Rollins (ROL) intends to double its revenue over the coming decade. This will require access to the capital markets. This now becomes possible with the assignment of investment-grade corporate credit ratings from Fitch and S&P Global.

I last reviewed Rollins (ROL) in this April 30, 2024 post at which time the most current financial information was for Q1 2024. With the recent release of ROL’s Q4 and FY2024 results and FY2025 guidance, I revisit this existing holding.

Business Overview

Through its family of brands, ROL provides pest control, termite services and wildlife removal to residential and commercial customers. Item 1 and 1-A in Part 1 in ROL’s FY2023 Form 10-K provide a comprehensive business overview.

ROL has strong focus on accelerating recurring organic growth. It does, however, grow through acquisitions. In FY2024, it completed 44 acquisitions (32 acquisitions and 12 franchise buybacks).

ROL’s largest competitors are Ecolab and Rentokil.

Financials

Q4 and FY2024 Results

Material related to ROL’s Q4 and FY2024 results is accessible here.

ROL’s current ratio (current assets minus current liabilities) is typically under 1. At FYE2024, current assets were $442.6 million and current liabilities were $645.2 million. Just under $181 million of the current liabilities, however, is unearned revenue. This represents the receipt of funds prior to the rendering of services.

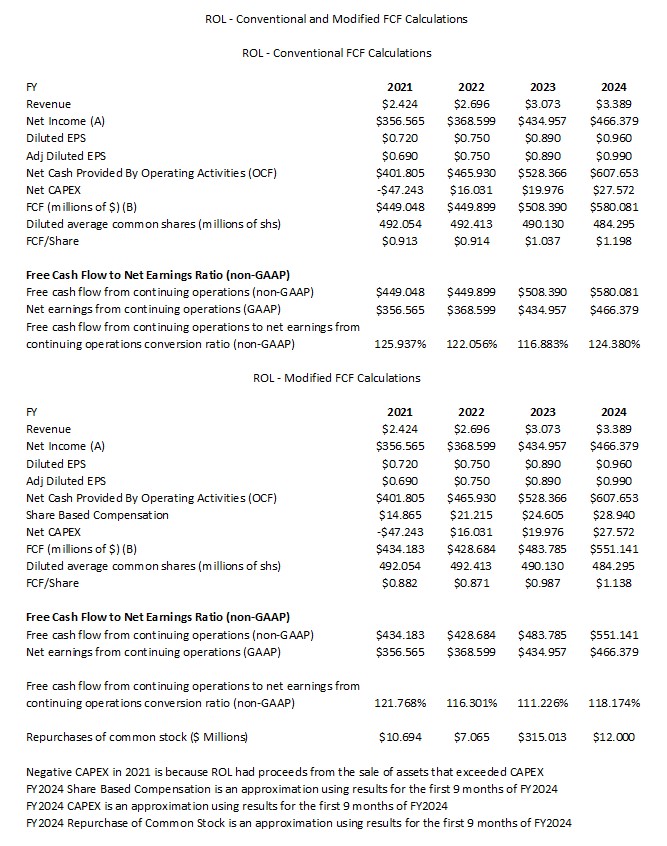

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

My recent Danaher (DHR) post explains my rationale for deducting share based compensation (SBC) when determining FCF.

The following table reflects ROL’s FCF using the conventional method and the modified method where I deduct SBC.

ROL’s CAPEX differs from my CAPEX values because I account for the proceeds from sale of assets and ROL does not.

The currently available FY2024 financial information provides insufficient information about SBC, CAPEX, and share repurchases. I, therefore, use YTD2024 results at the end of Q3 2024 and make minor adjustments.

When we deduct SBC in determining FCF under the modified calculation, we see that FCF continues to exceed earnings.

FY2025 Guidance

ROL is now starting to provide guidance.

Risk Assessment

In recent years, ROL’s senior executives ranks have been overhauled (see Management Team).

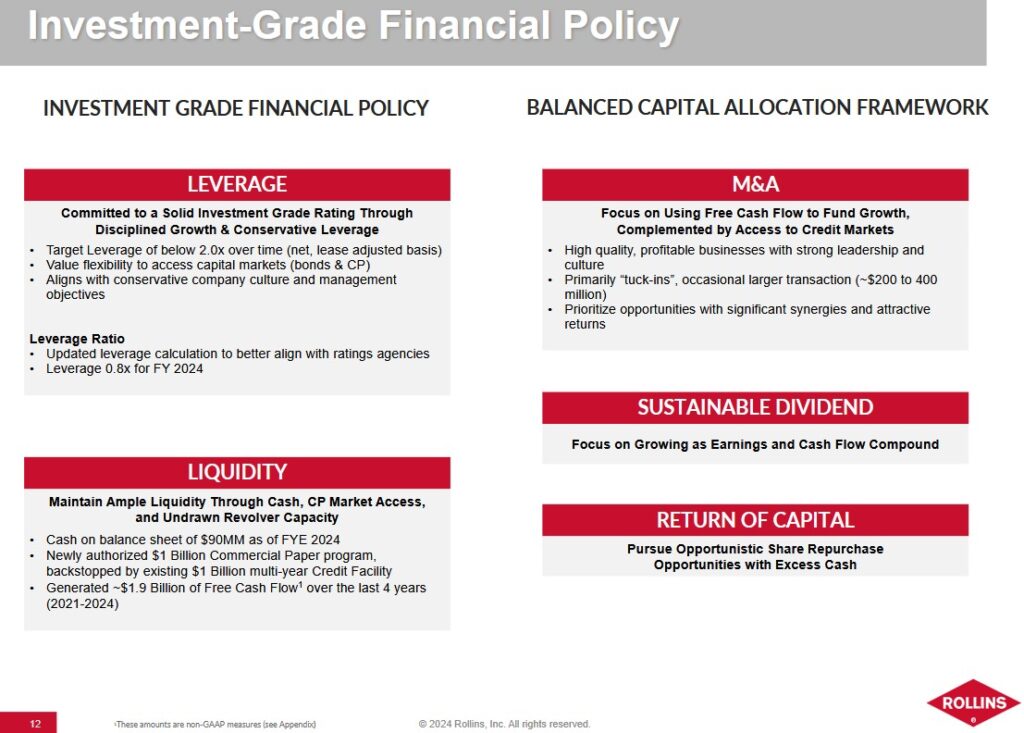

ROL continues to make progress in modernizing the company’s back office and capital structure. A key goal of this effort has been to ensure access to the most efficient capital to further enable a balanced and disciplined approach to capital allocation.

One of the top priorities has been to achieve investment-grade ratings. Just recently, Fitch and S&P Global have announced public credit ratings for ROL.

- Fitch: BBB+

- S&P Global: BBB

These ratings will assist ROL in its growth efforts while using the most cost-efficient capital.

Fitch’s rating is the top tier of the lower-medium grade investment grade category. S&P assigns a rating that is one tier lower. Bother ratings define ROL as having an adequate capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity for ROL to meet its financial commitments.

ROL’s Board approval of a $1B commercial paper program backstopped by the company’s existing $1B revolving credit facility will help provide flexibility and more efficient shorter-term liquidity options.

On the Q4 2024 earnings call, management states a commitment to maintaining a strong investment-grade rating with leverage well under 2x supported by healthy cash flow generation and disciplined capital allocation.

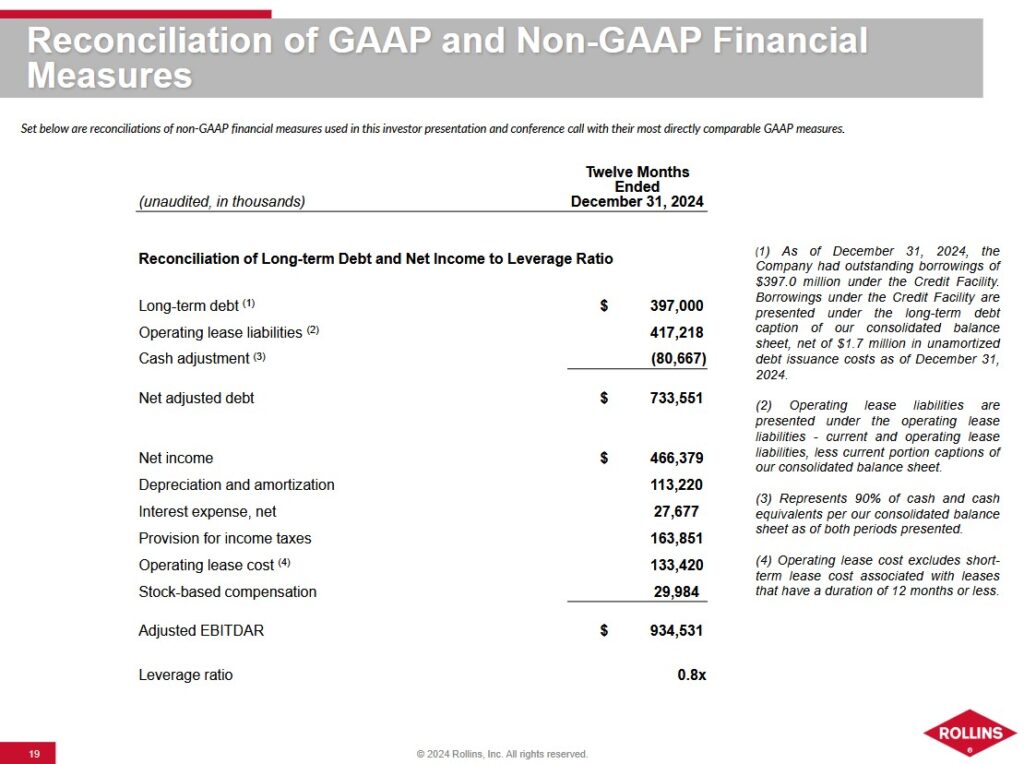

The definition of leverage has also been amended to better align with the rating agencies. Going forward, ROL’s leverage ratio is an assessment of overall liquidity, financial flexibility, and leverage and is to be calculated by dividing adjusted net debt by adjusted EBITDAR.

- Adjusted net debt is calculated by adding operating lease liabilities to total long-term debt less a cash adjustment of 90% of cash and cash equivalents.

- Adjusted EBITDAR is calculated by adding back to net income depreciation and amortization, interest expense, net, provision for income taxes, operating lease cost, and stock-based compensation expense.

Dividends, Share Repurchases, and Stock Splits

Dividend and Dividend Yield

ROL’s dividend history is accessible here.

Share Repurchases

Reinvesting in the company (including mergers and acquisitions) and dividend distributions currently rank in priority to share repurchases from a capital allocation perspective.

Stock Splits

ROL has had stock splits over the years with the most recent being a 3-for-2 stock split in late 2020.

Valuation

The high amortization expense related to multiple acquisitions makes it impractical to value ROL using Earnings per Share (EPS). Depreciation and Amortization are significant components of the ‘Adjustments to reconcile net income to net cash provided by operating activities’ in the Consolidated Statement of Cash Flows.

ROL’s current forward adjusted diluted PE levels using the adjusted diluted EPS broker estimates and the current ~$51.20 share price are:

- FY2025 – 12 brokers – mean of $1.11 and low/high of $1.08 – $1.14. Using the mean, the forward adjusted diluted PE is ~46.

- FY2026 – 12 brokers – mean of $1.24 and low/high of $1.19 – $1.31. Using the mean, the forward adjusted diluted PE is ~41.3.

- FY2027 – 8 brokers – mean of $1.39 and low/high of $1.30 – $1.46. Using the mean, the forward adjusted diluted PE is ~36.8.

Minor revisions to these estimates could occur over the next several days given the February 12 earnings release.

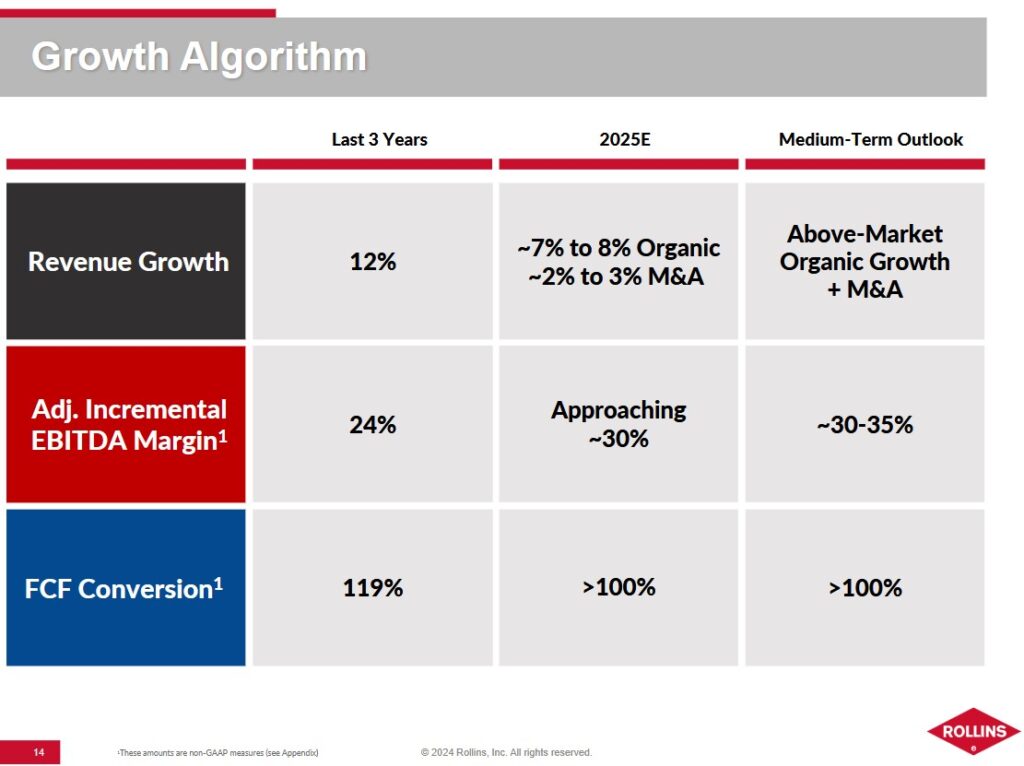

ROL consistently generates FCF exceeding EPS and the outlook is for this to continue. Using modified FCF calculations where we deduct SBC, I estimate that the FCF conversion ratio will be at least 1.11. The variance between diluted EPS and adjusted diluted EPS is historically slim. I, therefore, estimate FY2025’s FCF/share as being ~$1.23 ($1.11 x 1.11).

If we divide $51.20 by $1.23, the forward P/FCF is ~41.6. This level is relatively similar to the levels calculated in prior posts.

I continue to think a fair value is closer to the low $40s. At ~$42, the P/FCF ($42/$1.23) is ~32.5.

Final Thoughts

On June 10, 2021, I initiated a 500 share position @ ~$33.14 in one of the ‘Core’ accounts in the FFJ Portfolio. I subsequently acquired another 100 shares on September 7, 2023 @ ~$34.86 in the same account. With the reinvestment of the dividend income, my exposure is currently 612 shares.

ROL was not a top 30 holding when I completed my 2024 Year End FFJ Portfolio Review and it is unlikely to ever become a top 30 holding. I intend to merely increase my exposure through the automatic reinvestment of dividend income.

Looking at ROL from a P/E perspective will lead an investor to view it as being grossly overvalued. It is, however, preferable that we look at ROL from a FCF perspective. Furthermore, we need to consider that ROL is a leader in the highly fragmented pest control industry. Management also plans to double the company’s revenue over the coming decade. If it continues to generate an Operating Margin in the mid to upper teens as it has over the past several years, investors should be aptly rewarded.

The following are some additional considerations.

- The pest control business is relatively steady;

- ROL focuses heavily on efficiency and cost control;

- The FCF conversion ratio is consistently above 100%;

- Management quality has improved considerably;

- The level of financial reporting continues to improve;

- Investment-grade corporate credit ratings now provide ROL with an important access point to the capital markets; and

- More than 80% of business is recurring.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ROL.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.