Often times, great companies suffer from temporary headwinds which may present buying opportunities. RTX Corporation (RTX) is a case in point.

In 2023, RTX disclosed that its Pratt & Whitney business segment was experiencing significant challenges resulting from microscopic contaminants in a metal used in part of the Geared Turbofan (GTF) engines that power Airbus’ popular A320neo jets.

Investors did not react kindly to this news. Throughout the second half of 2023 and the first few months of 2024, RTX’s share price was under pressure. I envisioned that it would cost billions to rectify the issue but nevertheless decided to add to my exposure and made the following purchases:

- July 25, 2023: 100 shares @ $85.67; and

- September 11, 2023: 100 shares @ ~$78.02.

I last reviewed RTX in this April 24 post at which time the most currently available information was for Q1. During Q1, RTX had:

- completed the sale of Raytheon’s cybersecurity business with gross proceeds of $1.3B;

- made progress on deleveraging the balance sheet, having paid down over $2B of debt since it initiated the Accelerated Share Repurchase in late 2023;

- a record $202B backlog and remained focused on meeting its customer commitments;

- communicated its plans to invest over $10B R&D, modernization and digital capabilities; and

- remained on track to return $36B – $37B of capital to shareholders from the date of the United Technologies/Raytheon merger through 2025.

Based on the currently available information, I deemed RTX’s valuation to be fair when I wrote that post.

I recently reviewed Lockheed Martin, one of RTX’s major competitors, in this July 24 post as it had just released its Q2 and YTD2024 results and concluded shares were too richly valued to add to my exposure. Now that RTX has released its Q2 and YTD2024 and revised FY2024 outlook on July 25, I revisit this holding.

Business Overview

RTX has 3 business segments (Collins Aerospace, Pratt & Whitney, and Raytheon). Investors unfamiliar with RTX should review the company’s website and Part 1 Item 1 within the 2023 Form 10-K.

Financials

Q2 and YTD2024 Results

In Q2, RTX continued to make progress on its critical initiatives.

The Geared Turbofan (GTF) fleet management plan (discussed in prior posts) remains on track with the financial and operational outlook consistent with prior comments.

RTX has inspected over 6,000 powder metal parts that are in the field across all programs; the associated fallout rate remains below the 1% threshold RTX had assumed and the findings are consistent with the assumptions that underpin RTX’s fleet management plan.

At RTX’s maintenance, repair, and operations (MRO) facilities, throughput of engines continues to improve. Overall capacity is expanding with the recent addition of 2 new MRO shops into the network.

Pratt & Whitney PW1100 MRO output increased 10% versus Q1 and ramp up is to continue in the second half of the year.

As it relates to the PW1100 fleet, the number of aircraft on ground due to the GTF issue has leveled out over the past few months and remain in line with expectations.

RTX has also reached support agreements with 20 of its customers, covering roughly 65% of the impacted fleet; the terms are in line with RTX’s assumptions.

I dispense with a review of Q2 and YTD2024 results as the results are presented in the Q2 Form 10-Q and in the July 25 Press Release and Earnings Presentation.

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

RTX’s’s OCF, CAPEX, and FCF over FY2014 – FY2023 is:

- OCF was (in B$) 7.34, 6.33, 3.88, 5.63, 6.32, 8.88, 3.61, 7.07, 7.17, and 7.88.

- CAPEX was (in B$) 2.30, 2.09, 2.09, 2.39, 2.30, 2.61, 1.97, 2.32, 2.78, and 3.17 .

- FCF was (in B$) 6.28, 5.46, 5.49, 3.29, 4.78, 6.51, 1.56, 5.10, 3.87, and 3.20.

In Q1 and Q2, RTX generated OCF of ~$0.342B and ~$2.7B for a YTD total of $3.042B.

CAPEX in Q1 and Q2 was ~$0.467B and ~$0.5B for a total of ~0.967B.

We get YTD2024 FCF of ~$2.07B by deducting YTD CAPEX from YTD OCF.

In addition to generating this FCF, RTX reported ~$1.29B of cash inflow from the sale of its cybersecurity business in Q1. This amount, however, is excluded in determining FCF generated from normal business operations.

Return On Invested Capital (ROIC)

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

RTX’s FY2013 – FY2023 ROIC (%) was 13.34, 16.53, 11.78, 9.45, 8.47, 7.79, (2.61), 4.70, 5.92, and 4.32 .

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company’s cost of capital will be lower than this level. RTX’s ROIC leaves a lot to be desired. Other factors which I have covered in prior posts, however, justify my investment in this company.

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

FY2024 Outlook

The following reflects updates to RTX’s FY2024 outlook.

- Organic Sales Growth ~8% – 9%, up from ~7% – 8%;

- Adjusted sales of $78.75B – $79.5B, up from $78.0B – $79.0B;

- Adjusted EPS of $5.35 – $5.45, up from $5.25 – $5.40; and

- Free Cash Flow (FCF) of ~$4.7B, down from ~$5.7B.

Risk Assessment

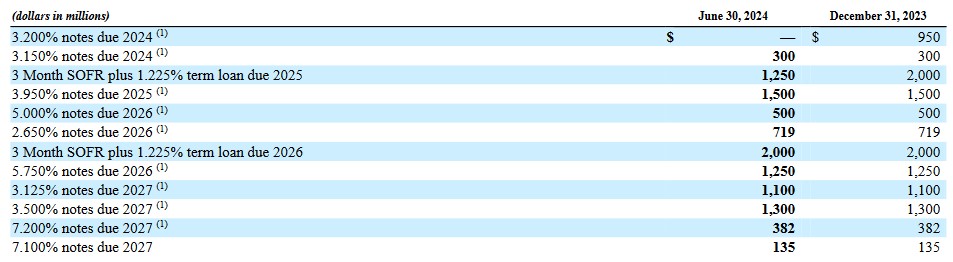

Details of RTX’s ‘Borrowings and Lines of Credit’ are included in the Q2 Form 10-Q commencing on page 13 of 76.

As of June 30, 2024, RTX had a revolving credit agreement with various banks permitting aggregate borrowings of up to $5.0B. As of June 30, 2024, there were no borrowings outstanding under this agreement. This agreement expires in August 2028.

The total long-term debt is $41.92B after $63 million of fair market value adjustments, (discounts)/premiums, and debt issuance costs.

The following partial list of RTX’s long-term debt reflects the debt maturing over the next few years. The current portion (due within 1 year) is $1.617B while the average maturity of RTX’s long-term debt as of June 30, 2024 is ~13 years.

Moody’s assigns a Baa1 rating to RTX’s senior unsecured domestic currency debt with a stable outlook.

S&P Global assigns a BBB+ to RTX Corp.’s senior unsecured notes with a negative outlook. This rating is equivalent to that assigned by Moody’s.

Both ratings are the top tier of the lower medium-grade category and define RTX as having an ADEQUATE capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity to meet its financial commitments.

Both ratings are investment grade and are acceptable for my purposes.

Dividend and Dividend Yield

The company’s website reflects RTX’s dividend history.

I am interested in an investment’s total potential shareholder return. Dividend metrics, therefore, are of little relevance in my investment decision making process.

RTX’s weighted average number of issued and outstanding shares in FY2010 – FY2023 (in millions rounded) is 923, 907, 907, 915, 912, 883, 826, 799, 810, 864, 1,358, 1,509, 1,486, and 1,435. The weighted average number of shares outstanding in Q2 2024 1,342.1.

The significant decline in the weighted average is explained in Note 17 in the Q2 2024 Form 10-Q.

On October 24, 2023, we entered into accelerated share repurchase (ASR) agreements with certain financial institution counterparties to repurchase shares of our common stock for an aggregate purchase price of $10 billion. Pursuant to the ASR agreements, we made aggregate payments of $10 billion on October 26, 2023, and received initial deliveries of approximately 108.4 million shares of our common stock at a price of $78.38 per share, which, on that date, represented approximately 85% of the shares expected to be repurchased. The total number of shares to be repurchased is subject to final settlement as discussed below. The aggregate purchase price was recorded as a reduction to Shareowners’ equity, consisting of an $8.5 billion increase in Treasury stock and a $1.5 billion decrease in Common stock.

The final number of shares to be repurchased will be based on the average of the daily volume-weighted average prices of our common stock during the term of the ASR agreements, less a discount and subject to adjustments pursuant to the terms and conditions of the ASR agreements. Upon final settlement of the ASR, under certain circumstances, each of the counterparties may be required to deliver additional shares of common stock, or we may be required to deliver shares of common stock or to make a cash payment to the counterparties, at our election. The final settlement of each transaction under the ASR agreements is scheduled to occur no later than the third quarter of 2024 and in each case may be accelerated at the option of the applicable counterparty.

Valuation

My January 24, 2024 post reflects RTX’s valuation at the time of prior posts.

When I wrote my April 24 post, shares were trading at ~$101.40 and there was no change to RTX’s $5.25 – $5.40 FY2024 adjusted diluted EPS outlook; the forward adjusted diluted PE range was ~18.8 – ~19.3.

RTX’s valuation using the current broker forward-adjusted diluted earnings estimates was:

- FY2024 – 23 brokers – mean of $5.39 and low/high of $5.17 – $5.55. Using the current mean, the forward adjusted diluted PE is ~18.8.

- FY2025 – 23 brokers – mean of $6.13 and low/high of $5.24 – $6.78. Using the current mean, the forward adjusted diluted PE is ~16.6.

- FY2026 – 15 brokers – mean of $6.83 and low/high of $5.38 – $7.40. Using the current mean, the forward adjusted diluted PE is ~14.8.

Looking at RTX’s valuation from a FCF perspective, it repurchased $10.283B of its shares by way of an ASR in late 2023, and therefore, I expected no significant share repurchases in FY2024.

The weighted average number of shares outstanding in Q1 2024 was 1,337.3 million versus 1,474.2 million in Q1 2023. Additional shares may be issued as part of the company’s stock based compensation arrangements so I estimated a weighted average of 1,340 million shares for FY2024.

Dividing RTX’s ~$5.7B FY2024 FCF outlook by 1,340 million shares gave us ~$4.25 FCF/share. Using the ~$101.40 share price and my ~$4.25 FCF/share estimate resulted in a forward P/FCF of ~23.9. RTX’s P/FCF in FY2014 – FY2023 was 13.81, 14.16, 19.81, 20.84, 12.46, 15.83, 16.99, 24.53, 26.62, and 15.84; United Technologies and Raytheon merged on April 3, 2020 so we can’t make a direct comparison between the current P/FCF and levels prior to the merger.

Shares now trade at ~$114 following the July 26 market close. RTX has also raised its FY2024 adjusted diluted EPS to $5.35 – $5.45 from $5.25 – $5.40. This gives us a forward adjusted diluted PE of ~20.9 – ~21.3.

RTX’s valuation using the current broker forward-adjusted diluted earnings estimates is:

- FY2024 – 20 brokers – mean of $5.43 and low/high of $5.19 – $5.54. Using the current mean, the forward adjusted diluted PE is ~21.

- FY2025 – 21 brokers – mean of $6.09 and low/high of $5.48 – $6.40. Using the current mean, the forward adjusted diluted PE is ~18.7.

- FY2026 – 17 brokers – mean of $6.83 and low/high of $6.02 – $7.40. Using the current mean, the forward adjusted diluted PE is ~16.7.

The weighted average number of shares outstanding in Q1 2024 was 1,342.1 million and 1,339.7 million for the first half of FY2024.

The ~$4.7B FY2024 FCF outlook has been lowered from the prior ~$5.7B outlook. Dividing $4.7B by ~1,340 million shares we get~$3.50 FCF/share. Divide the current ~$114 share price by ~$3.50 we get a ~32.6 forward P/FCF. Following the ~$1B reduction in the FY2024 FCF outlook, RTX’s valuation based on FCF is much less attractive than the forward P/FCF of ~23.9 I calculated just a few months ago.

Final Thoughts

I hold 941 RTX shares in 2 ‘Core’ accounts within the FFJ Portfolio. When I completed my 2024 Mid Year FFJ Portfolio Review, RTX was my 29th largest holding. This review was prepared using the June 28 closing share prices at which time RTX shares were trading at ~$102.

The current broker forward-adjusted diluted earnings estimates are not much different from when I wrote my April 24 post. We also need to consider that RTX’s FY2024 FCF outlook is $1B lower than the prior ~$5.7B outlook. RTX’s share price, however, is ~$12.60 higher than the ~$101.40 at the time of my last analysis.

In my recent LMT post I concluded shares were overvalued. My opinion about RTX is similar. Both might be great companies but I think it will be difficult to generate an attractive total annual rate of return if we purchase shares at the current valuation. The time to acquire RTX shares was months ago. Now, we seem to be experiencing irrational exuberance.

If RTX’s share price were to retrace to ~$100, the forward adjusted diluted PE would be ~18.3 – ~18.7 and the forward P/FCF would be ~28.6. RTX still appears to be richly valued based on P/FCF but, once again, we need to consider that FCF is being temporarily depressed because of the costly GTF issues.

Given my take on RTX’s valuation, I do not intend to immediately acquire additional shares.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long RTX and LMT.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.