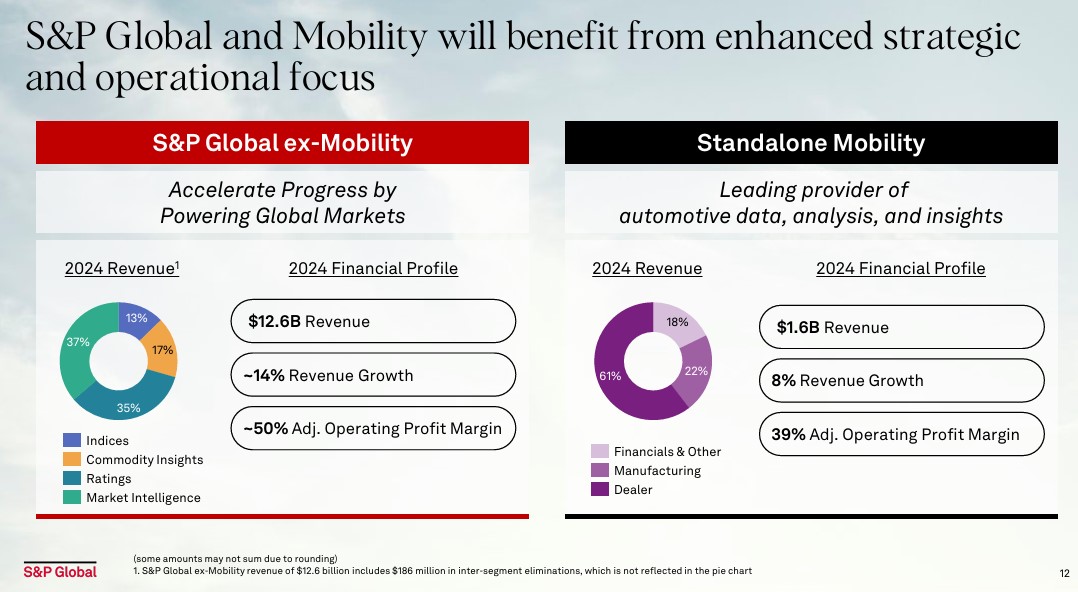

Intent To Separate Mobility Division

On April 29, SPGI announced its intent to separate S&P Global Mobility (Mobility) from SPGI. The planned separation is expected to result in Mobility becoming a standalone public company.

On the Q1 2025 earnings call, management states:

This is something we’ve been thinking about for quite some time. We’ve done a very rigorous and deep analysis around this. To be clear, the mobility business is a phenomenal business. It has a very long history of innovation, of strong growth, and it’s got incredibly talented leaders across the business. We believe that the plan to do a tax-free spin is really the best opportunity for long-term shareholder value here. It allows Mobility to pursue its profitable growth trajectory and for S&P Global, excluding Mobility, allows our four core divisions to grow and be very closely aligned with our strategy.

In FY2024, the Mobility segment generated $1.6B in revenue, a YoY increase of approximately 8%. In comparison, SPGI’s total FY2024 revenue was $14.208B.

The separation is expected to be tax-free to shareholders and to be completed within 12 – 18 months.

Financial Results

Q1 2025

Material related to the Q1 2025 earnings is accessible here.

Details about each business segment’s performance in Q1 2025 relative to Q1 2024 is in the Q1 2025 Earnings Release.

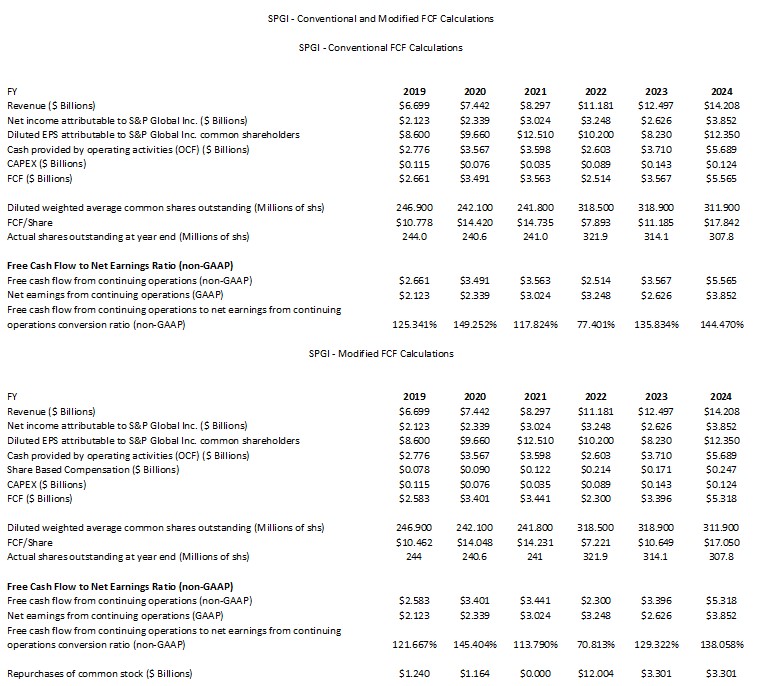

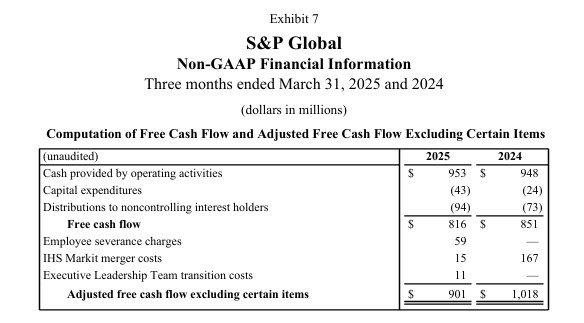

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

FCF is a non-GAAP metric, and therefore, its method of calculation is inconsistent. Historically, SPGI deducts CAPEX from OCF to calculate its FCF. In recent posts, however, I explain my rationale for also deducting share-based compensation (SBC) from a company’s OCF.

The following reflects SPGI’s FCF using the conventional and modified methods.

The following reflects SPGI’s FCF and adjusted FCF in Q1 2024 and Q1 2025. SPGI’s addition of more line items to determine its adjusted FCF demonstrates the inconsistency in the calculation of FCF.

If we deduct SBC of ~$0.033B and ~$0.047B in Q1 2024 and Q1 2025, SPGI’s adjusted FCF drops to ~$0.985B and ~$0.854B. Using a Q1 2024 and Q1 2025 diluted weighted average number of outstanding shares of ~314 million and ~307.7 million, SPGI’s adjusted FCF/share is ~$3.14 and ~$2.78. SPGI typically generates more FCF than earnings. I, therefore, anticipate FCF/share over the remainder of FY2025 will exceed EPS.

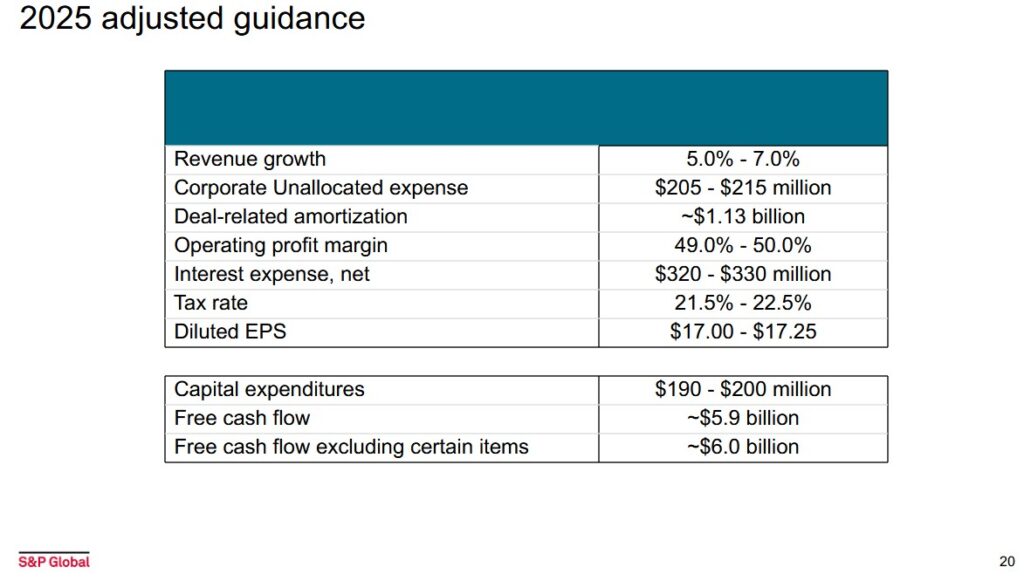

FY2025 Guidance

Much like Moody’s (MCO) (refer my Wide-Moat Moody’s Is Almost Fairly Valued post), the recently introduced tariffs may not directly impact SPGI. SPGI does not, however, operate in a vacuum. If the global economy suffers, SPGI will undoubtedly feel the impact.

On the Q1 2205 earnings call, management states:

We expect billed issuance to moderate from Q1 levels for the remainder of 2025, and we have already seen declines in April. We believe some of the strength in Q1, particularly in investment grade was driven by the pull forward of some issuance to get ahead of April.

We expect the tariff discussion and related market volatility is likely leading to some pushback of issuance as well, both of which put pressure on issuance volumes in the near term.

As we look at the broader macro and commercial conditions, it’s clear that we are going through a phase of unpredictable market movements, geopolitical risk and fluidity in the regulatory landscape.

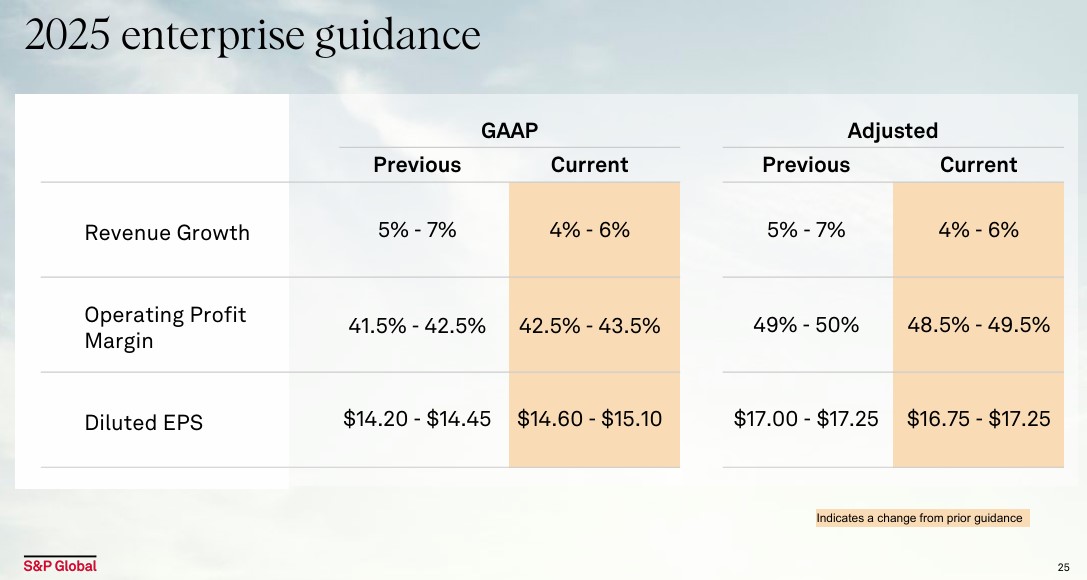

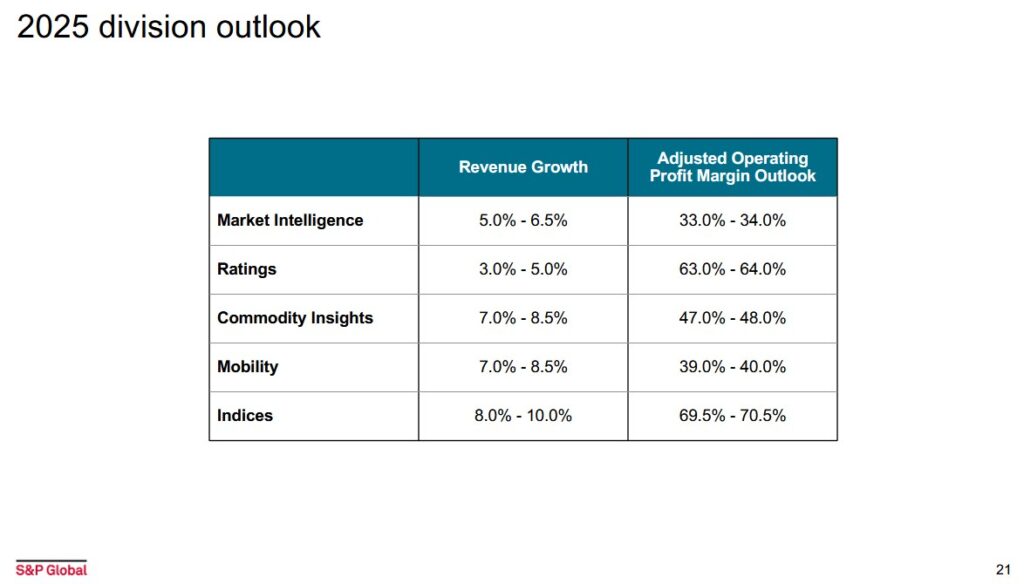

The following reflects SPGI’s current and prior enterprise guidance. The division revenue and adjusted margin outlook is found within the Q1 2025 earnings presentation.

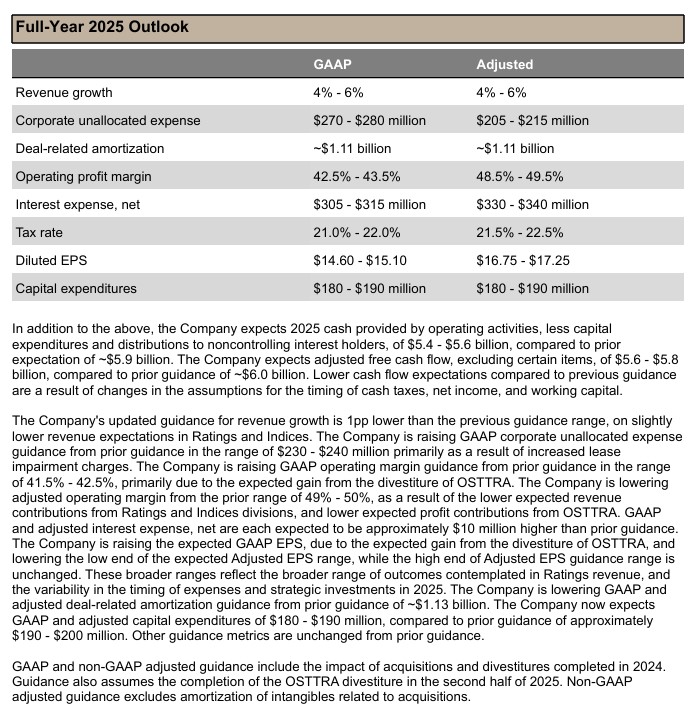

The following provides additional information regarding SPGI’s FY2025 outlook.

With the planned closing of the OSTTRA sale in the second half of 2025, there will be slightly lower operating income with no corresponding revenue impact. This will directly impact margins for the year. The OSTTRA impact and the mix shift in revenue are the primary drivers for the change to SPGI’s enterprise margin guidance.

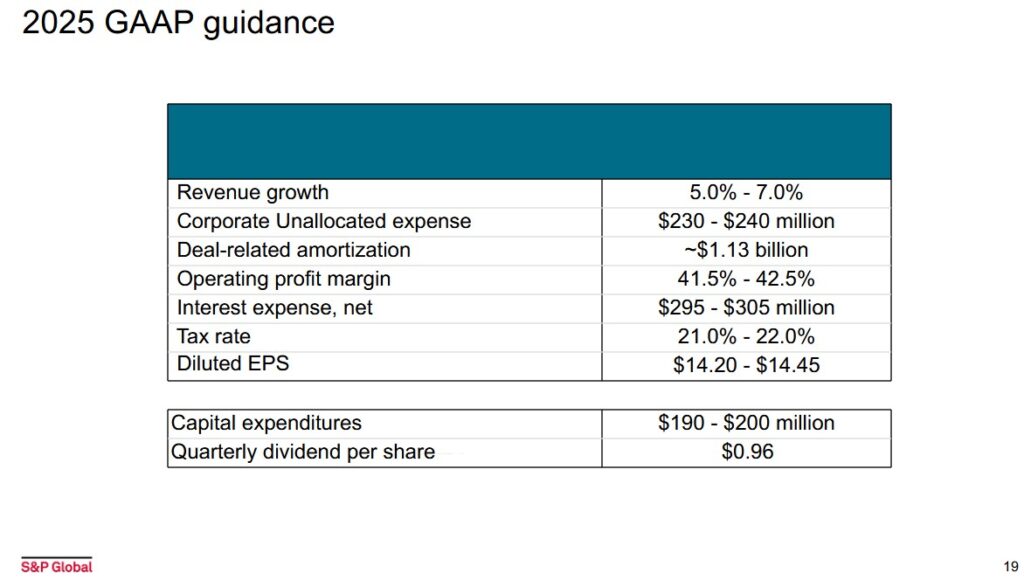

SPGI’s FY2025 outlook at the time of its Q4 2024 earnings release is provided below for comparison.

Risk Assessment

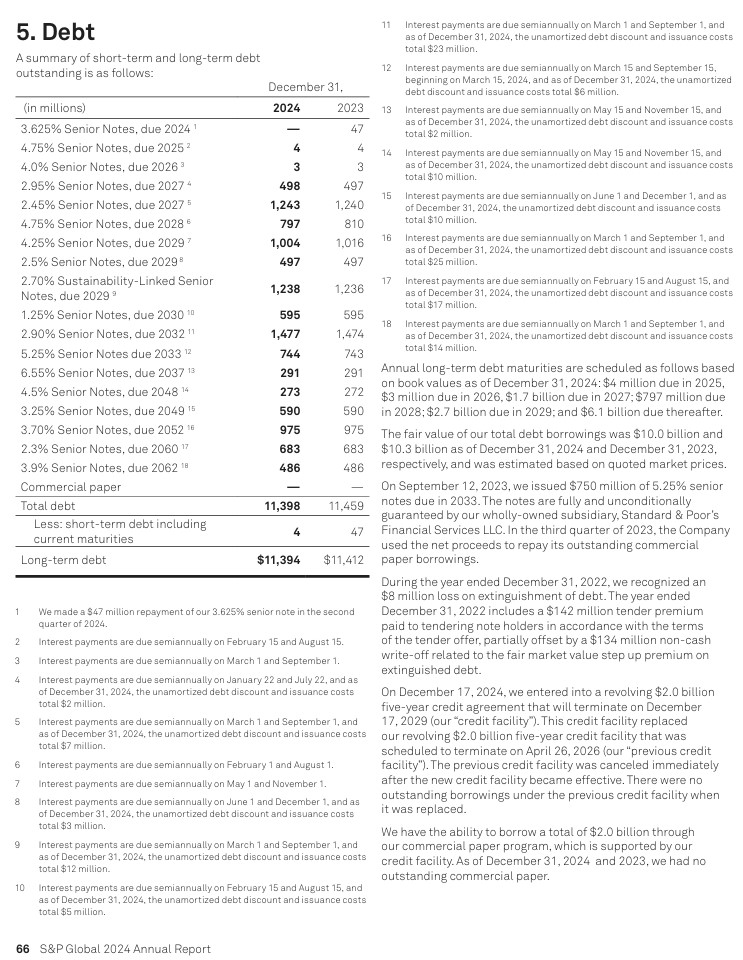

I pay particularly close attention to the risk aspect of my investments. I, therefore, have a particular interest in a company’s schedule of long-term debt.

At the end of Q1 2025, SPGI’s total long-term debt was ~$11.388B which is very similar to the amount owing at FYE2024.

We see from this schedule that SPGI borrows at very attractive rates and that the maturity of its debt is well staggered.

On August 8, 2018, Moody’s upgraded SPGI’s domestic senior unsecured debt from Baa1 to A3 which is the lowest tier within the upper-medium investment-grade group of ratings. This rating was affirmed on March 6, 2024.

This rating means SPGI has a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

SPGI’s credit risk is acceptable from my perspective.

Dividend and Dividend Yield

SPGI’s dividend history on its website only dates back to 1995 but its track record of consecutive years of dividend increases extends well beyond this.

Investors would be wise not to focus solely on the dividend return but rather the overall potential return. With most of SPGI’s potential return likely to come from capital gains, it is all that much more important to acquire shares when attractively or fairly valued!

Share Repurchases

SPGI has a newly approved share repurchase authorization up to $4.3B.

The weighted average diluted shares outstanding for FY2019 – FY2024 is reflected in the table provided in the Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX section of this post.

At the end of Q1 2025, the actual shares outstanding was 306.7 million; the diluted weighted average is 307.7 million.

In Q1 2025, SPGI repurchased ~$0.65B of shares. It has also recently disclosed its intent to execute additional accelerated share repurchases (ASR) totaling $0.65B in the coming weeks. SPGI also expects to use the proceeds from the OSTTRA sale for additional share repurchases. I anticipate SPGI will repurchase at least ~$3.301B of its shares in FY2025 just as it did in FY2023 and FY2024.

Under an ASR agreement, SPGI pays a specified amount to the financial institution and receives an initial delivery of shares. This initial delivery of shares represents the minimum number of shares that it may receive under the agreement. Upon settlement of the ASR agreement, the financial institution typically delivers additional shares. The total number of shares ultimately delivered, and therefore the average price paid per share, is determined at the end of the applicable purchase period of each ASR agreement based on the volume weighted-average share price, less a discount.

SPGI accounts for its ASR agreements as two transactions:

- a stock purchase transaction; and

- a forward stock purchase contract.

The shares delivered under the ASR agreements result in a reduction of outstanding shares used to determine the weighted average common shares outstanding for purposes of calculating basic

and diluted EPS. The repurchased shares are held in Treasury and the forward stock purchase contracts are classified as equity instruments.

Valuation

My preference is to gauge a company’s valuation based on cash flow. I do, however, also consider GAAP and non-GAAP earnings guidance.

Management’s revised GAAP diluted EPS guidance is $14.60 – $15.10 and the current share price is ~$492. Using these figures, the forward diluted PE is ~33.1 based on the ~$14.85 mid-point. The forward adjusted diluted PE is ~29 based on the ~$17 mid-point of management’s $16.75 – $17.25 adjusted diluted EPS guidance.

The forward-adjusted diluted PE levels using the current share price and broker estimates are:

- FY2025 – 23 brokers – ~29 using a mean of $16.97 and low/high of $16.35 – $17.62.

- FY2026 – 23 brokers – ~25.9 using a mean of $19.03 and low/high of $18.10 – $19.74.

- FY2027 – 13 brokers – ~23.1 using a mean of $21.29 and low/high of $20.05 – $21.85.

Take these earnings estimates with a ‘grain of salt’. I don’t know how anybody can consistently accurately predict how a company is going to perform 2+ years from now…especially in the current environment.

In FY2025, SPGI expects to return approximately 85% of adjusted free cash flow to shareholders through dividends and share repurchases. SPGI is lowering its adjusted FCF outlook to $5.6B – $5.8B ($5.7B average x 85% = ~$4.845B). The prior guidance is ~$6.0B ($6.0B x 85% = ~$5.1B). This reduction is the result of changes in the assumptions for the timing of cash taxes, net income, and working capital.

At the end of Q1 2025, the actual shares outstanding was ~306.7 million versus 321.9, 314.1, and 307.8 at FYE 2022 – 2024.

If SPGI continues to aggressively repurchase shares while they remain undervalued, the FYE2025 shares outstanding could drop to ~300 million. The FYE2024 shares outstanding was 307.8 million so the mid-point of ~300 – ~307.8 million is ~304 million.

To estimate SPGI’s valuation using FCF, divide the average of management’s guidance (~$5.7B) by ~304 million shares to arrive at ~$18.75 in FCF/share. Divide the current ~$492 share price by ~$18.75 and the forward P/FCF is ~26.24.

If we estimate FY2025’s SBC will be ~$0.255B (~$0.247B in FY2024), the FY2025 FCF drops to ~$5.445B ($5.7B – ~$0.255B). Divide this by 304 million shares to get ~$17.91 FCF/share. Divide $492 by ~$17.91 and the P/FCF is ~27.5.

For comparison, I calculate SPGI’s approximate valuation as follows in my March 5 post:

Using management’s GAAP diluted EPS guidance of $14.20 – $14.45 and my $518.76 purchase price, the forward diluted PE is ~36.2 based on the ~$14.325 mid-point. The forward adjusted diluted PE is ~30.3 based on the ~$17.125 mid-point of management’s $17.00 – $17.25 adjusted guidance.

The forward-adjusted diluted PE levels using my purchase price and the current broker estimates are:

- FY2025 – 20 brokers – ~30.1 using a mean of $17.21 and low/high of $16.40 – $17.51.

- FY2026 – 20 brokers – ~27 using a mean of $19.27 and low/high of $18.15 – $19.80.

- FY2027 – 12 brokers – ~24.1 using a mean of $21.56 and low/high of $20.05 – $22.45.

On the Q4 earnings call, management states its intention to maintain its target of returning 85% or more of the 2025 $6B FCF forecast ($6B x 85% = ~$5.1B) in the form of dividends and share repurchases.

At FYE 2022 – 2024 the actual shares outstanding were (in millions) 321.9, 314.1, and 307.8. Using a weighted-average number of diluted common shares outstanding of 304 million and a $0.96 quarterly dividend, we can expect SPGI to distribute ~$292 million a quarter in dividends or ~$1.167B in FY2025 (~$1.147B, and ~$1.134B in FY2023 and FY2024).

Subtract $1.167B from the $5.1B SPGI plans to return to shareholders and we get ~$3.93B to be returned in the form of share repurchases (versus $3.3B in FY2023 and FY2024). If it repurchases shares @ ~$560, this works out to share repurchases of ~7 million giving us FYE2025 shares outstanding of ~300 million. The FYE2024 shares outstanding was 307.8 million so the mid-point of this value and 300 million is ~304 million.

To estimate SPGI’s valuation using FCF, divide management’s $6B guidance by ~304 million shares. We get ~$19.74 in FCF/share. Divide my $518.76 purchase price by ~$19.74 and the forward P/FCF is ~26.3.

If we estimate FY2025’s SBC will be ~$0.255B (~$0.247B in FY2024), the FY2025 FCF drops to ~$5.745B ($6B – ~$0.255B). Divide this by 304 million shares and we get ~$18.90 FCF/share. Divide $518.76 by ~$18.90 and the P/FCF is ~27.4.

Final Thoughts

SPGI was my 17th largest holding at the time of my 2024 year end review. I do not know its current ranking and can merely surmise that it is currently a top 15 holding.

Excluding the shares I acquired for a young investor, I now hold 550 SPGI shares (350 shares in a ‘Core’ account and 200 shares in a ‘Side’ account in the FFJ Portfolio). If market conditions deteriorate, SPGI’s share price could pull back to ~$470 or lower at which time I would consider adding to my exposure.

Market turbulence is inevitable and the ‘wheels are in motion’ to lead to further swift and dramatic sell-offs. Given my short-term outlook and SPGI’s current fair valuation, I will bide my time before adding to my exposure. In essence, I am trying to stack the odds of investment success by following the advice of highly successful investors who have experienced periods of market volatility.

Warren Buffett’s words of advice for investors, for example, are:

-

Predicting rain doesn’t count, building the ark does.

-

The years ahead will occasionally deliver major market declines — even panics — that will affect virtually all stocks. No one can tell you when these traumas will occur – not me, not Charlie, not economists, not the media.

-

In the business world, the rearview mirror is always clearer than the windshield.

-

Forecasts may tell you a great deal about the forecaster – they tell you nothing about the future.

In addition to heeding Buffett’s advice, I am also heeding Howard Marks’s advice (interview and presentation).

I wish you much success on your journey to financial freedom.

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long SPGI and MCO.

Disclaimer: I do not know your individual circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.